Homework Answers

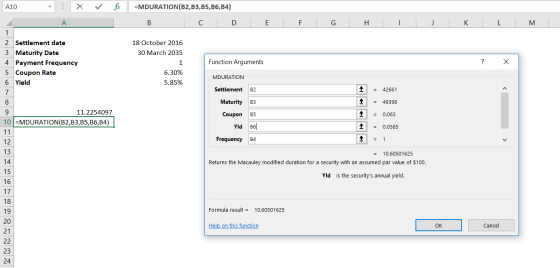

To calculate Macaulay, please use the below values in Duration function in excel, as shown in screenshot below:

Macaulay duration = 11.23 years

To calculate modified duration, use Mduration function on excel and the same values, as shown in the screenshot below :

Modified duration = 10.61 years

Add Answer to:

A Treasury bond that settles on October 18, 2016, matures on March 30, 2035. The coupon...

porte A Treasury bond that settles on October 18, 2016, matures on March 30, 2035. The...

porte A Treasury bond that settles on October 18, 2016, matures on March 30, 2035. The coupon rate is 5.75 percent and the bond has a yield to maturity of 5.08 percent. What are the Macaulay duration and modified duration? (Use the duration function in Excel to solve the problem. Do not found intermediate calculations. Round your answers to 4 decimal places.) Macaulay duration Modified duration

porte A Treasury bond that settles on October 18, 2016, matures on March 30, 2035. The coupon rate is 5.75 percent and the bond has a yield to maturity of 5.08 percent. What are the Macaulay duration and modified duration? (Use the duration function in Excel to solve the problem. Do not found intermediate calculations. Round your answers to 4 decimal places.) Macaulay duration Modified duration

ATreasury bond that settles on October 18, 2016, matures on March 30, 2035. The coupon rate...

ATreasury bond that settles on October 18, 2016, matures on March 30, 2035. The coupon rate is 5.75 percent and the bond has a leld to maturity of 5.08 percent. What are the Macaulay duration and modified duration? (Use the duration function in Excel to solve the problem. Do not round intermediate calculations. Round your answers to 4 decimal places.) Macaulay duration Modified duration

ATreasury bond that settles on October 18, 2016, matures on March 30, 2035. The coupon rate is 5.75 percent and the bond has a leld to maturity of 5.08 percent. What are the Macaulay duration and modified duration? (Use the duration function in Excel to solve the problem. Do not round intermediate calculations. Round your answers to 4 decimal places.) Macaulay duration Modified duration

Problem 10-35 Duration (LO4, CFA6) A Treasury bond that settles on October 18, 2016, matures on...

Problem 10-35 Duration (LO4, CFA6) A Treasury bond that settles on October 18, 2016, matures on March 30, 2035. The coupon rate is 6.15 percent and the bond has a yield to maturity of 5.64 percent. What are the Macaulay duration and modified duration? (Use the duration function in Excel to solve the problem. Do not round intermediate calculations. Round your answers to 4 decimal places.) Answer is complete but not entirely correct. 11.3694 Macaulay duration Modified duration 10.7624

Problem 10-35 Duration (LO4, CFA6) A Treasury bond that settles on October 18, 2016, matures on March 30, 2035. The coupon rate is 6.15 percent and the bond has a yield to maturity of 5.64 percent. What are the Macaulay duration and modified duration? (Use the duration function in Excel to solve the problem. Do not round intermediate calculations. Round your answers to 4 decimal places.) Answer is complete but not entirely correct. 11.3694 Macaulay duration Modified duration 10.7624

Problem 10-35 Duration (LO4, CFA6) A Treasury bond that settles on October 18, 2016, ma yield...

Problem 10-35 Duration (LO4, CFA6) A Treasury bond that settles on October 18, 2016, ma yield to maturity of 5.64 percent. What are the Macau the problem. Do not round intermediate calculation & Answer is complete but not entirely correct. 11.3694 Macaulay duration Modified duration 10.7624 X

Problem 10-35 Duration (LO4, CFA6) A Treasury bond that settles on October 18, 2016, ma yield to maturity of 5.64 percent. What are the Macau the problem. Do not round intermediate calculation & Answer is complete but not entirely correct. 11.3694 Macaulay duration Modified duration 10.7624 X

A bond with a coupon rate of 9 percent sells at a yield to maturity of...

A bond with a coupon rate of 9 percent sells at a yield to maturity of 10 percent. If the bond matures in 11 years, what is the Macaulay duration of the bond? What is the modified duration? (Do not round intermediate calculations. Round your answers to 3 decimal places.)

A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming...

A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming a discount rate of 3.23 percent, what are the price and bond equivalent yield? Use Excel to answer this question. (Round your price answer to 2 decimal places. Enter your yield answer as a percent rounded to 3 decimal places.) Price ____ Bond equivelent yield _____

A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming...

A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming a discount rate of 1.87 percent, what are the price and bond equivalent yield? Use Excel to answer this question. (Round your price answer to 2 decimal places. Enter your yield answer as a percent rounded to 3 decimal places.) Price Bond equivalent yield

A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming a discount rate of 1.87 percent, what are the price and bond equivalent yield? Use Excel to answer this question. (Round your price answer to 2 decimal places. Enter your yield answer as a percent rounded to 3 decimal places.) Price Bond equivalent yield

A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming...

A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming a discount rate of 3.87 percent, what are the price and bond equivalent yield? Use Excel to answer this question. (Round your price answer to 2 decimal places, Enter your yield answer as a percent rounded to 3 decimal places.) Price Bond equivalent yield rences

A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming a discount rate of 3.87 percent, what are the price and bond equivalent yield? Use Excel to answer this question. (Round your price answer to 2 decimal places, Enter your yield answer as a percent rounded to 3 decimal places.) Price Bond equivalent yield rences

A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming...

A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming a discount rate of .64 percent, what are the price and bond equivalent yield? Use Excel to answer this question. (Round your price answer to 2 decimal places. Enter your yield answer as a percent rounded to 3 decimal places.) X Answer is complete but not entirely correct. 83,466.67 X Price Bond equivalent yield 77.742 X %

A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming a discount rate of .64 percent, what are the price and bond equivalent yield? Use Excel to answer this question. (Round your price answer to 2 decimal places. Enter your yield answer as a percent rounded to 3 decimal places.) X Answer is complete but not entirely correct. 83,466.67 X Price Bond equivalent yield 77.742 X %

We try DIN UTRAJ Sints A Treasury bill that settles on May 18, 2016, pays $100,000...

We try DIN UTRAJ Sints A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming a discount rate of 3.87 percent, what are the price and bond equivalent yield? Use Excel to answer this question. (Round your price answer to 2 decimal places. Enter your yield answer as a percent rounded to 3 decimal places.) Bond equivalented

We try DIN UTRAJ Sints A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming a discount rate of 3.87 percent, what are the price and bond equivalent yield? Use Excel to answer this question. (Round your price answer to 2 decimal places. Enter your yield answer as a percent rounded to 3 decimal places.) Bond equivalented

porte A Treasury bond that settles on October 18, 2016, matures on March 30, 2035. The coupon rate is 5.75 percent and the bond has a yield to maturity of 5.08 percent. What are the Macaulay duration and modified duration? (Use the duration function in Excel to solve the problem. Do not found intermediate calculations. Round your answers to 4 decimal places.) Macaulay duration Modified duration

porte A Treasury bond that settles on October 18, 2016, matures on March 30, 2035. The coupon rate is 5.75 percent and the bond has a yield to maturity of 5.08 percent. What are the Macaulay duration and modified duration? (Use the duration function in Excel to solve the problem. Do not found intermediate calculations. Round your answers to 4 decimal places.) Macaulay duration Modified duration

ATreasury bond that settles on October 18, 2016, matures on March 30, 2035. The coupon rate is 5.75 percent and the bond has a leld to maturity of 5.08 percent. What are the Macaulay duration and modified duration? (Use the duration function in Excel to solve the problem. Do not round intermediate calculations. Round your answers to 4 decimal places.) Macaulay duration Modified duration

ATreasury bond that settles on October 18, 2016, matures on March 30, 2035. The coupon rate is 5.75 percent and the bond has a leld to maturity of 5.08 percent. What are the Macaulay duration and modified duration? (Use the duration function in Excel to solve the problem. Do not round intermediate calculations. Round your answers to 4 decimal places.) Macaulay duration Modified duration

Problem 10-35 Duration (LO4, CFA6) A Treasury bond that settles on October 18, 2016, matures on March 30, 2035. The coupon rate is 6.15 percent and the bond has a yield to maturity of 5.64 percent. What are the Macaulay duration and modified duration? (Use the duration function in Excel to solve the problem. Do not round intermediate calculations. Round your answers to 4 decimal places.) Answer is complete but not entirely correct. 11.3694 Macaulay duration Modified duration 10.7624

Problem 10-35 Duration (LO4, CFA6) A Treasury bond that settles on October 18, 2016, matures on March 30, 2035. The coupon rate is 6.15 percent and the bond has a yield to maturity of 5.64 percent. What are the Macaulay duration and modified duration? (Use the duration function in Excel to solve the problem. Do not round intermediate calculations. Round your answers to 4 decimal places.) Answer is complete but not entirely correct. 11.3694 Macaulay duration Modified duration 10.7624

Problem 10-35 Duration (LO4, CFA6) A Treasury bond that settles on October 18, 2016, ma yield to maturity of 5.64 percent. What are the Macau the problem. Do not round intermediate calculation & Answer is complete but not entirely correct. 11.3694 Macaulay duration Modified duration 10.7624 X

Problem 10-35 Duration (LO4, CFA6) A Treasury bond that settles on October 18, 2016, ma yield to maturity of 5.64 percent. What are the Macau the problem. Do not round intermediate calculation & Answer is complete but not entirely correct. 11.3694 Macaulay duration Modified duration 10.7624 X

A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming a discount rate of 1.87 percent, what are the price and bond equivalent yield? Use Excel to answer this question. (Round your price answer to 2 decimal places. Enter your yield answer as a percent rounded to 3 decimal places.) Price Bond equivalent yield

A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming a discount rate of 1.87 percent, what are the price and bond equivalent yield? Use Excel to answer this question. (Round your price answer to 2 decimal places. Enter your yield answer as a percent rounded to 3 decimal places.) Price Bond equivalent yield

A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming a discount rate of 3.87 percent, what are the price and bond equivalent yield? Use Excel to answer this question. (Round your price answer to 2 decimal places, Enter your yield answer as a percent rounded to 3 decimal places.) Price Bond equivalent yield rences

A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming a discount rate of 3.87 percent, what are the price and bond equivalent yield? Use Excel to answer this question. (Round your price answer to 2 decimal places, Enter your yield answer as a percent rounded to 3 decimal places.) Price Bond equivalent yield rences

A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming a discount rate of .64 percent, what are the price and bond equivalent yield? Use Excel to answer this question. (Round your price answer to 2 decimal places. Enter your yield answer as a percent rounded to 3 decimal places.) X Answer is complete but not entirely correct. 83,466.67 X Price Bond equivalent yield 77.742 X %

A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming a discount rate of .64 percent, what are the price and bond equivalent yield? Use Excel to answer this question. (Round your price answer to 2 decimal places. Enter your yield answer as a percent rounded to 3 decimal places.) X Answer is complete but not entirely correct. 83,466.67 X Price Bond equivalent yield 77.742 X %

We try DIN UTRAJ Sints A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming a discount rate of 3.87 percent, what are the price and bond equivalent yield? Use Excel to answer this question. (Round your price answer to 2 decimal places. Enter your yield answer as a percent rounded to 3 decimal places.) Bond equivalented

We try DIN UTRAJ Sints A Treasury bill that settles on May 18, 2016, pays $100,000 on August 21, 2016. Assuming a discount rate of 3.87 percent, what are the price and bond equivalent yield? Use Excel to answer this question. (Round your price answer to 2 decimal places. Enter your yield answer as a percent rounded to 3 decimal places.) Bond equivalented

Most questions answered within 3 hours.

-

The Problem: The Case of the Harmonizing Vacations

Your CEO is exploring partnering with a European...

asked 44 minutes ago -

A chemical equation is balanced by adding coefficients in front

of some formulas so that the...

asked 42 minutes ago -

From the literature (reference your sources): What are the

lattice parameters of calcite and aragonite? Why...

asked 1 hour ago -

Your system is rejecting the question am asking which is

preceded by a case study. It...

asked 1 hour ago -

3. On January 2, 2000, Larry creates a trust with himself as

trustee. Larry as trustee...

asked 1 hour ago -

A member of the volleyball team spikes the ball. During this

process, she changes the velocity...

asked 1 hour ago -

Are adult gamers less likely to use a gaming console (Xbox,

PlayStation, Wii, etc...) than teen...

asked 2 hours ago -

The University of

Texas recently reported that 43% of college students aged 18-24

would spend their...

asked 2 hours ago -

The length of stay at a specific emergency department in

Phoenix, Arizona, in 2009 had a...

asked 1 hour ago -

. Please give the mechanism for this type of problem. Step by

Step

The toxin that...

asked 1 hour ago -

If you have a 1M stock solution and you want to dilute 1 :10

with water,...

asked 1 hour ago -

In a load instruction, the effective address is obtained by

A) Retriving the address from a...

asked 1 hour ago