Homework Answers

Solution:

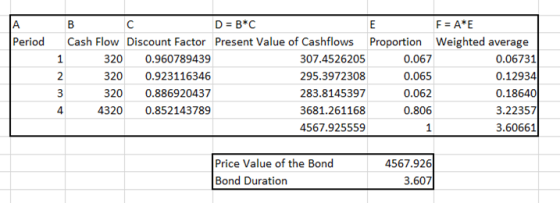

Here Cash flows are the Coupon for the first 3 periods and for the fourth period its coupon plus Value at maturity.

Coupon = Coupon rate * Value of the bond

= 8% * 4000 = 320 { here 8% rate is assumed at semi-annually }

For fourth year, it is Coupon + Value of bond

= 320+4000 = 4320

==>Here, Discount Factor for option a and b = 1/(1+r)^n

Example: for option (a) for year 1 = 1/(1+0.02)^1 = 0.98039 approximately

{ here n is period, and rate is semi-annually}

==> Proportion = Present Value of cashflow at n / Price of the bond

==> Weighted Average = Proportion*Period

(a) Here rate is 2%. as in question it is given 4% annually, but we are calculating semi-annually.

Semi-annually rate = Annual rate / 2

= 4% / 2 = 2%

(b) Here Yield rate is 4% semi-annually

(c) Here Discount Factor = e^(-r*Period)

This is done as the rate is compounded continuously.

Here r is 4%

Add Answer to:

Consider a 2-year $4000 bond that's redeemable at par and pays semi-annual coupons at a rate...

(1 point) Consider the continuously compounded yield curve y(T-0.035-0.0 15є-0.5T Consider a 2-year $ 2500 bond...

(1 point) Consider the continuously compounded yield curve y(T-0.035-0.0 15є-0.5T Consider a 2-year $ 2500 bond that's redeemable at par and pays semi-annual coupons at a rate of C(2) 596. () Determine the bond's purchase price. Purchase Price $ (i) Determine the duration of the bond to 3 decimals. Duration years Note: Use the purchase price to the closest cent in your duration calculation

(1 point) Consider the continuously compounded yield curve y(T-0.035-0.0 15є-0.5T Consider a 2-year $ 2500 bond that's redeemable at par and pays semi-annual coupons at a rate of C(2) 596. () Determine the bond's purchase price. Purchase Price $ (i) Determine the duration of the bond to 3 decimals. Duration years Note: Use the purchase price to the closest cent in your duration calculation

1 point) Consider the continuously compounded yield curve y(T) 0.045 - 0.015e0."7. Consider a 2-year $...

1 point) Consider the continuously compounded yield curve y(T) 0.045 - 0.015e0."7. Consider a 2-year $ 1000 bond that's redeemable at par and pays semi-annual coupons at a rate of 42) 7%. (1) Determine the bond's purchase price. Purchase Price-$ (i) Determine the duration of the bond to 3 decimals. Duration Note: Use the purchase price to the closest cent in your duration calculation. years

1 point) Consider the continuously compounded yield curve y(T) 0.045 - 0.015e0."7. Consider a 2-year $ 1000 bond that's redeemable at par and pays semi-annual coupons at a rate of 42) 7%. (1) Determine the bond's purchase price. Purchase Price-$ (i) Determine the duration of the bond to 3 decimals. Duration Note: Use the purchase price to the closest cent in your duration calculation. years

Consider the continuously compounded yield curve . Consider a 2-year $ 5000 bond that's redeemable at...

Consider the continuously compounded yield curve

.

Consider a 2-year $ 5000 bond that's redeemable at par and pays

semi-annual coupons at a rate of

%.

(i) Determine the bond's purchase price.

(ii) Determine the duration of the bond to 3 decimals.

y(T) 0.045-0.02e-0.57 C(2) -3

Consider the continuously compounded yield curve

.

Consider a 2-year $ 5000 bond that's redeemable at par and pays

semi-annual coupons at a rate of

%.

(i) Determine the bond's purchase price.

(ii) Determine the duration of the bond to 3 decimals.

y(T) 0.045-0.02e-0.57 C(2) -3

Consider a 2-year $1000 par value bond that pays semi-annual coupons at a rate of 42)...

Consider a 2-year $1000 par value bond that pays semi-annual coupons at a rate of 42) purchased for $1058.82 6%. Suppose that the bond was (a) Use the method of averages to approximate the effective yield rate compounded semi-annually. State the result as a percent to 1 decimal place % compounded semi-annually (b) Complete the chart below by performing 2 iterations of the bisection method to approximate the effective yield rate compounded semi-annually [Note: For the initial interval [a(0),b(0) use...

Consider a 2-year $1000 par value bond that pays semi-annual coupons at a rate of 42) purchased for $1058.82 6%. Suppose that the bond was (a) Use the method of averages to approximate the effective yield rate compounded semi-annually. State the result as a percent to 1 decimal place % compounded semi-annually (b) Complete the chart below by performing 2 iterations of the bisection method to approximate the effective yield rate compounded semi-annually [Note: For the initial interval [a(0),b(0) use...

Consider the following zero coupon bonds each of which are redeemable at par and have a...

Consider the following zero coupon bonds each of which are redeemable at par and have a yield rate of 3.5 % compounded continuously. Bond Face Value (in dollars) 4000 10000 5000 1000 Maturity (in years) 10 15 25 30 (a) Determine the purchase price of each bond: Bond Price (in dollars to closest cent) NOTE: Do not include the $ sign. (b) Determine the present value of the portfolio of bonds. NOTE: Do not include the $ sign. (b) Determine...

Consider the following zero coupon bonds each of which are redeemable at par and have a yield rate of 3.5 % compounded continuously. Bond Face Value (in dollars) 4000 10000 5000 1000 Maturity (in years) 10 15 25 30 (a) Determine the purchase price of each bond: Bond Price (in dollars to closest cent) NOTE: Do not include the $ sign. (b) Determine the present value of the portfolio of bonds. NOTE: Do not include the $ sign. (b) Determine...

A $51,000, 88% bond redeemable at 104 with semi-annual coupons bought eleven years before matu...

A $51,000, 88% bond redeemable at 104 with semi-annual coupons bought eleven years before maturity to yield 9% compounded semi-annually is sold three years before maturity at 102.25. Find the gain or loss on the sale of the bond. (Round the final answer to the nearest cent as needed. Round all intermediate values to six decimal places as needed.)

6. A $10,000, 6% bond with semi-annual coupons is redeemable at par. What is the purchase...

6. A $10,000, 6% bond with semi-annual coupons is redeemable at par. What is the purchase price to yield 7.5% compounded semi-annually (a) nine years before maturity? (b) fifteen years before maturity? (a) The purchase price is $ (Round the final answer to the nearest cent as needed. Round all intermediate values to six decimal places as needed.) (b) The purchase price is $ (Round the final answer to the nearest cent as needed. Round all intermediate values to six...

6. A $10,000, 6% bond with semi-annual coupons is redeemable at par. What is the purchase price to yield 7.5% compounded semi-annually (a) nine years before maturity? (b) fifteen years before maturity? (a) The purchase price is $ (Round the final answer to the nearest cent as needed. Round all intermediate values to six decimal places as needed.) (b) The purchase price is $ (Round the final answer to the nearest cent as needed. Round all intermediate values to six...

Consider a $3000 par value bond that pays 5 annual coupons at a nominal rate of...

Consider a $3000 par value bond that pays 5 annual coupons at a nominal rate of 4% compounded annually. Suppose that the bond was purchased for $2981.91. a) Price using the Method of Averages yield = $ ____ b) Rate of Change of Price (to 2 decimals) using the Method of Averages yield = $ ____ per % change

● LOO A $1000 bond bearing interest at 8% payable 2 semi-annually redeemable at par on February 1...

● LOO A $1000 bond bearing interest at 8% payable 2 semi-annually redeemable at par on February 1, 2020, was purchased on October 12, 2013, to yield 7% compounded semi-annually. Determine the purchase price.

● LOO A $1000 bond bearing interest at 8% payable 2 semi-annually redeemable at par on February 1, 2020, was purchased on October 12, 2013, to yield 7% compounded semi-annually. Determine the purchase price.

● LOO A $1000 bond bearing interest at 8% payable 2 semi-annually redeemable at par on February 1, 2020, was purchased on October 12, 2013, to yield 7% compounded semi-annually. Determine the purchase price.

● LOO A $1000 bond bearing interest at 8% payable 2 semi-annually redeemable at par on February 1, 2020, was purchased on October 12, 2013, to yield 7% compounded semi-annually. Determine the purchase price.

Suppose a ten-year, $ 1 000 bond with an 8.4 % coupon rate and semi-annual coupons...

Suppose a ten-year, $ 1 000 bond with an 8.4 % coupon rate and semi-annual coupons is trading for a price of $ 1 035.72. a. What is the bond's yield to maturity (expressed as an APR with semi-annual compounding)? b. If the bond's yield to maturity changes to 9.1 % APR , what will the bond's price be? a. The bond's yield to maturity is nothing %. (Enter your response as a percent rounded to two decimal places.) b....

(1 point) Consider the continuously compounded yield curve y(T-0.035-0.0 15є-0.5T Consider a 2-year $ 2500 bond that's redeemable at par and pays semi-annual coupons at a rate of C(2) 596. () Determine the bond's purchase price. Purchase Price $ (i) Determine the duration of the bond to 3 decimals. Duration years Note: Use the purchase price to the closest cent in your duration calculation

(1 point) Consider the continuously compounded yield curve y(T-0.035-0.0 15є-0.5T Consider a 2-year $ 2500 bond that's redeemable at par and pays semi-annual coupons at a rate of C(2) 596. () Determine the bond's purchase price. Purchase Price $ (i) Determine the duration of the bond to 3 decimals. Duration years Note: Use the purchase price to the closest cent in your duration calculation

1 point) Consider the continuously compounded yield curve y(T) 0.045 - 0.015e0."7. Consider a 2-year $ 1000 bond that's redeemable at par and pays semi-annual coupons at a rate of 42) 7%. (1) Determine the bond's purchase price. Purchase Price-$ (i) Determine the duration of the bond to 3 decimals. Duration Note: Use the purchase price to the closest cent in your duration calculation. years

1 point) Consider the continuously compounded yield curve y(T) 0.045 - 0.015e0."7. Consider a 2-year $ 1000 bond that's redeemable at par and pays semi-annual coupons at a rate of 42) 7%. (1) Determine the bond's purchase price. Purchase Price-$ (i) Determine the duration of the bond to 3 decimals. Duration Note: Use the purchase price to the closest cent in your duration calculation. years

Consider a 2-year $1000 par value bond that pays semi-annual coupons at a rate of 42) purchased for $1058.82 6%. Suppose that the bond was (a) Use the method of averages to approximate the effective yield rate compounded semi-annually. State the result as a percent to 1 decimal place % compounded semi-annually (b) Complete the chart below by performing 2 iterations of the bisection method to approximate the effective yield rate compounded semi-annually [Note: For the initial interval [a(0),b(0) use...

Consider a 2-year $1000 par value bond that pays semi-annual coupons at a rate of 42) purchased for $1058.82 6%. Suppose that the bond was (a) Use the method of averages to approximate the effective yield rate compounded semi-annually. State the result as a percent to 1 decimal place % compounded semi-annually (b) Complete the chart below by performing 2 iterations of the bisection method to approximate the effective yield rate compounded semi-annually [Note: For the initial interval [a(0),b(0) use...

Consider the following zero coupon bonds each of which are redeemable at par and have a yield rate of 3.5 % compounded continuously. Bond Face Value (in dollars) 4000 10000 5000 1000 Maturity (in years) 10 15 25 30 (a) Determine the purchase price of each bond: Bond Price (in dollars to closest cent) NOTE: Do not include the $ sign. (b) Determine the present value of the portfolio of bonds. NOTE: Do not include the $ sign. (b) Determine...

Consider the following zero coupon bonds each of which are redeemable at par and have a yield rate of 3.5 % compounded continuously. Bond Face Value (in dollars) 4000 10000 5000 1000 Maturity (in years) 10 15 25 30 (a) Determine the purchase price of each bond: Bond Price (in dollars to closest cent) NOTE: Do not include the $ sign. (b) Determine the present value of the portfolio of bonds. NOTE: Do not include the $ sign. (b) Determine...

6. A $10,000, 6% bond with semi-annual coupons is redeemable at par. What is the purchase price to yield 7.5% compounded semi-annually (a) nine years before maturity? (b) fifteen years before maturity? (a) The purchase price is $ (Round the final answer to the nearest cent as needed. Round all intermediate values to six decimal places as needed.) (b) The purchase price is $ (Round the final answer to the nearest cent as needed. Round all intermediate values to six...

6. A $10,000, 6% bond with semi-annual coupons is redeemable at par. What is the purchase price to yield 7.5% compounded semi-annually (a) nine years before maturity? (b) fifteen years before maturity? (a) The purchase price is $ (Round the final answer to the nearest cent as needed. Round all intermediate values to six decimal places as needed.) (b) The purchase price is $ (Round the final answer to the nearest cent as needed. Round all intermediate values to six...

● LOO A $1000 bond bearing interest at 8% payable 2 semi-annually redeemable at par on February 1, 2020, was purchased on October 12, 2013, to yield 7% compounded semi-annually. Determine the purchase price.

● LOO A $1000 bond bearing interest at 8% payable 2 semi-annually redeemable at par on February 1, 2020, was purchased on October 12, 2013, to yield 7% compounded semi-annually. Determine the purchase price.

● LOO A $1000 bond bearing interest at 8% payable 2 semi-annually redeemable at par on February 1, 2020, was purchased on October 12, 2013, to yield 7% compounded semi-annually. Determine the purchase price.

● LOO A $1000 bond bearing interest at 8% payable 2 semi-annually redeemable at par on February 1, 2020, was purchased on October 12, 2013, to yield 7% compounded semi-annually. Determine the purchase price.

Most questions answered within 3 hours.

-

Using MARS simulator, write MIPS programs according to

the following scenarios: Receive a positive integer number...

asked 10 minutes ago -

An object in front of a concave mirror has a real image that is

11.5 cm...

asked 24 minutes ago -

Consider the reaction, C3 H8 + O2 --> CO2 + H2O. How many

moles of O2...

asked 2 hours ago -

You and your opponent both roll a fair die. If you both roll the

same number,...

asked 2 hours ago -

In a study of the accuracy of fast food drive-through orders,

Restaurant A had 257 accurate...

asked 2 hours ago -

Identify and describe in detail the four categories of

institutions that could be included in a...

asked 2 hours ago -

In python

class Customer:

def __init__(self, customer_id, last_name, first_name, phone_number, address):

self._customer_id = int(customer_id)

self._last_name =...

asked 2 hours ago -

What is an example of a limitation in implementing a new

ERP system and how it...

asked 2 hours ago -

In a section of 9.7cm of an artery with a radius of 2.6mm there

is a...

asked 2 hours ago -

the two carboxylic acid groups of aspartic acid have different

acidities with pKa values of 2.1...

asked 2 hours ago -

Would CuCO3 aqueous salt combined with calcium chloride

form a solid precipitate? If so, what would...

asked 2 hours ago -

How do ECM Solutions assist in embedding a culture of continuous

improvement in an organization? (Project...

asked 2 hours ago