Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The following transactions took place during the year:

- Raw materials purchased on account, $230,000.

- Raw materials used in production (all direct materials), $215,000.

- Utility bills incurred on account, $65,000 (85% related to factory operations, and the remainder related to selling and administrative activities).

- Accrued salary and wage costs:

| Direct labor (1,135 hours) | $ | 260,000 |

| Indirect labor | $ | 96,000 |

| Selling and administrative salaries | $ |

140,000 |

- Maintenance costs incurred on account in the factory, $60,000

- Advertising costs incurred on account, $142,000.

- Depreciation was recorded for the year, $90,000 (75% related to factory equipment, and the remainder related to selling and administrative equipment).

- Rental cost incurred on account, $115,000 (80% related to factory facilities, and the remainder related to selling and administrative facilities).

- Manufacturing overhead cost was applied to jobs, $ ? .

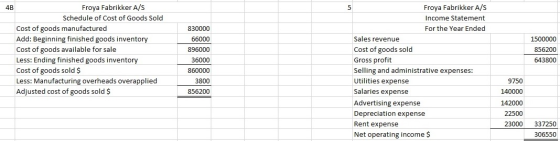

- Cost of goods manufactured for the year, $830,000.

- Sales for the year (all on account) totaled $1,500,000. These goods cost $860,000 according to their job cost sheets.

The balances in the inventory accounts at the beginning of the year were:

| Raw Materials | $ | 36,000 |

| Work in Process | $ | 27,000 |

| Finished Goods | $ | 66,000 |

Required:

1. Prepare journal entries to record the preceding transactions.

2. Post your entries to T-accounts. (Don’t forget to enter the beginning inventory balances above.)

3. Prepare a schedule of cost of goods manufactured.

4A. Prepare a journal entry to close any balance in the Manufacturing Overhead account to Cost of Goods Sold.

4B. Prepare a schedule of cost of goods sold.

5. Prepare an income statement for the year.

Homework Answers

Predetermined overhead rate = $349800/1060 = $330 per direct labor hour

1.

| Transaction | General Journal | Debit | Credit |

| a. | Raw materials | 230000 | |

| Accounts payable | 230000 | ||

| (To record raw materials purchased on account) | |||

| b. | Work in process | 215000 | |

| Raw Materials | 215000 | ||

| (To record direct materials used in production) | |||

| c. | Manufacturing overhead ($65000 x 85%) | 55250 | |

| Utilities expense ($65000 x 15%) | 9750 | ||

| Accounts Payable | 65000 | ||

| (To record utility bills incurred on account) | |||

| d. | Work in process | 260000 | |

| Manufacturing overhead | 96000 | ||

| Salaries expense | 140000 | ||

| Salaries and wages payable | 496000 | ||

| (To record salary and wage costs incurred) | |||

| e. | Manufacturing overhead | 60000 | |

| Accounts payable | 60000 | ||

| (To record maintenance costs incurred on account in factory) | |||

| f. | Advertising expense | 142000 | |

| Accounts payable | 142000 | ||

| (To record advertising costs incurred on account) | |||

| g. | Manufacturing overhead ($90000 x 75%) | 67500 | |

| Depreciation expense ($90000 x 25%) | 22500 | ||

| Accumulated depreciation | 90000 | ||

| (To record depreciation for the year) | |||

| h. | Manufacturing overhead ($115000 x 80%) | 92000 | |

| Rent expense ($115000 x 20%) | 23000 | ||

| Accounts Payable | 115000 | ||

| (To record rental cost incurred on account) | |||

| i. | Work in process (1135 x $330) | 374550 | |

| Manufacturing overhead | 374550 | ||

| (To record manufacturing overhead applied) | |||

| j. | Finished goods | 830000 | |

| Work in process | 830000 | ||

| (To record goods completed and transferred to finished goods) | |||

| k(1) | Accounts receivable | 1500000 | |

| Sales | 1500000 | ||

| (To record sales on account) | |||

| k(2) | Cost of goods sold | 860000 | |

| Finished goods | 860000 | ||

| (To record cost of sales) |

2.

| Finished Goods | Advertising Expense | |||||||

| Beg. Bal. | 66000 | Beg. Bal. | 0 | |||||

| j. | 830000 | 860000 | k(2) | f. | 142000 | |||

| End. Bal. | 142000 | |||||||

| End. Bal. | 36000 | |||||||

| Accumulated Depreciation | Utilities Expense | |||||||

| Beg. Bal. | 0 | Beg. Bal. | 0 | |||||

| 90000 | g. | c. | 9750 | |||||

| End. Bal. | 90000 | End. Bal. | 9750 | |||||

| Accounts Payable | Salaries Expense | |||||||

| Beg. Bal. | 0 | Beg. Bal. | 0 | |||||

| 230000 | a. | d. | 140000 | |||||

| 65000 | c. | |||||||

| 60000 | e. | End. Bal. | 140000 | |||||

| 142000 | f. | |||||||

| 115000 | h. | |||||||

| End. Bal. | 612000 | |||||||

| Depreciation Expense | Salaries and Wages Payable | |||||||

| Beg. Bal. | 0 | Beg. Bal. | 0 | |||||

| g. | 22500 | 496000 | d. | |||||

| End. Bal. | 22500 | End. Bal. | 496000 | |||||

| Rent Expense | ||||||||

| Beg. Bal. | 0 | |||||||

| h. | 23000 | |||||||

| End. Bal. | 23000 | |||||||

Add Answer to:

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $380,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $380,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $395,600 of manufacturing overhead for an

estimated allocation base of 920 direct labor-hours. The following

transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $395,600 of manufacturing overhead for an

estimated allocation base of 920 direct labor-hours. The following

transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $360,000 of manufacturing overhead for an estimated allocation base of 900 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $360,000 of manufacturing overhead for an estimated allocation base of 900 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $380,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $380,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $374,000 of manufacturing overhead for an estimated allocation base of 1,100 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $374,000 of manufacturing overhead for an estimated allocation base of 1,100 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Eroya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Eroya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $360,000 of manufacturing overhead for an estimated allocation base of 900 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased on...

Eroya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $360,000 of manufacturing overhead for an estimated allocation base of 900 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased on...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea fields.

The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct labo

hoursIts predetermined overhead rate was based on a cost formula

that estimated $372,000 of manufacturing overhead for an estimated

allocation base of 1.200 direct laborhours. The following

transactions took place during the year

Froya Fabrikker A/S of Bergen, Norway,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea fields.

The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct labo

hoursIts predetermined overhead rate was based on a cost formula

that estimated $372,000 of manufacturing overhead for an estimated

allocation base of 1.200 direct laborhours. The following

transactions took place during the year

Froya Fabrikker A/S of Bergen, Norway,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system and applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year (all purchases and services were...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system and applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year (all purchases and services were...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $380,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $380,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $395,600 of manufacturing overhead for an

estimated allocation base of 920 direct labor-hours. The following

transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $395,600 of manufacturing overhead for an

estimated allocation base of 920 direct labor-hours. The following

transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $360,000 of manufacturing overhead for an estimated allocation base of 900 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $360,000 of manufacturing overhead for an estimated allocation base of 900 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $380,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $380,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $374,000 of manufacturing overhead for an estimated allocation base of 1,100 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $374,000 of manufacturing overhead for an estimated allocation base of 1,100 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased...

Eroya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $360,000 of manufacturing overhead for an estimated allocation base of 900 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased on...

Eroya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $360,000 of manufacturing overhead for an estimated allocation base of 900 direct labor-hours. The following transactions took place during the year: a. Raw materials purchased on...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea fields.

The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct labo

hoursIts predetermined overhead rate was based on a cost formula

that estimated $372,000 of manufacturing overhead for an estimated

allocation base of 1.200 direct laborhours. The following

transactions took place during the year

Froya Fabrikker A/S of Bergen, Norway,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea fields.

The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct labo

hoursIts predetermined overhead rate was based on a cost formula

that estimated $372,000 of manufacturing overhead for an estimated

allocation base of 1.200 direct laborhours. The following

transactions took place during the year

Froya Fabrikker A/S of Bergen, Norway,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system and applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year (all purchases and services were...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system and applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year (all purchases and services were...

Most questions answered within 3 hours.

-

A combustion reaction is describes as a carbon source reacting

with oxygen and producing carbon dioxide...

asked 4 minutes ago -

Buckminsterfullerence is a recently allotrope of carbon in which

carbon atoms form molecules of formula C_60,...

asked 7 minutes ago -

Lower Equitorial and Upper Equitorial are the same except Lower

Equitorial has a larger capital stock....

asked 12 minutes ago -

how do you think that pH of a jar where you have added a certain

amount...

asked 22 minutes ago -

If the Federal Reserve increases the reserve requirement, what

will happen to the Money Supply in...

asked 16 minutes ago -

Suppose that market demand for a good is given by Q = 9 - 0.3 P...

asked 23 minutes ago -

two thin lenses are separated by a distance x. The first lens

has a focal length...

asked 24 minutes ago -

The computer that controls a bank's automatic teller machine

crashes a mean of 0.6 times per...

asked 28 minutes ago -

`1) How is -9 (base 10) represented in 8-bit two's complement

notation?

a) 00001001

b)11110111

c)11110110...

asked 38 minutes ago -

A 10.000 g sample of water contains 11.19% H by mass. what

should be the %H...

asked 55 minutes ago -

Consider an investment game among 2 players. Each player can

either invest,

i, or not invest,-i....

asked 53 minutes ago -

The time taken to complete a particular task is normally

distributed with a standard deviation of...

asked 1 hour ago