Homework Answers

Add Answer to:

1. (60 points) Company X is in a perfectly competitive industry and is in long run....

1. (60 points) Company X is in a perfectly competitive industry and is in long run....

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option I: TFC $7,500,000, TVC(Q) 100+ 10,000 Q, in $ Option ll: TFC $3,000,000, TVC(Q) 120+ 25,000 Q2, in $ a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can...

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option I: TFC $7,500,000, TVC(Q) 100+ 10,000 Q, in $ Option ll: TFC $3,000,000, TVC(Q) 120+ 25,000 Q2, in $ a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can...

1. (60 points) Company X is in a perfectly competitive industry and is in long run....

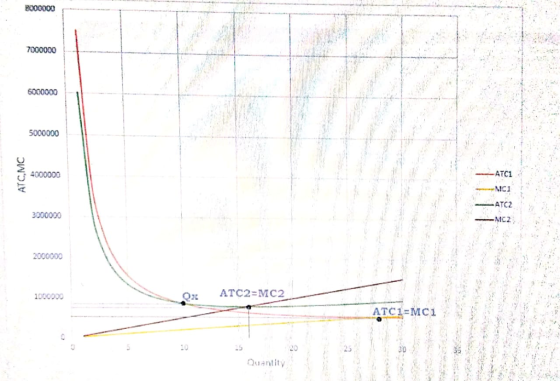

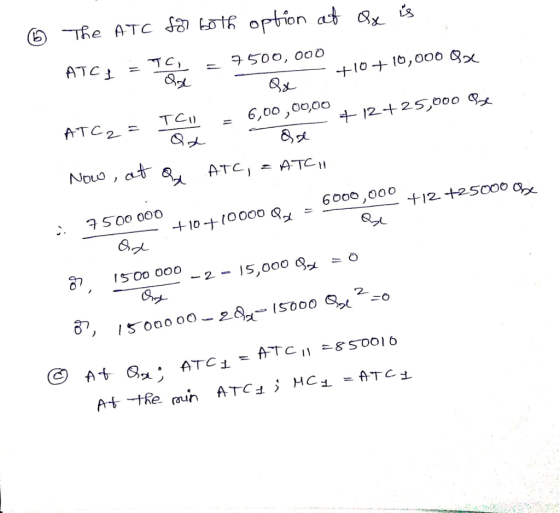

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option I: TFC $7,500,000, TVC(a) 100+ 10,000 Q2, in $. Option Il: TFC $6,000,000, TVC(Q) 120+ 25,000 Q2, in $. a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can...

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option I: TFC $7,500,000, TVC(a) 100+ 10,000 Q2, in $. Option Il: TFC $6,000,000, TVC(Q) 120+ 25,000 Q2, in $. a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can...

1. (60 points) Company X is in a perfectly competitive industry and is in long run....

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option I: TFC $7,500,000, TVC(a) 100+ 10,000 Q2, in $. Option Il: TFC $6,000,000, TVC(Q) 120+ 25,000 Q2, in $. a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can...

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option I: TFC $7,500,000, TVC(a) 100+ 10,000 Q2, in $. Option Il: TFC $6,000,000, TVC(Q) 120+ 25,000 Q2, in $. a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can...

1. (60 points) Company X is in a perfectly competitive industry and is in long run....

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option I: TFC $7,500,000, TVC(a) 100+ 10,000 Q2, in $. Option Il: TFC $6,000,000, TVC(Q) 120+ 25,000 Q2, in $. a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can...

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option I: TFC $7,500,000, TVC(a) 100+ 10,000 Q2, in $. Option Il: TFC $6,000,000, TVC(Q) 120+ 25,000 Q2, in $. a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can...

1. (60 points) Company X is in a perfectly competitive industry and is in long run....

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option 1: TFC-$7,500,000, TVC(Q)-10Q+ 10,000 Q. in $. Option Il: TFC $3,000,000, TVC(a) 120+ 25,000 a2, in $. a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can use any...

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option 1: TFC-$7,500,000, TVC(Q)-10Q+ 10,000 Q. in $. Option Il: TFC $3,000,000, TVC(a) 120+ 25,000 a2, in $. a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can use any...

10. Linda wants to open a T-shirt stand for Homecoming week. The school will license her...

10. Linda wants to open a T-shirt stand for Homecoming week. The school will license her a booth for $100. Each T-shirt from the store will cost her $4. Linda's average cost function will be: A) $100+ $4X B) $100/X + $4 C) $104/X D) $100/X+S4/X 11. Which of the following formulas is NOT correct? a. MC = TC/Q b. TVC = AVC * Q c. TC=(AFC + AVC)*Q d. AFC = TFC/Q e. ATC = AVC + (TFC/Q) 12....

10. Linda wants to open a T-shirt stand for Homecoming week. The school will license her a booth for $100. Each T-shirt from the store will cost her $4. Linda's average cost function will be: A) $100+ $4X B) $100/X + $4 C) $104/X D) $100/X+S4/X 11. Which of the following formulas is NOT correct? a. MC = TC/Q b. TVC = AVC * Q c. TC=(AFC + AVC)*Q d. AFC = TFC/Q e. ATC = AVC + (TFC/Q) 12....

5. Deriving the short-run supply curve Aa Aa Consider the perfectly competitive market for halogen ceiling...

5. Deriving the short-run supply curve Aa Aa Consider the perfectly competitive market for halogen ceiling lamps. The following graph shows the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves for a typical firm in the industry. COSTS Dollars per lampl 100 MC 90 80 70 60 ATC AVC 50 40 30 20 10 0 4 8 12 16 20 24 28 32 36 40 QUANTITY OF OUTPUT (Thousands of lamps) For each price in...

5. Deriving the short-run supply curve Aa Aa Consider the perfectly competitive market for halogen ceiling lamps. The following graph shows the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves for a typical firm in the industry. COSTS Dollars per lampl 100 MC 90 80 70 60 ATC AVC 50 40 30 20 10 0 4 8 12 16 20 24 28 32 36 40 QUANTITY OF OUTPUT (Thousands of lamps) For each price in...

2. (40 points) A monopolistically competitive company assembles and installs solar panels it imports at $10...

2. (40 points) A monopolistically competitive company assembles and installs solar panels it imports at $10 per unit. All remaining costs of the company, denoted RC, is given by the following (as a function of per unit solar panel): RC(Q) = 1,000+5Q2 The demand faced by this company is given by Q-16.67-xP where P denotes the price, Q denotes the quantity and x is currently equal to 1/30. a) (10) points) What is the optimal production level, Q*, and what...

2. (40 points) A monopolistically competitive company assembles and installs solar panels it imports at $10 per unit. All remaining costs of the company, denoted RC, is given by the following (as a function of per unit solar panel): RC(Q) = 1,000+5Q2 The demand faced by this company is given by Q-16.67-xP where P denotes the price, Q denotes the quantity and x is currently equal to 1/30. a) (10) points) What is the optimal production level, Q*, and what...

Question 2 (15 points) Continuing your analysis of the competitive US manufacturing industry from Question 1,...

Question 2 (15 points) Continuing your analysis of the competitive US manufacturing industry from Question 1, with demand of Q = 200-P and supply of Q. = P-20, suppose a technological innovation causes the supply curve to shift down by $20 for every given quantity Q. • Depict the original supply, the new supply, and the original demand curves on the usual P, Q diagram. Label all intercepts. Clearly indicate and label the new market equilibrium. 2/8/2 compass 20 Mlinois.edu/bbcswebdavipid-4037356-dt-con020%20ECON528%20M6...

Question 2 (15 points) Continuing your analysis of the competitive US manufacturing industry from Question 1, with demand of Q = 200-P and supply of Q. = P-20, suppose a technological innovation causes the supply curve to shift down by $20 for every given quantity Q. • Depict the original supply, the new supply, and the original demand curves on the usual P, Q diagram. Label all intercepts. Clearly indicate and label the new market equilibrium. 2/8/2 compass 20 Mlinois.edu/bbcswebdavipid-4037356-dt-con020%20ECON528%20M6...

Question 2 (18) In scenario 1, Kobus specialises in the production of two products, namely apples...

Question 2 (18) In scenario 1, Kobus specialises in the production of two products, namely apples and honey. With reference to Humming Honey, answer the following questions: 2.1 With reference to the (per box) production of Humming Honey, differentiate between marginal cost, marginal revenue and marginal production. (3) 2.2. In the short run, the farmer's costs in the production of Humming Honey consist of fixed costs and variable costs. Using your knowledge of cost formulas and calculations, redraw and complete...

Question 2 (18) In scenario 1, Kobus specialises in the production of two products, namely apples and honey. With reference to Humming Honey, answer the following questions: 2.1 With reference to the (per box) production of Humming Honey, differentiate between marginal cost, marginal revenue and marginal production. (3) 2.2. In the short run, the farmer's costs in the production of Humming Honey consist of fixed costs and variable costs. Using your knowledge of cost formulas and calculations, redraw and complete...

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option I: TFC $7,500,000, TVC(Q) 100+ 10,000 Q, in $ Option ll: TFC $3,000,000, TVC(Q) 120+ 25,000 Q2, in $ a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can...

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option I: TFC $7,500,000, TVC(Q) 100+ 10,000 Q, in $ Option ll: TFC $3,000,000, TVC(Q) 120+ 25,000 Q2, in $ a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can...

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option I: TFC $7,500,000, TVC(a) 100+ 10,000 Q2, in $. Option Il: TFC $6,000,000, TVC(Q) 120+ 25,000 Q2, in $. a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can...

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option I: TFC $7,500,000, TVC(a) 100+ 10,000 Q2, in $. Option Il: TFC $6,000,000, TVC(Q) 120+ 25,000 Q2, in $. a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can...

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option I: TFC $7,500,000, TVC(a) 100+ 10,000 Q2, in $. Option Il: TFC $6,000,000, TVC(Q) 120+ 25,000 Q2, in $. a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can...

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option I: TFC $7,500,000, TVC(a) 100+ 10,000 Q2, in $. Option Il: TFC $6,000,000, TVC(Q) 120+ 25,000 Q2, in $. a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can...

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option I: TFC $7,500,000, TVC(a) 100+ 10,000 Q2, in $. Option Il: TFC $6,000,000, TVC(Q) 120+ 25,000 Q2, in $. a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can...

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option I: TFC $7,500,000, TVC(a) 100+ 10,000 Q2, in $. Option Il: TFC $6,000,000, TVC(Q) 120+ 25,000 Q2, in $. a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can...

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option 1: TFC-$7,500,000, TVC(Q)-10Q+ 10,000 Q. in $. Option Il: TFC $3,000,000, TVC(a) 120+ 25,000 a2, in $. a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can use any...

1. (60 points) Company X is in a perfectly competitive industry and is in long run. That is, X has not picked its scale and fixed equipment yet. X has two scale options: Option 1: TFC-$7,500,000, TVC(Q)-10Q+ 10,000 Q. in $. Option Il: TFC $3,000,000, TVC(a) 120+ 25,000 a2, in $. a) (10 points) Plot ATC and MC for both options on the same graph with x-axis representing the quantity and y-axis representing MC and ATC. (You can use any...

10. Linda wants to open a T-shirt stand for Homecoming week. The school will license her a booth for $100. Each T-shirt from the store will cost her $4. Linda's average cost function will be: A) $100+ $4X B) $100/X + $4 C) $104/X D) $100/X+S4/X 11. Which of the following formulas is NOT correct? a. MC = TC/Q b. TVC = AVC * Q c. TC=(AFC + AVC)*Q d. AFC = TFC/Q e. ATC = AVC + (TFC/Q) 12....

10. Linda wants to open a T-shirt stand for Homecoming week. The school will license her a booth for $100. Each T-shirt from the store will cost her $4. Linda's average cost function will be: A) $100+ $4X B) $100/X + $4 C) $104/X D) $100/X+S4/X 11. Which of the following formulas is NOT correct? a. MC = TC/Q b. TVC = AVC * Q c. TC=(AFC + AVC)*Q d. AFC = TFC/Q e. ATC = AVC + (TFC/Q) 12....

5. Deriving the short-run supply curve Aa Aa Consider the perfectly competitive market for halogen ceiling lamps. The following graph shows the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves for a typical firm in the industry. COSTS Dollars per lampl 100 MC 90 80 70 60 ATC AVC 50 40 30 20 10 0 4 8 12 16 20 24 28 32 36 40 QUANTITY OF OUTPUT (Thousands of lamps) For each price in...

5. Deriving the short-run supply curve Aa Aa Consider the perfectly competitive market for halogen ceiling lamps. The following graph shows the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves for a typical firm in the industry. COSTS Dollars per lampl 100 MC 90 80 70 60 ATC AVC 50 40 30 20 10 0 4 8 12 16 20 24 28 32 36 40 QUANTITY OF OUTPUT (Thousands of lamps) For each price in...

2. (40 points) A monopolistically competitive company assembles and installs solar panels it imports at $10 per unit. All remaining costs of the company, denoted RC, is given by the following (as a function of per unit solar panel): RC(Q) = 1,000+5Q2 The demand faced by this company is given by Q-16.67-xP where P denotes the price, Q denotes the quantity and x is currently equal to 1/30. a) (10) points) What is the optimal production level, Q*, and what...

2. (40 points) A monopolistically competitive company assembles and installs solar panels it imports at $10 per unit. All remaining costs of the company, denoted RC, is given by the following (as a function of per unit solar panel): RC(Q) = 1,000+5Q2 The demand faced by this company is given by Q-16.67-xP where P denotes the price, Q denotes the quantity and x is currently equal to 1/30. a) (10) points) What is the optimal production level, Q*, and what...

Question 2 (15 points) Continuing your analysis of the competitive US manufacturing industry from Question 1, with demand of Q = 200-P and supply of Q. = P-20, suppose a technological innovation causes the supply curve to shift down by $20 for every given quantity Q. • Depict the original supply, the new supply, and the original demand curves on the usual P, Q diagram. Label all intercepts. Clearly indicate and label the new market equilibrium. 2/8/2 compass 20 Mlinois.edu/bbcswebdavipid-4037356-dt-con020%20ECON528%20M6...

Question 2 (15 points) Continuing your analysis of the competitive US manufacturing industry from Question 1, with demand of Q = 200-P and supply of Q. = P-20, suppose a technological innovation causes the supply curve to shift down by $20 for every given quantity Q. • Depict the original supply, the new supply, and the original demand curves on the usual P, Q diagram. Label all intercepts. Clearly indicate and label the new market equilibrium. 2/8/2 compass 20 Mlinois.edu/bbcswebdavipid-4037356-dt-con020%20ECON528%20M6...

Question 2 (18) In scenario 1, Kobus specialises in the production of two products, namely apples and honey. With reference to Humming Honey, answer the following questions: 2.1 With reference to the (per box) production of Humming Honey, differentiate between marginal cost, marginal revenue and marginal production. (3) 2.2. In the short run, the farmer's costs in the production of Humming Honey consist of fixed costs and variable costs. Using your knowledge of cost formulas and calculations, redraw and complete...

Question 2 (18) In scenario 1, Kobus specialises in the production of two products, namely apples and honey. With reference to Humming Honey, answer the following questions: 2.1 With reference to the (per box) production of Humming Honey, differentiate between marginal cost, marginal revenue and marginal production. (3) 2.2. In the short run, the farmer's costs in the production of Humming Honey consist of fixed costs and variable costs. Using your knowledge of cost formulas and calculations, redraw and complete...

Most questions answered within 3 hours.

-

What is responsible for Jupiter's enormous magnetic field?

asked 14 minutes ago -

At the end of the year, a company offered to buy 5,000 units of

a product...

asked 15 minutes ago -

Implement C++ program for each of the following.

Let D = [-48, -14, -8, 0, 1,...

asked 35 minutes ago -

Consider a labor market in which LD = 400 – 4W and LS = 250 +...

asked 49 minutes ago -

Let’s say you are teaching a typically-developing young child

how to eat with a spoon. Describe...

asked 33 minutes ago -

Ask Your Teacher A toy gun uses a spring to project a 5.6-g soft

rubber sphere...

asked 45 minutes ago -

*****DO NOT ANSWER THIS QUESTION IF YOU DON'T

KNOW*******

Question - PERSONAL DEVELOPMENT ESSAY and Detailed...

asked 52 minutes ago -

A certain rifle bullet has a mass of 5.25 g. Calculate the de

Broglie wavelength of...

asked 1 hour ago -

Research new software products that assist in project

communication management. Write a paper summarizing your findings,...

asked 1 hour ago -

the figure below to the left shows a beaker completely filled

with water. then a block...

asked 1 hour ago -

what is the duistribution channels of HUL in india and how they

distribute?

how is this...

asked 1 hour ago -

Batteries play an important role in our everyday lives. From

making many devices mobile, to allowing...

asked 1 hour ago