Homework Answers

Please refer to below spreadsheet for calculation and answer. Cell reference also provided.

Cell reference -

Hope this will help, please do comment if you need any further explanation. Your feedback would be highly appreciated.

Add Answer to:

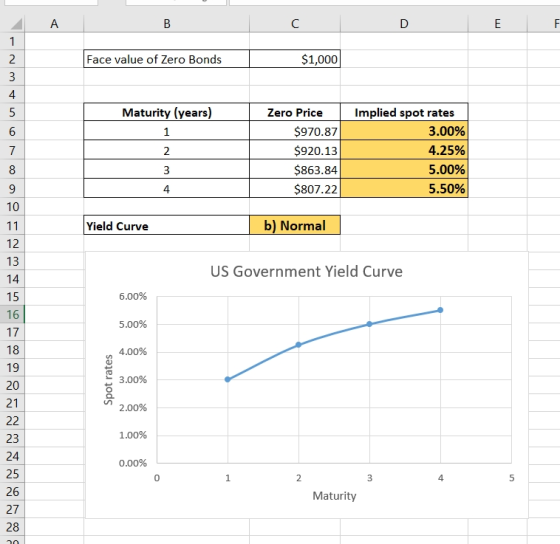

Prices in the table are for zero interest rate government bonds with a $1000 face value...

Suppose that you observe the following prices of three zero-coupon bonds issued by the government: YTM...

Suppose that you observe the following prices of three zero-coupon bonds issued by the government: YTM (spot rate) Price 985.22 1-year zero-coupon bond X 2-year zero-coupon bond Y 3-year zero-coupon bond Z Face value 1,000 1,000 1,000 P2 4% 901.94 Questions: A. (4 pts) Draw a yield curve based on the above three zero-coupon bonds. Comment on the shape. B. (6 pts) Calculate the implied 1-year forward interest rate, two years from now (i.e. f2.a)

Suppose that you observe the following prices of three zero-coupon bonds issued by the government: YTM (spot rate) Price 985.22 1-year zero-coupon bond X 2-year zero-coupon bond Y 3-year zero-coupon bond Z Face value 1,000 1,000 1,000 P2 4% 901.94 Questions: A. (4 pts) Draw a yield curve based on the above three zero-coupon bonds. Comment on the shape. B. (6 pts) Calculate the implied 1-year forward interest rate, two years from now (i.e. f2.a)

1. The following table summarizes prices of various default-free, zero-coupon bonds (expressed as a percentage of...

1. The following table summarizes prices of various default-free, zero-coupon bonds (expressed as a percentage of face value): Maturity (years) Price (per $100 face value) $95.51 9105 $86.38 $81.65 $76.51 (a) Compute the yield to maturity for each bond. (b) Plot the zero-coupon yield curve (for the first five years). (c) Is the yield curve upward sloping, downward sloping, or flat? 2. Suppose a seven-year, $1000 bond with an 8% coupon rate and semiannual coupons is trading with a yield...

1. The following table summarizes prices of various default-free, zero-coupon bonds (expressed as a percentage of face value): Maturity (years) Price (per $100 face value) $95.51 9105 $86.38 $81.65 $76.51 (a) Compute the yield to maturity for each bond. (b) Plot the zero-coupon yield curve (for the first five years). (c) Is the yield curve upward sloping, downward sloping, or flat? 2. Suppose a seven-year, $1000 bond with an 8% coupon rate and semiannual coupons is trading with a yield...

You currently own a 25-year maturity Government of Canada bond with a face value of $1000...

You currently own a 25-year maturity Government of Canada bond with a face value of $1000 that was issued Oct 15, 2015 (i.e. 5 years ago) with a 6% coupon paid semi-annually. The current price of the bond is $1075. a) What is the current YTM of this Government of Canada bond? Assume semi-annual compounding. b) You also own a Corporate bond that will mature in 20 years. It also pays a semi-annual coupon of 6% and has a face...

The table below shows market prices for four zero coupon bonds with four different terms: one,...

The table below shows market prices for four zero coupon bonds with four different terms: one, two, three and four years. The bonds all have a face value of $1 comma 000. Calculate the yields on the zero coupon bonds and graph the yield curve. What is the shape of the yield curve? Zero Coupon Bond Prices Term (years) Price ($) 1 925.93 2 841.68 3 751.31 4 658.73

URGENT!! The following table shows the prices of a sample of Treasury strips. Each strip makes...

URGENT!!

The following table shows the prices of a sample of Treasury strips. Each strip makes a single payment at maturity. Years to Maturity Price, % of face value) 98.152% 94.651 90.844 86.780 a. What is the 1-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) b. What is the 2-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) c....

URGENT!!

The following table shows the prices of a sample of Treasury strips. Each strip makes a single payment at maturity. Years to Maturity Price, % of face value) 98.152% 94.651 90.844 86.780 a. What is the 1-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) b. What is the 2-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) c....

The following table shows the prices of a sample of Treasury strips. Each strip makes a...

The following table shows the prices of a sample of Treasury strips. Each strip makes a single payment at maturity. Years to Maturity Price, (% of face value) 98.552% 95.051 91.244 87.180 a. What is the 1-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) b. What is the 2-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) c. What...

The following table shows the prices of a sample of Treasury strips. Each strip makes a single payment at maturity. Years to Maturity Price, (% of face value) 98.552% 95.051 91.244 87.180 a. What is the 1-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) b. What is the 2-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) c. What...

The following table shows the prices of a sample of Treasury strips. Each strip makes a...

The following table shows the prices of a sample of Treasury strips. Each strip makes a single payment at maturity. Years to Maturity Price, (% of face value) 98.152% 94.651 90.844 86.780 a. What is the 1-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) b. What is the 2-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) c. What...

The following table shows the prices of a sample of Treasury strips. Each strip makes a single payment at maturity. Years to Maturity Price, (% of face value) 98.152% 94.651 90.844 86.780 a. What is the 1-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) b. What is the 2-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) c. What...

6. Spot rates of interest for zero-coupon Government of Canada bonds are observed for different terms...

6. Spot rates of interest for zero-coupon Government of Canada bonds are observed for different terms to maturity as follows: 1-year spot rate 4% 2-year spot rate 4.5% 3-year spot rate 5% A 3-year bond has a face value of $1,000 and a coupon rate of 7%. It pays coupons annually. What is its value today? (3 marks)

11) When discussing bonds, convexity relates to the ________. A. shape of the bond price curve...

11) When discussing bonds, convexity relates to the ________. A. shape of the bond price curve B. shape of the yield curve C. slope of the yield curve D. shape of the bond dealer 12) A zero-coupon bond has a yield to maturity of 5% and a par value of $1,000. If the bond matures in 16 years, it should sell for a price of __________ today. A. $458.00 B. $641.00 C. $789.00 D. $1,100.00 13) The yield-to-maturity (YTM) on...

PLEASE INCLUDE B AND C IN ANSWER. SAYS 6 numbers need to be entered total The...

PLEASE INCLUDE B AND C IN ANSWER. SAYS 6 numbers need to be

entered total

The following table summarizes prices of various default-free zero-coupon bonds ($100 face value): 1 Maturity (years) Price (per $100 face value) $95.19 $90.71 $86.04 $81.16 $76.08 a. Compute the yield to maturity for each bond. b. Plot the zero-coupon yield curve (for the first five years). c. Is the yield curve upward sloping, downward sloping, or flat? Note: Assume annual compounding. a. Compute the yield...

PLEASE INCLUDE B AND C IN ANSWER. SAYS 6 numbers need to be

entered total

The following table summarizes prices of various default-free zero-coupon bonds ($100 face value): 1 Maturity (years) Price (per $100 face value) $95.19 $90.71 $86.04 $81.16 $76.08 a. Compute the yield to maturity for each bond. b. Plot the zero-coupon yield curve (for the first five years). c. Is the yield curve upward sloping, downward sloping, or flat? Note: Assume annual compounding. a. Compute the yield...

Suppose that you observe the following prices of three zero-coupon bonds issued by the government: YTM (spot rate) Price 985.22 1-year zero-coupon bond X 2-year zero-coupon bond Y 3-year zero-coupon bond Z Face value 1,000 1,000 1,000 P2 4% 901.94 Questions: A. (4 pts) Draw a yield curve based on the above three zero-coupon bonds. Comment on the shape. B. (6 pts) Calculate the implied 1-year forward interest rate, two years from now (i.e. f2.a)

Suppose that you observe the following prices of three zero-coupon bonds issued by the government: YTM (spot rate) Price 985.22 1-year zero-coupon bond X 2-year zero-coupon bond Y 3-year zero-coupon bond Z Face value 1,000 1,000 1,000 P2 4% 901.94 Questions: A. (4 pts) Draw a yield curve based on the above three zero-coupon bonds. Comment on the shape. B. (6 pts) Calculate the implied 1-year forward interest rate, two years from now (i.e. f2.a)

1. The following table summarizes prices of various default-free, zero-coupon bonds (expressed as a percentage of face value): Maturity (years) Price (per $100 face value) $95.51 9105 $86.38 $81.65 $76.51 (a) Compute the yield to maturity for each bond. (b) Plot the zero-coupon yield curve (for the first five years). (c) Is the yield curve upward sloping, downward sloping, or flat? 2. Suppose a seven-year, $1000 bond with an 8% coupon rate and semiannual coupons is trading with a yield...

1. The following table summarizes prices of various default-free, zero-coupon bonds (expressed as a percentage of face value): Maturity (years) Price (per $100 face value) $95.51 9105 $86.38 $81.65 $76.51 (a) Compute the yield to maturity for each bond. (b) Plot the zero-coupon yield curve (for the first five years). (c) Is the yield curve upward sloping, downward sloping, or flat? 2. Suppose a seven-year, $1000 bond with an 8% coupon rate and semiannual coupons is trading with a yield...

URGENT!!

The following table shows the prices of a sample of Treasury strips. Each strip makes a single payment at maturity. Years to Maturity Price, % of face value) 98.152% 94.651 90.844 86.780 a. What is the 1-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) b. What is the 2-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) c....

URGENT!!

The following table shows the prices of a sample of Treasury strips. Each strip makes a single payment at maturity. Years to Maturity Price, % of face value) 98.152% 94.651 90.844 86.780 a. What is the 1-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) b. What is the 2-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) c....

The following table shows the prices of a sample of Treasury strips. Each strip makes a single payment at maturity. Years to Maturity Price, (% of face value) 98.552% 95.051 91.244 87.180 a. What is the 1-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) b. What is the 2-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) c. What...

The following table shows the prices of a sample of Treasury strips. Each strip makes a single payment at maturity. Years to Maturity Price, (% of face value) 98.552% 95.051 91.244 87.180 a. What is the 1-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) b. What is the 2-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) c. What...

The following table shows the prices of a sample of Treasury strips. Each strip makes a single payment at maturity. Years to Maturity Price, (% of face value) 98.152% 94.651 90.844 86.780 a. What is the 1-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) b. What is the 2-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) c. What...

The following table shows the prices of a sample of Treasury strips. Each strip makes a single payment at maturity. Years to Maturity Price, (% of face value) 98.152% 94.651 90.844 86.780 a. What is the 1-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) b. What is the 2-year interest rate? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) c. What...

PLEASE INCLUDE B AND C IN ANSWER. SAYS 6 numbers need to be

entered total

The following table summarizes prices of various default-free zero-coupon bonds ($100 face value): 1 Maturity (years) Price (per $100 face value) $95.19 $90.71 $86.04 $81.16 $76.08 a. Compute the yield to maturity for each bond. b. Plot the zero-coupon yield curve (for the first five years). c. Is the yield curve upward sloping, downward sloping, or flat? Note: Assume annual compounding. a. Compute the yield...

PLEASE INCLUDE B AND C IN ANSWER. SAYS 6 numbers need to be

entered total

The following table summarizes prices of various default-free zero-coupon bonds ($100 face value): 1 Maturity (years) Price (per $100 face value) $95.19 $90.71 $86.04 $81.16 $76.08 a. Compute the yield to maturity for each bond. b. Plot the zero-coupon yield curve (for the first five years). c. Is the yield curve upward sloping, downward sloping, or flat? Note: Assume annual compounding. a. Compute the yield...

Most questions answered within 3 hours.

-

Calculate the specific heat of a certain unknown metal, if it

requires 195 joules of heat...

asked 1 minute ago -

Identify the characteristics of a successful

project.

Describe the phases the project lifecycle.

Define the roles...

asked 10 minutes ago -

1. In Module 2 "headers" and "footers" are

described. Explain the difference between them and how...

asked 5 minutes ago -

Three polarizing filters are stacked with the polarizing axes of

the second and third at 58.5...

asked 14 minutes ago -

The capacitance in a series RCL circuit is C1 = 3.3 μF, and

the corresponding resonant...

asked 24 minutes ago -

A 357.7-gram sample of an unknown substance (MM = 92.41 g/mol)

is heated from -23.1 °C...

asked 23 minutes ago -

The project aims to design a network for a casino. The casino

has 10 floors including...

asked 28 minutes ago -

Combustion of an unknown compound containing only carbon and

hydrogen produces 54.9 g of CO₂ and...

asked 43 minutes ago -

A basketball player achieves a hang time, the total time of

flight, of 0.748 s when...

asked 44 minutes ago -

A processor of carrots cuts the green top off each carrot,

washes the carrots, and inserts...

asked 56 minutes ago -

Please help me find the coefficient of kinetic and static

friction of two masses (500kg and...

asked 52 minutes ago -

Stanley Department Stores reported net income of $815,000 for

the year ended December 31, 2018.

Additional...

asked 57 minutes ago