14. Note that the Black-Scholes formula gives the price of European call c given the time...

14. Note that the Black-Scholes formula gives the price of European call c given the time to expiration T, the strike price K, the stock’s spot price S0, the stock’s volatility σ, and the risk-free rate of return r : c = c(T, K, S0, σ, r). All the variables but one are “observable,” because an investor can quickly observe T, K, S0, r. The stock volatility, however, is not observable. Rather it relies on the choice of models the investor uses. The price of the option, c, if traded, is observable. So we can flip the problem around. Given observables T, K, S0, r and c, what volatility σ should the stock have in order for the Black-Scholes formula to be correct. This is called the implied volatility, σBS. Some calculus, shows that σBS exists and is unique.

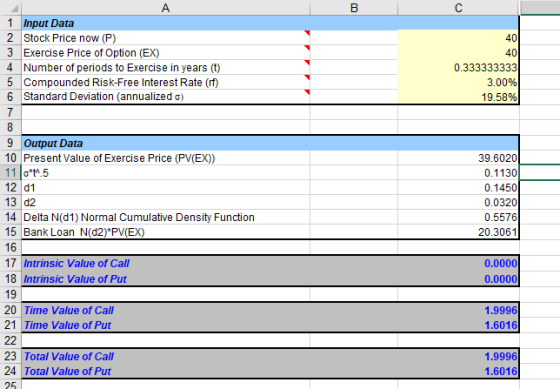

The current spot price is $40, the expected rate of return of the stock is 8%, the risk-free rate is 3%. A European call option on the stock with strike price $40 expiring in 4 months is currently trading for $2. With trial and error, find a one-percentage point range which contains the implied volatility. So your answer should be of the form “14% ≤ σBS ≤ 15%”

Homework Answers

19% ≤ σBS ≤ 20%

Add Answer to:

14. Note that the Black-Scholes formula gives the price of

European call c given the time...

Problem 1: - Using the Black/Scholes formula and put/call parity, value a European put option on...

Problem 1: - Using the Black/Scholes formula and put/call parity, value a European put option on the equity in Amgen, which has the following characteristics. Expiration: Current stock price of Amgen: Strike Price: Volatility of Amgen Stock price: Risk-free rate (continuously compounded): Dividends: 3 months (i.e., 60 trade days) $53.00 $50.00 26% per year 2% None If the market price of the Amgen put is actually $2.00 per share, is the above estimate of volatility higher or lower than the...

Problem 1: - Using the Black/Scholes formula and put/call parity, value a European put option on the equity in Amgen, which has the following characteristics. Expiration: Current stock price of Amgen: Strike Price: Volatility of Amgen Stock price: Risk-free rate (continuously compounded): Dividends: 3 months (i.e., 60 trade days) $53.00 $50.00 26% per year 2% None If the market price of the Amgen put is actually $2.00 per share, is the above estimate of volatility higher or lower than the...

Calculate the Black and Scholes price of a European Call option, with a strike of $120...

Calculate the Black and Scholes price of a European Call option, with a strike of $120 and a time to expiry of 6 months. The underlying currentely trades at $100 and has a (future) volatility of 23% p.a. Assume a risk free rate of 1% p.a. 0.07 0.08 O 1.20 O 1.24

Calculate the Black and Scholes price of a European Call option, with a strike of $120 and a time to expiry of 6 months. The underlying currentely trades at $100 and has a (future) volatility of 23% p.a. Assume a risk free rate of 1% p.a. 0.07 0.08 O 1.20 O 1.24

What is the price of a European call option according to the Black-Sholes formula on a...

What is the price of a European call option according to the Black-Sholes formula on a non-dividend-paying stock when the stock price is $45, the strike price is $50, the risk-free interest rate is 12% per annum, the volatility is 25% per annum, and the time to maturity is six months? Show your work in details.

(a) State the Black-Scholes formulas for the prices at time 0 of a European call and put options on a non-dividend-paying stock ABC

2. (a) State the Black-Scholes formulas for the prices at time 0 of a European call and put options on a non-dividend-paying stock ABC.(b) Consider an option on a non-dividend paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 20% per annum, and the time to maturity is 5 months. What is the price of the option if it is a European call?

In this question we assume the Black-Scholes model. We denote interest rate by r, drift rate...

In this question we assume the Black-Scholes model. We denote interest rate by r, drift rate pi and volatility by o. A European power put option is an option with the payoff function below, Ka – rº, ha if x <K, 0, if x > K, for some a > 0. In particular, it will be a standard European put option when a = 1. (a) Derive the pricing formula for the time t, 0 <t< T, price of a...

In this question we assume the Black-Scholes model. We denote interest rate by r, drift rate pi and volatility by o. A European power put option is an option with the payoff function below, Ka – rº, ha if x <K, 0, if x > K, for some a > 0. In particular, it will be a standard European put option when a = 1. (a) Derive the pricing formula for the time t, 0 <t< T, price of a...

5. Use the Black-Scholes methodology to find, by direct calculation, an explicit formula for the fair...

5. Use the Black-Scholes methodology to find, by direct calculation, an explicit formula for the fair price (at time t) of the following contingent claims (European type options). The price of the underlying (stock) at time t is denoted by S(0); the time of maturity by T; the risk-free interest rate by r; the volatility of the underlying by o (a) The stock or nothing call option: This is a claim that will pay exactly the price of the underlying...

5. Use the Black-Scholes methodology to find, by direct calculation, an explicit formula for the fair price (at time t) of the following contingent claims (European type options). The price of the underlying (stock) at time t is denoted by S(0); the time of maturity by T; the risk-free interest rate by r; the volatility of the underlying by o (a) The stock or nothing call option: This is a claim that will pay exactly the price of the underlying...

Use the Black-Scholes formula to price a call option for a stock whose share price today...

Use the Black-Scholes formula to price a call option for a stock whose share price today is $16 when the interest rate is 4%, the maturity date is 6 month, the strike price is $17.5 and the volatility is 20%. Find the price of the same option half way to maturity if the share price at that time is $17.

In the use of the Black-Scholes option valuation model to determine the value of a European...

In the use of the Black-Scholes option valuation model to determine the value of a European call option, which one of the following relationships is NOT correct? A. An increase in the risk-free rate increases the value of the European call option. B. An increase in the exercise price of the European call option increases the value of the option. C. An increase in the price of the underlying stock increases the value of the European call option. D. An...

In referring to the Black-Scholes formula for pricing a European put option on a dividend paying...

In referring to the Black-Scholes formula for pricing a European put option on a dividend paying stock, which of the following statements are true? I. The put price increases as the strike decreases II. The put price increases as volatility increases III. The put price increases as the dividend decreases a) I only c) I and II e) I, II and III b) Il only d) II and III

In referring to the Black-Scholes formula for pricing a European put option on a dividend paying stock, which of the following statements are true? I. The put price increases as the strike decreases II. The put price increases as volatility increases III. The put price increases as the dividend decreases a) I only c) I and II e) I, II and III b) Il only d) II and III

The price of the underlying asset is $290.48 Case: Today is April 30th, 2020, and a...

The price of the underlying asset is

$290.48

Case: Today is April 30th, 2020, and a trader sold 100,000 European call options on the SPY ETF with an exercise price of $310, expiring on June 30, 2020. The trader was able to write these options for $3.80. Additional Information: Suppose that the SPY obeys to a GBM process under risk neutral probability, such that (1) Sx = Sex exp ((- - -)+0B4) where Sc is the SPY price at time...

The price of the underlying asset is

$290.48

Case: Today is April 30th, 2020, and a trader sold 100,000 European call options on the SPY ETF with an exercise price of $310, expiring on June 30, 2020. The trader was able to write these options for $3.80. Additional Information: Suppose that the SPY obeys to a GBM process under risk neutral probability, such that (1) Sx = Sex exp ((- - -)+0B4) where Sc is the SPY price at time...

Problem 1: - Using the Black/Scholes formula and put/call parity, value a European put option on the equity in Amgen, which has the following characteristics. Expiration: Current stock price of Amgen: Strike Price: Volatility of Amgen Stock price: Risk-free rate (continuously compounded): Dividends: 3 months (i.e., 60 trade days) $53.00 $50.00 26% per year 2% None If the market price of the Amgen put is actually $2.00 per share, is the above estimate of volatility higher or lower than the...

Problem 1: - Using the Black/Scholes formula and put/call parity, value a European put option on the equity in Amgen, which has the following characteristics. Expiration: Current stock price of Amgen: Strike Price: Volatility of Amgen Stock price: Risk-free rate (continuously compounded): Dividends: 3 months (i.e., 60 trade days) $53.00 $50.00 26% per year 2% None If the market price of the Amgen put is actually $2.00 per share, is the above estimate of volatility higher or lower than the...

Calculate the Black and Scholes price of a European Call option, with a strike of $120 and a time to expiry of 6 months. The underlying currentely trades at $100 and has a (future) volatility of 23% p.a. Assume a risk free rate of 1% p.a. 0.07 0.08 O 1.20 O 1.24

Calculate the Black and Scholes price of a European Call option, with a strike of $120 and a time to expiry of 6 months. The underlying currentely trades at $100 and has a (future) volatility of 23% p.a. Assume a risk free rate of 1% p.a. 0.07 0.08 O 1.20 O 1.24

In this question we assume the Black-Scholes model. We denote interest rate by r, drift rate pi and volatility by o. A European power put option is an option with the payoff function below, Ka – rº, ha if x <K, 0, if x > K, for some a > 0. In particular, it will be a standard European put option when a = 1. (a) Derive the pricing formula for the time t, 0 <t< T, price of a...

In this question we assume the Black-Scholes model. We denote interest rate by r, drift rate pi and volatility by o. A European power put option is an option with the payoff function below, Ka – rº, ha if x <K, 0, if x > K, for some a > 0. In particular, it will be a standard European put option when a = 1. (a) Derive the pricing formula for the time t, 0 <t< T, price of a...

5. Use the Black-Scholes methodology to find, by direct calculation, an explicit formula for the fair price (at time t) of the following contingent claims (European type options). The price of the underlying (stock) at time t is denoted by S(0); the time of maturity by T; the risk-free interest rate by r; the volatility of the underlying by o (a) The stock or nothing call option: This is a claim that will pay exactly the price of the underlying...

5. Use the Black-Scholes methodology to find, by direct calculation, an explicit formula for the fair price (at time t) of the following contingent claims (European type options). The price of the underlying (stock) at time t is denoted by S(0); the time of maturity by T; the risk-free interest rate by r; the volatility of the underlying by o (a) The stock or nothing call option: This is a claim that will pay exactly the price of the underlying...

In referring to the Black-Scholes formula for pricing a European put option on a dividend paying stock, which of the following statements are true? I. The put price increases as the strike decreases II. The put price increases as volatility increases III. The put price increases as the dividend decreases a) I only c) I and II e) I, II and III b) Il only d) II and III

In referring to the Black-Scholes formula for pricing a European put option on a dividend paying stock, which of the following statements are true? I. The put price increases as the strike decreases II. The put price increases as volatility increases III. The put price increases as the dividend decreases a) I only c) I and II e) I, II and III b) Il only d) II and III

The price of the underlying asset is

$290.48

Case: Today is April 30th, 2020, and a trader sold 100,000 European call options on the SPY ETF with an exercise price of $310, expiring on June 30, 2020. The trader was able to write these options for $3.80. Additional Information: Suppose that the SPY obeys to a GBM process under risk neutral probability, such that (1) Sx = Sex exp ((- - -)+0B4) where Sc is the SPY price at time...

The price of the underlying asset is

$290.48

Case: Today is April 30th, 2020, and a trader sold 100,000 European call options on the SPY ETF with an exercise price of $310, expiring on June 30, 2020. The trader was able to write these options for $3.80. Additional Information: Suppose that the SPY obeys to a GBM process under risk neutral probability, such that (1) Sx = Sex exp ((- - -)+0B4) where Sc is the SPY price at time...

Most questions answered within 3 hours.

-

Dopamine Hydrochloride: draw the structure And Show the

functional groups in different colors and label the...

asked 4 minutes ago -

A rope supports a 10 kg dumbbell hanging from it. What is the

tension in the...

asked 3 minutes ago -

Suppose that you know that in the population of full-time

employees in the United States, the...

asked 11 minutes ago -

This experiment was designed originally to sample various meat and carcass quality

aspects of Ontario pigs...

asked 12 minutes ago -

) Raw materials are studied for contamination. Suppose that

the number of particles of contamination per...

asked 26 minutes ago -

After running a regression analysis we calculated an F test and

the significance level was 0.15....

asked 21 minutes ago -

----Can someone please help me solve this one using JAVA

----I thank you in advance

Create...

asked 26 minutes ago -

1. What force primarily attracts the potassium ion to

the nitrate ion?

a. London forces...

asked 28 minutes ago -

What are the negative effects of abruptly stopping the use of

all fossil fuels? Give at...

asked 35 minutes ago -

Given that many conflict are the result of different parties having

different interests, is it possible...

asked 40 minutes ago -

A 750 g block can slide uniformly along the horizontal track

when a string attached to...

asked 43 minutes ago -

In 2017, Juan entered into a contract to write a book. The

publisher advanced Juan $50,000,...

asked 56 minutes ago