QQQ corporation has 1000 of earnings and profits. It makes distribution to its shareholder of 2000....

QQQ corporation has 1000 of earnings and profits. It makes distribution to its shareholder of 2000. The shareholders basis is 200. How much of the distribution is taxable as a dividend?

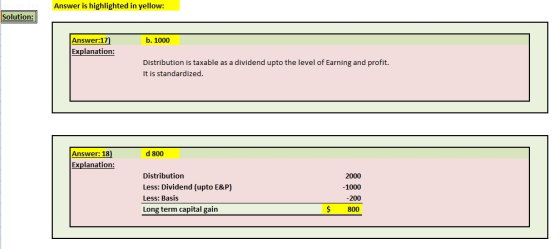

17 a. 2000 b. 1000 c. 0 d. 800 e. 200

18 How much of the dividends a long term capital gain?

a 2000 b 1000 c 0 d 800 e 200

Homework Answers

Hi

Let me know in case you face any issue:

Add Answer to:

QQQ corporation has 1000 of earnings and profits. It makes

distribution to its shareholder of 2000....

s 1. QQQ Corporation has $1,000 of Earnings and Profits. It makes a distribution to shareholder...

s 1. QQQ Corporation has $1,000 of Earnings and Profits. It makes a distribution to shareholder of $2,000. The shareholder's basis in QQQ is $200. How much of the distribution is taxable as a dividend? A. $2,000 B. $1,000 C. Zero D. $800 E. $200

s 1. QQQ Corporation has $1,000 of Earnings and Profits. It makes a distribution to shareholder of $2,000. The shareholder's basis in QQQ is $200. How much of the distribution is taxable as a dividend? A. $2,000 B. $1,000 C. Zero D. $800 E. $200

Susan is the sole shareholder in Square, Inc. This year, Square, Inc. has accumulated earnings and...

Susan is the sole shareholder in Square, Inc. This year, Square, Inc. has accumulated earnings and profits of $25,000. Susan's basis for the stock she owns in the company is $7,000. Square, Inc makes a distribution of $40,000 to Susan. How much of this distribution is taxable to Susan as dividends? How much of this distribution is taxable to Susan as a capital gain? 2. On November 20, 2018, Dylan purchased stock in Tech, Inc. for $10,000. On October 31,...

Jane is the sole shareholder of Buttons, Inc. Buttons has accumulated earnings and profits (E &...

Jane is the sole shareholder of Buttons, Inc. Buttons has accumulated earnings and profits (E & P) of $65,000 at the beginning of the current year. The current E & P is $35,000. Buttons pays out a property distribution to Jane during the current year with an FMV of $150,000 and an adjusted basis of $130,000. How much is taxable dividend to Jane? a. $35,000 b. $100,000 c. $120,000 d. $150,000 Please show your work.

3. Purple Corporation makes a property distribution to its sole shareholder, Paul. The property distributed is...

3. Purple Corporation makes a property distribution to its sole shareholder, Paul. The property distributed is a house (fair market value of $189,000; basis of $154,000) Before considering the consequences of the distribution, Purple's current E & P is $35,000 and its accumulated E & P is $140,000. Purple makes no other distributions during the current year. What is Purple's taxable gain on the distribution of the house, if any?

3. Purple Corporation makes a property distribution to its sole shareholder, Paul. The property distributed is a house (fair market value of $189,000; basis of $154,000) Before considering the consequences of the distribution, Purple's current E & P is $35,000 and its accumulated E & P is $140,000. Purple makes no other distributions during the current year. What is Purple's taxable gain on the distribution of the house, if any?

Nancy is the sole shareholder of Indigo Corporation. The basis of her stock is $90,000. Indigo...

Nancy is the sole shareholder of Indigo Corporation. The basis of her stock is $90,000. Indigo distributes $230,000 to Nancy in 20X8. Earnings and profits for Indigo are $60,000. What are the tax consequences of the distribution to Nancy? Taxable Dividend Decrease in Stock Basis Capital Gain a. $90,000 $80,000 $60,000 b. $80,000 $90,000 $60,000 C. $90,000 $60,000 $80,000 d. $60,000 $90,000 $80,000 e. None of the above

Z Inc. distributed a parcel of land to Zeke, the sole shareholder. The land had a...

Z Inc. distributed a parcel of land to Zeke, the sole shareholder. The land had a fair value of $30,000 and a basis of $50,000. Prior to considering this distribution, Z had accumulated E&P of $0 and current earnings and profits of $20,000. How much of the distribution will be a taxable dividend? What is the total remaining E&P after this distribution?

Trolley Corp., which had earnings and profits of $500,000, made a non-liquidating distribution of property to...

Trolley Corp., which had earnings and profits of $500,000, made a non-liquidating distribution of property to its shareholders in Year 1 as a dividend in kind. This property, which had an adjusted basis of $20,000 and a fair market value of $30,000 at the date of distribution, did not constitute assets used in the active conduct of Trolley’s business. How much gain did Trolley recognize on this distribution?

1. Corporation P files a consolidated return with Corporation S. In preparing a consolidated return, their ...

1. Corporation P files a consolidated return with Corporation S. In preparing a consolidated return, their accountant finds the following: P S Separate taxable income (loss) $500,000 ($200,000) Capital gain (loss) ($25,000) $50,000 Charitable contributions $20,000 $10,000 Dividend from S $10,000 What is the consolidated return taxable income? a. $365,000 b. $295,000 c. $280,000 d. $315,000 2. Jude received a $25,000 distribution from BC Corporation that the corporation identified as $15,000 dividend and $10,000 return of capital. What effect does...

5. mike is the sole shareholder of Led Corporation. The basis of his stock is $65,000....

5. mike is the sole shareholder of Led Corporation. The basis of his stock is $65,000. mike distributes $150,000 to Rob in 20X1. Eamings and profits for mike are $45,000. What are the tax consequences of the distribution? Taxable Dividend a. $ 40,000 b. $ 45,000 c.$ 45,000 d. $150,000 e. all are incorrect

XYZ Corporation distributed to its shareholders a total of $30,000 in cash plus property that had...

XYZ Corporation distributed to its shareholders a total of $30,000 in cash plus property that had a fair market value of $80,000 and a basis of $60,000. The corporation’s earnings and profits were $100,000 on the last day of the year in which the distribution was made after taking into effect the impact on the corporation’s earning and profits of the gain recognized on the distribution (but before reducing earnings and profits by the fair market value of the distribution)....

s 1. QQQ Corporation has $1,000 of Earnings and Profits. It makes a distribution to shareholder of $2,000. The shareholder's basis in QQQ is $200. How much of the distribution is taxable as a dividend? A. $2,000 B. $1,000 C. Zero D. $800 E. $200

s 1. QQQ Corporation has $1,000 of Earnings and Profits. It makes a distribution to shareholder of $2,000. The shareholder's basis in QQQ is $200. How much of the distribution is taxable as a dividend? A. $2,000 B. $1,000 C. Zero D. $800 E. $200

3. Purple Corporation makes a property distribution to its sole shareholder, Paul. The property distributed is a house (fair market value of $189,000; basis of $154,000) Before considering the consequences of the distribution, Purple's current E & P is $35,000 and its accumulated E & P is $140,000. Purple makes no other distributions during the current year. What is Purple's taxable gain on the distribution of the house, if any?

3. Purple Corporation makes a property distribution to its sole shareholder, Paul. The property distributed is a house (fair market value of $189,000; basis of $154,000) Before considering the consequences of the distribution, Purple's current E & P is $35,000 and its accumulated E & P is $140,000. Purple makes no other distributions during the current year. What is Purple's taxable gain on the distribution of the house, if any?

Most questions answered within 3 hours.

-

Our ability to see distinct edges as well as our errors in

contrast perceptions (e.g., seeing...

asked 19 seconds from now -

you want to measure the gravitational acceleration at your

location. since g does not vary significantly...

asked 13 minutes ago -

Aside from commercial tools that are specifically geared toward

TAR/PC( Technology-Assisted Review), are there potential

alternative...

asked 15 minutes ago -

A woman expends 94 kJ of energy in walking a kilometer. The

energy is supplied by...

asked 8 minutes ago -

the period of a pendulum on earth is 5 seconds. what will be the

period of...

asked 31 minutes ago -

The

act of turning media against itself, such as flash mobs and

billboard is called

a....

asked 27 minutes ago -

A set of length measurements are obtained with the values 165.6

± 0.3, 165.1± 0.4,166.4± 1.0,...

asked 28 minutes ago -

Vertical Analysis

Income statement information for Einsworth Corporation

follows:

Sales

$237,000

Cost of goods sold

78,210...

asked 35 minutes ago -

A simple random sample was taken to test the claim that the

population mean is no...

asked 30 minutes ago -

Overview

JAVA LANGUAGE PROBLEM:

The owner of a restaurant wants a program to manage online

orders...

asked 35 minutes ago -

1- What is “progressive production?”

2- Where did the assembly line originate? (Name the industry)

3....

asked 33 minutes ago -

NPV

Project L costs $60,000 it’s expected cash inflows are $13,000

per year for 10 years,...

asked 38 minutes ago