•Suppose that you forecast the GBP/USD exchange rate at the end of next year to be...

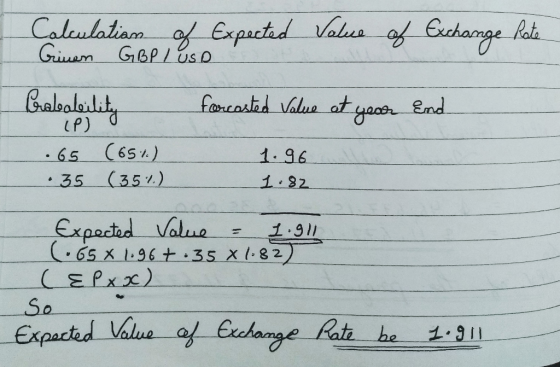

•Suppose that you forecast the GBP/USD exchange rate at the end of next year to be either:

•1.96 with a probability of 65%, or

1.82 with a probability of 35%

•What is the expected value of the exchange rate at the end of next year?

Homework Answers

Add Answer to:

•Suppose that you forecast the GBP/USD exchange rate at the end

of next year to be...

22 The spot ask USD/GBP exchange rate is $1.89 - £100. The spot bid USD/GBP exchange rate is $1.88 - £100. What is the...

22 The spot ask USD/GBP exchange rate is $1.89 - £100. The spot bid USD/GBP exchange rate is $1.88 - £100. What is the profit (loss) if an investor buys $10,000,000 worth of British pounds and simultaneously sell the pounds proceeds of that purchase? points Multiple Choice 302.50:11 0 ($52,910) 0 None of the options 0 (552,632) 0 $52,910 0 $52,632 The dollar-euro exchange rate is $1.40 - €1.00 and the dollar-yen exchange rate is 110 - $1.00. What is...

22 The spot ask USD/GBP exchange rate is $1.89 - £100. The spot bid USD/GBP exchange rate is $1.88 - £100. What is the profit (loss) if an investor buys $10,000,000 worth of British pounds and simultaneously sell the pounds proceeds of that purchase? points Multiple Choice 302.50:11 0 ($52,910) 0 None of the options 0 (552,632) 0 $52,910 0 $52,632 The dollar-euro exchange rate is $1.40 - €1.00 and the dollar-yen exchange rate is 110 - $1.00. What is...

Currently the spot exchange rate is $1.558 per pound (USD/GBP). The interest rate in the UK...

Currently the spot exchange rate is $1.558 per pound (USD/GBP). The interest rate in the UK is 6%. The one-year forward exchange rate is $1.5200/GBP. If interest rate parity holds, what must be the US interest rate for the same period?

2) The spot USD /GBP rate is 1.1505. The1 year t-bill rate in the US is...

2) The spot USD /GBP rate is 1.1505. The1 year t-bill rate in the US is .9335%. The 1 year rate in the UK is 0.7969%. a) Calculate the 1 year USD/GBP 1 year forward rate. b) If the observed 1 year forward rate is 1.35 USD/GBP, is there an arbitrage opportunity? How would you take advantage of this? Show all your transactions and steps.

2) The spot USD /GBP rate is 1.1505. The1 year t-bill rate in the US is .9335%. The 1 year rate in the UK is 0.7969%. a) Calculate the 1 year USD/GBP 1 year forward rate. b) If the observed 1 year forward rate is 1.35 USD/GBP, is there an arbitrage opportunity? How would you take advantage of this? Show all your transactions and steps.

Suppose that the exchange rate (spot price) of Euro in GBP (British Pound) is GBP 0.95. &nbs...

Suppose that the exchange rate (spot price) of Euro in GBP (British Pound) is GBP 0.95. In addition, assume that you can freely borrow and lend in GBP for any maturity at a rate of 2% per annum and that you can do the same in Euro at a rate of 1% per annum. Both rates are continuously compounded rates. Given these assumptions: Compute the forward price (exchange rate) of the GBP in Euro for delivery of the GBP in...

Country USD Nominal Rate 2.5% GBP 3.5% The above table contains nominal interest rate information for the United States...

Country USD Nominal Rate 2.5% GBP 3.5% The above table contains nominal interest rate information for the United States and Great Britain. Assume the current U.S. dollar-British spot rate is GBP0.6134/USD. what is the approximate forward exchange rate for delivery 360 days from now? [Assume the USD is the home currency (currency of interest)] 0 GBP 0.6195/USD GBP 0.6073/USD USD 0.6195/GBP 0 USD0.6073/GBP

Country USD Nominal Rate 2.5% GBP 3.5% The above table contains nominal interest rate information for the United States and Great Britain. Assume the current U.S. dollar-British spot rate is GBP0.6134/USD. what is the approximate forward exchange rate for delivery 360 days from now? [Assume the USD is the home currency (currency of interest)] 0 GBP 0.6195/USD GBP 0.6073/USD USD 0.6195/GBP 0 USD0.6073/GBP

Suppose your broker give you the following information: Spot exchange rate (USD/EUR) = 1.1370 One year...

Suppose your broker give you the following information: Spot exchange rate (USD/EUR) = 1.1370 One year forward rate (USD/EUR) = 1.1405 One year USD interest rate = 0.87% One year Euro interest rate = 0.65% a. Is there any violation of interest rate parity? b. How would you take advantage of any arbitrage situation? c. What is your profit? d. Suggest an equilibrium value for the forward rate

19 Suppose that the GBP is pegged to gold at £20 per ounce. The USD is...

19 Suppose that the GBP is pegged to gold at £20 per ounce. The USD is pegged to gold at $35 per ounce. This implies an exchange rate of $175/18. How might an Investor take advantage of situation if the current market exchange rate is $1.60/1£? Multiple Choice points 02-50-30 0 Buy gold at $35 per ounce. Convert the gold to $200 at $20 per ounce. Exchange the €200 for dollars at the current rate of $160 per pound 0...

19 Suppose that the GBP is pegged to gold at £20 per ounce. The USD is pegged to gold at $35 per ounce. This implies an exchange rate of $175/18. How might an Investor take advantage of situation if the current market exchange rate is $1.60/1£? Multiple Choice points 02-50-30 0 Buy gold at $35 per ounce. Convert the gold to $200 at $20 per ounce. Exchange the €200 for dollars at the current rate of $160 per pound 0...

5. Suppose that the current value of the S&P 500 stock index is USD 2600. Assume that the per ann...

5. Suppose that the current value of the S&P 500 stock index is USD 2600. Assume that the per annum rates of interest in USD and GBP(British Pound) are respectively 3% and 2% on a continuously compounded basis, and that the S&P 500 index pays a continuous dividend rate of 2% per annum. Finally, the spot exchange rate is USD1.3 per GBP. a) Compute the forward price of the S&P 500 in USD for delivery in one year. for delivery...

5. Suppose that the current value of the S&P 500 stock index is USD 2600. Assume that the per annum rates of interest in USD and GBP(British Pound) are respectively 3% and 2% on a continuously compounded basis, and that the S&P 500 index pays a continuous dividend rate of 2% per annum. Finally, the spot exchange rate is USD1.3 per GBP. a) Compute the forward price of the S&P 500 in USD for delivery in one year. for delivery...

Suppose that your firm is attempting to determine the euro/pound exchange rate and you have the...

Suppose that your firm is attempting to determine the euro/pound exchange rate and you have the following exchange rate information: GBP/USD = 1.5509 and the EUR/USD rate = 1.2194. Therefore, GBP1 = EUR ….. (round the number to 4 decimals)

Suppose the annual interest rate is 2 percent in the US and 4 percent in Germany, the spot exchange rate is USD 1.60 / E...

Suppose the annual interest rate is 2 percent in the US and 4 percent in Germany, the spot exchange rate is USD 1.60 / EUR, and the 1year forward rate is USD 1.58 / EUR. What is the arbitrage profit in USD at the end of the year if you start by borrowing USD 5,000,000?

22 The spot ask USD/GBP exchange rate is $1.89 - £100. The spot bid USD/GBP exchange rate is $1.88 - £100. What is the profit (loss) if an investor buys $10,000,000 worth of British pounds and simultaneously sell the pounds proceeds of that purchase? points Multiple Choice 302.50:11 0 ($52,910) 0 None of the options 0 (552,632) 0 $52,910 0 $52,632 The dollar-euro exchange rate is $1.40 - €1.00 and the dollar-yen exchange rate is 110 - $1.00. What is...

22 The spot ask USD/GBP exchange rate is $1.89 - £100. The spot bid USD/GBP exchange rate is $1.88 - £100. What is the profit (loss) if an investor buys $10,000,000 worth of British pounds and simultaneously sell the pounds proceeds of that purchase? points Multiple Choice 302.50:11 0 ($52,910) 0 None of the options 0 (552,632) 0 $52,910 0 $52,632 The dollar-euro exchange rate is $1.40 - €1.00 and the dollar-yen exchange rate is 110 - $1.00. What is...

2) The spot USD /GBP rate is 1.1505. The1 year t-bill rate in the US is .9335%. The 1 year rate in the UK is 0.7969%. a) Calculate the 1 year USD/GBP 1 year forward rate. b) If the observed 1 year forward rate is 1.35 USD/GBP, is there an arbitrage opportunity? How would you take advantage of this? Show all your transactions and steps.

2) The spot USD /GBP rate is 1.1505. The1 year t-bill rate in the US is .9335%. The 1 year rate in the UK is 0.7969%. a) Calculate the 1 year USD/GBP 1 year forward rate. b) If the observed 1 year forward rate is 1.35 USD/GBP, is there an arbitrage opportunity? How would you take advantage of this? Show all your transactions and steps.

Country USD Nominal Rate 2.5% GBP 3.5% The above table contains nominal interest rate information for the United States and Great Britain. Assume the current U.S. dollar-British spot rate is GBP0.6134/USD. what is the approximate forward exchange rate for delivery 360 days from now? [Assume the USD is the home currency (currency of interest)] 0 GBP 0.6195/USD GBP 0.6073/USD USD 0.6195/GBP 0 USD0.6073/GBP

Country USD Nominal Rate 2.5% GBP 3.5% The above table contains nominal interest rate information for the United States and Great Britain. Assume the current U.S. dollar-British spot rate is GBP0.6134/USD. what is the approximate forward exchange rate for delivery 360 days from now? [Assume the USD is the home currency (currency of interest)] 0 GBP 0.6195/USD GBP 0.6073/USD USD 0.6195/GBP 0 USD0.6073/GBP

19 Suppose that the GBP is pegged to gold at £20 per ounce. The USD is pegged to gold at $35 per ounce. This implies an exchange rate of $175/18. How might an Investor take advantage of situation if the current market exchange rate is $1.60/1£? Multiple Choice points 02-50-30 0 Buy gold at $35 per ounce. Convert the gold to $200 at $20 per ounce. Exchange the €200 for dollars at the current rate of $160 per pound 0...

19 Suppose that the GBP is pegged to gold at £20 per ounce. The USD is pegged to gold at $35 per ounce. This implies an exchange rate of $175/18. How might an Investor take advantage of situation if the current market exchange rate is $1.60/1£? Multiple Choice points 02-50-30 0 Buy gold at $35 per ounce. Convert the gold to $200 at $20 per ounce. Exchange the €200 for dollars at the current rate of $160 per pound 0...

5. Suppose that the current value of the S&P 500 stock index is USD 2600. Assume that the per annum rates of interest in USD and GBP(British Pound) are respectively 3% and 2% on a continuously compounded basis, and that the S&P 500 index pays a continuous dividend rate of 2% per annum. Finally, the spot exchange rate is USD1.3 per GBP. a) Compute the forward price of the S&P 500 in USD for delivery in one year. for delivery...

5. Suppose that the current value of the S&P 500 stock index is USD 2600. Assume that the per annum rates of interest in USD and GBP(British Pound) are respectively 3% and 2% on a continuously compounded basis, and that the S&P 500 index pays a continuous dividend rate of 2% per annum. Finally, the spot exchange rate is USD1.3 per GBP. a) Compute the forward price of the S&P 500 in USD for delivery in one year. for delivery...

Most questions answered within 3 hours.

-

4. Without doing any calculations, predict whether the observed

∆T would increase, decrease or remain the...

asked 1 hour ago -

Based on the range, which of the following sets of scores has

the greatest variability? 3,...

asked 2 hours ago -

Ripples in a pond travel at a velocity of 3 m/s with one peak

passing a...

asked 2 hours ago -

A man stands on the roof of a building of height 13.0 mm and

throws a...

asked 2 hours ago -

The extent to which assets are financed by borrowed funds and

other liabilities is indicated by:...

asked 3 hours ago -

Explain in detail

Germany is the fifth largest economy

explain what goods and services Germany specializes...

asked 3 hours ago -

The density of platinum is 21.45 g/mL. If a cube of platinum

with a mass of...

asked 3 hours ago -

Accounts Receivable

Sales

A/R Posting

Extended Sales Invoice

Packing Slip

Compare invoice to packing slip 2...

asked 3 hours ago -

Michaella, age 23, is a full-time law student and is claimed by

her parents as a...

asked 3 hours ago -

Why are polymers not typically casted into products?

asked 3 hours ago -

When rolling a die 129 times, what is the probability of rolling

a 6 no more...

asked 4 hours ago -

4. A call option currently sells for $7.75. It has a strike

price of $85 and...

asked 3 hours ago