Homework Answers

Add Answer to:

The yield to maturity (YTM) on 1-year zero-coupon bonds is 4% and the YTM on 2-year...

The yield to maturity (YTM) on 1-year zero-coupon bonds is 5% and the YTM on 2-year...

The yield to maturity (YTM) on 1-year zero-coupon bonds is 5% and the YTM on 2-year zeros is 6%. The yield to maturity on 2-year- maturity coupon bonds with coupon rates of 9% (paid annually) is 5.9%. a. What arbitrage opportunity is available for an investment banking firm? The arbitrage strategy is to buy zeros with face values of $ D and $C , and respective maturities of one year and two years. b. What is the profit on the...

The yield to maturity (YTM) on 1-year zero-coupon bonds is 5% and the YTM on 2-year zeros is 6%. The yield to maturity on 2-year- maturity coupon bonds with coupon rates of 9% (paid annually) is 5.9%. a. What arbitrage opportunity is available for an investment banking firm? The arbitrage strategy is to buy zeros with face values of $ D and $C , and respective maturities of one year and two years. b. What is the profit on the...

The yield to maturity (YTM) on 1-year zero-coupon bonds is 5% and the YTM on 2-year...

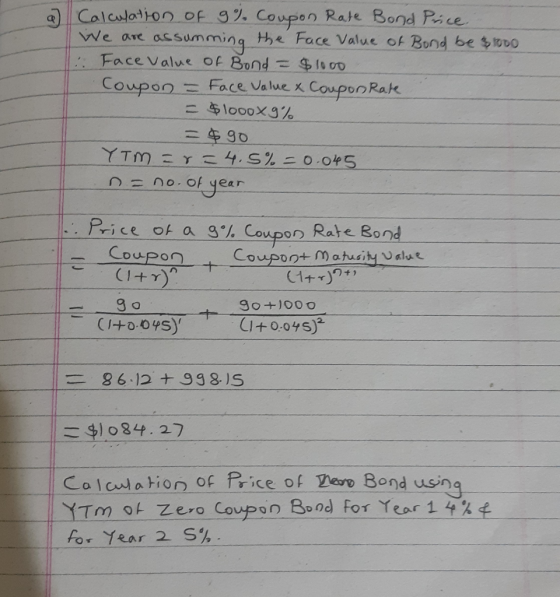

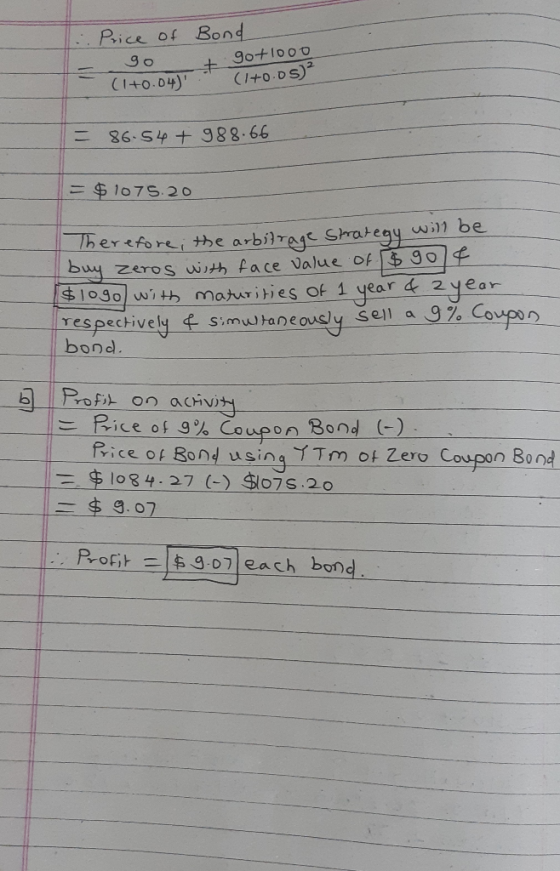

The yield to maturity (YTM) on 1-year zero-coupon bonds is 5% and the YTM on 2-year zeros is 6%. The yield to maturity on 2-year-maturity coupon bonds with coupon rate of 12% (paid annually) is 5.8%. What arbitrage opportunity is available for an investment banking firm? What is the profit on the activity?

The yield to maturity on 1-year zero-coupon bonds is currently 4.5%; the YTM on 2-year zeros...

The yield to maturity on 1-year zero-coupon bonds is currently 4.5%; the YTM on 2-year zeros is 5.5%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 6% The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Price b. What will the yield to maturity on the bond be? (Do...

The yield to maturity on 1-year zero-coupon bonds is currently 4.5%; the YTM on 2-year zeros is 5.5%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 6% The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Price b. What will the yield to maturity on the bond be? (Do...

15.5 The yield to maturity on 1-year zero-coupon bonds is currently 7.5%; the YTM on 2-year...

15.5 The yield to maturity on 1-year zero-coupon bonds is currently 7.5%; the YTM on 2-year zeros is 8.5%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 9.5%. The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places.) b. What will the yield to maturity on the bond be? (Do...

The yield to maturity on 1-year zero-coupon bonds is currently 6.5%; the YTM on 2-year zeros...

The yield to maturity on 1-year zero-coupon bonds is currently 6.5%; the YTM on 2-year zeros is 7.5%. The Government of Canada plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 8.5%. The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places. Omit the "$" sign in your response.) 6.25 points Price $...

The yield to maturity on 1-year zero-coupon bonds is currently 6.5%; the YTM on 2-year zeros is 7.5%. The Government of Canada plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 8.5%. The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places. Omit the "$" sign in your response.) 6.25 points Price $...

Zero-coupon bonds: a. A ten-year, zero coupon bond trades at a Yield-to-Maturity (YTM) of 3.5%. Assume...

Zero-coupon bonds: a. A ten-year, zero coupon bond trades at a Yield-to-Maturity (YTM) of 3.5%. Assume you buy $1000 worth of the bond today. How much will it be worth 10 years from now at maturity? b. A 5-year, zero coupon bond trades at a Yield-to-Maturity (YTM) of 2.5%. Assume you buy $1000 worth of the bond today. How much will it be worth 5 years from now at maturity? C. Assume you invest $1,131.41 today and receive $1,410.60 five...

Zero-coupon bonds: a. A ten-year, zero coupon bond trades at a Yield-to-Maturity (YTM) of 3.5%. Assume you buy $1000 worth of the bond today. How much will it be worth 10 years from now at maturity? b. A 5-year, zero coupon bond trades at a Yield-to-Maturity (YTM) of 2.5%. Assume you buy $1000 worth of the bond today. How much will it be worth 5 years from now at maturity? C. Assume you invest $1,131.41 today and receive $1,410.60 five...

The yield to maturity on 1-year zero-coupon bonds is currently 7%; the YTM on 2-year zeros is 8%. The Government plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupo...

The yield to maturity on 1-year zero-coupon bonds is currently 7%; the YTM on 2-year zeros is 8%. The Government plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 9%. The face value of the bond is $100. a. At what price will the bond sell? b. What will the yield to maturity on the bond be? (Hint: Use a financial calculator to get the YTM) c. If the expectations theory...

Bond prices in the absence of arbitrage Consider a market with two risk-free zero-coupon bonds, A...

Bond prices in the absence of arbitrage Consider a market with two risk-free zero-coupon bonds, A and B. Their respective maturities are 1 and 2 years, and their market prices are 97.0874 and 95.1814 (expressed as percentage of the face value). (a) Calculate the discount rates rt for t = 1 and 2 years. (b) Suppose that a two-year bond C, with a coupon rate of 2.75%, also trades in the market. What should be its price if there is...

The current zero-coupon yield curve for risk-free bonds is as follows: Maturity (years) YTM 4.99% 5.79%...

The current zero-coupon yield curve for risk-free bonds is as follows: Maturity (years) YTM 4.99% 5.79% 5.99% 6.03% What is the price per $100 face value of a four-year, zero-coupon, risk-free bond? The price per $100 face value of the four-year, zero-coupon, risk-free bond is $ . (Round to the nearest cent.) The current zero-coupon yield curve for risk-free bonds is as follows: Maturity (years) YTM - 5.54% 4.99% 5.54% 5.97% 6.06% What is the risk-free interest rate for a...

The current zero-coupon yield curve for risk-free bonds is as follows: Maturity (years) YTM 4.99% 5.79% 5.99% 6.03% What is the price per $100 face value of a four-year, zero-coupon, risk-free bond? The price per $100 face value of the four-year, zero-coupon, risk-free bond is $ . (Round to the nearest cent.) The current zero-coupon yield curve for risk-free bonds is as follows: Maturity (years) YTM - 5.54% 4.99% 5.54% 5.97% 6.06% What is the risk-free interest rate for a...

The current yield curve for default-free zero-coupon bonds is as follows: Maturity (Years) 10 YTM (%)...

The current yield curve for default-free zero-coupon bonds is as follows: Maturity (Years) 10 YTM (%) 10.5% 11.5 12.5 points a. What are the implied 1-year forward rates? (Do not round intermediate calculations. Round your answers to 2 decimal places.) eBook Forward Rate Maturity 2 years 3 years Print References b. Assume that the pure expectations hypothesis of the term structure is correct. If market expectations are accurate, what will be the yield to maturity on 1-year zero-coupon bonds next...

The current yield curve for default-free zero-coupon bonds is as follows: Maturity (Years) 10 YTM (%) 10.5% 11.5 12.5 points a. What are the implied 1-year forward rates? (Do not round intermediate calculations. Round your answers to 2 decimal places.) eBook Forward Rate Maturity 2 years 3 years Print References b. Assume that the pure expectations hypothesis of the term structure is correct. If market expectations are accurate, what will be the yield to maturity on 1-year zero-coupon bonds next...

The yield to maturity (YTM) on 1-year zero-coupon bonds is 5% and the YTM on 2-year zeros is 6%. The yield to maturity on 2-year- maturity coupon bonds with coupon rates of 9% (paid annually) is 5.9%. a. What arbitrage opportunity is available for an investment banking firm? The arbitrage strategy is to buy zeros with face values of $ D and $C , and respective maturities of one year and two years. b. What is the profit on the...

The yield to maturity (YTM) on 1-year zero-coupon bonds is 5% and the YTM on 2-year zeros is 6%. The yield to maturity on 2-year- maturity coupon bonds with coupon rates of 9% (paid annually) is 5.9%. a. What arbitrage opportunity is available for an investment banking firm? The arbitrage strategy is to buy zeros with face values of $ D and $C , and respective maturities of one year and two years. b. What is the profit on the...

The yield to maturity on 1-year zero-coupon bonds is currently 4.5%; the YTM on 2-year zeros is 5.5%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 6% The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Price b. What will the yield to maturity on the bond be? (Do...

The yield to maturity on 1-year zero-coupon bonds is currently 4.5%; the YTM on 2-year zeros is 5.5%. The Treasury plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 6% The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Price b. What will the yield to maturity on the bond be? (Do...

The yield to maturity on 1-year zero-coupon bonds is currently 6.5%; the YTM on 2-year zeros is 7.5%. The Government of Canada plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 8.5%. The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places. Omit the "$" sign in your response.) 6.25 points Price $...

The yield to maturity on 1-year zero-coupon bonds is currently 6.5%; the YTM on 2-year zeros is 7.5%. The Government of Canada plans to issue a 2-year maturity coupon bond, paying coupons once per year with a coupon rate of 8.5%. The face value of the bond is $100. a. At what price will the bond sell? (Do not round intermediate calculations. Round your answer to 2 decimal places. Omit the "$" sign in your response.) 6.25 points Price $...

Zero-coupon bonds: a. A ten-year, zero coupon bond trades at a Yield-to-Maturity (YTM) of 3.5%. Assume you buy $1000 worth of the bond today. How much will it be worth 10 years from now at maturity? b. A 5-year, zero coupon bond trades at a Yield-to-Maturity (YTM) of 2.5%. Assume you buy $1000 worth of the bond today. How much will it be worth 5 years from now at maturity? C. Assume you invest $1,131.41 today and receive $1,410.60 five...

Zero-coupon bonds: a. A ten-year, zero coupon bond trades at a Yield-to-Maturity (YTM) of 3.5%. Assume you buy $1000 worth of the bond today. How much will it be worth 10 years from now at maturity? b. A 5-year, zero coupon bond trades at a Yield-to-Maturity (YTM) of 2.5%. Assume you buy $1000 worth of the bond today. How much will it be worth 5 years from now at maturity? C. Assume you invest $1,131.41 today and receive $1,410.60 five...

The current zero-coupon yield curve for risk-free bonds is as follows: Maturity (years) YTM 4.99% 5.79% 5.99% 6.03% What is the price per $100 face value of a four-year, zero-coupon, risk-free bond? The price per $100 face value of the four-year, zero-coupon, risk-free bond is $ . (Round to the nearest cent.) The current zero-coupon yield curve for risk-free bonds is as follows: Maturity (years) YTM - 5.54% 4.99% 5.54% 5.97% 6.06% What is the risk-free interest rate for a...

The current zero-coupon yield curve for risk-free bonds is as follows: Maturity (years) YTM 4.99% 5.79% 5.99% 6.03% What is the price per $100 face value of a four-year, zero-coupon, risk-free bond? The price per $100 face value of the four-year, zero-coupon, risk-free bond is $ . (Round to the nearest cent.) The current zero-coupon yield curve for risk-free bonds is as follows: Maturity (years) YTM - 5.54% 4.99% 5.54% 5.97% 6.06% What is the risk-free interest rate for a...

The current yield curve for default-free zero-coupon bonds is as follows: Maturity (Years) 10 YTM (%) 10.5% 11.5 12.5 points a. What are the implied 1-year forward rates? (Do not round intermediate calculations. Round your answers to 2 decimal places.) eBook Forward Rate Maturity 2 years 3 years Print References b. Assume that the pure expectations hypothesis of the term structure is correct. If market expectations are accurate, what will be the yield to maturity on 1-year zero-coupon bonds next...

The current yield curve for default-free zero-coupon bonds is as follows: Maturity (Years) 10 YTM (%) 10.5% 11.5 12.5 points a. What are the implied 1-year forward rates? (Do not round intermediate calculations. Round your answers to 2 decimal places.) eBook Forward Rate Maturity 2 years 3 years Print References b. Assume that the pure expectations hypothesis of the term structure is correct. If market expectations are accurate, what will be the yield to maturity on 1-year zero-coupon bonds next...

Most questions answered within 3 hours.

-

The extent to which assets are financed by borrowed funds and

other liabilities is indicated by:...

asked 36 minutes ago -

Explain in detail

Germany is the fifth largest economy

explain what goods and services Germany specializes...

asked 51 minutes ago -

The density of platinum is 21.45 g/mL. If a cube of platinum

with a mass of...

asked 56 minutes ago -

Accounts Receivable

Sales

A/R Posting

Extended Sales Invoice

Packing Slip

Compare invoice to packing slip 2...

asked 59 minutes ago -

Michaella, age 23, is a full-time law student and is claimed by

her parents as a...

asked 1 hour ago -

Why are polymers not typically casted into products?

asked 1 hour ago -

When rolling a die 129 times, what is the probability of rolling

a 6 no more...

asked 1 hour ago -

4. A call option currently sells for $7.75. It has a strike

price of $85 and...

asked 1 hour ago -

1.

You need to prepare 10.0 liters of an acid aqueous solution with a

pH of...

asked 1 hour ago -

Along an aggregate supply curve, if the level of output is less

than the natural level...

asked 1 hour ago -

By 2025, annual consumption in emerging markets will total $30

trillion and contribute more than ________...

asked 1 hour ago -

At what point does reformation cease to be a viable option for

those who are oppressed...

asked 1 hour ago