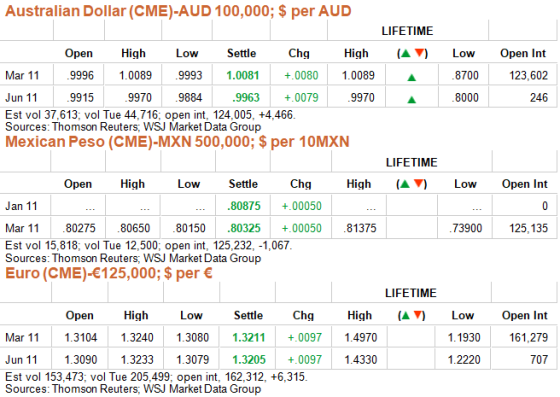

Use the accompanying chart of currency futures market activity, for Wednesday, December 30, 2010 to answer this question. Of the seven currency futures shown, using the March, 2011 contracts only, assuming equal volatility for each currency, which one had the highest fairly priced dollar value for its at the money 90 day calls?

Currency Futures Trading Summary for Thursday, December 30,

2010

Homework Answers

Total Value of the Option = Intrinsic Value of the option + Time Premium of the Option

Apart from this the sensitivities of the Options can viewed from the Option Greeks like Delta, Gamma, Theta (Time decay),

Vega (Volatility), RHO (Interest Rate)

In the given question, Theta and Vega assumed to be remains the same then when price increases then the value of Option increases by its Delta and when price falls it falls by same Delta.

By looking at the price table of different currencies pair the least movement observed is in CAD that too a downward movement and hence a least change in value of Option. Since Call options is mentioned hence Call options of CAD would be at Fair Value.

Add Answer to:

Use the accompanying chart of currency futures market activity,

for Wednesday, December 30, 2010 to answer...

Laura Cervantes. Laura Cervantes is a currency speculator and she sells eight June futures contracts for...

Laura Cervantes. Laura Cervantes is a currency speculator and she sells eight June futures contracts for 500,000 pesos at the closing price quoted here: a. What is the value of her position at maturity if the ending spot rate is $0.12007/Ps? b. What is the value of her position at maturity if the ending spot rate is $0.09802/Ps? c. What is the value of her position at maturity if the ending spot rate is $0.11006/Ps? Data Table - a. What...

Laura Cervantes. Laura Cervantes is a currency speculator and she sells eight June futures contracts for 500,000 pesos at the closing price quoted here: a. What is the value of her position at maturity if the ending spot rate is $0.12007/Ps? b. What is the value of her position at maturity if the ending spot rate is $0.09802/Ps? c. What is the value of her position at maturity if the ending spot rate is $0.11006/Ps? Data Table - a. What...

Refer to Table 10-6 Price quotes are stated in 1/64ths a. How many ExxonMobil October 2016...

Refer to Table 10-6 Price quotes are stated in 1/64ths a. How many ExxonMobil October 2016 $90.00 put options were outstanding at the open of trading on August 3, 2016? b. What was the closing price of a 10-year Treasury note December 13300 futures call option on August 3, 2016? c. What was the closing and dollar price of a December 2160 call option on the S&P 500 Stock Index futures contract on August 3. 2016? d. What was the...

Refer to Table 10-6 Price quotes are stated in 1/64ths a. How many ExxonMobil October 2016 $90.00 put options were outstanding at the open of trading on August 3, 2016? b. What was the closing price of a 10-year Treasury note December 13300 futures call option on August 3, 2016? c. What was the closing and dollar price of a December 2160 call option on the S&P 500 Stock Index futures contract on August 3. 2016? d. What was the...

Suppose you purchase a July 2011 soybean oil futures contract on March 29, 2011, at the...

Suppose you purchase a July 2011 soybean oil futures contract on

March 29, 2011, at the last price of the day. Use Table 23.1

What will your profit or loss be if soybean oil prices turn out

to be $0.4652 per pound at expiration

Suppose you sell eight May 2011 silver futures contracts on

March 29, 2011, at the last price of the day. Use Table 23.1

What will your profit or loss be if silver prices turn...

Suppose you purchase a July 2011 soybean oil futures contract on

March 29, 2011, at the last price of the day. Use Table 23.1

What will your profit or loss be if soybean oil prices turn out

to be $0.4652 per pound at expiration

Suppose you sell eight May 2011 silver futures contracts on

March 29, 2011, at the last price of the day. Use Table 23.1

What will your profit or loss be if silver prices turn...

Suppose you sell six August 2017 gold futures contracts on this day, at the last price...

Suppose you sell six August 2017 gold futures contracts on this day, at the last price of the day. Use Table 23.1 a. What will your profit or loss be if gold prices turn out to be $1,249.70 per ounce at expiration? (Do not round intermediate calculations. Enter your answer as a positive value rounded to the nearest whole number, e.g., 32.) b. What will your profit or loss be if gold prices are $1,235.90 per ounce at expiration? (Do...

Suppose you sell six August 2017 gold futures contracts on this day, at the last price of the day. Use Table 23.1 a. What will your profit or loss be if gold prices turn out to be $1,249.70 per ounce at expiration? (Do not round intermediate calculations. Enter your answer as a positive value rounded to the nearest whole number, e.g., 32.) b. What will your profit or loss be if gold prices are $1,235.90 per ounce at expiration? (Do...

Suppose you purchase a March 2017 oats futures contract on this day at the last price...

Suppose you purchase a March 2017 oats futures contract on this day at the last price of the day. Use Table 23.1 What will your profit or loss be if oats prices turn out to be $2.4713 per bushel at expiration? (Do not round intermediate calculations. Enter your answer as a positive value and round your answer to 2 decimal places, e.g., 32.16.) Loss TABLE 23.1 Sample Wall Street Journal Futures Price Quotations Chg Open interest -0.0125 -0.0130 6 72...

Suppose you purchase a March 2017 oats futures contract on this day at the last price of the day. Use Table 23.1 What will your profit or loss be if oats prices turn out to be $2.4713 per bushel at expiration? (Do not round intermediate calculations. Enter your answer as a positive value and round your answer to 2 decimal places, e.g., 32.16.) Loss TABLE 23.1 Sample Wall Street Journal Futures Price Quotations Chg Open interest -0.0125 -0.0130 6 72...

Suppose today is February 10, 2017, and your firm produces breakfast cereal and needs 170,000 bushels...

Suppose today is February 10, 2017, and your firm produces breakfast cereal and needs 170,000 bushels of corn in May 2017 for an upcoming promotion. You would like to lock in your costs today because you are concerned that corn prices might rise between now and May. Use Table 23.1 a. What total cost would you effectively be locking in based on the closing price of the day? (Round your answer to the nearest whole number, e.g., 32.) b. Suppose...

Suppose today is February 10, 2017, and your firm produces breakfast cereal and needs 170,000 bushels of corn in May 2017 for an upcoming promotion. You would like to lock in your costs today because you are concerned that corn prices might rise between now and May. Use Table 23.1 a. What total cost would you effectively be locking in based on the closing price of the day? (Round your answer to the nearest whole number, e.g., 32.) b. Suppose...

Laura Cervantes. Laura Cervantes is a currency speculator and she sells eight June futures contracts for 500,000 pesos at the closing price quoted here: a. What is the value of her position at maturity if the ending spot rate is $0.12007/Ps? b. What is the value of her position at maturity if the ending spot rate is $0.09802/Ps? c. What is the value of her position at maturity if the ending spot rate is $0.11006/Ps? Data Table - a. What...

Laura Cervantes. Laura Cervantes is a currency speculator and she sells eight June futures contracts for 500,000 pesos at the closing price quoted here: a. What is the value of her position at maturity if the ending spot rate is $0.12007/Ps? b. What is the value of her position at maturity if the ending spot rate is $0.09802/Ps? c. What is the value of her position at maturity if the ending spot rate is $0.11006/Ps? Data Table - a. What...

Refer to Table 10-6 Price quotes are stated in 1/64ths a. How many ExxonMobil October 2016 $90.00 put options were outstanding at the open of trading on August 3, 2016? b. What was the closing price of a 10-year Treasury note December 13300 futures call option on August 3, 2016? c. What was the closing and dollar price of a December 2160 call option on the S&P 500 Stock Index futures contract on August 3. 2016? d. What was the...

Refer to Table 10-6 Price quotes are stated in 1/64ths a. How many ExxonMobil October 2016 $90.00 put options were outstanding at the open of trading on August 3, 2016? b. What was the closing price of a 10-year Treasury note December 13300 futures call option on August 3, 2016? c. What was the closing and dollar price of a December 2160 call option on the S&P 500 Stock Index futures contract on August 3. 2016? d. What was the...

Suppose you purchase a July 2011 soybean oil futures contract on

March 29, 2011, at the last price of the day. Use Table 23.1

What will your profit or loss be if soybean oil prices turn out

to be $0.4652 per pound at expiration

Suppose you sell eight May 2011 silver futures contracts on

March 29, 2011, at the last price of the day. Use Table 23.1

What will your profit or loss be if silver prices turn...

Suppose you purchase a July 2011 soybean oil futures contract on

March 29, 2011, at the last price of the day. Use Table 23.1

What will your profit or loss be if soybean oil prices turn out

to be $0.4652 per pound at expiration

Suppose you sell eight May 2011 silver futures contracts on

March 29, 2011, at the last price of the day. Use Table 23.1

What will your profit or loss be if silver prices turn...

Suppose you sell six August 2017 gold futures contracts on this day, at the last price of the day. Use Table 23.1 a. What will your profit or loss be if gold prices turn out to be $1,249.70 per ounce at expiration? (Do not round intermediate calculations. Enter your answer as a positive value rounded to the nearest whole number, e.g., 32.) b. What will your profit or loss be if gold prices are $1,235.90 per ounce at expiration? (Do...

Suppose you sell six August 2017 gold futures contracts on this day, at the last price of the day. Use Table 23.1 a. What will your profit or loss be if gold prices turn out to be $1,249.70 per ounce at expiration? (Do not round intermediate calculations. Enter your answer as a positive value rounded to the nearest whole number, e.g., 32.) b. What will your profit or loss be if gold prices are $1,235.90 per ounce at expiration? (Do...

Suppose you purchase a March 2017 oats futures contract on this day at the last price of the day. Use Table 23.1 What will your profit or loss be if oats prices turn out to be $2.4713 per bushel at expiration? (Do not round intermediate calculations. Enter your answer as a positive value and round your answer to 2 decimal places, e.g., 32.16.) Loss TABLE 23.1 Sample Wall Street Journal Futures Price Quotations Chg Open interest -0.0125 -0.0130 6 72...

Suppose you purchase a March 2017 oats futures contract on this day at the last price of the day. Use Table 23.1 What will your profit or loss be if oats prices turn out to be $2.4713 per bushel at expiration? (Do not round intermediate calculations. Enter your answer as a positive value and round your answer to 2 decimal places, e.g., 32.16.) Loss TABLE 23.1 Sample Wall Street Journal Futures Price Quotations Chg Open interest -0.0125 -0.0130 6 72...

Suppose today is February 10, 2017, and your firm produces breakfast cereal and needs 170,000 bushels of corn in May 2017 for an upcoming promotion. You would like to lock in your costs today because you are concerned that corn prices might rise between now and May. Use Table 23.1 a. What total cost would you effectively be locking in based on the closing price of the day? (Round your answer to the nearest whole number, e.g., 32.) b. Suppose...

Suppose today is February 10, 2017, and your firm produces breakfast cereal and needs 170,000 bushels of corn in May 2017 for an upcoming promotion. You would like to lock in your costs today because you are concerned that corn prices might rise between now and May. Use Table 23.1 a. What total cost would you effectively be locking in based on the closing price of the day? (Round your answer to the nearest whole number, e.g., 32.) b. Suppose...

Most questions answered within 3 hours.

-

I was looking for help with a computer science c programming

class. not c++

This program...

asked 11 minutes ago -

Albinism is an autosomal recessive condition characterized by

absence of melanin pigment from the skin, eye...

asked 1 minute ago -

Suppose you're looking at a physics example online, and come

across this expression in the middle...

asked 9 minutes ago -

Compile a list (7 or more) of other commands useful for

navigating or manipulating the UNIX/Linux...

asked 19 minutes ago -

How many grams of PbBr2 will precipitate when excess CrBr3

solution is added to 61.0 mL...

asked 21 minutes ago -

If I was given the address of 134.15.0.0/16 from my ISP and I

wanted to use...

asked 26 minutes ago -

What is the pH of the solution that results of dissolving 1.74g

of sodium hydroxide in...

asked 30 minutes ago -

Given a standardized normal distribution (with μ = 0 and a σ =

1), what is...

asked 1 hour ago -

Given the following information:

acetic acid

CH3COOH

Ka = 1.8×10-5

triethylamine

(C2H5)3N

Kb = 5.2×10-4

(1)...

asked 53 minutes ago -

Potassium permanganate(KMNO4)is has a solubility of 6.4 g/ 100 g

of water at 20ºC, and 250...

asked 50 minutes ago -

51.

As the marginal propensity to expend rises, the multiplier:

decreases.

is impossible to determine.

increases....

asked 57 minutes ago -

The Baldwin Company currently has the following balances on their

balance sheet:

Total

Liabilities

$69,309

Common...

asked 1 hour ago