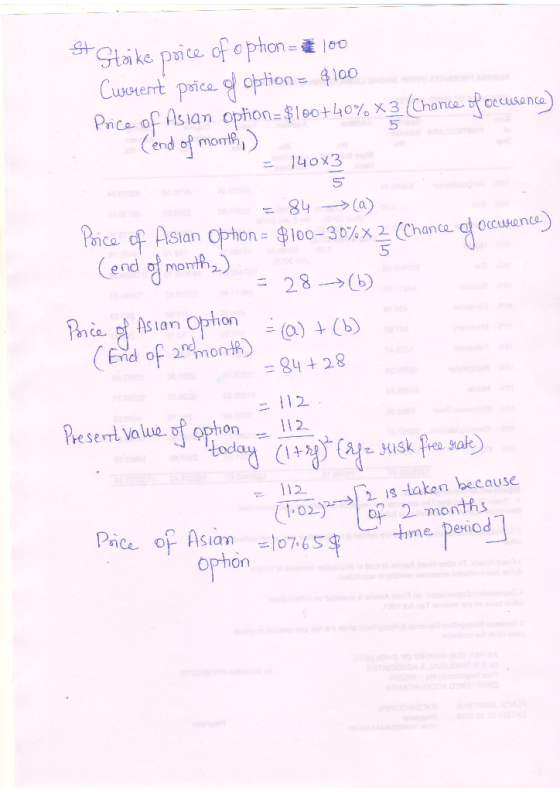

Asian call option with strike equal to 100. Find the price of an Asian 2 month...

Homework Answers

Add Answer to:

Asian call option with strike equal to 100. Find the price of an

Asian 2 month...

4. An Asian option is an option whose payoffs depend on the average price of the...

4. An Asian option is an option whose payoffs depend on the average price of the un- derlying asset over a certain period of time (instead of the price at maturity in the case of standard options). Early exercise of the option is not allowed. For instance, consider the payoff of an Asian Call option at maturity (in three months) on a stock ABC that does not pay dividends : Cz = max ( Si + S2 + S3 -...

4. An Asian option is an option whose payoffs depend on the average price of the un- derlying asset over a certain period of time (instead of the price at maturity in the case of standard options). Early exercise of the option is not allowed. For instance, consider the payoff of an Asian Call option at maturity (in three months) on a stock ABC that does not pay dividends : Cz = max ( Si + S2 + S3 -...

Consider a six-month call option written on €100,000 with a strike price of $1.00 = €1.00....

Consider a six-month call option written on €100,000 with a strike price of $1.00 = €1.00. The current exchange rate is $1.25 = €1.00; The U.S. risk-free rate is 5% over the period and the euro-zone risk-free rate is 4%. The volatility of the underlying asset is 10.7 percent. What is value of d1 using the Black-Scholes model? The answer is 3.053 How do I get that?

A stock's current price is $72. A call option with 3-month maturity and strike price of...

A stock's current price is $72. A call option with 3-month maturity and strike price of $ 68 is trading for 6, while a put with the same strike and expiration is trading for $20. The risk free rate is 2%. How much arbitrage profit can you make by selling the put and purchasing a synthetic put? (Provide your answer rounded to two decimals.) You have purchased a put option for $ 11 three months ago. The option's strike price...

(i) The current stock price is 100. The call option premium with a strike price 100...

(i) The current stock price is 100. The call option premium with a strike price 100 is 8. The effective risk-free interest rate is 2%. The stock pays no dividend. What is the price of a put option with strike price 100? (Both options mature in 3 months.) (ii) The 3-month forward price is 50. The put option premium with a strike price 52 is 3 and the put option matures in 3 months. The risk-free interest rate is 4%...

Calculate the Black and Scholes price of a European Call option, with a strike of $120...

Calculate the Black and Scholes price of a European Call option, with a strike of $120 and a time to expiry of 6 months. The underlying currentely trades at $100 and has a (future) volatility of 23% p.a. Assume a risk free rate of 1% p.a. 0.07 0.08 O 1.20 O 1.24

Calculate the Black and Scholes price of a European Call option, with a strike of $120 and a time to expiry of 6 months. The underlying currentely trades at $100 and has a (future) volatility of 23% p.a. Assume a risk free rate of 1% p.a. 0.07 0.08 O 1.20 O 1.24

5. Consider a European call option on the stock of XYZ, with a strike price of...

5. Consider a European call option on the stock of XYZ, with a strike price of $25 and two months to expiration. The stock pays continuous dividends at the annual yield rate of 5%. The annual continuously compounded risk free interst rate is 11%. The stock currently trades for $23 per share. Suppose that in two months, the stock will trade for either S18 per share or $29 per share. Use the one-period binomial option pricing model to find today's...

5. Consider a European call option on the stock of XYZ, with a strike price of $25 and two months to expiration. The stock pays continuous dividends at the annual yield rate of 5%. The annual continuously compounded risk free interst rate is 11%. The stock currently trades for $23 per share. Suppose that in two months, the stock will trade for either S18 per share or $29 per share. Use the one-period binomial option pricing model to find today's...

The price of a call option with a strike of $100 is $10. The price of...

The price of a call option with a strike of $100 is $10. The price of a put option with a strike of $100 is $5. Interest rates are 0 and the current price of the underlying is $100. Can you make an arbitrage profit? If so how? Describe the trade and your pay offs in detail?

The price of a call option with a strike of $100 is $10. The price of...

The price of a call option with a strike of $100 is $10. The price of a put option with a strike of $100 is $5. Interest rates are 0 and the current price of the underlying is $100. Can you make an arbitrage profit? If so how? Describe the trade and your pay offs in detail?

The current stock price is 100. The call option premium with a strike price 100 is...

The current stock price is 100. The call option premium with a strike price 100 is 8. The effective risk-free interest rate is 2%. The stock pays no dividend. What is the price of a put option with strike price 100? (Both options mature in 3 months.)

4. A call option currently sells for $7.75. It has a strike price of $85 and...

4. A call option currently sells for $7.75. It has a strike price of $85 and seven months to maturity. A put with the same strike and expiration date sells for $6.00. If the risk-free interest rate is 3.2 percent, what is the current stock price? 5. Suppose you buy one SPX call option contract with a strike of 1300. At maturity, the S&P 500 Index is at 1321. What is your net gain or loss if the premium you...

4. An Asian option is an option whose payoffs depend on the average price of the un- derlying asset over a certain period of time (instead of the price at maturity in the case of standard options). Early exercise of the option is not allowed. For instance, consider the payoff of an Asian Call option at maturity (in three months) on a stock ABC that does not pay dividends : Cz = max ( Si + S2 + S3 -...

4. An Asian option is an option whose payoffs depend on the average price of the un- derlying asset over a certain period of time (instead of the price at maturity in the case of standard options). Early exercise of the option is not allowed. For instance, consider the payoff of an Asian Call option at maturity (in three months) on a stock ABC that does not pay dividends : Cz = max ( Si + S2 + S3 -...

Calculate the Black and Scholes price of a European Call option, with a strike of $120 and a time to expiry of 6 months. The underlying currentely trades at $100 and has a (future) volatility of 23% p.a. Assume a risk free rate of 1% p.a. 0.07 0.08 O 1.20 O 1.24

Calculate the Black and Scholes price of a European Call option, with a strike of $120 and a time to expiry of 6 months. The underlying currentely trades at $100 and has a (future) volatility of 23% p.a. Assume a risk free rate of 1% p.a. 0.07 0.08 O 1.20 O 1.24

5. Consider a European call option on the stock of XYZ, with a strike price of $25 and two months to expiration. The stock pays continuous dividends at the annual yield rate of 5%. The annual continuously compounded risk free interst rate is 11%. The stock currently trades for $23 per share. Suppose that in two months, the stock will trade for either S18 per share or $29 per share. Use the one-period binomial option pricing model to find today's...

5. Consider a European call option on the stock of XYZ, with a strike price of $25 and two months to expiration. The stock pays continuous dividends at the annual yield rate of 5%. The annual continuously compounded risk free interst rate is 11%. The stock currently trades for $23 per share. Suppose that in two months, the stock will trade for either S18 per share or $29 per share. Use the one-period binomial option pricing model to find today's...

Most questions answered within 3 hours.

-

Can you figure out if any R functions used to subset a time

series 1 or...

asked 20 minutes ago -

Which of the following is correct?

A. APC + MPS = 1

B. APS + MPS...

asked 32 minutes ago -

Given a regression sum of squares equal to 2373.59 and a total

sum of squares equal...

asked 2 hours ago -

Compare and contrast the linear motion and angular motion

equations F ma and . That is,...

asked 1 hour ago -

Now that this course has taken you on a journey of introduction

to the world of...

asked 1 hour ago -

The sandwich maker of the EE-Cole-Eye Sandwich Truck was just

fired (for a reason described below)...

asked 4 hours ago -

Name the following coordination compounds using systematic

nomenclature.

1. [Co(H2O)6]Cl2:

2. [Cr(NH3)6](NO3)3:

3. K4[Fe(CN)6]:

4. Na[Au(CN)4]:...

asked 3 hours ago -

Propose an efficient synthesis of 2-Bromo-5-nitrotoluene from

benzene. Hint: 3 steps. Consider directing effects of substituents....

asked 6 hours ago -

This assignment will explore the impact of corporate decisions

on a local versus a global perspective....

asked 5 hours ago -

Given the function below, F(w,x,y,z)= x’z+w’z’+w’y

a) draw a logic diagram for an implementation which uses...

asked 4 hours ago -

Most political philosophers believe we have a duty to obey laws,

even if the laws in...

asked 5 hours ago -

Which of the following are common negotiation outcome

mistakes?

a. Leave money on the table b....

asked 5 hours ago