Homework Answers

Add Answer to:

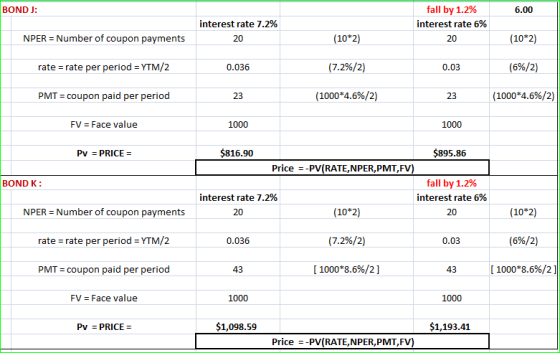

Problem 10-18 Interest Rate Risk (LO3, CFA4) Bond J has a coupon of 4.6 percent. Bond...

Problem 10-18 Interest Rate Risk (LO3, CFA4) Bond J has a coupon of 4.6 percent. Bond K has a coupon of 8.6 percent. Bo...

Problem 10-18 Interest Rate Risk (LO3, CFA4) Bond J has a coupon of 4.6 percent. Bond K has a coupon of 8.6 percent. Both bonds have 10 years to maturity and have a YTM of 7.2 percent. a. If interest rates suddenly rise by 1.2 percent, what is the percentage price change of these bonds? (A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal...

Problem 10-18 Interest Rate Risk (LO3, CFA4) Bond J has a coupon of 4.6 percent. Bond K has a coupon of 8.6 percent. Both bonds have 10 years to maturity and have a YTM of 7.2 percent. a. If interest rates suddenly rise by 1.2 percent, what is the percentage price change of these bonds? (A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal...

Bond J has a coupon of 4 percent. Bond K has a coupon of 8 percent....

Bond J has a coupon of 4 percent. Bond K has a coupon of 8 percent. Both bonds have 10 years to maturity and have a YTM of 7 percent. a. If interest rates suddenly rise by 2 percent, what is the percentage price change of these bonds? (A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.) b. If interest rates suddenly fall...

Bond J has a coupon of 4.2 percent. Bond K has a coupon of 8.2 percent....

Bond J has a coupon of 4.2 percent. Bond K has a coupon of 8.2 percent. Both bonds have 10 years to maturity and have a YTM of 6 percent. a. If interest rates suddenly rise by 1 percent, what is the percentage price change of these bonds? (A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.) %A in Price Bond J Bond...

Bond J has a coupon of 4.2 percent. Bond K has a coupon of 8.2 percent. Both bonds have 10 years to maturity and have a YTM of 6 percent. a. If interest rates suddenly rise by 1 percent, what is the percentage price change of these bonds? (A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.) %A in Price Bond J Bond...

Problem 10-18 Interest Rate RIS (LUS, CP44) 10 points Bond J has a coupon of 74...

Problem 10-18 Interest Rate RIS (LUS, CP44) 10 points Bond J has a coupon of 74 percent. Bond K has a coupon of 11.4 percent. Both bonds have 12 years to maturity and have a YTM of 78 percent. a. If interest rates suddenly rise by 2 percent, what is the percentage price change of these bonds? (A negative value should be Indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to...

Problem 10-18 Interest Rate RIS (LUS, CP44) 10 points Bond J has a coupon of 74 percent. Bond K has a coupon of 11.4 percent. Both bonds have 12 years to maturity and have a YTM of 78 percent. a. If interest rates suddenly rise by 2 percent, what is the percentage price change of these bonds? (A negative value should be Indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to...

Bond J has a coupon of 6.8 percent. Bond K has a coupon of 10.8 percent....

Bond J has a coupon of 6.8 percent. Bond K has a coupon of 10.8 percent. Both bonds have 20 years to maturity and have a YTM of 7.1 percent. a. If interest rates suddenly rise by 1.4 percent, what is the percentage price change of these bonds? (A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.) b. If interest rates suddenly fall...

Bond A has a 4% coupon. Bond B has a 10 percent coupon. Both bonds have...

Bond A has a 4% coupon. Bond B has a 10 percent coupon. Both bonds have 8 years to maturity, make annual payments, and have a YTM of 9 percent. If interest rates suddenly rise by 3 percent, what is the percentage price change in these bonds? What does this say about the interest rate risk of lower-coupon bonds? Please show the formulas you used.

Interest Rate Risk Laurel, Inc., and Hardy Corp. both have 5.8 percent coupon bonds outstanding, with...

Interest Rate Risk Laurel, Inc., and Hardy Corp. both have 5.8 percent coupon bonds outstanding, with semiannual interest payments, and both are priced at par value. The Laurel, Inc., bond has 3 years to maturity, whereas the Hardy Corp. bond has 20 years to maturity. If interest rates suddenly rise by 2 percent, what is the percentage change in the price of these bonds? If interest rates were to suddenly fall by 2 percent instead, what would the percentage change...

Interest Rate Risk Laurel, Inc., and Hardy Corp. both have 5.8 percent coupon bonds outstanding, with semiannual interest payments, and both are priced at par value. The Laurel, Inc., bond has 3 years to maturity, whereas the Hardy Corp. bond has 20 years to maturity. If interest rates suddenly rise by 2 percent, what is the percentage change in the price of these bonds? If interest rates were to suddenly fall by 2 percent instead, what would the percentage change...

The Faulk Corp. has a 5 percent coupon bond outstanding. The Gonas Company has a 11...

The Faulk Corp. has a 5 percent coupon bond outstanding. The Gonas Company has a 11 percent bond outstanding. Both bonds have 13 years to maturity, make semiannual payments, and have a YTM of 8 percent. If interest rates suddenly rise by 2 percent, what is the percentage change in the price of these bonds? What if interest rates suddenly fall by 2 percent instead?

Interest Rate Risk. Both Bond Bill and Bond Ted have 6.2 percent coupons, make semiannual payments,...

Interest Rate Risk. Both Bond Bill and Bond Ted have 6.2 percent coupons, make semiannual payments, and are priced at par value. Bond Bill has 5 years to maturity, whereas Bond Ted has 25 years to maturity. If interest rates suddenly rise by 2 percent, what is the percentage change in the price of Bond Bill? Of Bond Ted? Both bonds have a par value of $1,000. If rates were to suddenly fall by 2 percent instead, what would the...

Both Bond A and Bond B have 7.8 percent coupons and are priced at par value. Bond A has 9 years to maturity, while...

Both Bond A and Bond B have 7.8 percent coupons and are priced at par value. Bond A has 9 years to maturity, while Bond B has 16 years to maturity a. If interest rates suddenly rise by 2.2 percent, what is the percentage change in price of Bond A and Bond B? (A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.) Bond...

Both Bond A and Bond B have 7.8 percent coupons and are priced at par value. Bond A has 9 years to maturity, while Bond B has 16 years to maturity a. If interest rates suddenly rise by 2.2 percent, what is the percentage change in price of Bond A and Bond B? (A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.) Bond...

Problem 10-18 Interest Rate Risk (LO3, CFA4) Bond J has a coupon of 4.6 percent. Bond K has a coupon of 8.6 percent. Both bonds have 10 years to maturity and have a YTM of 7.2 percent. a. If interest rates suddenly rise by 1.2 percent, what is the percentage price change of these bonds? (A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal...

Problem 10-18 Interest Rate Risk (LO3, CFA4) Bond J has a coupon of 4.6 percent. Bond K has a coupon of 8.6 percent. Both bonds have 10 years to maturity and have a YTM of 7.2 percent. a. If interest rates suddenly rise by 1.2 percent, what is the percentage price change of these bonds? (A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal...

Bond J has a coupon of 4.2 percent. Bond K has a coupon of 8.2 percent. Both bonds have 10 years to maturity and have a YTM of 6 percent. a. If interest rates suddenly rise by 1 percent, what is the percentage price change of these bonds? (A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.) %A in Price Bond J Bond...

Bond J has a coupon of 4.2 percent. Bond K has a coupon of 8.2 percent. Both bonds have 10 years to maturity and have a YTM of 6 percent. a. If interest rates suddenly rise by 1 percent, what is the percentage price change of these bonds? (A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.) %A in Price Bond J Bond...

Problem 10-18 Interest Rate RIS (LUS, CP44) 10 points Bond J has a coupon of 74 percent. Bond K has a coupon of 11.4 percent. Both bonds have 12 years to maturity and have a YTM of 78 percent. a. If interest rates suddenly rise by 2 percent, what is the percentage price change of these bonds? (A negative value should be Indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to...

Problem 10-18 Interest Rate RIS (LUS, CP44) 10 points Bond J has a coupon of 74 percent. Bond K has a coupon of 11.4 percent. Both bonds have 12 years to maturity and have a YTM of 78 percent. a. If interest rates suddenly rise by 2 percent, what is the percentage price change of these bonds? (A negative value should be Indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to...

Interest Rate Risk Laurel, Inc., and Hardy Corp. both have 5.8 percent coupon bonds outstanding, with semiannual interest payments, and both are priced at par value. The Laurel, Inc., bond has 3 years to maturity, whereas the Hardy Corp. bond has 20 years to maturity. If interest rates suddenly rise by 2 percent, what is the percentage change in the price of these bonds? If interest rates were to suddenly fall by 2 percent instead, what would the percentage change...

Interest Rate Risk Laurel, Inc., and Hardy Corp. both have 5.8 percent coupon bonds outstanding, with semiannual interest payments, and both are priced at par value. The Laurel, Inc., bond has 3 years to maturity, whereas the Hardy Corp. bond has 20 years to maturity. If interest rates suddenly rise by 2 percent, what is the percentage change in the price of these bonds? If interest rates were to suddenly fall by 2 percent instead, what would the percentage change...

Both Bond A and Bond B have 7.8 percent coupons and are priced at par value. Bond A has 9 years to maturity, while Bond B has 16 years to maturity a. If interest rates suddenly rise by 2.2 percent, what is the percentage change in price of Bond A and Bond B? (A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.) Bond...

Both Bond A and Bond B have 7.8 percent coupons and are priced at par value. Bond A has 9 years to maturity, while Bond B has 16 years to maturity a. If interest rates suddenly rise by 2.2 percent, what is the percentage change in price of Bond A and Bond B? (A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.) Bond...

Most questions answered within 3 hours.

-

a. Discuss the reciprocal/opposite “hormonal” regulation of the

most highly regulated steps of these two pathways....

asked 2 minutes ago -

Members of unions had mounted campaigns to persuade customers

not to shop at a company because...

asked 3 minutes ago -

Why is the alpha carboxyl group pka value 2 ?

And why is an alpha amino...

asked 12 minutes ago -

Identify and assess an intrapreneurial

opportunities within Bank of America and

intrapreneurial assessment. Assess its impact...

asked 18 minutes ago -

How do I figure out the range of possible numbers that can be

represented by the...

asked 19 minutes ago -

A 0.48-kg metal sphere oscillates at the end of a vertical

spring. As the spring stretches...

asked 22 minutes ago -

If a block of Si is doped with 10^17 Boron atom/cm^3 and 5X10^16

Arsenic atoms/cm^3,

(a)...

asked 49 minutes ago -

Why would natural selection not minimize costs (in the form of

symptoms) of evolved defenses? (choose...

asked 1 hour ago -

What is true about a critical task?

Latest finish time - latest start time = 0...

asked 1 hour ago -

A company uses a

process costing system. Its Assembly Department's beginning

inventory consisted of 56,800 units,...

asked 1 hour ago -

a

sealed glass cylinder contains 325 g of N2 gas at 1.02 atm at 20 c....

asked 1 hour ago -

The main difference between an equity and a nonequity alliance

is that

A

equity alliances are...

asked 1 hour ago