Gray, Stone, and Lawson open an accounting practice on January 1, 2016, in San Diego, California, to be operated as a partnership. Gray and Stone will serve as the senior partners because of their years of experience. To establish the business, Gray, Stone, and Lawson contribute cash and other properties valued at $420,000, $390,000, and $195,000, respectively. An articles of partnership agreement is drawn up. It has the following stipulations:

- Personal drawings are allowed annually up to an amount equal to 10 percent of the beginning capital balance for the year.

- Profits and losses are allocated according to the following plan:

- A salary allowance is credited to each partner in an amount equal to $7 per billable hour worked by that individual during the year.

- Interest is credited to the partners’ capital accounts at the rate of 12 percent of the average monthly balance for the year (computed without regard for current income or drawings).

- An annual bonus is to be credited to Gray and Stone. Each bonus is to be 10 percent of net income after subtracting the bonus, the salary allowance, and the interest. Also included in the agreement is the provision that there will be no bonus if there is a net loss or if salary and interest result in a negative remainder of net income to be distributed.

- Any remaining partnership profit or loss is to be divided evenly among all partners.

Because of financial shortfalls encountered in getting the business started, Gray invests an additional $9,400 on May 1, 2016. On January 1, 2017, the partners allow Monet to buy into the partnership. Monet contributes cash directly to the business in an amount equal to a 20 percent interest in the book value of the partnership property subsequent to this contribution. The partnership agreement as to splitting profits and losses is not altered upon Monet’s entrance into the firm; the general provisions continue to be applicable.

The billable hours for the partners during the first three years of operation follow:

| 2016 | 2017 | 2018 | |

| Gray | 1,870 | 3,900 | 2,110 |

| Stone | 1,650 | 2,400 | 1,830 |

| Lawson | 3,400 | 1,590 | 1,520 |

| Monet | 0 | 1,400 | 1,790 |

The partnership reports net income for 2016 through 2018 as follows:

| 2016 | $ | 97,000 |

| 2017 | (41,400) | |

| 2018 | 224,000 | |

Each partner withdraws the maximum allowable amount each year.

-

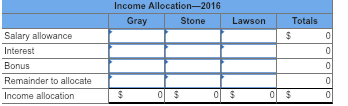

Determine the allocation of income for each of these three years. (picture format below, complete table for all three years)

-

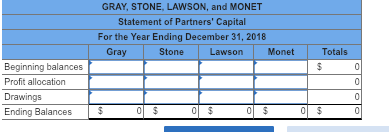

Prepare in appropriate form a statement of partners’ capital for the year ending December 31, 2018. (picture format below)

Homework Answers

Part A

Income Allocation—2016

|

Gray |

Stone |

Lawson |

Total |

|

|

Salary allowance |

13090 |

11550 |

23800 |

48440 |

|

Interest |

51152 |

46800 |

23400 |

121352 |

|

Bonus |

0 |

0 |

0 |

0 |

|

Remaining loss |

(24264) |

(24264) |

(24264) |

(72792) |

|

Profit allocation |

39978 |

34086 |

22936 |

97000 |

Explanation:

|

Gray |

Stone |

Lawson |

Total |

|

|

Salary allowance |

13090 (1870*7) |

11550 (1650*7) |

23800 (3400*7) |

48440 |

|

Interest |

51152 ((420000*12%*4/12)+(429400*12%*8/12)) |

46800 (390000*12%) |

23400 (195000*12%) |

121352 |

|

Bonus |

0 |

0 |

0 |

0 |

|

Remaining loss (97000-48440-121352 = -72792) |

(24264) (-72792/3) |

(24264) (-72792/3) |

(24264) (-72792/3) |

(72792) |

|

Profit allocation |

39978 |

34086 |

22936 |

97000 |

Bonus is not applicable here because salary and interest would necessitate a negative bonus

|

Gray |

Stone |

Lawson |

Total |

|

|

Beginning contributions |

420000 |

390000 |

195000 |

1005000 |

|

Added Investment |

9400 |

0 |

0 |

9400 |

|

Profit allocation |

39978 |

34086 |

22936 |

97000 |

|

Drawing (10% of beginning capital) |

(42000) |

(39000) |

(19500) |

100500 |

|

Ending balances |

427378 |

385086 |

198436 |

1010900 |

Monet's Investment = 20%* ($1010900 + Monet's Investment)

0.80 Monet's Investment = 202180

Monet's Investment = 252725

Part A

Income Allocation—2017

|

Gray |

Stone |

Lawson |

Monet |

Total |

|

|

Salary allowance |

27300 |

16800 |

11130 |

9800 |

65030 |

|

Interest |

51285 |

46210 |

23812 |

30327 |

151634 |

|

Bonus |

0 |

0 |

0 |

0 |

0 |

|

Remaining loss |

(64516) |

(64516) |

(64516) |

(64516) |

(258064) |

|

Loss allocation |

14069 |

(1506) |

(29574) |

(24389) |

(41400) |

Explanation:

|

Gray |

Stone |

Lawson |

Monet |

Total |

|

|

Salary allowance |

27300 (3900*7) |

16800 (2400*7) |

11130 (1590*7) |

9800 (1400*7) |

65030 |

|

Interest |

51285 (427378*12%) |

46210 (385086*12%) |

23812 (198436*12%) |

30327 (252725*12%) |

151634 |

|

Bonus |

0 |

0 |

0 |

0 |

0 |

|

Remaining loss (-41400-65030-151634) = -258064 |

(64516) (-258064/4) |

(64516) (-258064/4) |

(64516) (-258064/4) |

(64516) (-258064/4) |

(258064) |

|

Loss allocation |

14069 |

(1506) |

(29574) |

(24389) |

(41400) |

|

Gray |

Stone |

Lawson |

Monet |

Total |

|

|

Beginning contributions |

427378 |

385086 |

198436 |

252725 |

1263625 |

|

Loss allocation |

14069 |

(1506) |

(29574) |

(24389) |

(41400) |

|

Drawing (10% of beginning capital) |

(42738) |

(38509) |

(19844) |

(25273) |

(126364) |

|

Ending balances |

398709 |

345071 |

149018 |

203063 |

1095861 |

Part A

Income Allocation—2018

|

Gray |

Stone |

Lawson |

Monet |

Total |

|

|

Salary allowance |

14770 |

12810 |

10640 |

12530 |

50750 |

|

Interest |

47845 |

41409 |

17882 |

24368 |

131503 |

|

Bonus |

3479 |

3479 |

6958 |

||

|

Remaining profit |

8697 |

8697 |

8697 |

8698 |

22610 |

|

Profit allocation |

74791 |

66395 |

37219 |

45595 |

224000 |

Explanation:

|

Gray |

Stone |

Lawson |

Monet |

Total |

|

|

Salary allowance |

14770 (2110*7) |

12810 (1830*7) |

10640 (1520*7) |

12530 (1790*7) |

50750 |

|

Interest |

47845 (398709*12%) |

41409 (345071*12%) |

17882 (149018*12%) |

24368 (203063*12%) |

131503 |

|

Bonus |

3479 |

3479 |

6958 |

||

|

Remaining profit (224000-50750-131503-6958) = 34789 |

8697 |

8697 |

8697 |

8698 |

22610 |

|

Profit allocation |

74791 |

66395 |

37219 |

45595 |

224000 |

Bonus = 20% (Net income – Salary – Interest – Bonus)

B = 0.2 ($224000 – $50750 – $131503 – B)

B = 0.2 ($41747 – B)

B = $8349.40 – .2B

1.2 B = $8349.40

B = $6958 (or $3479 per person)

Part B

GRAY, STONE, LAWSON and MONET

Statement of partner’s capital

For the year ending December 31, 2018

|

Gray |

Stone |

Lawson |

Monet |

Total |

|

|

Beginning balances |

398709 |

345071 |

149018 |

203063 |

1095861 |

|

Profit allocation |

74791 |

66395 |

37219 |

45595 |

224000 |

|

Drawings (10% of beginning capital) |

(39871) |

(34507) |

(14902) |

(20306) |

-109589 |

|

Ending balances |

433629 |

376959 |

171335 |

228352 |

1210275 |

Add Answer to:

Gray, Stone, and Lawson open an accounting practice on January

1, 2016, in San Diego, California,...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016, in San Diego, California,...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016, in San Diego, California, to be operated as a partnership. Gray and Stone will serve as the senior partners because of their years of experience. To establish the business, Gray, Stone, and Lawson contribute cash and other properties valued at $290,000, $260,000, and $130,000, respectively. An articles of partnership agreement is drawn up. It has the following stipulations: Personal drawings are allowed annually up to an amount equal...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016, in San Diego, California,...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016, in San Diego, California, to be operated as a partnership. Gray and Stone will serve as the senior partners because of their years of experience. To establish the business, Gray, Stone, and Lawson contribute cash and other properties valued at $410,000, $340,000, and $170,000, respectively. An articles of partnership agreement is drawn up. It has the following stipulations: Personal drawings are allowed annually up to an amount equal...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016, in San Diego, California,...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016, in San Diego, California, to be operated as a partnership. Gray and Stone will serve as the senior partners because of their years of experience. To establish the business, Gray, Stone, and Lawson contribute cash and other properties valued at $340,000, $310,000, and $155,000, respectively. An articles of partnership agreement is drawn up. It has the following stipulations: Personal drawings are allowed annually up to an amount equal...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016 in San Diego, California,...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016 in San Diego, California, to be operated as a partnership. Gray and Stone will serve as the senior partners because of their years of experience. To establish the business, Gray, Stone, and Lawson contribute cash and other properties valued at $280,000, $250,000, and $125,000, respectively. An articles of partnership agreement is drawn up. It has the following stipulations: • Personal drawings are allowed annually up to an amount...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016 in San Diego, California, to be operated as a partnership. Gray and Stone will serve as the senior partners because of their years of experience. To establish the business, Gray, Stone, and Lawson contribute cash and other properties valued at $280,000, $250,000, and $125,000, respectively. An articles of partnership agreement is drawn up. It has the following stipulations: • Personal drawings are allowed annually up to an amount...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016, in San Diego, California,...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016, in San Diego, California, to be operated as a partnership. Gray and Stone will serve as the senior partners because of their years of experience. To establish the business, Gray, Stone, and Lawson contribute cash and other properties valued at $270,000, $240,000, and $120,000, respectively. An articles of partnership agreement is drawn up. It has the following stipulations: Personal drawings are allowed annually up to an amount equal...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016, in San Diego, California,...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016, in San Diego, California, to be operated as a partnership. Gray and Stone will serve as the senior partners because of their years of experience. To establish the business, Gray, Stone, and Lawsoń contribute cash and other properties valued at $210,000, $180,000, and $90,000, respectively. An articles of partnership agreement is drawn up. It has the following stipulations: Personal drawings are allowed annually up to an amount equal...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016, in San Diego, California, to be operated as a partnership. Gray and Stone will serve as the senior partners because of their years of experience. To establish the business, Gray, Stone, and Lawsoń contribute cash and other properties valued at $210,000, $180,000, and $90,000, respectively. An articles of partnership agreement is drawn up. It has the following stipulations: Personal drawings are allowed annually up to an amount equal...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016, in San Diego, California,...

Gray, Stone, and Lawson open an accounting practice on January

1, 2016, in San Diego, California, to be operated as a partnership.

Gray and Stone will serve as the senior partners because of their

years of experience. To establish the business, Gray, Stone, and

Lawson contribute cash and other properties valued at $280,000,

$250,000, and $125,000, respectively. An articles of partnership

agreement is drawn up. It has the following stipulations:

Personal drawings are allowed annually up to an amount equal...

Gray, Stone, and Lawson open an accounting practice on January

1, 2016, in San Diego, California, to be operated as a partnership.

Gray and Stone will serve as the senior partners because of their

years of experience. To establish the business, Gray, Stone, and

Lawson contribute cash and other properties valued at $280,000,

$250,000, and $125,000, respectively. An articles of partnership

agreement is drawn up. It has the following stipulations:

Personal drawings are allowed annually up to an amount equal...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016, in San Diego, California,...

Gray, Stone, and Lawson open an accounting practice on January

1, 2016, in San Diego, California, to be operated as a partnership.

Gray and Stone will serve as the senior partners because of their

years of experience. To establish the business, Gray, Stone, and

Lawson contribute cash and other properties valued at $270,000,

$240,000, and $120,000, respectively. An articles of partnership

agreement is drawn up. It has the following stipulations:

Personal drawings are allowed annually up to an amount equal...

Gray, Stone, and Lawson open an accounting practice on January

1, 2016, in San Diego, California, to be operated as a partnership.

Gray and Stone will serve as the senior partners because of their

years of experience. To establish the business, Gray, Stone, and

Lawson contribute cash and other properties valued at $270,000,

$240,000, and $120,000, respectively. An articles of partnership

agreement is drawn up. It has the following stipulations:

Personal drawings are allowed annually up to an amount equal...

l Gray, Stone, and Lawson open an accounting practice on January 1, 2016 in San Diego, California, to be operated as...

l

Gray, Stone, and Lawson open an accounting practice on January 1, 2016 in San Diego, California, to be operated as a partnership Gray and Stone will serve as the senior partners because of their years of experience. To establish the business, Gray, Stone, and Lawson contribute cash and other properties valued at $210,000, $180,000, and $90,000, respectively. An articles of partnership agreement is drawn up. It has the following stipulations: • Personal drawings are allowed annually up to an...

l

Gray, Stone, and Lawson open an accounting practice on January 1, 2016 in San Diego, California, to be operated as a partnership Gray and Stone will serve as the senior partners because of their years of experience. To establish the business, Gray, Stone, and Lawson contribute cash and other properties valued at $210,000, $180,000, and $90,000, respectively. An articles of partnership agreement is drawn up. It has the following stipulations: • Personal drawings are allowed annually up to an...

Exercise 15-5 On January 1, 2016, Tony and Jon formed T&J Personal Financial Planning with capital...

Exercise 15-5

On January 1, 2016, Tony and Jon formed T&J Personal

Financial Planning with capital investments of $482,900 and

$339,900, respectively. The partners wanted to draft a profit and

loss agreement that would reward each individual for the resources

invested in the partnership. Accordingly, the partnership agreement

provides that profits are to be allocated as follows:

1.

Annual salaries of $41,400 and $65,100 are granted to Tony and

Jon, respectively.

2.

In addition to the salary, Jon is entitled...

Exercise 15-5

On January 1, 2016, Tony and Jon formed T&J Personal

Financial Planning with capital investments of $482,900 and

$339,900, respectively. The partners wanted to draft a profit and

loss agreement that would reward each individual for the resources

invested in the partnership. Accordingly, the partnership agreement

provides that profits are to be allocated as follows:

1.

Annual salaries of $41,400 and $65,100 are granted to Tony and

Jon, respectively.

2.

In addition to the salary, Jon is entitled...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016 in San Diego, California, to be operated as a partnership. Gray and Stone will serve as the senior partners because of their years of experience. To establish the business, Gray, Stone, and Lawson contribute cash and other properties valued at $280,000, $250,000, and $125,000, respectively. An articles of partnership agreement is drawn up. It has the following stipulations: • Personal drawings are allowed annually up to an amount...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016 in San Diego, California, to be operated as a partnership. Gray and Stone will serve as the senior partners because of their years of experience. To establish the business, Gray, Stone, and Lawson contribute cash and other properties valued at $280,000, $250,000, and $125,000, respectively. An articles of partnership agreement is drawn up. It has the following stipulations: • Personal drawings are allowed annually up to an amount...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016, in San Diego, California, to be operated as a partnership. Gray and Stone will serve as the senior partners because of their years of experience. To establish the business, Gray, Stone, and Lawsoń contribute cash and other properties valued at $210,000, $180,000, and $90,000, respectively. An articles of partnership agreement is drawn up. It has the following stipulations: Personal drawings are allowed annually up to an amount equal...

Gray, Stone, and Lawson open an accounting practice on January 1, 2016, in San Diego, California, to be operated as a partnership. Gray and Stone will serve as the senior partners because of their years of experience. To establish the business, Gray, Stone, and Lawsoń contribute cash and other properties valued at $210,000, $180,000, and $90,000, respectively. An articles of partnership agreement is drawn up. It has the following stipulations: Personal drawings are allowed annually up to an amount equal...

Gray, Stone, and Lawson open an accounting practice on January

1, 2016, in San Diego, California, to be operated as a partnership.

Gray and Stone will serve as the senior partners because of their

years of experience. To establish the business, Gray, Stone, and

Lawson contribute cash and other properties valued at $280,000,

$250,000, and $125,000, respectively. An articles of partnership

agreement is drawn up. It has the following stipulations:

Personal drawings are allowed annually up to an amount equal...

Gray, Stone, and Lawson open an accounting practice on January

1, 2016, in San Diego, California, to be operated as a partnership.

Gray and Stone will serve as the senior partners because of their

years of experience. To establish the business, Gray, Stone, and

Lawson contribute cash and other properties valued at $280,000,

$250,000, and $125,000, respectively. An articles of partnership

agreement is drawn up. It has the following stipulations:

Personal drawings are allowed annually up to an amount equal...

Gray, Stone, and Lawson open an accounting practice on January

1, 2016, in San Diego, California, to be operated as a partnership.

Gray and Stone will serve as the senior partners because of their

years of experience. To establish the business, Gray, Stone, and

Lawson contribute cash and other properties valued at $270,000,

$240,000, and $120,000, respectively. An articles of partnership

agreement is drawn up. It has the following stipulations:

Personal drawings are allowed annually up to an amount equal...

Gray, Stone, and Lawson open an accounting practice on January

1, 2016, in San Diego, California, to be operated as a partnership.

Gray and Stone will serve as the senior partners because of their

years of experience. To establish the business, Gray, Stone, and

Lawson contribute cash and other properties valued at $270,000,

$240,000, and $120,000, respectively. An articles of partnership

agreement is drawn up. It has the following stipulations:

Personal drawings are allowed annually up to an amount equal...

l

Gray, Stone, and Lawson open an accounting practice on January 1, 2016 in San Diego, California, to be operated as a partnership Gray and Stone will serve as the senior partners because of their years of experience. To establish the business, Gray, Stone, and Lawson contribute cash and other properties valued at $210,000, $180,000, and $90,000, respectively. An articles of partnership agreement is drawn up. It has the following stipulations: • Personal drawings are allowed annually up to an...

l

Gray, Stone, and Lawson open an accounting practice on January 1, 2016 in San Diego, California, to be operated as a partnership Gray and Stone will serve as the senior partners because of their years of experience. To establish the business, Gray, Stone, and Lawson contribute cash and other properties valued at $210,000, $180,000, and $90,000, respectively. An articles of partnership agreement is drawn up. It has the following stipulations: • Personal drawings are allowed annually up to an...

Exercise 15-5

On January 1, 2016, Tony and Jon formed T&J Personal

Financial Planning with capital investments of $482,900 and

$339,900, respectively. The partners wanted to draft a profit and

loss agreement that would reward each individual for the resources

invested in the partnership. Accordingly, the partnership agreement

provides that profits are to be allocated as follows:

1.

Annual salaries of $41,400 and $65,100 are granted to Tony and

Jon, respectively.

2.

In addition to the salary, Jon is entitled...

Exercise 15-5

On January 1, 2016, Tony and Jon formed T&J Personal

Financial Planning with capital investments of $482,900 and

$339,900, respectively. The partners wanted to draft a profit and

loss agreement that would reward each individual for the resources

invested in the partnership. Accordingly, the partnership agreement

provides that profits are to be allocated as follows:

1.

Annual salaries of $41,400 and $65,100 are granted to Tony and

Jon, respectively.

2.

In addition to the salary, Jon is entitled...

Most questions answered within 3 hours.

-

The activation energy for a given reaction is 50.3 kJ/mol. If

the rate constant for the...

asked 32 minutes ago -

An entomologist discovers a dung beetle rolling a ball of dung

along the ground, and decides...

asked 2 hours ago -

Humans have used horses for transportation for millions of

years. Therefore, they will use horses for...

asked 4 hours ago -

The following are the Jensen Corporation's unit costs of making

and selling an item at a...

asked 4 hours ago -

Does direct Medicare reimbursement of Advanced practice nurses

increase access to their services?

asked 5 hours ago -

List and explain why a company would choose to use a

published

compensation survey vs. creating...

asked 5 hours ago -

A discrete random variable X can take values from 1 to 10. Find

the variance of...

asked 5 hours ago -

The primary financial goal of a corporation is to maximize:

shareholders wealth.

earnings per share.

stock...

asked 6 hours ago -

determine whether the vectors u=(1,2,3,), v=(-2,1,0) and

w=(1,0,1) are linearly dependent or independent.

asked 6 hours ago -

python

Define a function called print_values which takes a dictionary

object as a parameter. The function...

asked 7 hours ago -

In Chapter 1 you created a program named Triangle in

which you displayed a seven-line triangle...

asked 7 hours ago -

Research question: What are the differences between separately

stated and non separately stated transactions in an...

asked 7 hours ago