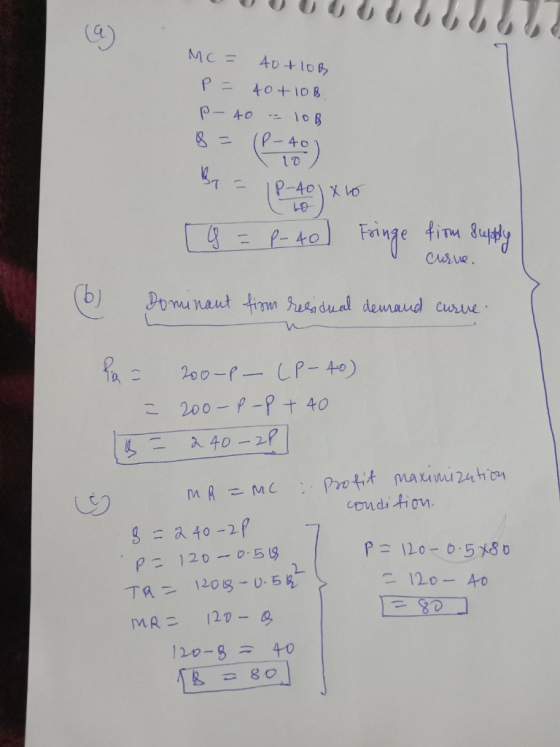

Consider a market with demand curve ?=200−? and suppose that the industry consists of a dominant...

Consider a market with demand curve ?=200−? and suppose that the

industry consists of a dominant firm which has a constant marginal

cost equal to $40 per unit. There are ten other fringe producers;

each has a marginal cost curve ??=40+10?,

where q is the output of a typical fringe producer. Assume there

are no fixed costs for any producer.

a. What is the supply curve of the competitive fringe?

b. What is the dominant firm’s residual demand curve?

c. Find dominant firm’s profit-maximizing output and price. At this

price, what is dominant firm’s market share?

Homework Answers

Add Answer to:

Consider a market with demand curve ?=200−? and suppose that the

industry consists of a dominant...

12. Consider an industry with a dominant firm and a competitive fringe. The market demand for...

12. Consider an industry with a dominant firm and a competitive fringe. The market demand for the product is given by P - 100 - 20 where P is the market price for the product, and Q is the total amount sold in the industry. The dominate firm's marginal cost is given by the equation MC-80, and the supply curve for the competitive fringe is Q-P/2. Use this information to find the Residual Demand curve faced by the dominant firm;...

12. Consider an industry with a dominant firm and a competitive fringe. The market demand for the product is given by P - 100 - 20 where P is the market price for the product, and Q is the total amount sold in the industry. The dominate firm's marginal cost is given by the equation MC-80, and the supply curve for the competitive fringe is Q-P/2. Use this information to find the Residual Demand curve faced by the dominant firm;...

The market demand curve is given by Q = 200-2p. There is one dominant firm, which sets the market...

The market demand curve is given by Q = 200-2p. There is one dominant firm, which sets the market price and has a constant marginal cost of 5, and a competitive fringe of 10 price-taking firms, each of which has a marginal cost function MC (Q) = 10 +Q. Derive the equation of the dominant firm’s residual demand curve. What price will the dominant firm set to maximize its profits? At this price, how much does the competitive fringe produce?

2. Consider a dominant firm in a market with a competitive fringe. The market demand curve...

2. Consider a dominant firm in a market with a competitive fringe. The market demand curve is given by P = 100 − Q.The supply curve of the competitive fringe is perfectly elastic and given by P=Pf. The dominant firm has a marginal cost c where Pf > c (a) For what value of Pf is the presence of the competitive fringe binding on the dominant firm? (b) Suppose the dominant firm has c = 0 and the competitive fringe...

Please answer me in detail. Thank you. Market demand curve is D(P)=400-5P. The oil drilling industry consists of 60 pro...

Please answer me in detail. Thank you.

Market demand curve is D(P)=400-5P.

The oil drilling industry consists of 60 producers, all of whom have an identical short- run total cost curve, STC(Q) = 64 + 2Q2, where Q is the monthly output of a firm and $64 is the monthly fixed cost. The corresponding short-run marginal cost curve is SMC(Q) 4Q. Assume that $32 of the firm's monthly $64 fixed cost can be avoided if the firm produces zero output...

Please answer me in detail. Thank you.

Market demand curve is D(P)=400-5P.

The oil drilling industry consists of 60 producers, all of whom have an identical short- run total cost curve, STC(Q) = 64 + 2Q2, where Q is the monthly output of a firm and $64 is the monthly fixed cost. The corresponding short-run marginal cost curve is SMC(Q) 4Q. Assume that $32 of the firm's monthly $64 fixed cost can be avoided if the firm produces zero output...

In a monopolistic competitive market for blood pressure monitor, suppose the market demand function for the monitor is P=160 – 3Q, where P is the price for monitor, Q and the quantity of monitor dema...

In a monopolistic competitive market for blood pressure monitor, suppose the market demand function for the monitor is P=160 – 3Q, where P is the price for monitor, Q and the quantity of monitor demanded. Marginal cost of producing it is MC: P = 20 + Q, where P is the price of the monitor and Q is the quantity of the monitor sold. Use the Twice as Steep Rule, form the marginal revenue function. What are the price and...

12.10. Suppose that the total market demand for crude oil is given by Qp70,000 - 2,000...

12.10. Suppose that the total market demand for crude oil is given by Qp70,000 - 2,000 P, where Qp is the quantity of oil in thousands of barrels per year and P is the dollar price per barrel. Suppose also that there are 1,000 identical small producers of crude oil, each with marginal costs given by MC = q+5, where q is the output of the typical firm a. Assuming that each small oil producer acts as a price taker,...

12.10. Suppose that the total market demand for crude oil is given by Qp70,000 - 2,000 P, where Qp is the quantity of oil in thousands of barrels per year and P is the dollar price per barrel. Suppose also that there are 1,000 identical small producers of crude oil, each with marginal costs given by MC = q+5, where q is the output of the typical firm a. Assuming that each small oil producer acts as a price taker,...

2. (15 points). The demand function for an oligopolistic market is given by the equation, Q 180-4P, where Q is quantity demanded and P is price. The industry has one dominant firm whose margina...

2. (15 points). The demand function for an oligopolistic market is given by the equation, Q 180-4P, where Q is quantity demanded and P is price. The industry has one dominant firm whose marginal cost function is: MC 12+1Qp, and many small firms, with a total supply function: Qs 20+ P. (a) Derive the demand equation for the dominant oligopoly firm. (b) Determine the dominant oligopoly firm's profit-maximizing out- put and price. (c) Determine the total output of the small...

2. (15 points). The demand function for an oligopolistic market is given by the equation, Q 180-4P, where Q is quantity demanded and P is price. The industry has one dominant firm whose marginal cost function is: MC 12+1Qp, and many small firms, with a total supply function: Qs 20+ P. (a) Derive the demand equation for the dominant oligopoly firm. (b) Determine the dominant oligopoly firm's profit-maximizing out- put and price. (c) Determine the total output of the small...

3. Suppose XYZ Company is a dominant firm in a particular industry. The demand curve for...

3. Suppose XYZ Company is a dominant firm in a particular industry. The demand curve for this industry’s product is ? = 200 − 10?, where Q is the quantity demanded and P is the price. The supply curve for the small firms in the industry is ?? = 20 + 2?, where ?? is the total amount supplied by all the small firms combined. XYZ Company’s marginal cost is ?? = 2??, where ?? is XYZ Company’s output. Question:...

Suppose demand for wind turbines is Q = 110-3P, where P is the price. The dominant...

Suppose demand for wind turbines is Q = 110-3P, where P is the price. The dominant producer in this industry is “Winnie’s Wind Turbines”. There are also a number of small price-taking firms that can be represented by the supply function S(P)=P-10. The marginal cost of production for the dominant firm is given by mcd=10 and the total cost function is given by 10qd. What quantity would Winnie’s Wind Turbines supply in the wind turbine market? What would be the...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve and supply curve are as follows: Demand: Qp = 2000-P Supply: 2 = 1400 +2P Firm K is one of the many firms producing popcorn in the market. The total cost function and marginal cost function are as follows: TC(q) =1250 +30 +29 MC(q) - 30 +49 i At what output level (g) would the average total cost be minimized? (6 marks) ii What...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve and supply curve are as follows: Demand: Qp = 2000-P Supply: 2 = 1400 +2P Firm K is one of the many firms producing popcorn in the market. The total cost function and marginal cost function are as follows: TC(q) =1250 +30 +29 MC(q) - 30 +49 i At what output level (g) would the average total cost be minimized? (6 marks) ii What...

12. Consider an industry with a dominant firm and a competitive fringe. The market demand for the product is given by P - 100 - 20 where P is the market price for the product, and Q is the total amount sold in the industry. The dominate firm's marginal cost is given by the equation MC-80, and the supply curve for the competitive fringe is Q-P/2. Use this information to find the Residual Demand curve faced by the dominant firm;...

12. Consider an industry with a dominant firm and a competitive fringe. The market demand for the product is given by P - 100 - 20 where P is the market price for the product, and Q is the total amount sold in the industry. The dominate firm's marginal cost is given by the equation MC-80, and the supply curve for the competitive fringe is Q-P/2. Use this information to find the Residual Demand curve faced by the dominant firm;...

Please answer me in detail. Thank you.

Market demand curve is D(P)=400-5P.

The oil drilling industry consists of 60 producers, all of whom have an identical short- run total cost curve, STC(Q) = 64 + 2Q2, where Q is the monthly output of a firm and $64 is the monthly fixed cost. The corresponding short-run marginal cost curve is SMC(Q) 4Q. Assume that $32 of the firm's monthly $64 fixed cost can be avoided if the firm produces zero output...

Please answer me in detail. Thank you.

Market demand curve is D(P)=400-5P.

The oil drilling industry consists of 60 producers, all of whom have an identical short- run total cost curve, STC(Q) = 64 + 2Q2, where Q is the monthly output of a firm and $64 is the monthly fixed cost. The corresponding short-run marginal cost curve is SMC(Q) 4Q. Assume that $32 of the firm's monthly $64 fixed cost can be avoided if the firm produces zero output...

12.10. Suppose that the total market demand for crude oil is given by Qp70,000 - 2,000 P, where Qp is the quantity of oil in thousands of barrels per year and P is the dollar price per barrel. Suppose also that there are 1,000 identical small producers of crude oil, each with marginal costs given by MC = q+5, where q is the output of the typical firm a. Assuming that each small oil producer acts as a price taker,...

12.10. Suppose that the total market demand for crude oil is given by Qp70,000 - 2,000 P, where Qp is the quantity of oil in thousands of barrels per year and P is the dollar price per barrel. Suppose also that there are 1,000 identical small producers of crude oil, each with marginal costs given by MC = q+5, where q is the output of the typical firm a. Assuming that each small oil producer acts as a price taker,...

2. (15 points). The demand function for an oligopolistic market is given by the equation, Q 180-4P, where Q is quantity demanded and P is price. The industry has one dominant firm whose marginal cost function is: MC 12+1Qp, and many small firms, with a total supply function: Qs 20+ P. (a) Derive the demand equation for the dominant oligopoly firm. (b) Determine the dominant oligopoly firm's profit-maximizing out- put and price. (c) Determine the total output of the small...

2. (15 points). The demand function for an oligopolistic market is given by the equation, Q 180-4P, where Q is quantity demanded and P is price. The industry has one dominant firm whose marginal cost function is: MC 12+1Qp, and many small firms, with a total supply function: Qs 20+ P. (a) Derive the demand equation for the dominant oligopoly firm. (b) Determine the dominant oligopoly firm's profit-maximizing out- put and price. (c) Determine the total output of the small...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve and supply curve are as follows: Demand: Qp = 2000-P Supply: 2 = 1400 +2P Firm K is one of the many firms producing popcorn in the market. The total cost function and marginal cost function are as follows: TC(q) =1250 +30 +29 MC(q) - 30 +49 i At what output level (g) would the average total cost be minimized? (6 marks) ii What...

Question 3 (32 marks) a The market of popcom is perfectly competitive. The market demand curve and supply curve are as follows: Demand: Qp = 2000-P Supply: 2 = 1400 +2P Firm K is one of the many firms producing popcorn in the market. The total cost function and marginal cost function are as follows: TC(q) =1250 +30 +29 MC(q) - 30 +49 i At what output level (g) would the average total cost be minimized? (6 marks) ii What...

Most questions answered within 3 hours.

-

A coach uses a new technique to train gymnasts. Seven

gymnasts were randomly selected and their...

asked 1 hour ago -

While rotating the tires on your car you notice a rock [mass =

0.1 Kg] stuck...

asked 3 hours ago -

Using MARS simulator, write MIPS programs according to

the following scenarios: Receive a positive integer number...

asked 5 hours ago -

An object in front of a concave mirror has a real image that is

11.5 cm...

asked 5 hours ago -

Consider the reaction, C3 H8 + O2 --> CO2 + H2O. How many

moles of O2...

asked 7 hours ago -

You and your opponent both roll a fair die. If you both roll the

same number,...

asked 7 hours ago -

In a study of the accuracy of fast food drive-through orders,

Restaurant A had 257 accurate...

asked 7 hours ago -

Identify and describe in detail the four categories of

institutions that could be included in a...

asked 7 hours ago -

In python

class Customer:

def __init__(self, customer_id, last_name, first_name, phone_number, address):

self._customer_id = int(customer_id)

self._last_name =...

asked 7 hours ago -

What is an example of a limitation in implementing a new

ERP system and how it...

asked 7 hours ago -

In a section of 9.7cm of an artery with a radius of 2.6mm there

is a...

asked 7 hours ago -

the two carboxylic acid groups of aspartic acid have different

acidities with pKa values of 2.1...

asked 7 hours ago