Homework Answers

Add Answer to:

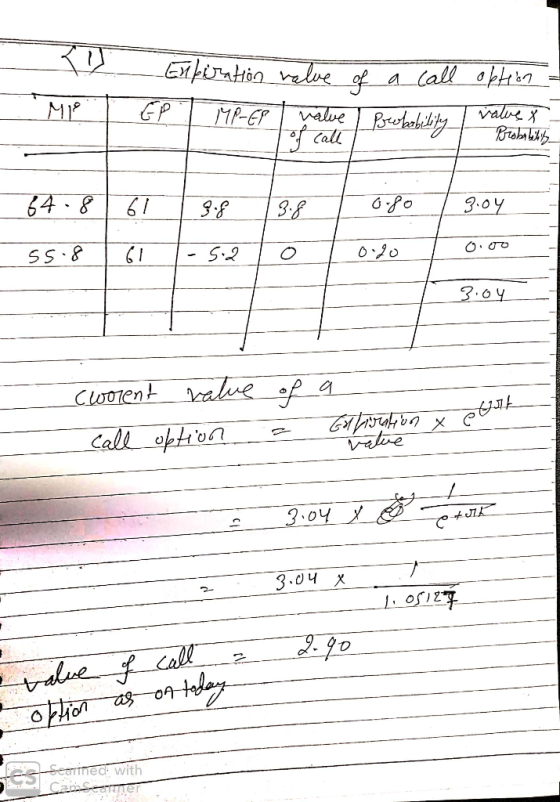

Question 17 ou a) A stock price is currently $60. Over each ofthe next two three-month...

1. A stock price is currently $100. Over each of the next two six-month periods it...

1. A stock price is currently $100. Over each of the next two six-month periods it is expected to go up by 10% or down by 10%. The risk-free rate is 8% per annum with continuous compounding. (a) What is the value of a one-year European call option with a strike price of $100? (b) What is the value of a one year European put option with a strike price of $100? (c) What is the value of a one-year...

A non-paying dividend stock price is currently 40 US$. Over each of the next two three-month...

A non-paying dividend stock price is currently 40 US$. Over each of the next two three-month periods it is expected to go either up by 10% or down by 10%. The riskless interest rate is 12% per annum with continuous compounding. What is the value of a six-month European put option with a strike price of 42 US$? Given the information above find the relevant call and put price of that European non-paying dividend stock option using the Black-Scholes formula

A stock price is currently $50. Over each of the next two three-month periods it is...

A stock price is currently $50. Over each of the next two three-month periods it is expected to go up by 5% or down by 5%. The risk-free interest rate is 10% per annum with continuous compounding. What is the value of a six-month American put option with a strike price of $54? quations you may find helpful: required precision O.01+- 0.01)

A stock price is currently $50. Over each of the next two three-month periods it is expected to go up by 5% or down by 5%. The risk-free interest rate is 10% per annum with continuous compounding. What is the value of a six-month American put option with a strike price of $54? quations you may find helpful: required precision O.01+- 0.01)

A stock price is currently $100. Over each of the next two 6-month periods it is...

A stock price is currently $100. Over each of the next two 6-month periods it is expected to go up by 10% or down by 10%. The risk-free interest rate is 8% per annum with continuous compounding. What is the value of a 1-year European call option with a strike price of $100?

3. A stock price is currently $30. Over each of the next two three-month periods it...

3. A stock price is currently $30. Over each of the next two three-month periods it is expected to go up by 20% or down by 20%. The risk-free interest rate is 4% per annum. What is the value of a six-month American put option with a strike price of $32? (15 marks)

3. A stock price is currently $30. Over each of the next two three-month periods it is expected to go up by 20% or down by 20%. The risk-free interest rate is 4% per annum. What is the value of a six-month American put option with a strike price of $32? (15 marks)

Question 1 a. A stock price is currently $30. It is known that at the end...

Question 1 a. A stock price is currently $30. It is known that at the end of two months it will be either $33 or $27. The risk-free interest rate is 10% per annum with continuous compounding. What is the value of a two-month European put option with a strike price of $31? b. What is meant by the delta of a stock option? A stock price is currently $100. Over each of the next two three-month periods it is...

Question 1 a. A stock price is currently $30. It is known that at the end of two months it will be either $33 or $27. The risk-free interest rate is 10% per annum with continuous compounding. What is the value of a two-month European put option with a strike price of $31? b. What is meant by the delta of a stock option? A stock price is currently $100. Over each of the next two three-month periods it is...

price of a non-dividend-paying stock is currently $40. periods it will go up by 5% or down with continuous com- 1. (30 points) The Over each of the next two four-month by 3%: The risk free inter...

price of a non-dividend-paying stock is currently $40. periods it will go up by 5% or down with continuous com- 1. (30 points) The Over each of the next two four-month by 3%: The risk free interest rate is 3% per annum pounding. Consider an eight-month option on the stock, with a strike price of $41. a) (5 points) What is the rick-neutral probability (P- 1-p)? b) (10 points) What is the price of the option if it is a...

price of a non-dividend-paying stock is currently $40. periods it will go up by 5% or down with continuous com- 1. (30 points) The Over each of the next two four-month by 3%: The risk free interest rate is 3% per annum pounding. Consider an eight-month option on the stock, with a strike price of $41. a) (5 points) What is the rick-neutral probability (P- 1-p)? b) (10 points) What is the price of the option if it is a...

Finance - Derivative Securities

1) A stock price is currently $100. Over each of the next two six-month periods it is expected togo up by 10% or down by 10%. The risk-free interest rate is 8% per annum with continuouscompounding. What is the value of a one-year European call option with a strike price of $100?2) For the situation considered in the previous problem, what is the value of a one-year Europeanput option with a strike price of $100? Verify that the European call...

urrently, the stock price is $50. Over each of the next two 1-yr periods it is...

urrently, the stock price is $50. Over each of the next two 1-yr periods it is expected to go up by 20% or down by 20%. The risk-free rate is 5% per annum with continuous compounding. What is the value of a 2-yr European call option with a strike price of $61? Round to the nearest cent. For example, if your answer is $12.345, then enter 12.35. Margin of error: +/- 0.10.

Question: Problem C. A stock's price is currently C1. Over each of the next two three-month...

Question: Problem C. A stock's price is currently C1. Over each of the next two three-month periods it is expected to go up by 10 percent or down by 10 percent. The risk-free interest rate is C2 percent per annum with continuous compounding. What is the current value of a six-month European Put option with strike price of C3 using a two-step binomial tree? How will you trade to make profits if the put option's current market price is C4,...

A stock price is currently $50. Over each of the next two three-month periods it is expected to go up by 5% or down by 5%. The risk-free interest rate is 10% per annum with continuous compounding. What is the value of a six-month American put option with a strike price of $54? quations you may find helpful: required precision O.01+- 0.01)

A stock price is currently $50. Over each of the next two three-month periods it is expected to go up by 5% or down by 5%. The risk-free interest rate is 10% per annum with continuous compounding. What is the value of a six-month American put option with a strike price of $54? quations you may find helpful: required precision O.01+- 0.01)

3. A stock price is currently $30. Over each of the next two three-month periods it is expected to go up by 20% or down by 20%. The risk-free interest rate is 4% per annum. What is the value of a six-month American put option with a strike price of $32? (15 marks)

3. A stock price is currently $30. Over each of the next two three-month periods it is expected to go up by 20% or down by 20%. The risk-free interest rate is 4% per annum. What is the value of a six-month American put option with a strike price of $32? (15 marks)

Question 1 a. A stock price is currently $30. It is known that at the end of two months it will be either $33 or $27. The risk-free interest rate is 10% per annum with continuous compounding. What is the value of a two-month European put option with a strike price of $31? b. What is meant by the delta of a stock option? A stock price is currently $100. Over each of the next two three-month periods it is...

Question 1 a. A stock price is currently $30. It is known that at the end of two months it will be either $33 or $27. The risk-free interest rate is 10% per annum with continuous compounding. What is the value of a two-month European put option with a strike price of $31? b. What is meant by the delta of a stock option? A stock price is currently $100. Over each of the next two three-month periods it is...

price of a non-dividend-paying stock is currently $40. periods it will go up by 5% or down with continuous com- 1. (30 points) The Over each of the next two four-month by 3%: The risk free interest rate is 3% per annum pounding. Consider an eight-month option on the stock, with a strike price of $41. a) (5 points) What is the rick-neutral probability (P- 1-p)? b) (10 points) What is the price of the option if it is a...

price of a non-dividend-paying stock is currently $40. periods it will go up by 5% or down with continuous com- 1. (30 points) The Over each of the next two four-month by 3%: The risk free interest rate is 3% per annum pounding. Consider an eight-month option on the stock, with a strike price of $41. a) (5 points) What is the rick-neutral probability (P- 1-p)? b) (10 points) What is the price of the option if it is a...

Most questions answered within 3 hours.

-

Consider the reaction, C3 H8 + O2 --> CO2 + H2O. How many

moles of O2...

asked 1 hour ago -

You and your opponent both roll a fair die. If you both roll the

same number,...

asked 1 hour ago -

In a study of the accuracy of fast food drive-through orders,

Restaurant A had 257 accurate...

asked 1 hour ago -

Identify and describe in detail the four categories of

institutions that could be included in a...

asked 1 hour ago -

In python

class Customer:

def __init__(self, customer_id, last_name, first_name, phone_number, address):

self._customer_id = int(customer_id)

self._last_name =...

asked 1 hour ago -

What is an example of a limitation in implementing a new

ERP system and how it...

asked 1 hour ago -

In a section of 9.7cm of an artery with a radius of 2.6mm there

is a...

asked 1 hour ago -

the two carboxylic acid groups of aspartic acid have different

acidities with pKa values of 2.1...

asked 1 hour ago -

Would CuCO3 aqueous salt combined with calcium chloride

form a solid precipitate? If so, what would...

asked 1 hour ago -

How do ECM Solutions assist in embedding a culture of continuous

improvement in an organization? (Project...

asked 1 hour ago -

Directions

These directions introduce the idea of Essential Questions.

Since this may be a new concept...

asked 1 hour ago -

1.b. Fiscal policy is said to suffer from ‘crowding out’.

Explain what this means and why...

asked 2 hours ago