Homework Answers

Add Answer to:

Text Question 3.9 A typical firm in long-run equilibrium in an industry with identical firms has...

2. (1.5 p) Consider perfectly competitive industry with identical firms. The long run average cots function...

2. (1.5 p) Consider perfectly competitive industry with identical firms. The long run average cots function of a typical firm is given by AC(q)- 24 - 49 + q. Market demand is given by c p)=100-2p. (a) Find the long run supply curve of the typical firm. (b) Find the number of firms in the industry in the long run equilibrium.

2. (1.5 p) Consider perfectly competitive industry with identical firms. The long run average cots function of a typical firm is given by AC(q)- 24 - 49 + q. Market demand is given by c p)=100-2p. (a) Find the long run supply curve of the typical firm. (b) Find the number of firms in the industry in the long run equilibrium.

11. Kites are manufactured by identical firms in a perfectly competitive environment. Each firm’s long run...

11. Kites are manufactured by identical firms in a perfectly competitive environment. Each firm’s long run average cost and marginal cost of production are given by: AC = Q + 100/Q and MC = 2Q where Q is the number of kites produced. a) In long run equilibrium, how many kites will each firm produce? (2 pts) b) What will the price of kites (P) be? (1 pt) c) Suppose the demand for kites is given by formula Q =...

2. A competitive industry has 12 identical firms, each one has a total variable cost function...

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

Suppose that all existing firms in a long-run competitive market equilibrium are identical and have the...

Suppose that all existing firms in a long-run competitive market equilibrium are identical and have the following cost function C(Q)= 1002 with MC(Q)=2Q. Suppose also that market demand is given by P(Q)=A-0.04Q, where A-40.0. What is the equilibrium market quantity? No units, no rounding. Your Answer: Your Answer

Suppose that all existing firms in a long-run competitive market equilibrium are identical and have the following cost function C(Q)= 1002 with MC(Q)=2Q. Suppose also that market demand is given by P(Q)=A-0.04Q, where A-40.0. What is the equilibrium market quantity? No units, no rounding. Your Answer: Your Answer

1. (25 points) The market for study desks is characterized by perfect competition. Firms and consumers are price takers and in the long run there is free entry and exit of firms in this industry. Al...

1. (25 points) The market for study desks is characterized by perfect competition. Firms and consumers are price takers and in the long run there is free entry and exit of firms in this industry. All firms are identical in terms of their technological capabilities. Thus the cost function as given below for a representative firm can be assumed to function faced by each firm in the industry. The total cost and marginal cost functions t the representative firm are...

1. (25 points) The market for study desks is characterized by perfect competition. Firms and consumers are price takers and in the long run there is free entry and exit of firms in this industry. All firms are identical in terms of their technological capabilities. Thus the cost function as given below for a representative firm can be assumed to function faced by each firm in the industry. The total cost and marginal cost functions t the representative firm are...

1. All (identical) firms in a competitive industry have the following long-run total cost curve: C(q)...

1. All (identical) firms in a competitive industry have the following long-run total cost curve: C(q) = q3 – 10q2 + 369 where q is the output of the firm. a. Compute the long run equilibrium price. What does the long-run supply curve look like? b. Suppose the market demand is given by Q=111 - p. Determine the long-run equilibrium number of firms in the industry.

1. All (identical) firms in a competitive industry have the following long-run total cost curve: C(q) = q3 – 10q2 + 369 where q is the output of the firm. a. Compute the long run equilibrium price. What does the long-run supply curve look like? b. Suppose the market demand is given by Q=111 - p. Determine the long-run equilibrium number of firms in the industry.

Question 2 The tortilla industry commissions you to examine the outlook for firms selling tortillas. There...

Question 2 The tortilla industry commissions you to examine the outlook for firms selling tortillas. There are currently twenty, identical price-taking firms in this perfectly competitive market. Each firm has a short-run cost function of STC(Q) = 9+ 2Q + . When the price is P, the total quantity demanded is given by Q(P) = 100 – 2P . (a) Assuming all fixed costs are sunk, find the short-run supply curve for a typical firm. (b) In the short run,...

Question 2 The tortilla industry commissions you to examine the outlook for firms selling tortillas. There are currently twenty, identical price-taking firms in this perfectly competitive market. Each firm has a short-run cost function of STC(Q) = 9+ 2Q + . When the price is P, the total quantity demanded is given by Q(P) = 100 – 2P . (a) Assuming all fixed costs are sunk, find the short-run supply curve for a typical firm. (b) In the short run,...

Suppose there are n identical firms in the market for plums. Each firm's cost function is...

Suppose there are n identical firms in the market for plums. Each firm's cost function is given by C(q)=25+q^2 where q represents the amount that an individual firm will produce. Also, the market demand for plums is given by P = 100 - 2Q, where Q is the total amount of the good produced by all the firms combined (Q=q*n). How much output will each firm produce in the long run? What will be the long run equilibrium price? How...

Suppose all firms in the market are identical. Each firm has a long run total cost...

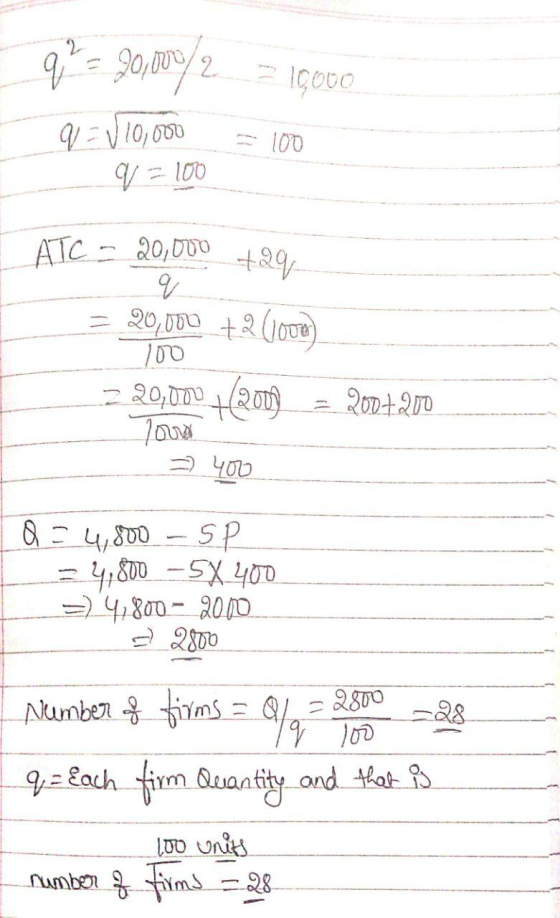

Suppose all firms in the market are identical. Each firm has a long run total cost curve LTC = 40Q – Q2 + 0.01Q3. The market demand curve is Q = 20,000 – 100P. Find the long run equilibrium quantity per firm, price, and number of firms in the market.

Suppose all firms in the market are identical. Each firm has a long run total cost curve LTC = 40Q – Q2 + 0.01Q3. The market demand curve is Q = 20,000 – 100P. Find the long run equilibrium quantity per firm, price, and number of firms in the market.

Question 12 (1 point) Suppose that all existing firms in a long-run competitive market equilibrium are...

Question 12 (1 point) Suppose that all existing firms in a long-run competitive market equilibrium are identical and have the following cost function C(Q) = 100 + Q? with MCIQ)=2Q. Suppose also that market demand is given by P(Q)=A-0.04Q, where A=80.0. What is the equilibrium market quantity? No units, no rounding. Your Answer: Your Answer

Question 12 (1 point) Suppose that all existing firms in a long-run competitive market equilibrium are identical and have the following cost function C(Q) = 100 + Q? with MCIQ)=2Q. Suppose also that market demand is given by P(Q)=A-0.04Q, where A=80.0. What is the equilibrium market quantity? No units, no rounding. Your Answer: Your Answer

2. (1.5 p) Consider perfectly competitive industry with identical firms. The long run average cots function of a typical firm is given by AC(q)- 24 - 49 + q. Market demand is given by c p)=100-2p. (a) Find the long run supply curve of the typical firm. (b) Find the number of firms in the industry in the long run equilibrium.

2. (1.5 p) Consider perfectly competitive industry with identical firms. The long run average cots function of a typical firm is given by AC(q)- 24 - 49 + q. Market demand is given by c p)=100-2p. (a) Find the long run supply curve of the typical firm. (b) Find the number of firms in the industry in the long run equilibrium.

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

2. A competitive industry has 12 identical firms, each one has a total variable cost function TVC(a) 402 and a marginal cost function MC(a) 40+q, the firm's fixed cost.s are entirely non-sunk (that is, must be paid only if q >0) and equal to 50. (a) Calculate the price below which the firm will produce q 0. (b) The market demand is QD(p) 360-2p. What is the short-run equilibrium price and quantity supplied by each firm? Calculate each firm's proft...

Suppose that all existing firms in a long-run competitive market equilibrium are identical and have the following cost function C(Q)= 1002 with MC(Q)=2Q. Suppose also that market demand is given by P(Q)=A-0.04Q, where A-40.0. What is the equilibrium market quantity? No units, no rounding. Your Answer: Your Answer

Suppose that all existing firms in a long-run competitive market equilibrium are identical and have the following cost function C(Q)= 1002 with MC(Q)=2Q. Suppose also that market demand is given by P(Q)=A-0.04Q, where A-40.0. What is the equilibrium market quantity? No units, no rounding. Your Answer: Your Answer

1. (25 points) The market for study desks is characterized by perfect competition. Firms and consumers are price takers and in the long run there is free entry and exit of firms in this industry. All firms are identical in terms of their technological capabilities. Thus the cost function as given below for a representative firm can be assumed to function faced by each firm in the industry. The total cost and marginal cost functions t the representative firm are...

1. (25 points) The market for study desks is characterized by perfect competition. Firms and consumers are price takers and in the long run there is free entry and exit of firms in this industry. All firms are identical in terms of their technological capabilities. Thus the cost function as given below for a representative firm can be assumed to function faced by each firm in the industry. The total cost and marginal cost functions t the representative firm are...

1. All (identical) firms in a competitive industry have the following long-run total cost curve: C(q) = q3 – 10q2 + 369 where q is the output of the firm. a. Compute the long run equilibrium price. What does the long-run supply curve look like? b. Suppose the market demand is given by Q=111 - p. Determine the long-run equilibrium number of firms in the industry.

1. All (identical) firms in a competitive industry have the following long-run total cost curve: C(q) = q3 – 10q2 + 369 where q is the output of the firm. a. Compute the long run equilibrium price. What does the long-run supply curve look like? b. Suppose the market demand is given by Q=111 - p. Determine the long-run equilibrium number of firms in the industry.

Question 2 The tortilla industry commissions you to examine the outlook for firms selling tortillas. There are currently twenty, identical price-taking firms in this perfectly competitive market. Each firm has a short-run cost function of STC(Q) = 9+ 2Q + . When the price is P, the total quantity demanded is given by Q(P) = 100 – 2P . (a) Assuming all fixed costs are sunk, find the short-run supply curve for a typical firm. (b) In the short run,...

Question 2 The tortilla industry commissions you to examine the outlook for firms selling tortillas. There are currently twenty, identical price-taking firms in this perfectly competitive market. Each firm has a short-run cost function of STC(Q) = 9+ 2Q + . When the price is P, the total quantity demanded is given by Q(P) = 100 – 2P . (a) Assuming all fixed costs are sunk, find the short-run supply curve for a typical firm. (b) In the short run,...

Suppose all firms in the market are identical. Each firm has a long run total cost curve LTC = 40Q – Q2 + 0.01Q3. The market demand curve is Q = 20,000 – 100P. Find the long run equilibrium quantity per firm, price, and number of firms in the market.

Suppose all firms in the market are identical. Each firm has a long run total cost curve LTC = 40Q – Q2 + 0.01Q3. The market demand curve is Q = 20,000 – 100P. Find the long run equilibrium quantity per firm, price, and number of firms in the market.

Question 12 (1 point) Suppose that all existing firms in a long-run competitive market equilibrium are identical and have the following cost function C(Q) = 100 + Q? with MCIQ)=2Q. Suppose also that market demand is given by P(Q)=A-0.04Q, where A=80.0. What is the equilibrium market quantity? No units, no rounding. Your Answer: Your Answer

Question 12 (1 point) Suppose that all existing firms in a long-run competitive market equilibrium are identical and have the following cost function C(Q) = 100 + Q? with MCIQ)=2Q. Suppose also that market demand is given by P(Q)=A-0.04Q, where A=80.0. What is the equilibrium market quantity? No units, no rounding. Your Answer: Your Answer

Most questions answered within 3 hours.

-

At the start of a CD it is spinning at a rate of 525 rpm

(revolutions...

asked 9 minutes ago -

4. Without doing any calculations, predict whether the observed

∆T would increase, decrease or remain the...

asked 1 hour ago -

Based on the range, which of the following sets of scores has

the greatest variability? 3,...

asked 2 hours ago -

Ripples in a pond travel at a velocity of 3 m/s with one peak

passing a...

asked 2 hours ago -

A man stands on the roof of a building of height 13.0 mm and

throws a...

asked 2 hours ago -

The extent to which assets are financed by borrowed funds and

other liabilities is indicated by:...

asked 3 hours ago -

Explain in detail

Germany is the fifth largest economy

explain what goods and services Germany specializes...

asked 3 hours ago -

The density of platinum is 21.45 g/mL. If a cube of platinum

with a mass of...

asked 3 hours ago -

Accounts Receivable

Sales

A/R Posting

Extended Sales Invoice

Packing Slip

Compare invoice to packing slip 2...

asked 3 hours ago -

Michaella, age 23, is a full-time law student and is claimed by

her parents as a...

asked 3 hours ago -

Why are polymers not typically casted into products?

asked 4 hours ago -

When rolling a die 129 times, what is the probability of rolling

a 6 no more...

asked 4 hours ago