The current price of a non-dividend paying stock is $30. Use a two-step tree to value...

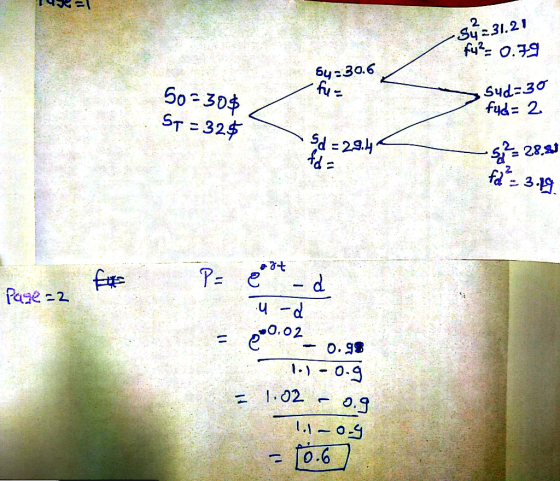

The current price of a non-dividend paying stock is $30. Use a two-step tree to value a European put option on the stock with a strike price of $32 that expires in 6 months with u=1.1 and d=0.9. Each step is 3 months, the risk free rate is 8%.

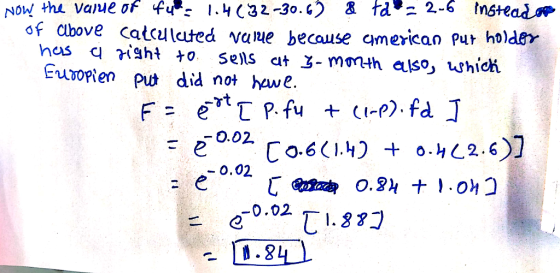

b) what is the value of the put if it were American style option, all else being equal to that problem.

Homework Answers

The main difference between these two options is American option can be exercised before maturity also so at the end of three months the difference in the pricing of option will be there let's understand with the help of calculation.

![Pax:-3 fuz ett [p. for? + <1-P)(fud) ] 500.02 [0.660.29*(0.4)(2)] = e =0.0210.494 + 0.8] = 1.248] fd2 = pot q Pcfud) + (1-P)](http://img.homeworklib.com/questions/135498d0-755e-11ea-b5e2-6b1a233260c4.png?x-oss-process=image/resize,w_560)

I hope my efforts will be fruitful to you...

Thanks for posting ...

Add Answer to:

The current price of a non-dividend paying stock is $30. Use a

two-step tree to value...

The current price of a non-dividend-paying stock is 30. The volatility of the stock is 0.3...

The current price of a non-dividend-paying stock is 30. The volatility of the stock is 0.3 per annum. The risk free rate is 0.05 for all maturities. Using the Cox-Ross-Rubinstein binomial tree model with two time steps to do the valuation, what is the value of a European call option with a strike price of 32 that expires in 6 months?

The current price of a non-dividend-paying stock is 30. The volatility of the stock is 0.3...

The current price of a non-dividend-paying stock is 30. The volatility of the stock is 0.3 per annum. The risk free rate is 0.05 for all maturities. Using the Cox-Ross-Rubinstein binomial tree model with two time steps to do the valuation, what is the value of a European call option with a strike price of 32 that expires in 6 months? (Your answer should be in the unit of dollar (up to the precision of cents), but without the dollar...

Q8-Part I (6 marks) The current price of a non-dividend-paying stock is $42. Over the next...

Q8-Part I (6 marks) The current price of a non-dividend-paying stock is $42. Over the next year it is expected to rise to-$44. or fall to $39. An investor buys put options with a strike price of $43. To hedge the position, should (and by how many) the investor buy or sell the underlying share (s) for each put option purchased? (6 marks) 08-Part II (9 marks) The current price of a non-dividend paying stock is $49. Use a two-step...

Q8-Part I (6 marks) The current price of a non-dividend-paying stock is $42. Over the next year it is expected to rise to-$44. or fall to $39. An investor buys put options with a strike price of $43. To hedge the position, should (and by how many) the investor buy or sell the underlying share (s) for each put option purchased? (6 marks) 08-Part II (9 marks) The current price of a non-dividend paying stock is $49. Use a two-step...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annu...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

The current price of a non-dividend-paying stock is $30. Over the next six months it is...

The current price of a non-dividend-paying stock is $30. Over the next six months it is expected to rise to $36 or fall to $28. Assume the risk-free rate is 10%. What, to the nearest cent, is the price of a European put option with a strike price of $33?

What is the price of a European put option on a non-dividend paying stock when the...

What is the price of a European put option on a non-dividend paying stock when the stock price is $69, the strike price is $70, the risk-free interest rate is 5% per annum, the volatility is 35%per annum, and the time to maturity is six months? Please give me step by step by step instructions.

Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price...

Consider an option on a non-dividend-paying stock when the stock price is $30, the exercise price is $29, the risk-free interest rate is 5% per annum, the volatility is 25% per annum, and the time to maturity is four months. Use the Black-Scholes-Merton formula. What is the price of the option if it is a European call? What is the price of the option if it is an American call? What is the price of the option if it is...

The current price of a non-dividend-paying stock is $30. Over the next six months it is...

The current price of a non-dividend-paying stock is $30. Over the next six months it is expected to rise to $36 or fall to $26. Assume that the risk-free rate is 10%. What, to the nearest cent, is the value of a 6-month European call option on the stock with a strike price of $33?

Q8-Part I (6 marks) The current price of a non-dividend-paying stock is $42. Over the next year it is expected to rise to-$44. or fall to $39. An investor buys put options with a strike price of $43. To hedge the position, should (and by how many) the investor buy or sell the underlying share (s) for each put option purchased? (6 marks) 08-Part II (9 marks) The current price of a non-dividend paying stock is $49. Use a two-step...

Q8-Part I (6 marks) The current price of a non-dividend-paying stock is $42. Over the next year it is expected to rise to-$44. or fall to $39. An investor buys put options with a strike price of $43. To hedge the position, should (and by how many) the investor buy or sell the underlying share (s) for each put option purchased? (6 marks) 08-Part II (9 marks) The current price of a non-dividend paying stock is $49. Use a two-step...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Question 1 - 35 Points Consider a European put option on a non-dividend-paying stock where the stock price is $15, the strike price is $13, the risk-free rate is 3% per annum, the volatility is 30% per annum and the time to maturity is 9 months. Consider a three-step troc. (Hint: dt = 3 months). (a) Compute u and d. (b) Compute the European put price using a three-step binomial tree. (c) If the option in (b) is American instead...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Question 3 - 20 Points Consider a European call option on a non-dividend-paying stock where the stock price is $33, the strike price is $36, the risk-free rate is 6% per annum, the volatility is 25% per annum and the time to maturity is 6 months. (a) Calculate u and d for a one-step binomial tree. (b) Value the option using a non arbitrage argument. (c) Assume that the option is a put instead of a call. Value the option...

Most questions answered within 3 hours.

-

You are trying to convince your friend who wants to attend

medical school to take BY123...

asked 9 minutes ago -

Subject: C++

I have created a class called QueueOfIntegers in a file called

QueueOfIntegers.h, which is...

asked 9 minutes ago -

calculate the number of molecules of gas in a

container of 2.0 liter at 30 degrees...

asked 26 minutes ago -

1.which of the following is a phototroph?

a. sulfolobus

b. chloroflexus

c. bacteroidetes

d. deinococcus radioduran...

asked 22 minutes ago -

The group of companies LC "High-precision measuring instruments"

is the global provider of measurement, analysis and...

asked 28 minutes ago -

I want to write a python function to find the minimum

I have an nested list:...

asked 28 minutes ago -

Convert the high level language programming statementts to 80x86

assembly, Assume X=AX and y=BX

for (i=1;...

asked 37 minutes ago -

SoleMate’s Burkins sneakers cost $40 per pair from the supplier

and are sold by SoleMate at...

asked 41 minutes ago -

The movie Moneyball (based on the book by Michael

Lewis) tells the story of Billy Beane,...

asked 40 minutes ago -

A regional highway uses 8 tollbooths that are open to all

vehicles. A chi-square goodness-of-fit test...

asked 44 minutes ago -

In her Semiannual Monetary Policy Report to Congress on July 13,

2017, then Federal Reserve Chair...

asked 43 minutes ago -

Suppose N packets are sent,

and each packet arrives at rate of L/2R to a link....

asked 1 hour ago