Stocks A and B each have an expected return of 15%, a standard deviation of 20%,...

Stocks A and B each have an expected return of 15%, a standard deviation of 20%, and a beta of 1.2. The returns on the two stocks have a correlation coefficient of -1.0. You have a portfolio that consists of 50% A and 50% B. Which of the following statements is CORRECT?

|

The portfolio's standard deviation is zero (i.e., a riskless portfolio). |

||

|

The portfolio's beta is greater than 1.2. |

||

|

The portfolio's standard deviation is greater than 20%. |

||

|

The portfolio's expected return is less than 15%. |

||

|

The portfolio's beta is less than 1.2. |

Homework Answers

ANSWER :

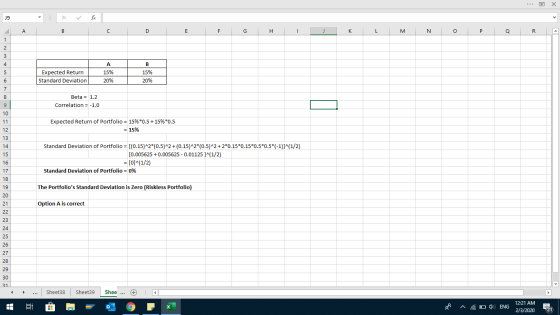

Beta of portfolio = WA bA+ WB bB = 0.5*1.2 + 0.5*1.2 = 1.2 .

So, option 2 and 5 are ruled out.

Expected return of portfolio = WA rA + WB rB = 0.5*15 + 0.5*15 = 15% .

So, option 4 is ruled out.

SD of portfolio = sqrt ((WA sA)^2 + (WB sB)^2 + 2WA WB sA sB r)

= sqrt((0.5*0.2)^2 + (0.5*0.2)^2 + 2*0.5*0.5*0.2*0.2*(-1.0))

= 0

So, option 1 is correct and option 3 is ruled out.

Therefore, the option 1 : The portfolio’s SD is zero (risk-less) is CORRECT.

(ANSWER

Add Answer to:

Stocks A and B each have an expected return of 15%, a standard

deviation of 20%,...

Stocks A and B each have an expected return of 15%, a standard deviation of 17%,...

Stocks A and B each have an expected return of 15%, a standard deviation of 17%, and a beta of 1.2. The returns on the two stocks have a correlation coefficient of <1.0. You have a portfolio that consists A) The portfolio's beta is less than 12. B) The portfolio's standard deviation is greater than 17%. C) The portfolio's standard deviation is less than 17%. D) The portfolio's expected return is 15%.

Stocks A and B each have an expected return of 15%, a standard deviation of 17%, and a beta of 1.2. The returns on the two stocks have a correlation coefficient of <1.0. You have a portfolio that consists A) The portfolio's beta is less than 12. B) The portfolio's standard deviation is greater than 17%. C) The portfolio's standard deviation is less than 17%. D) The portfolio's expected return is 15%.

Stocks A and B each have an expected return of 12%, a beta of 1.2, and...

Stocks A and B each have an expected return of 12%, a beta of 1.2, and a standard deviation of 25%. The returns on the two stocks have a correlation of 0.6. Portfolio P has 50% in Stock A and 50% in Stock B. Which of the following statements is CORRECT? Portfolio P has a beta that is greater than 1.2. Portfolio P has a standard deviation that is greater than 25%. Portfolio P has an expected return that is...

Stock A has an expected return of 11 percent, a beta of 0.9, and a standard deviation of 15 perce...

Stock A has an expected return of 11 percent, a beta of 0.9, and a standard deviation of 15 percent Stock B also has a beta of 0.9, but its expected returm is 9 percent and its standard deviation is 13 percent. Portfolio AB has $900,000 invested in Stock A and $300,000 invested in Stock B. The correlation between the two stocks' returns is zero. Which of the following statements is CORRECT? Select one O a.I am not sure b....

Stock A has an expected return of 11 percent, a beta of 0.9, and a standard deviation of 15 percent Stock B also has a beta of 0.9, but its expected returm is 9 percent and its standard deviation is 13 percent. Portfolio AB has $900,000 invested in Stock A and $300,000 invested in Stock B. The correlation between the two stocks' returns is zero. Which of the following statements is CORRECT? Select one O a.I am not sure b....

stocks c and m each have an expected return of 9%, a beta of .90, and...

stocks c and m each have an expected return of 9%, a beta of .90, and standard deviation of 30%. the returns on the two stocks have a correlation of .50. portfolio p has 60% in stock c and 40% in m. which is true? a) p standard dev less than 30% b) p standard dev equal to 30% c) p beta is less than .90 d) p beta is greater than .90 e) p expected return greater than 9%

Midas is considering two stocks. The expected return on LAN is 15% with a standard deviation...

Midas is considering two stocks. The expected return on LAN is 15% with a standard deviation of 32%. The expected return on GBT is 9% with a standard deviation of 23%. The correlation between the returns on LAN and GBT is 0.15. The betas of LAN and GBT are 1.2 and 0.8 respectively. a. Assume that Midas would like to have a portfolio with a beta of 0.9. Recommend how he can invest in two stocks to achieve his objective....

You have a portfolio with a standard deviation of 20% and an expected return of 20%....

You have a portfolio with a standard deviation of 20% and an expected return of 20%. You are considering adding one of the two stocks in the following table. If after adding the stock you will have 20% of your money in the new stock and 80% of your money in your existing portfolio, which one should you add? Expected Return Standard Deviation Correlation with Your Portfolio's Returns Stock A 15% 22% 0.4 Stock B 15% 18% 0.6 Standard deviation...

QUESTION 54 Your portfolio consists of $50,000 invested in Stock X and $50,000 invested in Stock ...

please assist with excel function or calculator

QUESTION 54 Your portfolio consists of $50,000 invested in Stock X and $50,000 invested in Stock Y. Both stocks have return of 15%, betas of 1.6, and standard deviations of 30%-The returns ofthe two stocks are independent correlation coefficient between them, xy, is zero. Which of the following statements best describes the cl your 2-stock portfolio? Your portfolio has a beta greater than 1.6, and its expected return is greater than 15% Your...

please assist with excel function or calculator

QUESTION 54 Your portfolio consists of $50,000 invested in Stock X and $50,000 invested in Stock Y. Both stocks have return of 15%, betas of 1.6, and standard deviations of 30%-The returns ofthe two stocks are independent correlation coefficient between them, xy, is zero. Which of the following statements best describes the cl your 2-stock portfolio? Your portfolio has a beta greater than 1.6, and its expected return is greater than 15% Your...

You have a portfolio with a standard deviation of 26% and an expected return of 20%....

You have a portfolio with a standard deviation of 26% and an expected return of 20%. You are considering adding one of the two stocks in the following table. If after adding the stock you will have 30% of your money in the new stock and 70% of your money in your existing portfolio, which one should you add? Expected Return 12% 12% Standard Deviation 24% 19% Correlation with Your Portfolio's Returns 0.4 0.6 Stock A Stock B Standard deviation...

You have a portfolio with a standard deviation of 26% and an expected return of 20%. You are considering adding one of the two stocks in the following table. If after adding the stock you will have 30% of your money in the new stock and 70% of your money in your existing portfolio, which one should you add? Expected Return 12% 12% Standard Deviation 24% 19% Correlation with Your Portfolio's Returns 0.4 0.6 Stock A Stock B Standard deviation...

You have a portfolio with a standard deviation of 30 % and .an expected return of...

You have a portfolio with a standard deviation of 30 % and .an expected return of 15 %. You are considering adding one of the two stocks in the following table. If after adding the stock you will have 30 % of your money in the new stock and 70 % of your money in your existing portfolio, which one should you add? Expected Return: (ER) Standard Deviation:(STNDDEV) Correlation with Your Portfolio's Returns(Corr) Stock A (ER) 15% (STNDDEV)25% (Corr)0.3 Stock...

6. Calculating a beta coefficient for a single stock Suppose that the standard deviation of returns...

6. Calculating a beta coefficient for a single stock Suppose that the standard deviation of returns for a single stock A IS A = 25%, and the standard deviation of the market return is on = 15%. If the correlation between stock A and the market is PAM - 0.6, then the stock's beta is prns against the market returns will equal the true value of Is it reasonable to expect that the beta value estimated via the regression of...

6. Calculating a beta coefficient for a single stock Suppose that the standard deviation of returns for a single stock A IS A = 25%, and the standard deviation of the market return is on = 15%. If the correlation between stock A and the market is PAM - 0.6, then the stock's beta is prns against the market returns will equal the true value of Is it reasonable to expect that the beta value estimated via the regression of...

Stocks A and B each have an expected return of 15%, a standard deviation of 17%, and a beta of 1.2. The returns on the two stocks have a correlation coefficient of <1.0. You have a portfolio that consists A) The portfolio's beta is less than 12. B) The portfolio's standard deviation is greater than 17%. C) The portfolio's standard deviation is less than 17%. D) The portfolio's expected return is 15%.

Stocks A and B each have an expected return of 15%, a standard deviation of 17%, and a beta of 1.2. The returns on the two stocks have a correlation coefficient of <1.0. You have a portfolio that consists A) The portfolio's beta is less than 12. B) The portfolio's standard deviation is greater than 17%. C) The portfolio's standard deviation is less than 17%. D) The portfolio's expected return is 15%.

Stock A has an expected return of 11 percent, a beta of 0.9, and a standard deviation of 15 percent Stock B also has a beta of 0.9, but its expected returm is 9 percent and its standard deviation is 13 percent. Portfolio AB has $900,000 invested in Stock A and $300,000 invested in Stock B. The correlation between the two stocks' returns is zero. Which of the following statements is CORRECT? Select one O a.I am not sure b....

Stock A has an expected return of 11 percent, a beta of 0.9, and a standard deviation of 15 percent Stock B also has a beta of 0.9, but its expected returm is 9 percent and its standard deviation is 13 percent. Portfolio AB has $900,000 invested in Stock A and $300,000 invested in Stock B. The correlation between the two stocks' returns is zero. Which of the following statements is CORRECT? Select one O a.I am not sure b....

please assist with excel function or calculator

QUESTION 54 Your portfolio consists of $50,000 invested in Stock X and $50,000 invested in Stock Y. Both stocks have return of 15%, betas of 1.6, and standard deviations of 30%-The returns ofthe two stocks are independent correlation coefficient between them, xy, is zero. Which of the following statements best describes the cl your 2-stock portfolio? Your portfolio has a beta greater than 1.6, and its expected return is greater than 15% Your...

please assist with excel function or calculator

QUESTION 54 Your portfolio consists of $50,000 invested in Stock X and $50,000 invested in Stock Y. Both stocks have return of 15%, betas of 1.6, and standard deviations of 30%-The returns ofthe two stocks are independent correlation coefficient between them, xy, is zero. Which of the following statements best describes the cl your 2-stock portfolio? Your portfolio has a beta greater than 1.6, and its expected return is greater than 15% Your...

You have a portfolio with a standard deviation of 26% and an expected return of 20%. You are considering adding one of the two stocks in the following table. If after adding the stock you will have 30% of your money in the new stock and 70% of your money in your existing portfolio, which one should you add? Expected Return 12% 12% Standard Deviation 24% 19% Correlation with Your Portfolio's Returns 0.4 0.6 Stock A Stock B Standard deviation...

You have a portfolio with a standard deviation of 26% and an expected return of 20%. You are considering adding one of the two stocks in the following table. If after adding the stock you will have 30% of your money in the new stock and 70% of your money in your existing portfolio, which one should you add? Expected Return 12% 12% Standard Deviation 24% 19% Correlation with Your Portfolio's Returns 0.4 0.6 Stock A Stock B Standard deviation...

6. Calculating a beta coefficient for a single stock Suppose that the standard deviation of returns for a single stock A IS A = 25%, and the standard deviation of the market return is on = 15%. If the correlation between stock A and the market is PAM - 0.6, then the stock's beta is prns against the market returns will equal the true value of Is it reasonable to expect that the beta value estimated via the regression of...

6. Calculating a beta coefficient for a single stock Suppose that the standard deviation of returns for a single stock A IS A = 25%, and the standard deviation of the market return is on = 15%. If the correlation between stock A and the market is PAM - 0.6, then the stock's beta is prns against the market returns will equal the true value of Is it reasonable to expect that the beta value estimated via the regression of...

Most questions answered within 3 hours.

-

There are four steps to algorithm methodology.

1. Design: Identify the problem and thoroughly

understand it....

asked 2 minutes ago -

It is known that The New York Times’ circulation is 731,500

print copies. You publish three...

asked 34 seconds ago -

Sales Order Processing

Vidar Foodservice’s salespeople telephone and bring handwritten

orders to the office, which prepares...

asked 15 minutes ago -

Consider a project to supply Detroit with 26,000 tons of machine

screws annually for automobile production....

asked 16 minutes ago -

3. An investor is concerned with the market return for the

coming year, where the market...

asked 22 minutes ago -

Random variable X corresponds to the daily number of accidents

in a small town during the...

asked 28 minutes ago -

What role did settlement houses play in the lives of women and

ethnic immigrants?

asked 24 minutes ago -

1. Assume that you are given values in eax, ebx, ecx.

Write an assembly code that...

asked 30 minutes ago -

A

researcher wishes to estimate with 99% confidence, the population

proportion of adults who eat fast...

asked 1 hour ago -

What are the differences between an ANOVA and a MANOVA? Which

would be simpler to use...

asked 1 hour ago -

Thank you in advance for the help on this question. There are 3

parts, a, b...

asked 1 hour ago -

In your own words, define M-Commerce. How does it effect

E-Commerce? What is your experience with...

asked 1 hour ago