Homework Answers

Add Answer to:

Problem 1.5 The yield curve is flat at 5% per annum with quarterly compounding. What is...

Suppose that zero interest rates are per annum with continuous compounding are as follows: Maturity (years)...

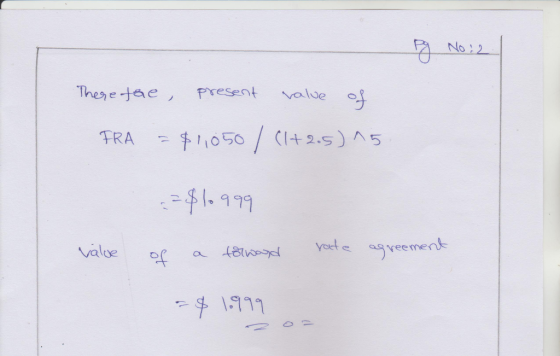

Suppose that zero interest rates are per annum with continuous compounding are as follows: Maturity (years) Rate (% per annum) (1, 2.5) (2, 3.0) (3, 3.5) (4, 4.2) (5, 4.7) Calculate 1-year forward interest rates for the second (f1,2), third (f2,3), fourth (f3,4), and fifth (f4,5) years. Use the rates in the previous part to value an FRA today as the borrower with 5% per annum for the third year on $1 million. (FRA is for the year starting at...

i need simple explain please 7) The zero rates for three, six, nine and twelve compounding....

i need simple explain

please

7) The zero rates for three, six, nine and twelve compounding. These rates suggest that the forwa continuous compounding. What is the present va annum rate with quarterly compounding) for $1,000,000? e, Six, nine and twelve months are 8%, 8.2%, 8.4% and 8.5% with continuous Best that the forward rate between nine months and twelve months is 8.8% with Is the present value of an FRA that enables the holder to earn 9.4% (per very...

i need simple explain

please

7) The zero rates for three, six, nine and twelve compounding. These rates suggest that the forwa continuous compounding. What is the present va annum rate with quarterly compounding) for $1,000,000? e, Six, nine and twelve months are 8%, 8.2%, 8.4% and 8.5% with continuous Best that the forward rate between nine months and twelve months is 8.8% with Is the present value of an FRA that enables the holder to earn 9.4% (per very...

1. Narelle borrows $600,000 on a 25-year property loan at 4 percent per annum compounding monthly....

1. Narelle borrows $600,000 on a 25-year property loan at 4 percent per annum compounding monthly. The loan provides for interest-only payments for 5 years and then reverts to principal and interest repayments sufficient to repay the loan within the original 25-year period. Assume rates do not change. a) Calculate the monthly repayment for the first 5 years. (CLUE: it is INTEREST ONLY) (2 marks) b) Calculate the new monthly repayment after 5 years assuming the interest rate does not...

Suppose that the term structure of interest rates is flat in the UK and Australia. The...

Suppose that the term structure of interest rates is flat in the UK and Australia. The UK interest rate is 0.5% per annum and the AUD rate is 1.5% per annum. The current value of the AUD is 0.59 GBP. Under the terms of a swap agreement a financial institution pays 1.3% per annum in AUD and receives 0.2% per annum in GBP. The principals in the two currencies are £ 23 million and 40 million AUD. Payments are exchanged...

A zero coupon bond of term 3 years has a continuously compounding yield of 5.85%. A zero coupon bond of term 5 years has a continuously compounding yield of 8.95%. Use Excel to compute the two year quarterly compounding rate 3 years forward.

A zero coupon bond of term 3 years has a continuously compounding yield of 5.85%. A zero coupon bond of term 5 years has a continuously compounding yield of 8.95%.Use Excel to compute the two year quarterly compounding rate 3 years forward.

Number 7 Consider an account with an APR of 5%. Calculate the APY with quarterly compounding,...

Number 7 Consider an account with an APR of 5%. Calculate the APY with quarterly compounding, monthly compounding, and daily compounding, Describe how changing the compounding period affects the annual yield. Explain why APR and APY are the same with annual compounding. Explain why APR and APY are different with daily compounding. Does APY depend on the starting principal? Why or why not? • How does APY depend on the number of compounding during a year? Explain.

Number 7 Consider an account with an APR of 5%. Calculate the APY with quarterly compounding, monthly compounding, and daily compounding, Describe how changing the compounding period affects the annual yield. Explain why APR and APY are the same with annual compounding. Explain why APR and APY are different with daily compounding. Does APY depend on the starting principal? Why or why not? • How does APY depend on the number of compounding during a year? Explain.

Intro Suppose that the current exchange rate is $1.3 per Euro. The Euro yield curve is...

Intro Suppose that the current exchange rate is $1.3 per Euro. The Euro yield curve is flat at 2.6% and the U.S yield curve is flat at 3.7%. Part 1 - Attempt 1/10 for 10 pts. What should be the 1-year forward exchange rate (in USD per EUR)? 2+ decimals Submit | Attempt 1/10 for 10 pts. Part 2 What should be the 2-year forward exchange rate (in USD per EUR)? 2+ decimals Submit Part 3 Attempt 1/10 for 10...

Intro Suppose that the current exchange rate is $1.3 per Euro. The Euro yield curve is flat at 2.6% and the U.S yield curve is flat at 3.7%. Part 1 - Attempt 1/10 for 10 pts. What should be the 1-year forward exchange rate (in USD per EUR)? 2+ decimals Submit | Attempt 1/10 for 10 pts. Part 2 What should be the 2-year forward exchange rate (in USD per EUR)? 2+ decimals Submit Part 3 Attempt 1/10 for 10...

Problem #3: A 5 year bond has semiannual coupons of 14% per annum. The continuously compounding...

Problem #3: A 5 year bond has semiannual coupons of 14% per annum. The continuously compounding yield is 19%. The bond has a face value of $300. You will be pricing the bond initially, and at future times throughout the life of the bond as it pulls to par at maturity, using the same continuously compounding yield throughout. Since the yield is given with continuous compounding, the usual formulas will not work without changing the yield to the equivalent discrete...

Problem #3: A 5 year bond has semiannual coupons of 14% per annum. The continuously compounding yield is 19%. The bond has a face value of $300. You will be pricing the bond initially, and at future times throughout the life of the bond as it pulls to par at maturity, using the same continuously compounding yield throughout. Since the yield is given with continuous compounding, the usual formulas will not work without changing the yield to the equivalent discrete...

Suppose that OIS rates of all maturities are 6% per annum, continuously compounded. The one-year LIBOR...

Suppose that OIS rates of all maturities are 6% per annum, continuously compounded. The one-year LIBOR rate is 6.4%, annually compounded and the two-year swap rate for a swap where payments are exchanged annually is 6.8%, annually compounded. Which of the following is closest to the LIBOR forward rate for the second year when LIBOR discounting is used and the rate is expressed with annual compounding

QUESTION # 2 Consider a 1-year swap initiated on January 10th, 2013, between Sony and Samsung, Under the terms of the swap contract Sony is agreed to pay Samsung an interest of 6% per annum on a...

QUESTION # 2 Consider a 1-year swap initiated on January 10th, 2013, between Sony and Samsung, Under the terms of the swap contract Sony is agreed to pay Samsung an interest of 6% per annum on a notional principle of Max. Marks 2+1] $200 n Samsung agrees to pay a 3-month LIBOR rate on the same principal. In addition, the payments are exchanged every three months, andthe6%is quoted with quarterly compounding. Following Table shows the LIBOR Samsung (complete the Table...

QUESTION # 2 Consider a 1-year swap initiated on January 10th, 2013, between Sony and Samsung, Under the terms of the swap contract Sony is agreed to pay Samsung an interest of 6% per annum on a notional principle of Max. Marks 2+1] $200 n Samsung agrees to pay a 3-month LIBOR rate on the same principal. In addition, the payments are exchanged every three months, andthe6%is quoted with quarterly compounding. Following Table shows the LIBOR Samsung (complete the Table...

i need simple explain

please

7) The zero rates for three, six, nine and twelve compounding. These rates suggest that the forwa continuous compounding. What is the present va annum rate with quarterly compounding) for $1,000,000? e, Six, nine and twelve months are 8%, 8.2%, 8.4% and 8.5% with continuous Best that the forward rate between nine months and twelve months is 8.8% with Is the present value of an FRA that enables the holder to earn 9.4% (per very...

i need simple explain

please

7) The zero rates for three, six, nine and twelve compounding. These rates suggest that the forwa continuous compounding. What is the present va annum rate with quarterly compounding) for $1,000,000? e, Six, nine and twelve months are 8%, 8.2%, 8.4% and 8.5% with continuous Best that the forward rate between nine months and twelve months is 8.8% with Is the present value of an FRA that enables the holder to earn 9.4% (per very...

Number 7 Consider an account with an APR of 5%. Calculate the APY with quarterly compounding, monthly compounding, and daily compounding, Describe how changing the compounding period affects the annual yield. Explain why APR and APY are the same with annual compounding. Explain why APR and APY are different with daily compounding. Does APY depend on the starting principal? Why or why not? • How does APY depend on the number of compounding during a year? Explain.

Number 7 Consider an account with an APR of 5%. Calculate the APY with quarterly compounding, monthly compounding, and daily compounding, Describe how changing the compounding period affects the annual yield. Explain why APR and APY are the same with annual compounding. Explain why APR and APY are different with daily compounding. Does APY depend on the starting principal? Why or why not? • How does APY depend on the number of compounding during a year? Explain.

Intro Suppose that the current exchange rate is $1.3 per Euro. The Euro yield curve is flat at 2.6% and the U.S yield curve is flat at 3.7%. Part 1 - Attempt 1/10 for 10 pts. What should be the 1-year forward exchange rate (in USD per EUR)? 2+ decimals Submit | Attempt 1/10 for 10 pts. Part 2 What should be the 2-year forward exchange rate (in USD per EUR)? 2+ decimals Submit Part 3 Attempt 1/10 for 10...

Intro Suppose that the current exchange rate is $1.3 per Euro. The Euro yield curve is flat at 2.6% and the U.S yield curve is flat at 3.7%. Part 1 - Attempt 1/10 for 10 pts. What should be the 1-year forward exchange rate (in USD per EUR)? 2+ decimals Submit | Attempt 1/10 for 10 pts. Part 2 What should be the 2-year forward exchange rate (in USD per EUR)? 2+ decimals Submit Part 3 Attempt 1/10 for 10...

Problem #3: A 5 year bond has semiannual coupons of 14% per annum. The continuously compounding yield is 19%. The bond has a face value of $300. You will be pricing the bond initially, and at future times throughout the life of the bond as it pulls to par at maturity, using the same continuously compounding yield throughout. Since the yield is given with continuous compounding, the usual formulas will not work without changing the yield to the equivalent discrete...

Problem #3: A 5 year bond has semiannual coupons of 14% per annum. The continuously compounding yield is 19%. The bond has a face value of $300. You will be pricing the bond initially, and at future times throughout the life of the bond as it pulls to par at maturity, using the same continuously compounding yield throughout. Since the yield is given with continuous compounding, the usual formulas will not work without changing the yield to the equivalent discrete...

QUESTION # 2 Consider a 1-year swap initiated on January 10th, 2013, between Sony and Samsung, Under the terms of the swap contract Sony is agreed to pay Samsung an interest of 6% per annum on a notional principle of Max. Marks 2+1] $200 n Samsung agrees to pay a 3-month LIBOR rate on the same principal. In addition, the payments are exchanged every three months, andthe6%is quoted with quarterly compounding. Following Table shows the LIBOR Samsung (complete the Table...

QUESTION # 2 Consider a 1-year swap initiated on January 10th, 2013, between Sony and Samsung, Under the terms of the swap contract Sony is agreed to pay Samsung an interest of 6% per annum on a notional principle of Max. Marks 2+1] $200 n Samsung agrees to pay a 3-month LIBOR rate on the same principal. In addition, the payments are exchanged every three months, andthe6%is quoted with quarterly compounding. Following Table shows the LIBOR Samsung (complete the Table...

Most questions answered within 3 hours.

-

----Can someone please help me solve this one using JAVA

----I thank you in advance

Create...

asked 41 seconds ago -

1. What force primarily attracts the potassium ion to

the nitrate ion?

a. London forces...

asked 2 minutes ago -

What are the negative effects of abruptly stopping the use of

all fossil fuels? Give at...

asked 9 minutes ago -

Given that many conflict are the result of different parties having

different interests, is it possible...

asked 14 minutes ago -

A 750 g block can slide uniformly along the horizontal track

when a string attached to...

asked 17 minutes ago -

In 2017, Juan entered into a contract to write a book. The

publisher advanced Juan $50,000,...

asked 30 minutes ago -

Determine the number of kinds of protons in each molecule (w/

respect to NMR spectroscopy). Drawing...

asked 40 minutes ago -

A jeweler whose near point is 68 cm from his eye uses a

magnifying glass as...

asked 38 minutes ago -

A company wants to determine how many units of each of two

products, A and B,...

asked 42 minutes ago -

The blood pressure of a person changes throughout the day.

Suppose the systolic blood pressure of...

asked 51 minutes ago -

A chemistry student desired to study sulfur. Sulfur exhibited

the following characteristics with oxygen:

(a) It...

asked 47 minutes ago -

An Atwood machine is constructed of a solid-disk frictionless

pulley of mass m3 and radius R....

asked 49 minutes ago