Homework Answers

SEE THE IMAGE. ANY DOUBTS, FEEL FREE TO ASK. THUMBS UP PLEASE

Add Answer to:

The yield to maturity on 1-year zero-coupon bonds is currently 6.5%; the YTM on 2-year zeros...

The yield to maturity on 1-year zero-coupon bonds is currently 4.5%; the YTM on 2-year zeros...

The yield to maturity on 1-year zero-coupon bonds is currently 4.5%; the YTM on 2-year zeros is 5.5%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 6% The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Price b. What will the yield to maturity on the bond be? (Do...

The yield to maturity on 1-year zero-coupon bonds is currently 4.5%; the YTM on 2-year zeros is 5.5%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 6% The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Price b. What will the yield to maturity on the bond be? (Do...

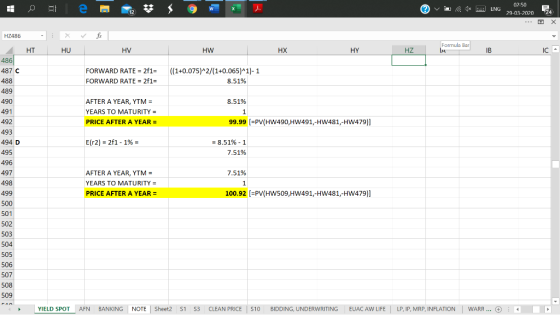

15.5 The yield to maturity on 1-year zero-coupon bonds is currently 7.5%; the YTM on 2-year...

15.5 The yield to maturity on 1-year zero-coupon bonds is currently 7.5%; the YTM on 2-year zeros is 8.5%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 9.5%. The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places.) b. What will the yield to maturity on the bond be? (Do...

The yield to maturity on 1-year zero-coupon bonds is currently 7%; the YTM on 2-year zeros is 8%. The Government plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupo...

The yield to maturity on 1-year zero-coupon bonds is currently 7%; the YTM on 2-year zeros is 8%. The Government plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 9%. The face value of the bond is $100. a. At what price will the bond sell? b. What will the yield to maturity on the bond be? (Hint: Use a financial calculator to get the YTM) c. If the expectations theory...

The yield to maturity on one-year zero-coupon bonds is 7.1%. The yield to maturity on two-year...

The yield to maturity on one-year zero-coupon bonds is 7.1%. The yield to maturity on two-year zero-coupon bonds is 8.1%. a. What is the forward rate of interest for the second year? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Answer is complete and correct. Forward rate of interest 9.10 % b. If you believe in the expectations hypothesis, what is your best guess as to the expected value of the short-term interest rate next year?...

The yield to maturity on one-year zero-coupon bonds is 7.1%. The yield to maturity on two-year zero-coupon bonds is 8.1%. a. What is the forward rate of interest for the second year? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Answer is complete and correct. Forward rate of interest 9.10 % b. If you believe in the expectations hypothesis, what is your best guess as to the expected value of the short-term interest rate next year?...

The yield to maturity on one-year zero-coupon bonds is 8.2%. The yield to maturity on two-year zero-coupon bonds is 9.2%. a. What is the forward rate of interest for the second year? (Do not round in...

The yield to maturity on one-year zero-coupon bonds is 8.2%. The yield to maturity on two-year zero-coupon bonds is 9.2%. a. What is the forward rate of interest for the second year? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Forward rate of interest b. If you believe in the expectations hypothesis, what is your best guess as to the expected value of the short-term interest rate next year? (Do not r answer to 2 decimal...

The yield to maturity on one-year zero-coupon bonds is 8.2%. The yield to maturity on two-year zero-coupon bonds is 9.2%. a. What is the forward rate of interest for the second year? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Forward rate of interest b. If you believe in the expectations hypothesis, what is your best guess as to the expected value of the short-term interest rate next year? (Do not r answer to 2 decimal...

The yield to maturity (YTM) on 1-year zero-coupon bonds is 4% and the YTM on 2-year...

The yield to maturity (YTM) on 1-year zero-coupon bonds is 4% and the YTM on 2-year zeros is 5%. The yield to maturity on 2-year-maturity coupon bonds with coupon rates of 9% (paid annually) is 4.5%. a. What arbitrage opportunity is available for an investment banking firm? and $ The arbitrage strategy is to buy zeros with face values of $ , and respective maturities of one year and two years. b. What is the profit on the activity? (Do...

The yield to maturity (YTM) on 1-year zero-coupon bonds is 4% and the YTM on 2-year zeros is 5%. The yield to maturity on 2-year-maturity coupon bonds with coupon rates of 9% (paid annually) is 4.5%. a. What arbitrage opportunity is available for an investment banking firm? and $ The arbitrage strategy is to buy zeros with face values of $ , and respective maturities of one year and two years. b. What is the profit on the activity? (Do...

The yield to maturity (YTM) on 1-year zero-coupon bonds is 5% and the YTM on 2-year...

The yield to maturity (YTM) on 1-year zero-coupon bonds is 5% and the YTM on 2-year zeros is 6%. The yield to maturity on 2-year- maturity coupon bonds with coupon rates of 9% (paid annually) is 5.9%. a. What arbitrage opportunity is available for an investment banking firm? The arbitrage strategy is to buy zeros with face values of $ D and $C , and respective maturities of one year and two years. b. What is the profit on the...

The yield to maturity (YTM) on 1-year zero-coupon bonds is 5% and the YTM on 2-year zeros is 6%. The yield to maturity on 2-year- maturity coupon bonds with coupon rates of 9% (paid annually) is 5.9%. a. What arbitrage opportunity is available for an investment banking firm? The arbitrage strategy is to buy zeros with face values of $ D and $C , and respective maturities of one year and two years. b. What is the profit on the...

Problem 15-17 The current yield curve for default-free zero-coupon bonds is as follows: Maturity (Years) YTM...

Problem 15-17 The current yield curve for default-free zero-coupon bonds is as follows: Maturity (Years) YTM (%) 5% 2 a. What are the implied 1-year forward rates? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Answer is complete but not entirely correct. Maturity 2 years Forward Rate 7.00 % 10.00 X % 3 years b. Assume that the pure expectations hypothesis of the term structure is correct. If market expectations are accurate, what will be the...

Problem 15-17 The current yield curve for default-free zero-coupon bonds is as follows: Maturity (Years) YTM (%) 5% 2 a. What are the implied 1-year forward rates? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Answer is complete but not entirely correct. Maturity 2 years Forward Rate 7.00 % 10.00 X % 3 years b. Assume that the pure expectations hypothesis of the term structure is correct. If market expectations are accurate, what will be the...

Consider the following $1,000 par value zero-coupon bonds: Bond Years to Maturity YTM(%) 5.7% 6.7 7.2...

Consider the following $1,000 par value zero-coupon bonds: Bond Years to Maturity YTM(%) 5.7% 6.7 7.2 7.7 According to the expectations hypothesis, what is the expected 1-year interest rate 3 years from now? (Do not round intermediate calculations. Round your answer to 2 decimal places. Omit the "%" sign in your response.) Interest rate

Consider the following $1,000 par value zero-coupon bonds: Bond Years to Maturity YTM(%) 5.7% 6.7 7.2 7.7 According to the expectations hypothesis, what is the expected 1-year interest rate 3 years from now? (Do not round intermediate calculations. Round your answer to 2 decimal places. Omit the "%" sign in your response.) Interest rate

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) F...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

The yield to maturity on 1-year zero-coupon bonds is currently 4.5%; the YTM on 2-year zeros is 5.5%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 6% The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Price b. What will the yield to maturity on the bond be? (Do...

The yield to maturity on 1-year zero-coupon bonds is currently 4.5%; the YTM on 2-year zeros is 5.5%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 6% The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Price b. What will the yield to maturity on the bond be? (Do...

The yield to maturity on one-year zero-coupon bonds is 7.1%. The yield to maturity on two-year zero-coupon bonds is 8.1%. a. What is the forward rate of interest for the second year? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Answer is complete and correct. Forward rate of interest 9.10 % b. If you believe in the expectations hypothesis, what is your best guess as to the expected value of the short-term interest rate next year?...

The yield to maturity on one-year zero-coupon bonds is 7.1%. The yield to maturity on two-year zero-coupon bonds is 8.1%. a. What is the forward rate of interest for the second year? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Answer is complete and correct. Forward rate of interest 9.10 % b. If you believe in the expectations hypothesis, what is your best guess as to the expected value of the short-term interest rate next year?...

The yield to maturity on one-year zero-coupon bonds is 8.2%. The yield to maturity on two-year zero-coupon bonds is 9.2%. a. What is the forward rate of interest for the second year? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Forward rate of interest b. If you believe in the expectations hypothesis, what is your best guess as to the expected value of the short-term interest rate next year? (Do not r answer to 2 decimal...

The yield to maturity on one-year zero-coupon bonds is 8.2%. The yield to maturity on two-year zero-coupon bonds is 9.2%. a. What is the forward rate of interest for the second year? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Forward rate of interest b. If you believe in the expectations hypothesis, what is your best guess as to the expected value of the short-term interest rate next year? (Do not r answer to 2 decimal...

The yield to maturity (YTM) on 1-year zero-coupon bonds is 4% and the YTM on 2-year zeros is 5%. The yield to maturity on 2-year-maturity coupon bonds with coupon rates of 9% (paid annually) is 4.5%. a. What arbitrage opportunity is available for an investment banking firm? and $ The arbitrage strategy is to buy zeros with face values of $ , and respective maturities of one year and two years. b. What is the profit on the activity? (Do...

The yield to maturity (YTM) on 1-year zero-coupon bonds is 4% and the YTM on 2-year zeros is 5%. The yield to maturity on 2-year-maturity coupon bonds with coupon rates of 9% (paid annually) is 4.5%. a. What arbitrage opportunity is available for an investment banking firm? and $ The arbitrage strategy is to buy zeros with face values of $ , and respective maturities of one year and two years. b. What is the profit on the activity? (Do...

The yield to maturity (YTM) on 1-year zero-coupon bonds is 5% and the YTM on 2-year zeros is 6%. The yield to maturity on 2-year- maturity coupon bonds with coupon rates of 9% (paid annually) is 5.9%. a. What arbitrage opportunity is available for an investment banking firm? The arbitrage strategy is to buy zeros with face values of $ D and $C , and respective maturities of one year and two years. b. What is the profit on the...

The yield to maturity (YTM) on 1-year zero-coupon bonds is 5% and the YTM on 2-year zeros is 6%. The yield to maturity on 2-year- maturity coupon bonds with coupon rates of 9% (paid annually) is 5.9%. a. What arbitrage opportunity is available for an investment banking firm? The arbitrage strategy is to buy zeros with face values of $ D and $C , and respective maturities of one year and two years. b. What is the profit on the...

Problem 15-17 The current yield curve for default-free zero-coupon bonds is as follows: Maturity (Years) YTM (%) 5% 2 a. What are the implied 1-year forward rates? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Answer is complete but not entirely correct. Maturity 2 years Forward Rate 7.00 % 10.00 X % 3 years b. Assume that the pure expectations hypothesis of the term structure is correct. If market expectations are accurate, what will be the...

Problem 15-17 The current yield curve for default-free zero-coupon bonds is as follows: Maturity (Years) YTM (%) 5% 2 a. What are the implied 1-year forward rates? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Answer is complete but not entirely correct. Maturity 2 years Forward Rate 7.00 % 10.00 X % 3 years b. Assume that the pure expectations hypothesis of the term structure is correct. If market expectations are accurate, what will be the...

Consider the following $1,000 par value zero-coupon bonds: Bond Years to Maturity YTM(%) 5.7% 6.7 7.2 7.7 According to the expectations hypothesis, what is the expected 1-year interest rate 3 years from now? (Do not round intermediate calculations. Round your answer to 2 decimal places. Omit the "%" sign in your response.) Interest rate

Consider the following $1,000 par value zero-coupon bonds: Bond Years to Maturity YTM(%) 5.7% 6.7 7.2 7.7 According to the expectations hypothesis, what is the expected 1-year interest rate 3 years from now? (Do not round intermediate calculations. Round your answer to 2 decimal places. Omit the "%" sign in your response.) Interest rate

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

A 33-year maturity bond making annual coupon payments with a coupon rate of 15% has duration of 10.8 years and convexity of 1916 . The bond currently sells at a yield to maturity of 8% Required (a) Find the price of the bond if its yield to maturity falls to 7% or rises to 9%. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) Yield to maturity of 7% Yield to maturity of 9% (b)...

Most questions answered within 3 hours.

-

Write a C – program that calls a user-defined function from

within main() that determines the...

asked 1 minute from now -

For a 2-Level design, with 8 factors, a recommended screening

design model is:

a. Taguchi L12...

asked 39 minutes ago -

1. Define a function in python that returns the sum of the

following 4 lists. Remember...

asked 30 minutes ago -

Elspeth, associate research specialist for a marketing research

firm in a large Midwestern city, had just...

asked 30 minutes ago -

If domestic savings are insufficient to finance domestic private

investment and exports are greater than imports,...

asked 45 minutes ago -

Q.4.

Use the format in Exhibit 9-1 to compute the ending LIFO

inventory and cost of...

asked 51 minutes ago -

Discuss the different receiving and dispatch equipment required

for uploading and loading different types of material...

asked 55 minutes ago -

Which of the following is true for simultaneous testing?

a. Net specificity is greater than the...

asked 59 minutes ago -

Discuss the importance of homologous recombination and

transposition in natural horizontal gene transfer and evolution. Be...

asked 1 hour ago -

Brittle material has the properties Sut = 30 kpsi and Suc = 90

kpsi. Using the...

asked 1 hour ago -

*

write about Plastic recycling statistics ( Plastic recycling rate )

last two years , i...

asked 1 hour ago -

The activation energy for a given reaction is 50.3 kJ/mol. If

the rate constant for the...

asked 1 hour ago