11A–1.

A summary of the controls for the revenue and cash receipts cycle of Keystone Computers & Networks, Inc., appears in this appendix.

For the following three controls over sales, indicate one type of error or fraud that the control serves to prevent or detect. Organize your solution as follows:

Control | Error or Fraud Controlled |

|

For the following three controls over cash receipts, indicate one type of error or fraud that the control serves to prevent or detect. Organize your solution as follows:

Control | Error or Fraud Controlled |

|

11A–2.

As indicated on the control risk assessment working paper Schedule IC-20 (its last section prior to the Assessed Level of Control Risk), the auditors identified two weaknesses in internal control over the revenue cycle of KCN. Describe the implications of each of the two weaknesses in terms of the type of errors or fraud that could result.

Risk of assessing control risk too low—5 percent

Tolerable deviation rate—15 percent

Expected deviation rate—1 percent

Describe the characteristic that a control must possess in order to be tested with audit sampling.

Assume that the auditors decided to use audit sampling to test the operating effectiveness of the procedures for matching sales invoices with delivery receipts. Determine the required sample size, using the following parameters.

Prepare a working paper similar to Schedule IC-15 documenting the planned audit procedure described in requirement (b).

11A–3.

As indicated on Schedule IC-15, the auditors decided to apply audit sampling to three controls for the revenue and cash receipts cycle.

A) Describe the characteristic that a control must possess in order to be tested with audit sampling.11B–2.

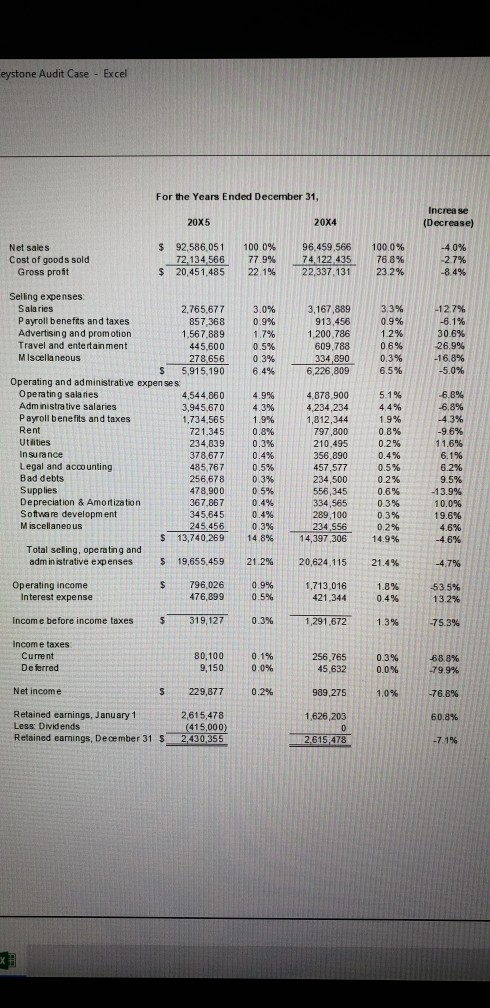

Assume that you have been assigned to the audit of Keystone after audit planning has occurred. Review the planning information in Appendix 6C of Chapter 6 and the audit plan for the accounts receivable and revenue (Schedule B-6). The manager on the engagement has given you the task of reviewing the monthly revenue report on Schedule B-11.

Based on your review of the report, describe any unusual relationships that might indicate a risk of misstatement of revenues based on your knowledge of the company derived from a review of the information on Schedule B-12.

Identify any procedures on the audit plan for receivables and revenue that might address the risk(s) identified in part (a).

Homework Answers

Revenue cycle controls

11A–1.

Sales controls:

| Control | Error or Fraud Controlled |

| Application controls are applied when customer orders are entered by the sales order clerk. | Controls errors in the delivery & billing of sales transactions |

| The computer assigns numbers to sales invoices when they are prepared. | Controls the recording of sales to ensure completeness & accuracy |

| Monthly statements are mailed to customers. | Controls the recording of false & inaccurate sales to customer accounts |

Cash receipt controls:

| Control | Error or Fraud Controlled |

| Cash receipts are prelisted by the receptionist. | Controls errors when recording of cash. |

| The accounting manager reconciles control totals generated by the accounts receivable computer program. | Controls the embezzlement of cash receipts & errors in accounts receivables records |

| The computer summaries of cash collections and cash sales are reconciled to prelistings of cash receipts and cash deposits by the accounting manager. | Controls the look of cash & recording of cash receipts and cash sales. |

Internal control weaknesses

11A–2.

1. Sales invoices are prepared and mailed prior to delivery of goods

Implications: Errors may occur where different quantities of goods may be delivered than what had been ordered, or goods may not be delivered at all. Sales and accounts receivable may be overstated for the year.

2. Accounts receivable are not written off on a regular basis

Implications: Receivables need to be monitored, otherwise the company may currently be selling goods on credit to customers who have poor credit. Allowance for Doubtful Accounts might end up being inadequate, with Bad Debt Expense being understated.

(A) Characteristic that a control must possess:

Audit sampling can be used when there is some sort of evidence of performance of the internal control procedure

- Completed document

- Initials of the person performing the procedure

Evidence of performance allows the auditors to determine whether the control procedure was applied to each item included in the sample.

(B) Sample Size required

Given parameters:

Risk of assessing control risk too low: 5%

Tolerable deviation rate: 15%

Expected deviation rate: 1%

30 with 1 allowable deviations

(C)

| KEYSTONE COMPUTERS & NETWORKS, INC. | ||||||

| Attributes Sampling Summary—Revenue Cycle | ||||||

| December 31, 20X5 | ||||||

| Objectives of test: | ||||||

| To test the operating effectiveness of the procedures for matching sales invoices with delivery receipts. | ||||||

| Test | Population | Size | ||||

| 1 | Sales Invoices | |||||

| Sampling unit: Individual reports | ||||||

| Random selection procedure: Random number table | ||||||

| Risk of assessing control risk too low: 5% | ||||||

| Sl.No. | Attributes Tested | Planning Parameters | Sample Results | |||

| Tolerable Deviation Rate | Expected Deviation Rate | Sample Size | Number of Deviations | Achieved Maximum Rate | ||

| 1 | Matching of sales invoices with delivery receipts | 15% | 1% | 30% | ||

Add Answer to:

11A–1.A summary of the controls for the revenue and cash receiptscycle of Keystone Computers...

14A–1. A summary of the controls for the acquisition cycle of Keystone Computers & Networks, Inc.,...

14A–1. A summary of the controls for the acquisition cycle of Keystone Computers & Networks, Inc., appears on pages 602–603. a. For the following three controls over the acquisition cycle, indicate one type of error or fraud that the control serves to prevent or detect. Organize your solution as follows: Required: LO 14-1, 3, 5, 6 Appendix 14A Problems Control Error or Fraud Controlled 1. Computer matches information from vendors’ invoice with purchase order and receiving data. 2. The computer...

The following audit procedures are included in the audit program of Holland Equipment, Inc. 1. Use...

The following audit procedures are included in the audit program of Holland Equipment, Inc. 1. Use audit software to examine journal entries in the sales, cash receipts, purchases, cash disbursements, payroll, and general journals for any amounts exceeding $1 million and for any entries with unusual account codings. Review related supporting documentation for reasonableness. 2. Examine the estimate for the Allowance for Doubtful Accounts recorded in the prior-year audited financial statements. Obtain information about receivable writeoffs recorded during the current...

Aman & Afdal is the auditor of Warisan Sdn Bhd. He is in charge of auditing...

Aman & Afdal is the auditor of Warisan Sdn Bhd. He is in charge of auditing the sales and collection cycle for the company which is a small fish distributor in East Malaysia. The company is respected for its high quality fish products, but their accounting office is perpetually neglected, and the sales department frequently makes errors in billing clients. In previous years, Aman & Afdal has found quite a few misstatements in billings, cash receipts, and accounts receivable. Like...

20) In a revenue cycle with proper controls, the involved in any cash handling activities. A)...

20) In a revenue cycle with proper controls, the involved in any cash handling activities. A) accounts receivable clerk, treasurer B) accounts receivable clerk; controller C) cashier, controller D) cashier; treasurer who reports to the is not 21) A serious exposure in the revenue eyele is loss of assets. What is the related applicable control procedure that address this exposure? A) shipping errors: reconciliation of sales order with picking ticket and packing B) theft of cash; segregation of duties and...

20) In a revenue cycle with proper controls, the involved in any cash handling activities. A) accounts receivable clerk, treasurer B) accounts receivable clerk; controller C) cashier, controller D) cashier; treasurer who reports to the is not 21) A serious exposure in the revenue eyele is loss of assets. What is the related applicable control procedure that address this exposure? A) shipping errors: reconciliation of sales order with picking ticket and packing B) theft of cash; segregation of duties and...

Evaluation and testing of controls at Hales Ltd Tyrone has provided a narrative of controls over...

Evaluation and testing of controls at Hales Ltd Tyrone has provided a narrative of controls over inventory at Hales Ltd and would like you to provide some advice on making the preliminary control risk assessment. Hales is a distributor of haircare products, including shampoos, conditioners and styling products throughout Australia. Hales uses an on-line ordering system. Hales does not manufacture any goods in house, instead, an inventory of raw materials is kept, with manufacturing being outsourced to other companies. Hales...

Evaluation and testing of controls at Hales Ltd Tyrone has provided a narrative of controls over...

Evaluation and testing of controls at Hales Ltd Tyrone has provided a narrative of controls over inventory at Hales Ltd and would like you to provide some advice on making the preliminary control risk assessment. Hales is a distributor of haircare products, including shampoos, conditioners and styling products throughout Australia. Hales uses an on-line ordering system. Hales does not manufacture any goods in house, instead, an inventory of raw materials is kept, with manufacturing being outsourced to other companies. Hales...

Which of the following matters would an auditor most likely consider to be a significant deficiency to be communicated to the audit committee

1. Which of the following matters would an auditor most likely consider to be a significant deficiency to be communicated to the audit committee? A. Management's failure to renegotiate unfavorable long-term purchase commitments.B. Recurring operating losses that may indicate going concern problems.C. Evidence of a lack of objectivity by those responsible for accounting decisions.D. Management's current plans to reduce its ownership equity in the entity. 2. After obtaining an understanding of internal control and arriving at a preliminary assessed level...

List the weaknesses and suggest improvements in internal controls related to revenue cycle. Identify weaknesses in...

List the weaknesses and

suggest improvements in internal controls related to revenue

cycle.

Identify weaknesses in the internal control structure relating

to the activities of

1) warehouse clerk

2)bookkeeper #1

3)bookkeeper #3

4)collection clerk

SALES CLERK WAREHOUSE CLERK BOOKKEEPER #1 BOOKKEEPER #2 COLLECTION CLERK RECEIVES CUSTOMER ORDER BY PHONE APPROVED SALES ORDER 1 SALES ORDER SALES ORDER INVOICE CUSTOMER CHECK FROM MAIL CLERK 2 1 INVOICE 3 PREPARES 4-COPY SALES ORDER PREPARES SHIPPING ADVICE AUTHORIZED CUSTOMER'S CREDIT MATCHES INV &...

List the weaknesses and

suggest improvements in internal controls related to revenue

cycle.

Identify weaknesses in the internal control structure relating

to the activities of

1) warehouse clerk

2)bookkeeper #1

3)bookkeeper #3

4)collection clerk

SALES CLERK WAREHOUSE CLERK BOOKKEEPER #1 BOOKKEEPER #2 COLLECTION CLERK RECEIVES CUSTOMER ORDER BY PHONE APPROVED SALES ORDER 1 SALES ORDER SALES ORDER INVOICE CUSTOMER CHECK FROM MAIL CLERK 2 1 INVOICE 3 PREPARES 4-COPY SALES ORDER PREPARES SHIPPING ADVICE AUTHORIZED CUSTOMER'S CREDIT MATCHES INV &...

E7.2 (LO 1, 2) C The following control procedures are used in Sheridan Company for cash receipts. Identify weaknesses i...

E7.2 (LO 1, 2) C The following control procedures are used in Sheridan Company for cash receipts. Identify weaknesses in internal control over cash receipts and suggest improvements. 1. To minimize the risk of robbery, cash in excess of $200 is stored in a locked metal box in the office manager's office until it is deposited in the bank. All employees know where the office manager keeps the key to the box. 2. The company has one cash register with...

E7.2 (LO 1, 2) C The following control procedures are used in Sheridan Company for cash receipts. Identify weaknesses in internal control over cash receipts and suggest improvements. 1. To minimize the risk of robbery, cash in excess of $200 is stored in a locked metal box in the office manager's office until it is deposited in the bank. All employees know where the office manager keeps the key to the box. 2. The company has one cash register with...

auditing Part Two: Multiple Choice Questions: (2.5 marks/ question) 1. To test the existence assertion for...

auditing

Part Two: Multiple Choice Questions: (2.5 marks/ question) 1. To test the existence assertion for recorded receivables, an auditor would select a sample from the A) Sales orders file. B) Customer purchase orders C) Accounts receivable subsidiary ledger D) Shipping documents (bill of lading) file. 2. When control risk for the existence assertion is assessed at a high level, which of the Gallerine is a likely effect with respect to the auditors' confirmation of receivables? A) The account balances...

auditing

Part Two: Multiple Choice Questions: (2.5 marks/ question) 1. To test the existence assertion for recorded receivables, an auditor would select a sample from the A) Sales orders file. B) Customer purchase orders C) Accounts receivable subsidiary ledger D) Shipping documents (bill of lading) file. 2. When control risk for the existence assertion is assessed at a high level, which of the Gallerine is a likely effect with respect to the auditors' confirmation of receivables? A) The account balances...

20) In a revenue cycle with proper controls, the involved in any cash handling activities. A) accounts receivable clerk, treasurer B) accounts receivable clerk; controller C) cashier, controller D) cashier; treasurer who reports to the is not 21) A serious exposure in the revenue eyele is loss of assets. What is the related applicable control procedure that address this exposure? A) shipping errors: reconciliation of sales order with picking ticket and packing B) theft of cash; segregation of duties and...

20) In a revenue cycle with proper controls, the involved in any cash handling activities. A) accounts receivable clerk, treasurer B) accounts receivable clerk; controller C) cashier, controller D) cashier; treasurer who reports to the is not 21) A serious exposure in the revenue eyele is loss of assets. What is the related applicable control procedure that address this exposure? A) shipping errors: reconciliation of sales order with picking ticket and packing B) theft of cash; segregation of duties and...

List the weaknesses and

suggest improvements in internal controls related to revenue

cycle.

Identify weaknesses in the internal control structure relating

to the activities of

1) warehouse clerk

2)bookkeeper #1

3)bookkeeper #3

4)collection clerk

SALES CLERK WAREHOUSE CLERK BOOKKEEPER #1 BOOKKEEPER #2 COLLECTION CLERK RECEIVES CUSTOMER ORDER BY PHONE APPROVED SALES ORDER 1 SALES ORDER SALES ORDER INVOICE CUSTOMER CHECK FROM MAIL CLERK 2 1 INVOICE 3 PREPARES 4-COPY SALES ORDER PREPARES SHIPPING ADVICE AUTHORIZED CUSTOMER'S CREDIT MATCHES INV &...

List the weaknesses and

suggest improvements in internal controls related to revenue

cycle.

Identify weaknesses in the internal control structure relating

to the activities of

1) warehouse clerk

2)bookkeeper #1

3)bookkeeper #3

4)collection clerk

SALES CLERK WAREHOUSE CLERK BOOKKEEPER #1 BOOKKEEPER #2 COLLECTION CLERK RECEIVES CUSTOMER ORDER BY PHONE APPROVED SALES ORDER 1 SALES ORDER SALES ORDER INVOICE CUSTOMER CHECK FROM MAIL CLERK 2 1 INVOICE 3 PREPARES 4-COPY SALES ORDER PREPARES SHIPPING ADVICE AUTHORIZED CUSTOMER'S CREDIT MATCHES INV &...

E7.2 (LO 1, 2) C The following control procedures are used in Sheridan Company for cash receipts. Identify weaknesses in internal control over cash receipts and suggest improvements. 1. To minimize the risk of robbery, cash in excess of $200 is stored in a locked metal box in the office manager's office until it is deposited in the bank. All employees know where the office manager keeps the key to the box. 2. The company has one cash register with...

E7.2 (LO 1, 2) C The following control procedures are used in Sheridan Company for cash receipts. Identify weaknesses in internal control over cash receipts and suggest improvements. 1. To minimize the risk of robbery, cash in excess of $200 is stored in a locked metal box in the office manager's office until it is deposited in the bank. All employees know where the office manager keeps the key to the box. 2. The company has one cash register with...

auditing

Part Two: Multiple Choice Questions: (2.5 marks/ question) 1. To test the existence assertion for recorded receivables, an auditor would select a sample from the A) Sales orders file. B) Customer purchase orders C) Accounts receivable subsidiary ledger D) Shipping documents (bill of lading) file. 2. When control risk for the existence assertion is assessed at a high level, which of the Gallerine is a likely effect with respect to the auditors' confirmation of receivables? A) The account balances...

auditing

Part Two: Multiple Choice Questions: (2.5 marks/ question) 1. To test the existence assertion for recorded receivables, an auditor would select a sample from the A) Sales orders file. B) Customer purchase orders C) Accounts receivable subsidiary ledger D) Shipping documents (bill of lading) file. 2. When control risk for the existence assertion is assessed at a high level, which of the Gallerine is a likely effect with respect to the auditors' confirmation of receivables? A) The account balances...

Most questions answered within 3 hours.

-

Using MARS simulator, write MIPS programs according to

the following scenarios: Receive a positive integer number...

asked 13 minutes ago -

An object in front of a concave mirror has a real image that is

11.5 cm...

asked 27 minutes ago -

Consider the reaction, C3 H8 + O2 --> CO2 + H2O. How many

moles of O2...

asked 2 hours ago -

You and your opponent both roll a fair die. If you both roll the

same number,...

asked 2 hours ago -

In a study of the accuracy of fast food drive-through orders,

Restaurant A had 257 accurate...

asked 2 hours ago -

Identify and describe in detail the four categories of

institutions that could be included in a...

asked 2 hours ago -

In python

class Customer:

def __init__(self, customer_id, last_name, first_name, phone_number, address):

self._customer_id = int(customer_id)

self._last_name =...

asked 2 hours ago -

What is an example of a limitation in implementing a new

ERP system and how it...

asked 2 hours ago -

In a section of 9.7cm of an artery with a radius of 2.6mm there

is a...

asked 2 hours ago -

the two carboxylic acid groups of aspartic acid have different

acidities with pKa values of 2.1...

asked 2 hours ago -

Would CuCO3 aqueous salt combined with calcium chloride

form a solid precipitate? If so, what would...

asked 2 hours ago -

How do ECM Solutions assist in embedding a culture of continuous

improvement in an organization? (Project...

asked 3 hours ago