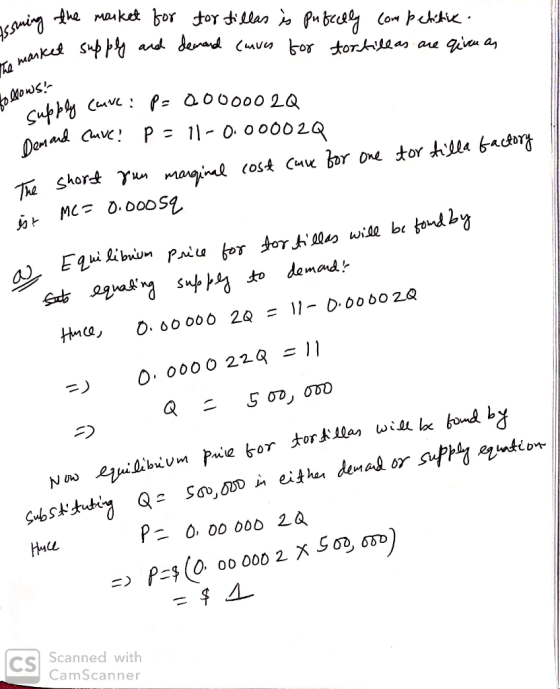

Assume the market for tortillas is perfectly competitive. The market supply and demand curves for tortillas...

Assume the market for tortillas is perfectly competitive. The market supply and demand curves for tortillas are given as follows:

Supply curve: P =0.000002Q

Demand curve: P = 11 - 0.00002Q

The short run marginal cost curve for one tortilla factory is: MC = 0.0005q

The firm's average variable cost curve intersects the marginal cost at a vertical distance of 0.1 above the horizontal axis.

a. Determine the equilibrium price for tortillas.

b. Determine the profit maximizing short run equilibrium level of output for the tortilla factory.

c. At the level of output determined above, is the factory making a profit, breaking even, or making a loss? Explain your answer.

d. Assuming that all of the tortilla factories are identical, how many tortilla factories are producing tortillas?

Homework Answers

Add Answer to:

Assume the market for tortillas is perfectly

competitive. The market supply and demand curves for tortillas...

1. Assume the market for tortillas is perfectly competitive. The market supply and demand curves for...

1. Assume the market for tortillas is perfectly competitive. The market supply and demand curves for tortillas are given as follows: Supply curve: P = 0.20 Demand curve: P = 1100 – 20 The short-run total cost curve for a typical tortilla factory, ABC, is: TC = 500 + 10 + 4.522 a) Determine the market equilibrium price and quantity. b) Determine the profit-maximizing level of output for factory ABC. c) Assuming that all of the factories are identical, how...

1. Assume the market for tortillas is perfectly competitive. The market supply and demand curves for tortillas are given as follows: Supply curve: P = 0.20 Demand curve: P = 1100 – 20 The short-run total cost curve for a typical tortilla factory, ABC, is: TC = 500 + 10 + 4.522 a) Determine the market equilibrium price and quantity. b) Determine the profit-maximizing level of output for factory ABC. c) Assuming that all of the factories are identical, how...

1. The market for tortillas is perfectly competitive, with market demand given by p 1.000022, with...

1. The market for tortillas is perfectly competitive, with market demand given by p 1.000022, with price in dollars per tortilla and Q in thousands of tortillas. The short-run marginal cost curve for a typical tortilla factory is MC 10+.0005q,with MC in dollars per tortilla and q in thousands of tortillas. The fixed cost of running a factory is $15,000 per firm. (a) If there are 50 identical factories, determine the short-run aggregate supply function. (b) What is the market...

1. The market for tortillas is perfectly competitive, with market demand given by p 1.000022, with price in dollars per tortilla and Q in thousands of tortillas. The short-run marginal cost curve for a typical tortilla factory is MC 10+.0005q,with MC in dollars per tortilla and q in thousands of tortillas. The fixed cost of running a factory is $15,000 per firm. (a) If there are 50 identical factories, determine the short-run aggregate supply function. (b) What is the market...

1. The market for tortillas is perfectly competitive, with market demand given by p 1-.000020, with...

1. The market for tortillas is perfectly competitive, with market demand given by p 1-.000020, with price in dollars per tortilla and Q in thousands of tortillas. The short-run marginal cost curve for a typical tortilla factory is MC = .10 + .0005g.with MC in dollars per tortilla and q in thousands of tortillas. The fixed cost of running a factory is $15,000 per firm. (a) If there are 50 identical factories, determine the short-run aggregate supply function. b) What...

1. The market for tortillas is perfectly competitive, with market demand given by p 1-.000020, with price in dollars per tortilla and Q in thousands of tortillas. The short-run marginal cost curve for a typical tortilla factory is MC = .10 + .0005g.with MC in dollars per tortilla and q in thousands of tortillas. The fixed cost of running a factory is $15,000 per firm. (a) If there are 50 identical factories, determine the short-run aggregate supply function. b) What...

#5 75. The graphs below show the market demand and supply curves for a good in...

#5

75. The graphs below show the market demand and supply curves for a good in a perfectly competitive industry along with a representative firm's short-run average and marginal cost curves. a. Determine the equilibrium price (label Pe) and output (label Qe) in the market. b. Draw the firm's demand (label d) and marginal revenue (label MR) curve. c. Determine the profit maximizing output (label 4). Explain why this is the profit-maximizing output d. Is the firm earning a profit...

#5

75. The graphs below show the market demand and supply curves for a good in a perfectly competitive industry along with a representative firm's short-run average and marginal cost curves. a. Determine the equilibrium price (label Pe) and output (label Qe) in the market. b. Draw the firm's demand (label d) and marginal revenue (label MR) curve. c. Determine the profit maximizing output (label 4). Explain why this is the profit-maximizing output d. Is the firm earning a profit...

31 In perfectly competitive industries: A. the shont-run market supply curves are positively sloped в. long-rusniustry...

31 In perfectly competitive industries: A. the shont-run market supply curves are positively sloped в. long-rusniustry supply curve,are positively sloped. C. the short-run D. All of the above E. Only B and C are correct market supply curves are more clastic than the long-run industry supply curvers s3. Assame a perfectly-competitive, increasing-cost industry composed of identical firms is initially in long-run equilibrium. Given a decrease in demand, in the short ran: equilbrium price decreases, equilibrium output increases, the output of...

31 In perfectly competitive industries: A. the shont-run market supply curves are positively sloped в. long-rusniustry supply curve,are positively sloped. C. the short-run D. All of the above E. Only B and C are correct market supply curves are more clastic than the long-run industry supply curvers s3. Assame a perfectly-competitive, increasing-cost industry composed of identical firms is initially in long-run equilibrium. Given a decrease in demand, in the short ran: equilbrium price decreases, equilibrium output increases, the output of...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve and supply curve are as follows: Demand: Qp = 2000-P Supply: 2 = 1400 +2P Firm K is one of the many firms producing popcorn in the market. The total cost function and marginal cost function are as follows: TC(q) =1250 +30 +29 MC(q) - 30 +49 i At what output level (g) would the average total cost be minimized? (6 marks) ii What...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve and supply curve are as follows: Demand: Qp = 2000-P Supply: 2 = 1400 +2P Firm K is one of the many firms producing popcorn in the market. The total cost function and marginal cost function are as follows: TC(q) =1250 +30 +29 MC(q) - 30 +49 i At what output level (g) would the average total cost be minimized? (6 marks) ii What...

Suppose the market for canola oil is perfectly competitive. There are 1,000 firms in the market,...

Suppose the market for canola oil is perfectly competitive. There are 1,000 firms in the market, each of which have a fixed cost of FC=2 and a marginal cost of MC= 1+Q, where q is quantity produced by an individual firm. Let QS denote the total quantity supplied in the market. The market demand is QD= 15,250-250P A) Find the market supply equation, that is write QS as a function of price P B)What is the equilibrium price? What is...

1. Let the market demand curve be P=1000 - 10Q. Assume the market is controlled by...

1. Let the market demand curve be P=1000 - 10Q. Assume the market is controlled by a monopolist. Let fixed cost be $10,000 and Marginal Costs (MC)=20Q. a) What is the profit maximizing output? b) What is the monopolist's total revenue at the profit maximizing output? c) How much profit is the monopolist earning? d) Assume the government breaks up the monopolist in order to create a perfectly competitive market of identical firms. Assume the MC curve is now the...

5. Short-run supply and long-run equilibrium Consider the perfectly competitive market for steel. Assume that, regardless...

5. Short-run supply and long-run equilibrium Consider the perfectly competitive market for steel. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. COSTS (Dollars per ton) + MC D AVC 0 10 90 100 20 30 40 50 60 70 80 QUANTITY (Thousands of tons) The following diagram shows the...

5. Short-run supply and long-run equilibrium Consider the perfectly competitive market for steel. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. COSTS (Dollars per ton) + MC D AVC 0 10 90 100 20 30 40 50 60 70 80 QUANTITY (Thousands of tons) The following diagram shows the...

Exercise 1. Short-Run Industry Supply Curve In a perfectly competitive market there are n firms with...

Exercise 1. Short-Run Industry Supply Curve In a perfectly competitive market there are n firms with identical technology: yi=Li½Ki½. Each firm’s cost function is Ci=wLi+rKi where w=r=1. a) In the short run all firms have a fixed level of Ki=100, so that yi=10Li½ and Ci=Li+100. What is the cost function Ci(yi)? What is the short-run average cost function ACi(yi)? b) What is each firm’s marginal cost function MCi(yi)? What is each firm’s short-run supply function si(p)? Find the inverse of...

1. Assume the market for tortillas is perfectly competitive. The market supply and demand curves for tortillas are given as follows: Supply curve: P = 0.20 Demand curve: P = 1100 – 20 The short-run total cost curve for a typical tortilla factory, ABC, is: TC = 500 + 10 + 4.522 a) Determine the market equilibrium price and quantity. b) Determine the profit-maximizing level of output for factory ABC. c) Assuming that all of the factories are identical, how...

1. Assume the market for tortillas is perfectly competitive. The market supply and demand curves for tortillas are given as follows: Supply curve: P = 0.20 Demand curve: P = 1100 – 20 The short-run total cost curve for a typical tortilla factory, ABC, is: TC = 500 + 10 + 4.522 a) Determine the market equilibrium price and quantity. b) Determine the profit-maximizing level of output for factory ABC. c) Assuming that all of the factories are identical, how...

1. The market for tortillas is perfectly competitive, with market demand given by p 1.000022, with price in dollars per tortilla and Q in thousands of tortillas. The short-run marginal cost curve for a typical tortilla factory is MC 10+.0005q,with MC in dollars per tortilla and q in thousands of tortillas. The fixed cost of running a factory is $15,000 per firm. (a) If there are 50 identical factories, determine the short-run aggregate supply function. (b) What is the market...

1. The market for tortillas is perfectly competitive, with market demand given by p 1.000022, with price in dollars per tortilla and Q in thousands of tortillas. The short-run marginal cost curve for a typical tortilla factory is MC 10+.0005q,with MC in dollars per tortilla and q in thousands of tortillas. The fixed cost of running a factory is $15,000 per firm. (a) If there are 50 identical factories, determine the short-run aggregate supply function. (b) What is the market...

1. The market for tortillas is perfectly competitive, with market demand given by p 1-.000020, with price in dollars per tortilla and Q in thousands of tortillas. The short-run marginal cost curve for a typical tortilla factory is MC = .10 + .0005g.with MC in dollars per tortilla and q in thousands of tortillas. The fixed cost of running a factory is $15,000 per firm. (a) If there are 50 identical factories, determine the short-run aggregate supply function. b) What...

1. The market for tortillas is perfectly competitive, with market demand given by p 1-.000020, with price in dollars per tortilla and Q in thousands of tortillas. The short-run marginal cost curve for a typical tortilla factory is MC = .10 + .0005g.with MC in dollars per tortilla and q in thousands of tortillas. The fixed cost of running a factory is $15,000 per firm. (a) If there are 50 identical factories, determine the short-run aggregate supply function. b) What...

#5

75. The graphs below show the market demand and supply curves for a good in a perfectly competitive industry along with a representative firm's short-run average and marginal cost curves. a. Determine the equilibrium price (label Pe) and output (label Qe) in the market. b. Draw the firm's demand (label d) and marginal revenue (label MR) curve. c. Determine the profit maximizing output (label 4). Explain why this is the profit-maximizing output d. Is the firm earning a profit...

#5

75. The graphs below show the market demand and supply curves for a good in a perfectly competitive industry along with a representative firm's short-run average and marginal cost curves. a. Determine the equilibrium price (label Pe) and output (label Qe) in the market. b. Draw the firm's demand (label d) and marginal revenue (label MR) curve. c. Determine the profit maximizing output (label 4). Explain why this is the profit-maximizing output d. Is the firm earning a profit...

31 In perfectly competitive industries: A. the shont-run market supply curves are positively sloped в. long-rusniustry supply curve,are positively sloped. C. the short-run D. All of the above E. Only B and C are correct market supply curves are more clastic than the long-run industry supply curvers s3. Assame a perfectly-competitive, increasing-cost industry composed of identical firms is initially in long-run equilibrium. Given a decrease in demand, in the short ran: equilbrium price decreases, equilibrium output increases, the output of...

31 In perfectly competitive industries: A. the shont-run market supply curves are positively sloped в. long-rusniustry supply curve,are positively sloped. C. the short-run D. All of the above E. Only B and C are correct market supply curves are more clastic than the long-run industry supply curvers s3. Assame a perfectly-competitive, increasing-cost industry composed of identical firms is initially in long-run equilibrium. Given a decrease in demand, in the short ran: equilbrium price decreases, equilibrium output increases, the output of...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve and supply curve are as follows: Demand: Qp = 2000-P Supply: 2 = 1400 +2P Firm K is one of the many firms producing popcorn in the market. The total cost function and marginal cost function are as follows: TC(q) =1250 +30 +29 MC(q) - 30 +49 i At what output level (g) would the average total cost be minimized? (6 marks) ii What...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve and supply curve are as follows: Demand: Qp = 2000-P Supply: 2 = 1400 +2P Firm K is one of the many firms producing popcorn in the market. The total cost function and marginal cost function are as follows: TC(q) =1250 +30 +29 MC(q) - 30 +49 i At what output level (g) would the average total cost be minimized? (6 marks) ii What...

5. Short-run supply and long-run equilibrium Consider the perfectly competitive market for steel. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. COSTS (Dollars per ton) + MC D AVC 0 10 90 100 20 30 40 50 60 70 80 QUANTITY (Thousands of tons) The following diagram shows the...

5. Short-run supply and long-run equilibrium Consider the perfectly competitive market for steel. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. COSTS (Dollars per ton) + MC D AVC 0 10 90 100 20 30 40 50 60 70 80 QUANTITY (Thousands of tons) The following diagram shows the...

Most questions answered within 3 hours.

-

What is the yield to maturity of a ten-year, $1,000 bond with a

5.2% coupon rate...

asked 31 minutes ago -

A mass m = 5 kg is tied on one end of a rope and is...

asked 36 minutes ago -

The Average sales price of single-family houses in Charlotte is

$210,000 with a standard deviation of...

asked 44 minutes ago -

Target Costing

Laser Impressions, Inc., manufactures color laser printers.

Model J20 presently sells for $225 and...

asked 50 minutes ago -

a bottle cap manufacturer with four machines and six operators

wants to see if variation in...

asked 1 hour ago -

State Farm Insurance studies show that in Colorado, 55% of the

auto insurance claims submitted for...

asked 2 hours ago -

Complete the following reactions which form ethers (A

and B) and cyclic ethers (C-E) as major...

asked 2 hours ago -

in a perfectly elastic collision what is the velocity of ball A

if the original direction...

asked 3 hours ago -

PLEASE ANSWER ALL

1) The pressure of the atmosphere decreases with increasing

altitude in the

Choose...

asked 3 hours ago -

A simple random sample of 25,000 individuals are surveyed in

order to determine the prevalence of...

asked 3 hours ago -

People who do very detailed work close up, such as jewelers,

often can see objects clearly...

asked 3 hours ago -

14 years ago, Blue Lake Corp. issued 30 year to maturity

zero-coupon bonds with a par...

asked 3 hours ago