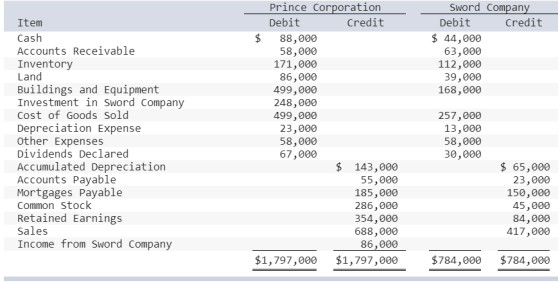

Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $192,000. The trial...

Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $192,000. The trial balances for the two companies on December 31, 20X7, included the following amounts:

Additional Information

- On January 1, 20X7, Sword reported net assets with a book value of $129,000. A total of $30,000 of the acquisition price is applied to goodwill, which was not impaired in 20X7.

- Sword’s depreciable assets had an estimated economic life of 11 years on the date of combination. The difference between fair value and book value of tangible assets is related entirely to buildings and equipment.

- Prince used the equity-method in accounting for its investment in Sword.

- Detailed analysis of receivables and payables showed that Sword owed Prince $18,000 on December 31, 20X7.

Required:

a. Prepare all journal entries recorded by Prince with regard to

its investment in Sword during 20X7. (If no entry is

required for a transaction/event, select "No journal entry

required" in the first account field.)

b. Prepare all consolidating entries needed to prepare a full set

of consolidated financial statements for 20X7. (If no entry

is required for a transaction/event, select "No journal entry

required" in the first account field.)

c. Prepare a three-part consolidation worksheet as of December 31, 20X7. (Values in the first two columns (the "parent" and "subsidiary" balances) that are to be deducted should be indicated with a minus sign, while all values in the "Consolidation Entries" columns should be entered as positive values. For accounts where multiple adjusting entries are required, combine all debit entries into one amount and enter this amount in the debit column of the worksheet. Similarly, combine all credit entries into one amount and enter this amount in the credit column of the worksheet.)

Homework Answers

a. At the time of investment in Sword, Prince will need to record only one journal entry related to it investment.

Investment in Sword Company (Dr) $192,000

Cash (Cr) $192,000

For the profit from Sword, Prince would have recorded below entry as per equity method

Investment in Sword Company (Dr) $86,000

Income from Sword Company (Cr) $86,000

Dividend from Sword, will be recorded like this in Prince's books

Cash (Dr) $30,000

Investment in Sword Company (Cr) $30,000

b.

| Acquisition Price | 192,000 |

| Net book Value on acquisition | (129,000) |

| Goodwill | (30,000) |

| Fair value adjustment in Building and equipments | 33,000 |

Consolidation journal entries will be like this

| Debit | Credit | Notes | |

| Goodwill | 30,000 | ||

| Building and equipments | 33,000 | ||

| Investment in Sword Company | 248,000 | Elimination of investment in subsidiary | |

| Income from Sword Company | 86,000 | Elimination of subsidiary income | |

| Dividend Declared | 30,000 | Elimination of subsidiary dividend | |

| Common Stock | 45,000 | Elimination of Subsidiary equity | |

| Retained Earnings | 84,000 | Elimination of Subsidiary equity | |

| Account Receivable | 18,000 | Elimination of inter-company receivable | |

| Accounts Payable | 18,000 | Elimination of inter-company payable |

Consolidation Worksheet

| Prince | Sword | Consolidation Adjustment | Consolidated Balance | |||||

| Items | Debit | Credit | Debit | Credit | Debit | Credit | Debit | Credit |

| Cash | 88,000 | 44,000 | 132,000 | |||||

| Accoutns Receivable | 58,000 | 63,000 | 18,000 | 103,000 | ||||

| Inventory | 171,000 | 112,000 | 283,000 | |||||

| Land | 86,000 | 39,000 | 125,000 | |||||

| Building and Equipment | 499,000 | 168,000 | 33,000 | 700,000 | ||||

| Investment in Sword Company | 248,000 | - | 248,000 | - | ||||

| Cost of goods sold | 499,000 | 257,000 | 756,000 | |||||

| Depreciation | 23,000 | 13,000 | 36,000 | |||||

| Other expense | 58,000 | 58,000 | 116,000 | |||||

| Dividends declared | 67,000 | 30,000 | 30,000 | 67,000 | ||||

| Accoumulated Depreciation | 143,000 | 65,000 | 208,000 | |||||

| Accounts Payable | 55,000 | 23,000 | 18,000 | 60,000 | ||||

| Mortgage payable | 185,000 | 150,000 | 335,000 | |||||

| Common stock | 286,000 | 45,000 | 45,000 | 286,000 | ||||

| Retained earnings | 354,000 | 84,000 | 84,000 | 354,000 | ||||

| Sales | 688,000 | 417,000 | 1,105,000 | |||||

| Income from Sword Company | 86,000 | - | 86,000 | - | - | |||

| Goodwill | 30,000 | 30,000 | ||||||

| Total | 1,797,000 | 1,797,000 | 784,000 | 784,000 | 296,000 | 296,000 | 2,348,000 | 2,348,000 |

bvhfuvhiibkjbjuuikkbkbibkbkboo\

iihoh9hihhuhinjhuhjio\

ihhohiuhhhiuhiuhuihkuihih\

ihiu8jhuoo;jiihuyghyjh9

ijijii

Add Answer to:

Prince Corporation acquired 100 percent of Sword Company on

January 1, 20X7, for $192,000. The trial...

Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $199,000. The trial...

Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $199,000. The trial balances for the two companies on December 31, 20X7, included the following amounts: Prince Corporation Sword Company Item Debit Credit Debit Credit Cash $ 89,000 $ 30,000 Accounts Receivable 59,000 64,000 Inventory 178,000 100,000 Land 87,000 25,000 Buildings and Equipment 493,000 152,000 Investment in Sword Company 265,000 Cost of Goods Sold 493,000 250,000 Depreciation Expense 23,000 13,000 Other Expenses 65,000 65,000 Dividends Declared 64,000...

image are fine posted 3 times A 25.00 points Prince Corporation acquired 100 percent of Sword...

image are fine posted 3 times

A 25.00 points Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $192,000. The trial balances for the two companies on December 31, 20X7, included the following amounts: Seord om $ 110 income from Sword Company St.O000 SROTO Additional Information 1. On January 1, 20X7. Sword reported net assets with a book value of $136,000 A total of $23,000 of the acquisition price is applied to goodwill, which was not...

image are fine posted 3 times

A 25.00 points Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $192,000. The trial balances for the two companies on December 31, 20X7, included the following amounts: Seord om $ 110 income from Sword Company St.O000 SROTO Additional Information 1. On January 1, 20X7. Sword reported net assets with a book value of $136,000 A total of $23,000 of the acquisition price is applied to goodwill, which was not...

Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $188,000. The trial...

Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $188,000. The trial balances for the two companies on December 31, 20X7, included the following amounts: Prince Corporation Sword Company Item Debit Credit Debit Credit Cash $ 94,000 $ 39,000 Accounts Receivable 53,000 58,000 Inventory 188,000 108,000 Land 92,000 34,000 Buildings and Equipment 494,000 161,000 Investment in Sword Company 217,000 Cost of Goods Sold 494,000 257,000 Depreciation Expense 24,000 14,000 Other Expenses 74,000 74,000 Dividends Declared 56,000...

Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $187,000. The trial...

Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $187,000. The trial balances for the two companies on December 31, 20X7, included the following amounts: Prince Corporation Sword Company Item Debit Credit Debit Credit Cash $ 83,000 $ 34,000 Accounts Receivable 53,000 58,000 Inventory 180,000 119,000 Land 81,000 29,000 Buildings and Equipment 496,000 155,000 Investment in Sword Company 240,000 Cost of Goods Sold 496,000 251,000 Depreciation Expense 23,000 13,000 Other Expenses 64,000 64,000 Dividends Declared 51,000...

Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $188,000. The trial...

Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $188,000. The trial balances for the two companies on December 31, 20X7, included the following amounts: Prince Corporation Sword Company Item Debit Credit Debit Credit Cash $ 94,000 $ 39,000 Accounts Receivable 53,000 58,000 Inventory 188,000 108,000 Land 92,000 34,000 Buildings and Equipment 494,000 161,000 Investment in Sword Company 217,000 Cost of Goods Sold 494,000 257,000 Depreciation Expense 24,000 14,000 Other Expenses 74,000 74,000 Dividends Declared 56,000...

How to computer the Accumulated depreciation? Prince Corporation acquired 100 percent of Sword Company on January...

How to computer the Accumulated

depreciation?

Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $19 1,000. The trial balances for the two companies on December 31, 20X7, included the following amounts: Sword Company Debit Credit $ 26,000 71,000 103,000 21,000 152,000 Item Cash Accounts Receivable Inventory Land Buildings and Equipment Investment in Sword Company Cost of Goods Sold Depreciation Expense Other Expenses Dividends Declared Accumulated Depreciation Accounts Payable Mortgages Payable Common Stock Retained Earnings Sales...

How to computer the Accumulated

depreciation?

Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $19 1,000. The trial balances for the two companies on December 31, 20X7, included the following amounts: Sword Company Debit Credit $ 26,000 71,000 103,000 21,000 152,000 Item Cash Accounts Receivable Inventory Land Buildings and Equipment Investment in Sword Company Cost of Goods Sold Depreciation Expense Other Expenses Dividends Declared Accumulated Depreciation Accounts Payable Mortgages Payable Common Stock Retained Earnings Sales...

Pizza Corporation acquired 80 percent ownership of SliceProducts Company on January 1, 20X1, for $155,000....

Pizza Corporation acquired 80 percent ownership of Slice

Products Company on January 1, 20X1, for $155,000. On that date,

the fair value of the noncontrolling interest was $38,750, and

Slice reported retained earnings of $46,000 and had $99,000 of

common stock outstanding. Pizza has used the equity method in

accounting for its investment in Slice. Trial balance data for the

two companies on December 31, 20X5, are as follows:Additional InformationOn the date of combination, the fair value of Slice's

depreciable...

Pizza Corporation acquired 80 percent ownership of Slice

Products Company on January 1, 20X1, for $155,000. On that date,

the fair value of the noncontrolling interest was $38,750, and

Slice reported retained earnings of $46,000 and had $99,000 of

common stock outstanding. Pizza has used the equity method in

accounting for its investment in Slice. Trial balance data for the

two companies on December 31, 20X5, are as follows:Additional InformationOn the date of combination, the fair value of Slice's

depreciable...

Proud Corporation acquired 80 percent of Spirited Company’s voting stock on January 1, 20X3, at underlying...

Proud Corporation acquired 80 percent of Spirited Company’s voting stock on January 1, 20X3, at underlying book value. The fair value of the noncontrolling interest was equal to 20 percent of the book value of Spirited at that date. Assume that the accumulated depreciation on depreciable assets was $56,000 on the acquisition date. Proud uses the equity method in accounting for its ownership of Spirited. On December 31, 20X4, the trial balances of the two companies are as follows: ...

A-RECORD THE INITIAL INVESTMENT IN SWORD CO. Investment in Sword Co Cash B-RECORD PRINCE CORP’S...

A-RECORD THE INITIAL INVESTMENT IN SWORD CO.

Investment in Sword Co

Cash

B-RECORD PRINCE CORP’S SHARE OF SWORD CO’S 2017 INCOME

Investment in Sword Co

Income from Sword Co

C-RECORD PRINCE CORP’S SHARE OF SWORD CO.’S 2017

DIVIDEND

Cash

Investment in Sword Co

D-RECORD THE AMORTIZATION OF THE EXCESS ACQUISITION

PRICE.

Income from Sword Co

Investment in Sword Co

Prepare all consolidating entries needed to prepare a full set

of consolidated financial statements for 20X7

A-RECORD THE BASIC CONSOLIDATION...

A-RECORD THE INITIAL INVESTMENT IN SWORD CO.

Investment in Sword Co

Cash

B-RECORD PRINCE CORP’S SHARE OF SWORD CO’S 2017 INCOME

Investment in Sword Co

Income from Sword Co

C-RECORD PRINCE CORP’S SHARE OF SWORD CO.’S 2017

DIVIDEND

Cash

Investment in Sword Co

D-RECORD THE AMORTIZATION OF THE EXCESS ACQUISITION

PRICE.

Income from Sword Co

Investment in Sword Co

Prepare all consolidating entries needed to prepare a full set

of consolidated financial statements for 20X7

A-RECORD THE BASIC CONSOLIDATION...

Pie Corporation acquired 65 percent of Slice Company's common stock on r 31, 20X5, at underlying...

Pie Corporation acquired 65 percent of Slice Company's common stock on r 31, 20X5, at underlying book value. The book values and fair values of Slice's assets and liabilities were equal, and the fair value of the noncontrolling interest was equal to 35 percent of the total book value of Slice. Slice provided the following trial balance data at December 31, 20X5: Deco Acco Required: a. How much did Pie pay to purchase its shares of Slice? (Round your answer...

Pie Corporation acquired 65 percent of Slice Company's common stock on r 31, 20X5, at underlying book value. The book values and fair values of Slice's assets and liabilities were equal, and the fair value of the noncontrolling interest was equal to 35 percent of the total book value of Slice. Slice provided the following trial balance data at December 31, 20X5: Deco Acco Required: a. How much did Pie pay to purchase its shares of Slice? (Round your answer...

image are fine posted 3 times

A 25.00 points Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $192,000. The trial balances for the two companies on December 31, 20X7, included the following amounts: Seord om $ 110 income from Sword Company St.O000 SROTO Additional Information 1. On January 1, 20X7. Sword reported net assets with a book value of $136,000 A total of $23,000 of the acquisition price is applied to goodwill, which was not...

image are fine posted 3 times

A 25.00 points Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $192,000. The trial balances for the two companies on December 31, 20X7, included the following amounts: Seord om $ 110 income from Sword Company St.O000 SROTO Additional Information 1. On January 1, 20X7. Sword reported net assets with a book value of $136,000 A total of $23,000 of the acquisition price is applied to goodwill, which was not...

How to computer the Accumulated

depreciation?

Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $19 1,000. The trial balances for the two companies on December 31, 20X7, included the following amounts: Sword Company Debit Credit $ 26,000 71,000 103,000 21,000 152,000 Item Cash Accounts Receivable Inventory Land Buildings and Equipment Investment in Sword Company Cost of Goods Sold Depreciation Expense Other Expenses Dividends Declared Accumulated Depreciation Accounts Payable Mortgages Payable Common Stock Retained Earnings Sales...

How to computer the Accumulated

depreciation?

Prince Corporation acquired 100 percent of Sword Company on January 1, 20X7, for $19 1,000. The trial balances for the two companies on December 31, 20X7, included the following amounts: Sword Company Debit Credit $ 26,000 71,000 103,000 21,000 152,000 Item Cash Accounts Receivable Inventory Land Buildings and Equipment Investment in Sword Company Cost of Goods Sold Depreciation Expense Other Expenses Dividends Declared Accumulated Depreciation Accounts Payable Mortgages Payable Common Stock Retained Earnings Sales...

Pizza Corporation acquired 80 percent ownership of Slice

Products Company on January 1, 20X1, for $155,000. On that date,

the fair value of the noncontrolling interest was $38,750, and

Slice reported retained earnings of $46,000 and had $99,000 of

common stock outstanding. Pizza has used the equity method in

accounting for its investment in Slice. Trial balance data for the

two companies on December 31, 20X5, are as follows:Additional InformationOn the date of combination, the fair value of Slice's

depreciable...

Pizza Corporation acquired 80 percent ownership of Slice

Products Company on January 1, 20X1, for $155,000. On that date,

the fair value of the noncontrolling interest was $38,750, and

Slice reported retained earnings of $46,000 and had $99,000 of

common stock outstanding. Pizza has used the equity method in

accounting for its investment in Slice. Trial balance data for the

two companies on December 31, 20X5, are as follows:Additional InformationOn the date of combination, the fair value of Slice's

depreciable...

A-RECORD THE INITIAL INVESTMENT IN SWORD CO.

Investment in Sword Co

Cash

B-RECORD PRINCE CORP’S SHARE OF SWORD CO’S 2017 INCOME

Investment in Sword Co

Income from Sword Co

C-RECORD PRINCE CORP’S SHARE OF SWORD CO.’S 2017

DIVIDEND

Cash

Investment in Sword Co

D-RECORD THE AMORTIZATION OF THE EXCESS ACQUISITION

PRICE.

Income from Sword Co

Investment in Sword Co

Prepare all consolidating entries needed to prepare a full set

of consolidated financial statements for 20X7

A-RECORD THE BASIC CONSOLIDATION...

A-RECORD THE INITIAL INVESTMENT IN SWORD CO.

Investment in Sword Co

Cash

B-RECORD PRINCE CORP’S SHARE OF SWORD CO’S 2017 INCOME

Investment in Sword Co

Income from Sword Co

C-RECORD PRINCE CORP’S SHARE OF SWORD CO.’S 2017

DIVIDEND

Cash

Investment in Sword Co

D-RECORD THE AMORTIZATION OF THE EXCESS ACQUISITION

PRICE.

Income from Sword Co

Investment in Sword Co

Prepare all consolidating entries needed to prepare a full set

of consolidated financial statements for 20X7

A-RECORD THE BASIC CONSOLIDATION...

Pie Corporation acquired 65 percent of Slice Company's common stock on r 31, 20X5, at underlying book value. The book values and fair values of Slice's assets and liabilities were equal, and the fair value of the noncontrolling interest was equal to 35 percent of the total book value of Slice. Slice provided the following trial balance data at December 31, 20X5: Deco Acco Required: a. How much did Pie pay to purchase its shares of Slice? (Round your answer...

Pie Corporation acquired 65 percent of Slice Company's common stock on r 31, 20X5, at underlying book value. The book values and fair values of Slice's assets and liabilities were equal, and the fair value of the noncontrolling interest was equal to 35 percent of the total book value of Slice. Slice provided the following trial balance data at December 31, 20X5: Deco Acco Required: a. How much did Pie pay to purchase its shares of Slice? (Round your answer...

Most questions answered within 3 hours.

-

New Air Heating and Cooling, manufactures furnaces and central

air units. The company pride itself on...

asked 9 minutes ago -

A coach uses a new technique to train gymnasts. Seven

gymnasts were randomly selected and their...

asked 2 hours ago -

While rotating the tires on your car you notice a rock [mass =

0.1 Kg] stuck...

asked 4 hours ago -

Using MARS simulator, write MIPS programs according to

the following scenarios: Receive a positive integer number...

asked 5 hours ago -

An object in front of a concave mirror has a real image that is

11.5 cm...

asked 6 hours ago -

Consider the reaction, C3 H8 + O2 --> CO2 + H2O. How many

moles of O2...

asked 7 hours ago -

You and your opponent both roll a fair die. If you both roll the

same number,...

asked 8 hours ago -

In a study of the accuracy of fast food drive-through orders,

Restaurant A had 257 accurate...

asked 8 hours ago -

Identify and describe in detail the four categories of

institutions that could be included in a...

asked 8 hours ago -

In python

class Customer:

def __init__(self, customer_id, last_name, first_name, phone_number, address):

self._customer_id = int(customer_id)

self._last_name =...

asked 8 hours ago -

What is an example of a limitation in implementing a new

ERP system and how it...

asked 8 hours ago -

In a section of 9.7cm of an artery with a radius of 2.6mm there

is a...

asked 8 hours ago