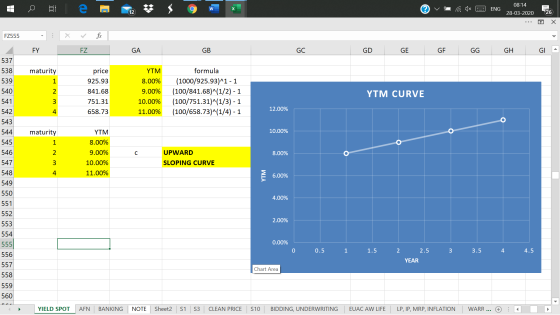

The table below shows market prices for four zero coupon bonds with four different terms: one,...

The table below shows market prices for four zero coupon bonds with four different terms: one, two, three and four years. The bonds all have a face value of $1 comma 000. Calculate the yields on the zero coupon bonds and graph the yield curve. What is the shape of the yield curve? Zero Coupon Bond Prices Term (years) Price ($) 1 925.93 2 841.68 3 751.31 4 658.73

Homework Answers

SEE THE IMAGE. ANY DOUBTS, FEEL FREE TO ASK. THUMBS UP PLEASE

Add Answer to:

The table below shows market prices for four zero coupon bonds

with four different terms: one,...

Suppose that you observe the following prices of three zero-coupon bonds issued by the government: YTM...

Suppose that you observe the following prices of three zero-coupon bonds issued by the government: YTM (spot rate) Price 985.22 1-year zero-coupon bond X 2-year zero-coupon bond Y 3-year zero-coupon bond Z Face value 1,000 1,000 1,000 P2 4% 901.94 Questions: A. (4 pts) Draw a yield curve based on the above three zero-coupon bonds. Comment on the shape. B. (6 pts) Calculate the implied 1-year forward interest rate, two years from now (i.e. f2.a)

Suppose that you observe the following prices of three zero-coupon bonds issued by the government: YTM (spot rate) Price 985.22 1-year zero-coupon bond X 2-year zero-coupon bond Y 3-year zero-coupon bond Z Face value 1,000 1,000 1,000 P2 4% 901.94 Questions: A. (4 pts) Draw a yield curve based on the above three zero-coupon bonds. Comment on the shape. B. (6 pts) Calculate the implied 1-year forward interest rate, two years from now (i.e. f2.a)

1. The following table summarizes prices of various default-free, zero-coupon bonds (expressed as a percentage of...

1. The following table summarizes prices of various default-free, zero-coupon bonds (expressed as a percentage of face value): Maturity (years) Price (per $100 face value) $95.51 9105 $86.38 $81.65 $76.51 (a) Compute the yield to maturity for each bond. (b) Plot the zero-coupon yield curve (for the first five years). (c) Is the yield curve upward sloping, downward sloping, or flat? 2. Suppose a seven-year, $1000 bond with an 8% coupon rate and semiannual coupons is trading with a yield...

1. The following table summarizes prices of various default-free, zero-coupon bonds (expressed as a percentage of face value): Maturity (years) Price (per $100 face value) $95.51 9105 $86.38 $81.65 $76.51 (a) Compute the yield to maturity for each bond. (b) Plot the zero-coupon yield curve (for the first five years). (c) Is the yield curve upward sloping, downward sloping, or flat? 2. Suppose a seven-year, $1000 bond with an 8% coupon rate and semiannual coupons is trading with a yield...

Prices in the table are for zero interest rate government bonds with a $1000 face value...

Prices in the table are for zero interest rate government bonds with a $1000 face value Maturity (years) Zero Price 1 $ 970.87 - 2 $ 920.13 3 $ 863.84 4 $ 807.22 • A 5 year government bond with a $1000 face value that pays a 4.0% coupon (with annual payments) is priced at $925 today. 13.(CH15) First, find the implied spot rates for years 1-5 (i.e. bootstrap the yield curve). Based on the spot rates, the shape of...

Prices in the table are for zero interest rate government bonds with a $1000 face value Maturity (years) Zero Price 1 $ 970.87 - 2 $ 920.13 3 $ 863.84 4 $ 807.22 • A 5 year government bond with a $1000 face value that pays a 4.0% coupon (with annual payments) is priced at $925 today. 13.(CH15) First, find the implied spot rates for years 1-5 (i.e. bootstrap the yield curve). Based on the spot rates, the shape of...

The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of face value...

The following table summarizes prices of

various default-free zero-coupon bonds (expressed as a percentage

of face value):

Maturity (years) Price (per $100 face value) | 1 | 2 | 3 | 4 | 5 94.52 89.68 85.40 81.65 78.35 The yield to maturity for the four-year zero-coupon bond is closest to _ a 0.18% Ob. 10.40% Oc. 2.60% Od. 22.47% Oe.5.20%

The following table summarizes prices of

various default-free zero-coupon bonds (expressed as a percentage

of face value):

Maturity (years) Price (per $100 face value) | 1 | 2 | 3 | 4 | 5 94.52 89.68 85.40 81.65 78.35 The yield to maturity for the four-year zero-coupon bond is closest to _ a 0.18% Ob. 10.40% Oc. 2.60% Od. 22.47% Oe.5.20%

Bond prices in the absence of arbitrage Consider a market with two risk-free zero-coupon bonds, A...

Bond prices in the absence of arbitrage Consider a market with two risk-free zero-coupon bonds, A and B. Their respective maturities are 1 and 2 years, and their market prices are 97.0874 and 95.1814 (expressed as percentage of the face value). (a) Calculate the discount rates rt for t = 1 and 2 years. (b) Suppose that a two-year bond C, with a coupon rate of 2.75%, also trades in the market. What should be its price if there is...

4. The following table summarizes prices of various zero-coupon bonds (expressed as a percentage of face...

4. The following table summarizes prices of various zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 123 Price (per $100 face value) $95.51 $91.05 | $86.38 $81.65 | $76.51 Compute the yield to maturity for each bond.

4. The following table summarizes prices of various zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 123 Price (per $100 face value) $95.51 $91.05 | $86.38 $81.65 | $76.51 Compute the yield to maturity for each bond.

14, A one-year zero coupon bond yields 3.0%. The two-and three-year zero-coupon bonds yield 4.0% and 5.0% respectively. a. The forward rate for a one-year loan beginning in two years is closest t...

14, A one-year zero coupon bond yields 3.0%. The two-and three-year zero-coupon bonds yield 4.0% and 5.0% respectively. a. The forward rate for a one-year loan beginning in two years is closest to? (10 points) b. The four-year spot rate is not given above; however, the forward price for a one-year zero-coupon bond beginning in three years is known to be 0.8400. The price today of a four-year zero-coupon bond is closest to? (5 points)

14, A one-year zero coupon...

14, A one-year zero coupon bond yields 3.0%. The two-and three-year zero-coupon bonds yield 4.0% and 5.0% respectively. a. The forward rate for a one-year loan beginning in two years is closest to? (10 points) b. The four-year spot rate is not given above; however, the forward price for a one-year zero-coupon bond beginning in three years is known to be 0.8400. The price today of a four-year zero-coupon bond is closest to? (5 points)

14, A one-year zero coupon...

Below is a list of prices for zero-coupon bonds of various maturities. Price of $1,000 Par...

Below is a list of prices for zero-coupon bonds of various maturities. Price of $1,000 Par Maturity (Years) Bond (Zero-Coupon) $966.78 894.28 803.54 WN a. A 6.4% coupon $1,000 par bond pays an annual coupon and will mature in 3 years. What should the yield to maturity on the bond be? (Round your answer to 2 decimal places.) Yield to maturity % b. If at the end of the first year the yield curve flattens out at 8.1%, what will...

Below is a list of prices for zero-coupon bonds of various maturities. Price of $1,000 Par Maturity (Years) Bond (Zero-Coupon) $966.78 894.28 803.54 WN a. A 6.4% coupon $1,000 par bond pays an annual coupon and will mature in 3 years. What should the yield to maturity on the bond be? (Round your answer to 2 decimal places.) Yield to maturity % b. If at the end of the first year the yield curve flattens out at 8.1%, what will...

The following is a list of prices for zero-coupon bonds of various maturities. a. Calculate the...

The following is a list of prices for zero-coupon bonds of various maturities. a. Calculate the yield to maturity for a bond with a maturity of (i) one year; (ii) two years; (iii) three years; (iv) four years. (Do not round intermediate calculations. Round your answers to two decimal places.) Maturity (Years) YTM Price of Bond $ 955.00 901.47 حج | ده | م 838.62 $ 779.89

The following is a list of prices for zero-coupon bonds of various maturities. a. Calculate the yield to maturity for a bond with a maturity of (i) one year; (ii) two years; (iii) three years; (iv) four years. (Do not round intermediate calculations. Round your answers to two decimal places.) Maturity (Years) YTM Price of Bond $ 955.00 901.47 حج | ده | م 838.62 $ 779.89

plz show steps Using zero coupon bonds You know the information on three bonds that make...

plz show steps

Using zero coupon bonds You know the information on three bonds that make annual coupon payments, if any. Bond Maturity 1) What are the prices of bonds A and B? Face value $1,000 $1,000 $1,000 tinin mo-NM Coupon rate 0.00% 0.00% 10.00% Yield to maturity 5.00% 5.85% 2) What are the zero-coupon bond yields for 1-year bond and 2-year bond? с 3) What is the price of bond C? 4) What is the yield of bond C?

plz show steps

Using zero coupon bonds You know the information on three bonds that make annual coupon payments, if any. Bond Maturity 1) What are the prices of bonds A and B? Face value $1,000 $1,000 $1,000 tinin mo-NM Coupon rate 0.00% 0.00% 10.00% Yield to maturity 5.00% 5.85% 2) What are the zero-coupon bond yields for 1-year bond and 2-year bond? с 3) What is the price of bond C? 4) What is the yield of bond C?

Suppose that you observe the following prices of three zero-coupon bonds issued by the government: YTM (spot rate) Price 985.22 1-year zero-coupon bond X 2-year zero-coupon bond Y 3-year zero-coupon bond Z Face value 1,000 1,000 1,000 P2 4% 901.94 Questions: A. (4 pts) Draw a yield curve based on the above three zero-coupon bonds. Comment on the shape. B. (6 pts) Calculate the implied 1-year forward interest rate, two years from now (i.e. f2.a)

Suppose that you observe the following prices of three zero-coupon bonds issued by the government: YTM (spot rate) Price 985.22 1-year zero-coupon bond X 2-year zero-coupon bond Y 3-year zero-coupon bond Z Face value 1,000 1,000 1,000 P2 4% 901.94 Questions: A. (4 pts) Draw a yield curve based on the above three zero-coupon bonds. Comment on the shape. B. (6 pts) Calculate the implied 1-year forward interest rate, two years from now (i.e. f2.a)

1. The following table summarizes prices of various default-free, zero-coupon bonds (expressed as a percentage of face value): Maturity (years) Price (per $100 face value) $95.51 9105 $86.38 $81.65 $76.51 (a) Compute the yield to maturity for each bond. (b) Plot the zero-coupon yield curve (for the first five years). (c) Is the yield curve upward sloping, downward sloping, or flat? 2. Suppose a seven-year, $1000 bond with an 8% coupon rate and semiannual coupons is trading with a yield...

1. The following table summarizes prices of various default-free, zero-coupon bonds (expressed as a percentage of face value): Maturity (years) Price (per $100 face value) $95.51 9105 $86.38 $81.65 $76.51 (a) Compute the yield to maturity for each bond. (b) Plot the zero-coupon yield curve (for the first five years). (c) Is the yield curve upward sloping, downward sloping, or flat? 2. Suppose a seven-year, $1000 bond with an 8% coupon rate and semiannual coupons is trading with a yield...

Prices in the table are for zero interest rate government bonds with a $1000 face value Maturity (years) Zero Price 1 $ 970.87 - 2 $ 920.13 3 $ 863.84 4 $ 807.22 • A 5 year government bond with a $1000 face value that pays a 4.0% coupon (with annual payments) is priced at $925 today. 13.(CH15) First, find the implied spot rates for years 1-5 (i.e. bootstrap the yield curve). Based on the spot rates, the shape of...

Prices in the table are for zero interest rate government bonds with a $1000 face value Maturity (years) Zero Price 1 $ 970.87 - 2 $ 920.13 3 $ 863.84 4 $ 807.22 • A 5 year government bond with a $1000 face value that pays a 4.0% coupon (with annual payments) is priced at $925 today. 13.(CH15) First, find the implied spot rates for years 1-5 (i.e. bootstrap the yield curve). Based on the spot rates, the shape of...

The following table summarizes prices of

various default-free zero-coupon bonds (expressed as a percentage

of face value):

Maturity (years) Price (per $100 face value) | 1 | 2 | 3 | 4 | 5 94.52 89.68 85.40 81.65 78.35 The yield to maturity for the four-year zero-coupon bond is closest to _ a 0.18% Ob. 10.40% Oc. 2.60% Od. 22.47% Oe.5.20%

The following table summarizes prices of

various default-free zero-coupon bonds (expressed as a percentage

of face value):

Maturity (years) Price (per $100 face value) | 1 | 2 | 3 | 4 | 5 94.52 89.68 85.40 81.65 78.35 The yield to maturity for the four-year zero-coupon bond is closest to _ a 0.18% Ob. 10.40% Oc. 2.60% Od. 22.47% Oe.5.20%

4. The following table summarizes prices of various zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 123 Price (per $100 face value) $95.51 $91.05 | $86.38 $81.65 | $76.51 Compute the yield to maturity for each bond.

4. The following table summarizes prices of various zero-coupon bonds (expressed as a percentage of face value): Maturity (years) 123 Price (per $100 face value) $95.51 $91.05 | $86.38 $81.65 | $76.51 Compute the yield to maturity for each bond.

14, A one-year zero coupon bond yields 3.0%. The two-and three-year zero-coupon bonds yield 4.0% and 5.0% respectively. a. The forward rate for a one-year loan beginning in two years is closest to? (10 points) b. The four-year spot rate is not given above; however, the forward price for a one-year zero-coupon bond beginning in three years is known to be 0.8400. The price today of a four-year zero-coupon bond is closest to? (5 points)

14, A one-year zero coupon...

14, A one-year zero coupon bond yields 3.0%. The two-and three-year zero-coupon bonds yield 4.0% and 5.0% respectively. a. The forward rate for a one-year loan beginning in two years is closest to? (10 points) b. The four-year spot rate is not given above; however, the forward price for a one-year zero-coupon bond beginning in three years is known to be 0.8400. The price today of a four-year zero-coupon bond is closest to? (5 points)

14, A one-year zero coupon...

Below is a list of prices for zero-coupon bonds of various maturities. Price of $1,000 Par Maturity (Years) Bond (Zero-Coupon) $966.78 894.28 803.54 WN a. A 6.4% coupon $1,000 par bond pays an annual coupon and will mature in 3 years. What should the yield to maturity on the bond be? (Round your answer to 2 decimal places.) Yield to maturity % b. If at the end of the first year the yield curve flattens out at 8.1%, what will...

Below is a list of prices for zero-coupon bonds of various maturities. Price of $1,000 Par Maturity (Years) Bond (Zero-Coupon) $966.78 894.28 803.54 WN a. A 6.4% coupon $1,000 par bond pays an annual coupon and will mature in 3 years. What should the yield to maturity on the bond be? (Round your answer to 2 decimal places.) Yield to maturity % b. If at the end of the first year the yield curve flattens out at 8.1%, what will...

The following is a list of prices for zero-coupon bonds of various maturities. a. Calculate the yield to maturity for a bond with a maturity of (i) one year; (ii) two years; (iii) three years; (iv) four years. (Do not round intermediate calculations. Round your answers to two decimal places.) Maturity (Years) YTM Price of Bond $ 955.00 901.47 حج | ده | م 838.62 $ 779.89

The following is a list of prices for zero-coupon bonds of various maturities. a. Calculate the yield to maturity for a bond with a maturity of (i) one year; (ii) two years; (iii) three years; (iv) four years. (Do not round intermediate calculations. Round your answers to two decimal places.) Maturity (Years) YTM Price of Bond $ 955.00 901.47 حج | ده | م 838.62 $ 779.89

plz show steps

Using zero coupon bonds You know the information on three bonds that make annual coupon payments, if any. Bond Maturity 1) What are the prices of bonds A and B? Face value $1,000 $1,000 $1,000 tinin mo-NM Coupon rate 0.00% 0.00% 10.00% Yield to maturity 5.00% 5.85% 2) What are the zero-coupon bond yields for 1-year bond and 2-year bond? с 3) What is the price of bond C? 4) What is the yield of bond C?

plz show steps

Using zero coupon bonds You know the information on three bonds that make annual coupon payments, if any. Bond Maturity 1) What are the prices of bonds A and B? Face value $1,000 $1,000 $1,000 tinin mo-NM Coupon rate 0.00% 0.00% 10.00% Yield to maturity 5.00% 5.85% 2) What are the zero-coupon bond yields for 1-year bond and 2-year bond? с 3) What is the price of bond C? 4) What is the yield of bond C?

Most questions answered within 3 hours.

-

Katelynn, a physician, earns $200,000 from her medical practice

in the current year. She receives $45,000...

asked 2 seconds ago -

Each row of the table below describes an aqueous solution at

25°C

.

The second column...

asked 4 minutes ago -

A horizontal wire is at y = 0. Current travels in the +x

direction. The magnetic...

asked 4 minutes ago -

Let X be a continuous random variable whose PDF is Let X be a

continuous random...

asked 26 minutes ago -

Martinez Company’s relevant range of production is 7,500 units

to 12,500 units. When it produces and...

asked 23 minutes ago -

A football with a mass of 1.2 kg is kicked from ground level to

a height...

asked 29 minutes ago -

Remember: Changes in supply determinants shift supply, and

changes in demand determinants shift demand. We say...

asked 28 minutes ago -

Why is the answer b), for this question? I came up with C) for

my incorrect...

asked 34 minutes ago -

Suppose that you know that in the population of full-time

employees in the United States, the...

asked 56 minutes ago -

This experiment was designed originally to sample various meat and carcass quality

aspects of Ontario pigs...

asked 56 minutes ago -

Dopamine Hydrochloride: draw the structure And Show the

functional groups in different colors and label the...

asked 48 minutes ago -

A rope supports a 10 kg dumbbell hanging from it. What is the

tension in the...

asked 48 minutes ago