Ryan anticipated a price decline in the price of Target in the next three years. He...

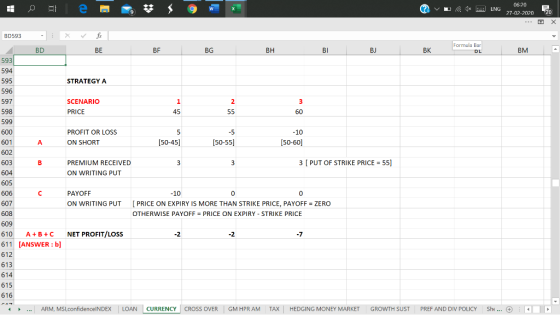

Ryan anticipated a price decline in the price of Target in the next three years. He has just shorted 100 shares of target common stock at $50 per share. To protect against losses, Ryan considers the following two investment strategies.

a. Strategy A is to write a TGT May 55 put with a premium equal to $3.

b. Strategy B is to buy a TGT May 55 call with a premium equal to $3

Evaluate each of the above two strategies under the three scenarios (1) future stock price is $45 (2) future stock price is $55 (3) future stock price is $60.

10. What would be Ryan’s profit from strategy A under the three scenarios?

- -$3, $3, $10

- -$2, -$2, -$7

- $3, -$2, -$5

- $2; -$8, -$8

11. What would be Ryan’s profit from strategy B under the three scenarios?

- -$3, $3, $10

- -$2, -$2, -$7

- $3, -$2, -$5

- $2; -$8, -$8

Homework Answers

SEE THE IMAGE. ANY DOUBTS, FEEL FREE TO ASK. THUMBS UP

PLEASE

Add Answer to:

Ryan anticipated a price decline in the price of Target in the

next three years. He...

The current price of a stock is $72. Three-month call options with a strike price of...

The current price of a stock is $72. Three-month call options with a strike price of $75 currently sell for $10. An investor with $9,000 to invest is considering the following three investment strategies: (a) Investing all his money in the stock (b) Doubling the amount to invest by taking a loan of $9,000 at an interest rate of 2% for three months, investing the resulting $18,000 in the stock and then repaying $9,180 on the loan (c) Investing all...

Problem 1.2. The current price of a stock is $72. Three-month call options with a strike...

Problem 1.2. The current price of a stock is $72. Three-month call options with a strike price of $75 currently sell for $10. An investor with $9,000 to invest is considering the following three investment strategies: (a) Investing all his money in the stock (6) Doubling the amount to invest by taking a loan of $9,000 at an interest rate of 2% for three months, investing the resulting $18,000 in the stock and then repaying $9,180 on the loan (c)...

Problem 1.2. The current price of a stock is $72. Three-month call options with a strike price of $75 currently sell for $10. An investor with $9,000 to invest is considering the following three investment strategies: (a) Investing all his money in the stock (6) Doubling the amount to invest by taking a loan of $9,000 at an interest rate of 2% for three months, investing the resulting $18,000 in the stock and then repaying $9,180 on the loan (c)...

2) A put option is priced at $4 with an exercise price of $60 and an...

2) A put option is priced at $4 with an exercise price of $60 and an underlying price of $62. Determine the following: o Option value for a long position if the stock price at expiry is $62 Profit for the long position if the stock price at expiry is $55 • What is the breakeven stock price at expiration (price at which the option cost is covered for the long position) 3) The share price of Win Big Inc....

2) A put option is priced at $4 with an exercise price of $60 and an underlying price of $62. Determine the following: o Option value for a long position if the stock price at expiry is $62 Profit for the long position if the stock price at expiry is $55 • What is the breakeven stock price at expiration (price at which the option cost is covered for the long position) 3) The share price of Win Big Inc....

1) A call option is priced at $7 with an exercise price of $100 and an...

1) A call option is priced at $7 with an exercise price of $100 and an underlying stock price of $98. If the stock price at expiry is $102 determine the following: o Option value for a long position o Profit for a long position 2) A put option is priced at $4 with an exercise price of $60 and an underlying price of $62. Determine the following: o Option value for a long position if the stock price at...

1) A call option is priced at $7 with an exercise price of $100 and an underlying stock price of $98. If the stock price at expiry is $102 determine the following: o Option value for a long position o Profit for a long position 2) A put option is priced at $4 with an exercise price of $60 and an underlying price of $62. Determine the following: o Option value for a long position if the stock price at...

Question 8 is worth 2 marks Ms. Taylor had taken a short position in 1,000 shares...

Question 8 is worth 2 marks Ms. Taylor had taken a short position in 1,000 shares of the common stock of Toronto Packaging Ltd. at the price of S40 per share in the past. Today the price per share is $30 which provides her gains in her short position. She is concerned that the price of the stock may go higher in the future, which will adversely affect her capital gains in the short position. Suppose she buys today 10...

Question 8 is worth 2 marks Ms. Taylor had taken a short position in 1,000 shares of the common stock of Toronto Packaging Ltd. at the price of S40 per share in the past. Today the price per share is $30 which provides her gains in her short position. She is concerned that the price of the stock may go higher in the future, which will adversely affect her capital gains in the short position. Suppose she buys today 10...

The common stock of the P.U.T.T. Corporation has been trading in a narrow price range for...

The common stock of the P.U.T.T. Corporation has been trading in a narrow price range for the past month, and you are convinced it is going to break far out of that range in the next three months. You do not know whether it will go up or down, however. The current price of the stock is $100 per share, and the price of a 3-month call option at an exercise price of $100 is $10. a. If the risk-free...

1. Consider a call option selling for $ 4 in which the exercise price is $50....

1. Consider a call option selling for $ 4 in which the exercise price is $50. A) Determine the value at expiration and the profit for a buyer under the following outcomes: i. The price of the underlying at expiration is $55 ii. The price of the underlying at expiration is $51 iii. The price of the underlying at expiration is $48 B) Determine the value at expiration and the profit for a seller under the following outcomes: i. The...

questions 14-17. (that is comparing expected price of the bond 6months in the future, 1 yr in the future, 1.5 yrs in the futur so on, till maturity 10203 D) 1056.4 as one moves ahead in time and y...

questions 14-17.

(that is comparing expected price of the bond 6months in the future, 1 yr in the future, 1.5 yrs in the futur so on, till maturity 10203 D) 1056.4 as one moves ahead in time and year. The bond has 3 yeals Io 10096 81045 21. h. Question the "expected price of the bondin the future" 2 A stock price is currently $40. Supposeit is known that at the end of the month, it will be either $42...

questions 14-17.

(that is comparing expected price of the bond 6months in the future, 1 yr in the future, 1.5 yrs in the futur so on, till maturity 10203 D) 1056.4 as one moves ahead in time and year. The bond has 3 yeals Io 10096 81045 21. h. Question the "expected price of the bondin the future" 2 A stock price is currently $40. Supposeit is known that at the end of the month, it will be either $42...

Consider the three stocks (Stock X, Stock Y and Stock Z) that have the following factor loadings (or factor betas)....

Consider the three stocks (Stock X, Stock Y and Stock Z) that have the following factor loadings (or factor betas). The zero-beta return (A): 3%, and the risk premium are:A : 10%入: 8%. Assume that all three stocks are currently priced at $50 Factor 2 Loading StockFactor 1 Loading 1.2 0.55 0.85 0.1 0.5 0.35 All rights reserved. 8 Calculation Problenm What are the expected returns for stock X, stock Y, and stock Zz 1. 2. What are the expected...

Consider the three stocks (Stock X, Stock Y and Stock Z) that have the following factor loadings (or factor betas). The zero-beta return (A): 3%, and the risk premium are:A : 10%入: 8%. Assume that all three stocks are currently priced at $50 Factor 2 Loading StockFactor 1 Loading 1.2 0.55 0.85 0.1 0.5 0.35 All rights reserved. 8 Calculation Problenm What are the expected returns for stock X, stock Y, and stock Zz 1. 2. What are the expected...

Question 17 ou a) A stock price is currently $60. Over each ofthe next two three-month...

Question 17 ou a) A stock price is currently $60. Over each ofthe next two three-month periods it is expected to go up by 8% or down by 7%. The risk-free interest rate is 10% per annum with continuous compounding. What is the value of a six-month European call option with a strike price of $61? (3 marks) b) Based on the information in part (a), what is the value of a six-month European put option with a strike price...

Question 17 ou a) A stock price is currently $60. Over each ofthe next two three-month periods it is expected to go up by 8% or down by 7%. The risk-free interest rate is 10% per annum with continuous compounding. What is the value of a six-month European call option with a strike price of $61? (3 marks) b) Based on the information in part (a), what is the value of a six-month European put option with a strike price...

Problem 1.2. The current price of a stock is $72. Three-month call options with a strike price of $75 currently sell for $10. An investor with $9,000 to invest is considering the following three investment strategies: (a) Investing all his money in the stock (6) Doubling the amount to invest by taking a loan of $9,000 at an interest rate of 2% for three months, investing the resulting $18,000 in the stock and then repaying $9,180 on the loan (c)...

Problem 1.2. The current price of a stock is $72. Three-month call options with a strike price of $75 currently sell for $10. An investor with $9,000 to invest is considering the following three investment strategies: (a) Investing all his money in the stock (6) Doubling the amount to invest by taking a loan of $9,000 at an interest rate of 2% for three months, investing the resulting $18,000 in the stock and then repaying $9,180 on the loan (c)...

2) A put option is priced at $4 with an exercise price of $60 and an underlying price of $62. Determine the following: o Option value for a long position if the stock price at expiry is $62 Profit for the long position if the stock price at expiry is $55 • What is the breakeven stock price at expiration (price at which the option cost is covered for the long position) 3) The share price of Win Big Inc....

2) A put option is priced at $4 with an exercise price of $60 and an underlying price of $62. Determine the following: o Option value for a long position if the stock price at expiry is $62 Profit for the long position if the stock price at expiry is $55 • What is the breakeven stock price at expiration (price at which the option cost is covered for the long position) 3) The share price of Win Big Inc....

1) A call option is priced at $7 with an exercise price of $100 and an underlying stock price of $98. If the stock price at expiry is $102 determine the following: o Option value for a long position o Profit for a long position 2) A put option is priced at $4 with an exercise price of $60 and an underlying price of $62. Determine the following: o Option value for a long position if the stock price at...

1) A call option is priced at $7 with an exercise price of $100 and an underlying stock price of $98. If the stock price at expiry is $102 determine the following: o Option value for a long position o Profit for a long position 2) A put option is priced at $4 with an exercise price of $60 and an underlying price of $62. Determine the following: o Option value for a long position if the stock price at...

Question 8 is worth 2 marks Ms. Taylor had taken a short position in 1,000 shares of the common stock of Toronto Packaging Ltd. at the price of S40 per share in the past. Today the price per share is $30 which provides her gains in her short position. She is concerned that the price of the stock may go higher in the future, which will adversely affect her capital gains in the short position. Suppose she buys today 10...

Question 8 is worth 2 marks Ms. Taylor had taken a short position in 1,000 shares of the common stock of Toronto Packaging Ltd. at the price of S40 per share in the past. Today the price per share is $30 which provides her gains in her short position. She is concerned that the price of the stock may go higher in the future, which will adversely affect her capital gains in the short position. Suppose she buys today 10...

questions 14-17.

(that is comparing expected price of the bond 6months in the future, 1 yr in the future, 1.5 yrs in the futur so on, till maturity 10203 D) 1056.4 as one moves ahead in time and year. The bond has 3 yeals Io 10096 81045 21. h. Question the "expected price of the bondin the future" 2 A stock price is currently $40. Supposeit is known that at the end of the month, it will be either $42...

questions 14-17.

(that is comparing expected price of the bond 6months in the future, 1 yr in the future, 1.5 yrs in the futur so on, till maturity 10203 D) 1056.4 as one moves ahead in time and year. The bond has 3 yeals Io 10096 81045 21. h. Question the "expected price of the bondin the future" 2 A stock price is currently $40. Supposeit is known that at the end of the month, it will be either $42...

Consider the three stocks (Stock X, Stock Y and Stock Z) that have the following factor loadings (or factor betas). The zero-beta return (A): 3%, and the risk premium are:A : 10%入: 8%. Assume that all three stocks are currently priced at $50 Factor 2 Loading StockFactor 1 Loading 1.2 0.55 0.85 0.1 0.5 0.35 All rights reserved. 8 Calculation Problenm What are the expected returns for stock X, stock Y, and stock Zz 1. 2. What are the expected...

Consider the three stocks (Stock X, Stock Y and Stock Z) that have the following factor loadings (or factor betas). The zero-beta return (A): 3%, and the risk premium are:A : 10%入: 8%. Assume that all three stocks are currently priced at $50 Factor 2 Loading StockFactor 1 Loading 1.2 0.55 0.85 0.1 0.5 0.35 All rights reserved. 8 Calculation Problenm What are the expected returns for stock X, stock Y, and stock Zz 1. 2. What are the expected...

Question 17 ou a) A stock price is currently $60. Over each ofthe next two three-month periods it is expected to go up by 8% or down by 7%. The risk-free interest rate is 10% per annum with continuous compounding. What is the value of a six-month European call option with a strike price of $61? (3 marks) b) Based on the information in part (a), what is the value of a six-month European put option with a strike price...

Question 17 ou a) A stock price is currently $60. Over each ofthe next two three-month periods it is expected to go up by 8% or down by 7%. The risk-free interest rate is 10% per annum with continuous compounding. What is the value of a six-month European call option with a strike price of $61? (3 marks) b) Based on the information in part (a), what is the value of a six-month European put option with a strike price...

Most questions answered within 3 hours.

-

Suppose, for any future year, the probability its October rain

is more than 3 inches is...

asked 43 seconds ago -

Solve the following systems of linear equations using

substitution 12p + 3q = 15 6q +...

asked 7 minutes ago -

Prof. D went grocery shopping and purchased one dozen eggs and

one pound of flour (all...

asked 15 minutes ago -

If

somehow loop of Henle were removed - that is if the proximal tubule

was connected...

asked 15 minutes ago -

Add 1ml of 0.18M of HCl (aq) to 1ml of 0.2M of [Ag(NH3)2]Br

(aq).

Write the...

asked 22 minutes ago -

1. Smoke detectors use Am-241, an alpha emitter, to detect smoke

particles. A parent is concerned...

asked 26 minutes ago -

Scenario: Web application developed to capture customers

demographic and financial information for filling their taxes. This...

asked 30 minutes ago -

Which of the following statements are true?

1. Glass is mostly silicon dioxide and so when...

asked 52 minutes ago -

Korman Company has the following securities in its portfolio of

equity securities on December 31, 2018:...

asked 53 minutes ago -

Using the 12th edition of Language Awareness,

complete the following assignment:

After reading Akiba Solomon's "Thugs....

asked 1 hour ago -

For all problems assume an effective monthly interest rate of 1%

unless otherwise indicated in the...

asked 1 hour ago -

Fix all syntax and logical errors for the following program.

Please generate the correct output. //...

asked 1 hour ago