Homework Answers

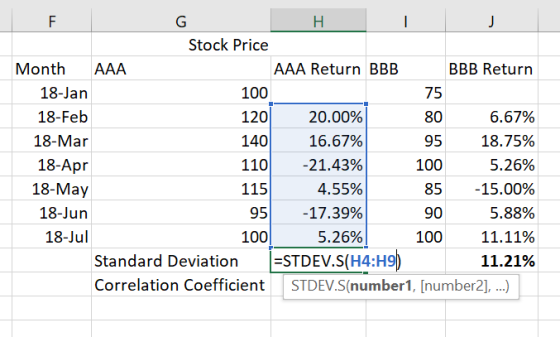

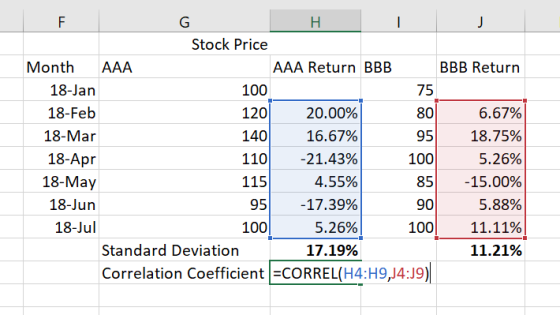

Hence, standard deviation of AAA is 17.19% and BBB is 11.21% and also correlation coefficient is 0.186

Hence, standard deviation of portfolio with 40% AAA and 60% BBB=sqrt of (0.4^2*17.19%^2+0.6^2*11.21%^2+2*0.4*0.6*0.186*0.1719*0.1121)

(ere w1=0.4, sigma

1=0.1719, w2=0.6, sigma 2= 0.1121, p1=0.186)

(ere w1=0.4, sigma

1=0.1719, w2=0.6, sigma 2= 0.1121, p1=0.186)

= 10.47%

Hence, standard deviation on monthly expected return would be 10.47%.

Add Answer to:

Given the following information estimate the standard deviation of a portfolio of 40% AAA and 60%...

Given the following information estimate the standard deviation of a portfolio of 40% AAA and 60%...

Given the following information estimate the standard deviation of a portfolio of 40% AAA and 60% BBB monthly returns. Enter your answer as a percent. Do not include the % sign. Round your final answer to two decimals. Stock Price Month AAA BBB Jan-18 100 75 Feb-18 120 80 Mar-18 140 95 Apr-18 110 100 May-18 115 85 Jun-18 95 90 Jul-18 100 100

1. Given the following information estimate the monthly expected return of a portfolio of 40% AAA...

1. Given the following information estimate the monthly expected return of a portfolio of 40% AAA and 60% BBB. Assume you purchase these shares in July 2018. Enter your answer as a percent. Do not include the % sign. Round your final answer to two decimals. 2. Given the following information estimate the standard deviation of a portfolio of 40% AAA and 60% BBB monthly returns. Stock Price Stock Price Month AAA BBB Jan-18 100 75 Feb-18 120 80 Mar-18...

Given the following information estimate the monthly expected return of a portfolio of 40% AAA and...

Given the following information estimate the monthly expected return of a portfolio of 40% AAA and 60% BBB. Assume you purchase these shares in July 2018. Enter your answer as a percent. Do not include the % sign. Round your final answer to two decimals. Stock Price Month AAA BBB Jan-18 100 75 Feb-18 120 80 Mar-18 140 95 Apr-18 110 100 May-18 115 85 Jun-18 95 90 Jul-18 100 100

Given the following information A. Estimate the monthly expected return of the AAA stock. B. Estimate the...

Given the following information A. Estimate the monthly expected return of the AAA stock. B. Estimate the standard deviation of BBB stock’s monthly returns C. Estimate the monthly expected return of a portfolio of 40% AAA and 60% BBB. Assume you purchase these shares in July 2018 D. Estimate the standard deviation of a portfolio of 40% AAA and 60% BBB monthly returns Enter your answer as a percent. Do not include the % sign. Round your final answer to two decimals....

Given the following information estimate the monthly expected return of the AAA stock. Enter your answer...

Given the following information estimate the monthly expected return of the AAA stock. Enter your answer as a percent. Round your final answer to two decimals. Estimate the standard deviation of BBB stock’s monthly returns. Enter your answer as a percent Stock Price Month AAA BBB Jan-18 100 75 Feb-18 120 80 Mar-18 140 95 Apr-18 110 100 May-18 115 85 Jun-18 95 90 Jul-18 100 100

Given the following information estimate the monthly expected return of the AAA stock. Enter your answer...

Given the following information estimate the monthly expected return of the AAA stock. Enter your answer as a percent. Do not include the % sign. Round your final answer to two decimals. Stock Price Month AAA BBB Jan-18 100 75 Feb-18 120 80 Mar-18 140 95 Apr-18 110 100 May-18 115 85 Jun-18 95 90 Jul-18 100 100

Given the following information estimate the monthly expected return of a portfolio of 40% AAA and...

Given the following information estimate the monthly expected return of a portfolio of 40% AAA and 60% BBB. Assume you purchase these shares in July 2018. Enter your answer as a percent. Do not include the % sign. Round your final answer to two decimals. Stock Price Month |ААА Jan-18 100 75 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 100

Given the following information estimate the monthly expected return of a portfolio of 40% AAA and 60% BBB. Assume you purchase these shares in July 2018. Enter your answer as a percent. Do not include the % sign. Round your final answer to two decimals. Stock Price Month |ААА Jan-18 100 75 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 100

Given the following data, what is the Mean Absolute Deviation (MAD): Month Demand Forecast Jan 100...

Given the following data, what is the Mean Absolute Deviation (MAD): Month Demand Forecast Jan 100 110 Feb 100 100 Mar 120 100 Apr 110 90 May 100 110 Jun 90 100 Jul 80 90 Aug 90 80 Sep 100 110 Oct 110 100 Nov 110 110 Dec 120 110 A. 10 B. 20 C. 30 D. 133.33

Given the following end of year prices and states of the economy. Combine the following assets...

Given the following end of year prices and states of the economy. Combine the following assets to form a portfolio with zero risk. A. What is the weight of AAA in your portfolio? B. What is the expected return of your portfolio? Enter your answer as a percent. Do not include the % sign. Round your answer to two decimals. Probability .25 .75 Price today Expansion Recession AAA 100 130 110 BBB 50 55 65

11. Consider the following returns of a portfolio: | Jan 2% | Feb 5% | Mar...

11. Consider the following returns of a portfolio: | Jan 2% | Feb 5% | Mar -6% | Apr 3% | May -2% | Jun 4% | A. Calculate the arithmetic average monthly return (1 point) B. Calculate the geometric average monthly return (1 point) C. Calculate the monthly variance (2 points)

Given the following information estimate the monthly expected return of a portfolio of 40% AAA and 60% BBB. Assume you purchase these shares in July 2018. Enter your answer as a percent. Do not include the % sign. Round your final answer to two decimals. Stock Price Month |ААА Jan-18 100 75 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 100

Given the following information estimate the monthly expected return of a portfolio of 40% AAA and 60% BBB. Assume you purchase these shares in July 2018. Enter your answer as a percent. Do not include the % sign. Round your final answer to two decimals. Stock Price Month |ААА Jan-18 100 75 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 100

Most questions answered within 3 hours.

-

A 0.25μF capacitor is charged to 50 V . It is then connected in

series with...

asked 10 minutes ago -

Calculate the current, I, through the batteries for:

- a 2-bulb parallel circuit

- How does...

asked 11 minutes ago -

Choose the sentence that uses correct punctuation.

1a. The prefatory parts of a report include the...

asked 17 minutes ago -

For the element arsenic, which one of the following sets of

quantum numbers could not apply...

asked 27 minutes ago -

Compare and contrast the architectures of 3 types of ADCs:

Flash, SAR, and pipelined. Use the...

asked 28 minutes ago -

Given P(A) = 0.40, P(B) = 0.50, P(A ∩ B) = 0.15. Which of the

following...

asked 32 minutes ago -

Explain changes in workforce participation for women with

children. What legislation exists related to work and...

asked 34 minutes ago -

How high must a pointed arch be if it is to span a

space 4.2 m...

asked 39 minutes ago -

A housepainter who weighs 750 N stands 0.6 m from one end of a

2.0 m...

asked 41 minutes ago -

Implement Singly Linked List detectLoop in Java.

It would check whether the linked list contains a...

asked 44 minutes ago -

A small mailbag is released from a helicopter that is descending

steadily at 2.10 m/s.

After...

asked 45 minutes ago -

Write a C – program that calls a user-defined function from

within main() that determines the...

asked 48 minutes ago