Homework Answers

Add Answer to:

1. Assume the market for tortillas is perfectly competitive. The market supply and demand curves for...

Assume the market for tortillas is perfectly competitive. The market supply and demand curves for tortillas...

Assume the market for tortillas is perfectly competitive. The market supply and demand curves for tortillas are given as follows: Supply curve: P =0.000002Q Demand curve: P = 11 - 0.00002Q The short run marginal cost curve for one tortilla factory is: MC = 0.0005q The firm's average variable cost curve intersects the marginal cost at a vertical distance of 0.1 above the horizontal axis. a. Determine the equilibrium price for tortillas. b. Determine the profit maximizing short run equilibrium...

1. The market for tortillas is perfectly competitive, with market demand given by p 1.000022, with...

1. The market for tortillas is perfectly competitive, with market demand given by p 1.000022, with price in dollars per tortilla and Q in thousands of tortillas. The short-run marginal cost curve for a typical tortilla factory is MC 10+.0005q,with MC in dollars per tortilla and q in thousands of tortillas. The fixed cost of running a factory is $15,000 per firm. (a) If there are 50 identical factories, determine the short-run aggregate supply function. (b) What is the market...

1. The market for tortillas is perfectly competitive, with market demand given by p 1.000022, with price in dollars per tortilla and Q in thousands of tortillas. The short-run marginal cost curve for a typical tortilla factory is MC 10+.0005q,with MC in dollars per tortilla and q in thousands of tortillas. The fixed cost of running a factory is $15,000 per firm. (a) If there are 50 identical factories, determine the short-run aggregate supply function. (b) What is the market...

1. The market for tortillas is perfectly competitive, with market demand given by p 1-.000020, with...

1. The market for tortillas is perfectly competitive, with market demand given by p 1-.000020, with price in dollars per tortilla and Q in thousands of tortillas. The short-run marginal cost curve for a typical tortilla factory is MC = .10 + .0005g.with MC in dollars per tortilla and q in thousands of tortillas. The fixed cost of running a factory is $15,000 per firm. (a) If there are 50 identical factories, determine the short-run aggregate supply function. b) What...

1. The market for tortillas is perfectly competitive, with market demand given by p 1-.000020, with price in dollars per tortilla and Q in thousands of tortillas. The short-run marginal cost curve for a typical tortilla factory is MC = .10 + .0005g.with MC in dollars per tortilla and q in thousands of tortillas. The fixed cost of running a factory is $15,000 per firm. (a) If there are 50 identical factories, determine the short-run aggregate supply function. b) What...

#5 75. The graphs below show the market demand and supply curves for a good in...

#5

75. The graphs below show the market demand and supply curves for a good in a perfectly competitive industry along with a representative firm's short-run average and marginal cost curves. a. Determine the equilibrium price (label Pe) and output (label Qe) in the market. b. Draw the firm's demand (label d) and marginal revenue (label MR) curve. c. Determine the profit maximizing output (label 4). Explain why this is the profit-maximizing output d. Is the firm earning a profit...

#5

75. The graphs below show the market demand and supply curves for a good in a perfectly competitive industry along with a representative firm's short-run average and marginal cost curves. a. Determine the equilibrium price (label Pe) and output (label Qe) in the market. b. Draw the firm's demand (label d) and marginal revenue (label MR) curve. c. Determine the profit maximizing output (label 4). Explain why this is the profit-maximizing output d. Is the firm earning a profit...

Assume Pork and chicken market in China is perfectly competitive and 1000 firms are producing the...

Assume Pork and chicken market in China is perfectly competitive and 1000 firms are producing the pork. Following equations shows the TC for the production for short run and long run. Qd = 5000-4p STC(q) = 100 + 10q +q2 TC(q) = 100q – 2q2 + 0.2 q3 13.6 What is the short run shut down price, Ps? 13.7 Given 13.6, what is the equation for the short run supply curve for a producer? 13.8 What is the short run...

Exercise 1. Short-Run Industry Supply Curve In a perfectly competitive market there are n firms with...

Exercise 1. Short-Run Industry Supply Curve In a perfectly competitive market there are n firms with identical technology: yi=Li½Ki½. Each firm’s cost function is Ci=wLi+rKi where w=r=1. a) In the short run all firms have a fixed level of Ki=100, so that yi=10Li½ and Ci=Li+100. What is the cost function Ci(yi)? What is the short-run average cost function ACi(yi)? b) What is each firm’s marginal cost function MCi(yi)? What is each firm’s short-run supply function si(p)? Find the inverse of...

[1] A perfectly competitive aluminum producer is currently producing a quantity where the market price is...

[1] A perfectly competitive aluminum producer is currently producing a quantity where the market price is $0.67 per pound (i.e., 67 cents per pound), average total cost is $0.70, and average variable cost of $0.60 (which corresponds to the minimum point on the average variable cost curve). Would you recommend this firm expand output, contract output, or shut down in the short-run? Provide a graph to illustrate your answer. [2] Suppose the local crawfish market is perfectly competitive, with the...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve and supply curve are as follows: Demand: Qp = 2000-P Supply: 2 = 1400 +2P Firm K is one of the many firms producing popcorn in the market. The total cost function and marginal cost function are as follows: TC(q) =1250 +30 +29 MC(q) - 30 +49 i At what output level (g) would the average total cost be minimized? (6 marks) ii What...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve and supply curve are as follows: Demand: Qp = 2000-P Supply: 2 = 1400 +2P Firm K is one of the many firms producing popcorn in the market. The total cost function and marginal cost function are as follows: TC(q) =1250 +30 +29 MC(q) - 30 +49 i At what output level (g) would the average total cost be minimized? (6 marks) ii What...

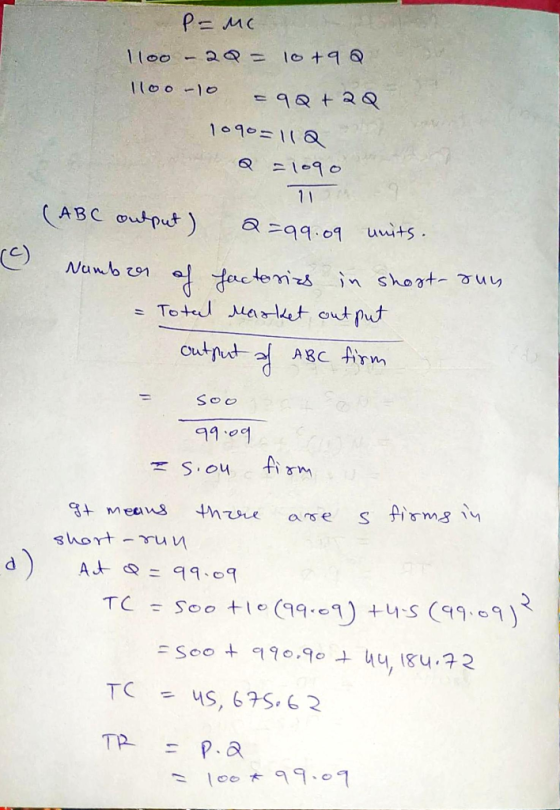

Question 2 The tortilla industry commissions you to examine the outlook for firms selling tortillas. There...

Question 2 The tortilla industry commissions you to examine the outlook for firms selling tortillas. There are currently twenty, identical price-taking firms in this perfectly competitive market. Each firm has a short-run cost function of STC(Q) = 9+ 2Q + . When the price is P, the total quantity demanded is given by Q(P) = 100 – 2P . (a) Assuming all fixed costs are sunk, find the short-run supply curve for a typical firm. (b) In the short run,...

Question 2 The tortilla industry commissions you to examine the outlook for firms selling tortillas. There are currently twenty, identical price-taking firms in this perfectly competitive market. Each firm has a short-run cost function of STC(Q) = 9+ 2Q + . When the price is P, the total quantity demanded is given by Q(P) = 100 – 2P . (a) Assuming all fixed costs are sunk, find the short-run supply curve for a typical firm. (b) In the short run,...

31 In perfectly competitive industries: A. the shont-run market supply curves are positively sloped в. long-rusniustry...

31 In perfectly competitive industries: A. the shont-run market supply curves are positively sloped в. long-rusniustry supply curve,are positively sloped. C. the short-run D. All of the above E. Only B and C are correct market supply curves are more clastic than the long-run industry supply curvers s3. Assame a perfectly-competitive, increasing-cost industry composed of identical firms is initially in long-run equilibrium. Given a decrease in demand, in the short ran: equilbrium price decreases, equilibrium output increases, the output of...

31 In perfectly competitive industries: A. the shont-run market supply curves are positively sloped в. long-rusniustry supply curve,are positively sloped. C. the short-run D. All of the above E. Only B and C are correct market supply curves are more clastic than the long-run industry supply curvers s3. Assame a perfectly-competitive, increasing-cost industry composed of identical firms is initially in long-run equilibrium. Given a decrease in demand, in the short ran: equilbrium price decreases, equilibrium output increases, the output of...

1. The market for tortillas is perfectly competitive, with market demand given by p 1.000022, with price in dollars per tortilla and Q in thousands of tortillas. The short-run marginal cost curve for a typical tortilla factory is MC 10+.0005q,with MC in dollars per tortilla and q in thousands of tortillas. The fixed cost of running a factory is $15,000 per firm. (a) If there are 50 identical factories, determine the short-run aggregate supply function. (b) What is the market...

1. The market for tortillas is perfectly competitive, with market demand given by p 1.000022, with price in dollars per tortilla and Q in thousands of tortillas. The short-run marginal cost curve for a typical tortilla factory is MC 10+.0005q,with MC in dollars per tortilla and q in thousands of tortillas. The fixed cost of running a factory is $15,000 per firm. (a) If there are 50 identical factories, determine the short-run aggregate supply function. (b) What is the market...

1. The market for tortillas is perfectly competitive, with market demand given by p 1-.000020, with price in dollars per tortilla and Q in thousands of tortillas. The short-run marginal cost curve for a typical tortilla factory is MC = .10 + .0005g.with MC in dollars per tortilla and q in thousands of tortillas. The fixed cost of running a factory is $15,000 per firm. (a) If there are 50 identical factories, determine the short-run aggregate supply function. b) What...

1. The market for tortillas is perfectly competitive, with market demand given by p 1-.000020, with price in dollars per tortilla and Q in thousands of tortillas. The short-run marginal cost curve for a typical tortilla factory is MC = .10 + .0005g.with MC in dollars per tortilla and q in thousands of tortillas. The fixed cost of running a factory is $15,000 per firm. (a) If there are 50 identical factories, determine the short-run aggregate supply function. b) What...

#5

75. The graphs below show the market demand and supply curves for a good in a perfectly competitive industry along with a representative firm's short-run average and marginal cost curves. a. Determine the equilibrium price (label Pe) and output (label Qe) in the market. b. Draw the firm's demand (label d) and marginal revenue (label MR) curve. c. Determine the profit maximizing output (label 4). Explain why this is the profit-maximizing output d. Is the firm earning a profit...

#5

75. The graphs below show the market demand and supply curves for a good in a perfectly competitive industry along with a representative firm's short-run average and marginal cost curves. a. Determine the equilibrium price (label Pe) and output (label Qe) in the market. b. Draw the firm's demand (label d) and marginal revenue (label MR) curve. c. Determine the profit maximizing output (label 4). Explain why this is the profit-maximizing output d. Is the firm earning a profit...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve and supply curve are as follows: Demand: Qp = 2000-P Supply: 2 = 1400 +2P Firm K is one of the many firms producing popcorn in the market. The total cost function and marginal cost function are as follows: TC(q) =1250 +30 +29 MC(q) - 30 +49 i At what output level (g) would the average total cost be minimized? (6 marks) ii What...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve and supply curve are as follows: Demand: Qp = 2000-P Supply: 2 = 1400 +2P Firm K is one of the many firms producing popcorn in the market. The total cost function and marginal cost function are as follows: TC(q) =1250 +30 +29 MC(q) - 30 +49 i At what output level (g) would the average total cost be minimized? (6 marks) ii What...

Question 2 The tortilla industry commissions you to examine the outlook for firms selling tortillas. There are currently twenty, identical price-taking firms in this perfectly competitive market. Each firm has a short-run cost function of STC(Q) = 9+ 2Q + . When the price is P, the total quantity demanded is given by Q(P) = 100 – 2P . (a) Assuming all fixed costs are sunk, find the short-run supply curve for a typical firm. (b) In the short run,...

Question 2 The tortilla industry commissions you to examine the outlook for firms selling tortillas. There are currently twenty, identical price-taking firms in this perfectly competitive market. Each firm has a short-run cost function of STC(Q) = 9+ 2Q + . When the price is P, the total quantity demanded is given by Q(P) = 100 – 2P . (a) Assuming all fixed costs are sunk, find the short-run supply curve for a typical firm. (b) In the short run,...

31 In perfectly competitive industries: A. the shont-run market supply curves are positively sloped в. long-rusniustry supply curve,are positively sloped. C. the short-run D. All of the above E. Only B and C are correct market supply curves are more clastic than the long-run industry supply curvers s3. Assame a perfectly-competitive, increasing-cost industry composed of identical firms is initially in long-run equilibrium. Given a decrease in demand, in the short ran: equilbrium price decreases, equilibrium output increases, the output of...

31 In perfectly competitive industries: A. the shont-run market supply curves are positively sloped в. long-rusniustry supply curve,are positively sloped. C. the short-run D. All of the above E. Only B and C are correct market supply curves are more clastic than the long-run industry supply curvers s3. Assame a perfectly-competitive, increasing-cost industry composed of identical firms is initially in long-run equilibrium. Given a decrease in demand, in the short ran: equilbrium price decreases, equilibrium output increases, the output of...

Most questions answered within 3 hours.

-

The value of the equilibrium constant Kc for the reaction

N2(g)+3H2(g)⇌2NH3(g) changes in the following manner...

asked 4 minutes ago -

There are two flasks on the bench top, one flask contains a 0.50

M NaCl solution...

asked 10 minutes ago -

Which of the following aqueous solutions are good buffer

systems?

.

0.10 M hydrofluoric acid +...

asked 11 minutes ago -

2. An S election is terminated if the S corporation has passive

investment income in excess...

asked 13 minutes ago -

Part of an ANOVA table is shown below.

Source of

Variation

Sum of

Squares

Degrees of...

asked 30 minutes ago -

Business process improvement initiatives often include

introducing new technology to support the new or changed ways...

asked 36 minutes ago -

Review your choice of either Agile or the Waterfall models and

for each of the 22...

asked 37 minutes ago -

Suppose an x distribution has mean μ = 4.

Consider two corresponding

x

distributions, the first...

asked 39 minutes ago -

A study of the effects of exercise used rats bred to have high

or low capacity...

asked 1 hour ago -

Using your data from the experiment, calculate the initial moles

of HCl that you started with....

asked 1 hour ago -

Suppose you want to make 500 mL of a 0.20 M Tris buffer at pH

8.0....

asked 1 hour ago -

The titanic hit an iceberg estimated to be half of her mass.

Before hitting the iceberg,...

asked 1 hour ago