ok

Complete this question by entering your answers in the tabs below. Required 1 Required 2 Determine pension expense for 2018. (Amounts to be deducted should be indicated with a minus sign. Enter your answers in thousands rounded to 1 decimal place (i.e., 5,500 should be entered as 5.5).) Pension Expense Pension expense 0.0 Required 2

V Required 1 Required 2 Prepare the journal entries to record pension expense, gains and losses (if any), funding, and retiree benefits for 2018. (If no entry is required for a transaction/event, select "No jounal entry required" in the first account field. Enter your answers in thousands rounded to 1 decimal place (1.e., 5,500 should be entered as 5.5).) 10 points View transaction list eBook Journal entry worksheet 1 3 4 Hint Record the pension expense. Note: Enter debits before credits. References Event General Journal Debit Credit 1 Record entry Clear entry View general journal

00 Required 1 Required 2 Prepare the journal entries to record pension expense, gains and losses (if any), funding, and retiree benefits for 2018. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Enter your answers in thousands rounded to 1 decimal place (l.e., 5,500 should be entered as 5.5).) 10 points View transaction list Journal entry worksheet eBook Hint Record the funding. Print Note: Enter debits before credits. References Event General Journal Debit Credit 3 Record entry Clear entry View general journal

0 Required 1 Required 2 Prepare the journal entries to record pension expense, gains and losses (if any),, funding, and retiree benefits for 2018. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Enter your answers in thousands rounded to 1 decimal place (i.e., 5,500 should be entered as 5.5).) 10 points View transaction list eBook Journal entry worksheet 2 3 4 Hint Record the retiree benefits. Print Note: Enter debits before credits. References Event General Journal Debit Credit 4 Record entry Clear entry View general journal

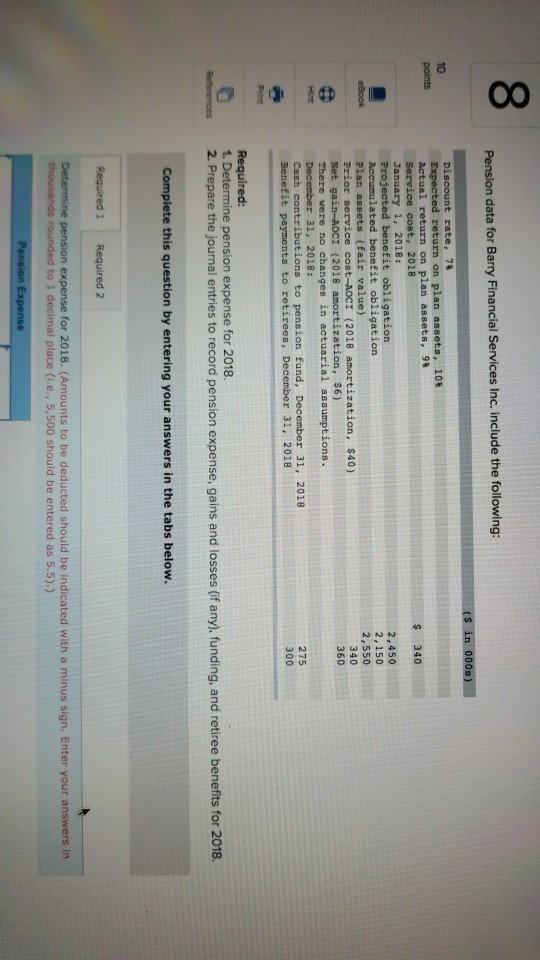

00 Pension data for Barry Financial Services Inc. include the following: ($ in 000s) Discount rate, 78 Expected return on plan assets, 10% Actual return on plan assets, 98 Service cost, 2018 January 1, 2018: Projected benefit obligation Accumulated benefit obligation Plan assets (fair value) Prior service cost--AOCI (2018 amortization, $40) Net gain-AOCI (2018 amortization, $6) There were no changes in actuarial assumptions. December 31, 2018: Cash contributions to pension fund, December 31, 2018 Benefit payments to retirees, December 31, 2018 10 points 340 Skipped 2,450 2,150 2,550 340 eBook 360 275 Hint 300 Required: 1. Determine pension expense for 2018. 2. Prepare the journal entries to record pension expense, gains and losses (if any), funding, and retiree benefits for 2018. Print References Complete this question by entering your answers in the tabs below. Required 1 Required 2 Determine pension se for 2018. (Amounts to be deducted should be indicated with a minus sign. Enter your answers n

Cash contributions to pension fund, December 31, 2018 Benefit payments to retirees, December 31, 2018 points 275 300 Skipped Required: 1. Determine pension expense for 2018. 2. Prepare the journal entries to record pension expense, gains and losses (if any), funding, and retiree benefits for 2018. eBook Complete this question by entering your answers in the tabs below. Hint Required 1 Required 2 Print Determine pension expense for 2018. (Amounts to be deducted should be indicated with a minus sign. Enter your answers in thousands rounded to 1 decimal place (i.e., 5,500 should be entered as 5.5).) References Pension Expense Pension expense 0.0 Required 2>

00 149 Che Complete this question by entering your answers in the tabs below. points Required 1 Required 2 Skipped Prepare the journal entries to record pension expense, gains and losses (if any), funding, and retiree benefits for 2018. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Enter your answers in thousands rounded to 1 decimal place (i.e., 5,500 should be entered as 5.5).) eBook View transaction list Hint Journal entry worksheet Print 1 2 4 Record the pension expense. References Note: Enter debits before credits. Event General Journal Debit Credit 1

00 Complete this question by entering your answers in the tabs below. 10 points Required 1 Required 2 Skipped Prepare the journal entries to record pension expense, gains and losses (if any), funding, and retiree benefits for 2018. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Enter your answers in thousands rounded to 1 decimal place (i.e., 5,500 should be entered as 5.5).) eBook View transaction list Hint Journal entry worksheet Print 1 2 3 4 Record the gain or loss on assets. References Note: Enter debits before credits. Event General Journal Debit Credit 2

00 Complete this question by entering your answers in the tabs below. 10 points Required 1 Required 2 Skipped Prepare the journal entries to record pension expense, gains and losses (if any), funding, and retiree benefits for 2018. (If no required for a transaction/event, select "No journal entry required" in the first account field. Enter your answers in thousands 1 decimal place (1.e., 5,500 should be entered as 5.5).) eBook View transaction list Hint Journal entry worksheet Print 1 2 4 Record the funding. References Note: Enter debits before credits. Event General Journal Debit Credit 3

00 Complete this question by entering your answers in the tabs below. 10 points Required 1 Required 2 Skipped Prepare the journal entries to record pension expense, gains and losses (if any), funding, and retiree benefits for 2018. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Enter your answers in thousands rounded to 1 decimal place (i.e., 5,500 should be entered as 5.5).) eBook View transaction list Hint Journal entry worksheet Print

Homework Answers

Part 1

Pension expense

|

Service cost |

340 |

|

Interest cost (2450*7%) |

171.5 |

|

Expected return on assets (2550*10%) |

(255) |

|

Amortization of prior service cost |

40 |

|

Amortization of net gain |

(6) |

|

Pension expense |

$290.5 |

Part 2

|

Event |

General journal |

Debit |

Credit |

|

1 |

Pension expense |

290.5 |

|

|

Plan assets |

255 |

||

|

Amortization of net gain—OCI |

6 |

||

|

Amortization of prior service cost—OCI |

40 |

||

|

PBO (340+171.5) |

511.5 |

||

|

(to record pension expense) |

|||

|

2 |

Loss—OCI |

25.5 |

|

|

Plan assets (10%*2550)-(9%*2550) |

25.5 |

||

|

(to record the gain or loss on assets) |

|||

|

3 |

Plan assets |

275 |

|

|

Cash |

275 |

||

|

(to record the funding) |

|||

|

4 |

PBO |

300 |

|

|

Plan assets |

300 |

||

|

(to record the retiree benefits) |

Add Answer to:

ok

IO 1 CO Pension data for Barry Financial Services Inc. include the following: (S in...

Pension data for Barry Financial Services Inc. include the following: ($ in 0008) $ 470 Discount...

Pension data for Barry Financial Services Inc. include the following: ($ in 0008) $ 470 Discount rate, 78 Expected return on plan assets, 116 Actual return on plan assets, 108 Service cost, 2018 January 1, 2018: Projected benefit obligation Accumulated benefit obligation Plan assets (fair value) Prior service cost-AOCI (2018 amortization, $45) Net gain-AOCI (2018 amortization, $12) There were no changes in actuarial assumptions. December 31, 2018: Cash contributions to pension fund, December 31, 2018 Benefit payments to retirees, December...

Pension data for Barry Financial Services Inc. include the following: ($ in 0008) $ 470 Discount rate, 78 Expected return on plan assets, 116 Actual return on plan assets, 108 Service cost, 2018 January 1, 2018: Projected benefit obligation Accumulated benefit obligation Plan assets (fair value) Prior service cost-AOCI (2018 amortization, $45) Net gain-AOCI (2018 amortization, $12) There were no changes in actuarial assumptions. December 31, 2018: Cash contributions to pension fund, December 31, 2018 Benefit payments to retirees, December...

Pension data for Barry Financial Services Inc. include the following: ($ in 000) $ 340 Discount...

Pension data for Barry Financial Services Inc. include the following: ($ in 000) $ 340 Discount rate, 78 Expected return on plan assets, 10% Actual return on plan assets, 99 Service cost, 2018 January 1, 2018: Projected benefit obligation Accumulated benefit obligation Plan assets (fair value) Prior service cost-AOCI (2018 amortization, $40) Net gain-AOCI (2018 amortization, $6) There were no changes in actuarial assumptions. December 31, 2018: Cash contributions to pension fund, December 31, 2018 Benefit payments to retirees, December...

Pension data for Barry Financial Services Inc. include the following: ($ in 000) $ 340 Discount rate, 78 Expected return on plan assets, 10% Actual return on plan assets, 99 Service cost, 2018 January 1, 2018: Projected benefit obligation Accumulated benefit obligation Plan assets (fair value) Prior service cost-AOCI (2018 amortization, $40) Net gain-AOCI (2018 amortization, $6) There were no changes in actuarial assumptions. December 31, 2018: Cash contributions to pension fund, December 31, 2018 Benefit payments to retirees, December...

Pension data for Barry Financial Services Inc. include the following: ($ in 000s) Discount rate, 7%...

Pension data for Barry Financial Services Inc. include the following: ($ in 000s) Discount rate, 7% Expected return on plan assets, 12% Actual return on plan assets, 11% Service cost, 2018 $ 360 January 1, 2018: Projected benefit obligation 2,550 Accumulated benefit obligation 2,250 Plan assets (fair value) 2,650 Prior service cost–AOCI (2018 amortization, $50) 350 Net gain–AOCI (2018 amortization, $8) 380 There were no changes in actuarial assumptions. December 31, 2018: Cash contributions to pension fund, December 31, 2018...

Exercise 17-22 IFRS; prior service cost [LO17-7, 17-12] Lacy Construction has a noncontributory, defined benefit pension...

Exercise 17-22 IFRS; prior service cost [LO17-7, 17-12] Lacy Construction has a noncontributory, defined benefit pension plan. At December 31, 2018. Lacy received the following information: ($ in millions) $ 749 98 Projected Benefit Obligation Balance, January 1 Service cost Prior service cost Interest cost(5%) Benefits paid Balance, December 31 50 (96) $ 829 ($ in millions) $ 610 62 Plan Assets Balance, January 1 Actual return on plan assets Contributions 2018 Benefits paid Balance, December 31 98 (96) The...

Exercise 17-22 IFRS; prior service cost [LO17-7, 17-12] Lacy Construction has a noncontributory, defined benefit pension plan. At December 31, 2018. Lacy received the following information: ($ in millions) $ 749 98 Projected Benefit Obligation Balance, January 1 Service cost Prior service cost Interest cost(5%) Benefits paid Balance, December 31 50 (96) $ 829 ($ in millions) $ 610 62 Plan Assets Balance, January 1 Actual return on plan assets Contributions 2018 Benefits paid Balance, December 31 98 (96) The...

Pension data for Barry Financial Services Inc. include the following: ($ in 000s) Discount rate, 7%...

Pension data for Barry Financial Services Inc. include the following: ($ in 000s) Discount rate, 7% Expected return on plan assets, 10% Actual return on plan assets, 9% Service cost, 2018 January 1, 2018: Projected benefit obligation Accumulated benefit obligation Plan assets (fair value) Prior service cost-A0CI (2018 amortization, $40) Net gain-A0CI (2018 amortization, $8) There were no changes in actuarial assumptions. December 31, 2018: Cash contributions to pension fund, December 31, 2018 Benefit payments to retirees, December 31, 2018...

Pension data for Barry Financial Services Inc. include the following: ($ in 000s) Discount rate, 7% Expected return on plan assets, 10% Actual return on plan assets, 9% Service cost, 2018 January 1, 2018: Projected benefit obligation Accumulated benefit obligation Plan assets (fair value) Prior service cost-A0CI (2018 amortization, $40) Net gain-A0CI (2018 amortization, $8) There were no changes in actuarial assumptions. December 31, 2018: Cash contributions to pension fund, December 31, 2018 Benefit payments to retirees, December 31, 2018...

Pension data for Barry Financial Services Inc. include the following: ($ in 000s) Discount rate, 7%...

Pension data for Barry Financial Services Inc. include the following: ($ in 000s) Discount rate, 7% Expected return on plan assets, 9% Actual return on plan assets, 8% Service cost, 2018 $ 390 January 1, 2018: Projected benefit obligation 2,700 Accumulated benefit obligation 2,400 Plan assets (fair value) 2,800 Prior service cost–AOCI (2018 amortization, $35) 365 Net gain–AOCI (2018 amortization, $8) 410 There were no changes in actuarial assumptions. December 31, 2018: Cash contributions to pension fund, December 31, 2018...

Exercise 17-27 Postretirement benefits; components of postretirement benefit expense (LO17-11] Data pertaining to the postretirement health...

Exercise 17-27 Postretirement benefits; components of postretirement benefit expense (LO17-11] Data pertaining to the postretirement health care benefit plan of Sterling Properties include the following for 2018: ($ in wees) $ 142 1.es 50 Service cost Accumulated postretirement benefit obligation, January 1 Plan assets (fair value), January 1 Prior service cost-AOCI Net gain-AOCI (2018 amortization, $1) Retiree benefits paid (end of year) Contribution to health care benefit fund (end of year) Discount rate, 6% Return on plan assets (actual and...

Exercise 17-27 Postretirement benefits; components of postretirement benefit expense (LO17-11] Data pertaining to the postretirement health care benefit plan of Sterling Properties include the following for 2018: ($ in wees) $ 142 1.es 50 Service cost Accumulated postretirement benefit obligation, January 1 Plan assets (fair value), January 1 Prior service cost-AOCI Net gain-AOCI (2018 amortization, $1) Retiree benefits paid (end of year) Contribution to health care benefit fund (end of year) Discount rate, 6% Return on plan assets (actual and...

Actuary and trustee reports indicate the following changes in the PBO and plan assets of Douglas-Roberts Industri...

Actuary and trustee reports indicate the following changes in the PBO and plan assets of Douglas-Roberts Industries during 2018: Prior service costat Jan. 1. 2018, from plan amendment at the beginning of 2015 (amortization$8 million per year) Net loss-AOCI at Jan.1, 2018 (previous losses exceeded previous gains) Average remaining service life of the active employee group Actuary's discount rate $ 40 million $118 million 10 years 5 ($ in millions) Pво Beginning of 2018 Service cost Plan Assets $ 660...

Actuary and trustee reports indicate the following changes in the PBO and plan assets of Douglas-Roberts Industries during 2018: Prior service costat Jan. 1. 2018, from plan amendment at the beginning of 2015 (amortization$8 million per year) Net loss-AOCI at Jan.1, 2018 (previous losses exceeded previous gains) Average remaining service life of the active employee group Actuary's discount rate $ 40 million $118 million 10 years 5 ($ in millions) Pво Beginning of 2018 Service cost Plan Assets $ 660...

Problem 17-8 Pension spreadsheet; record pension expense and funding; new gains and losses [LO17-7, 17-8] A...

Problem 17-8 Pension spreadsheet; record pension expense and funding; new gains and losses [LO17-7, 17-8] A partially completed pension spreadsheet showing the relationships among the elements that constitute Carney, Inc., defined benefit pension plan follows. Six years earlier. Carney revised its pension formula and recalculated benefits earned by employees in prior years using the more generous formula. The prior service cost created by the recalculation is being amortized at the rate of $4 million per year. At the end of...

Problem 17-8 Pension spreadsheet; record pension expense and funding; new gains and losses [LO17-7, 17-8] A partially completed pension spreadsheet showing the relationships among the elements that constitute Carney, Inc., defined benefit pension plan follows. Six years earlier. Carney revised its pension formula and recalculated benefits earned by employees in prior years using the more generous formula. The prior service cost created by the recalculation is being amortized at the rate of $4 million per year. At the end of...

Data pertaining to the postretirement health care benefit plan of Sterling Properties include the following for...

Data pertaining to the postretirement health care benefit plan of Sterling Properties include the following for 2018: ($ in 0008) $ 136 700 Service cost Accumulated postretirement benefit obligation, January 1 Plan assets (fair value), January 1 Prior service cost-AOCI Net gain-AOCI (2018 amortization, $2) Retiree benefits paid end of year) Contribution to health care benefit fund (end of year) Discount rate, 8% Return on plan assets (actual and expected), 10% none 100 200 Required: 1. Determine the postretirement benefit...

Data pertaining to the postretirement health care benefit plan of Sterling Properties include the following for 2018: ($ in 0008) $ 136 700 Service cost Accumulated postretirement benefit obligation, January 1 Plan assets (fair value), January 1 Prior service cost-AOCI Net gain-AOCI (2018 amortization, $2) Retiree benefits paid end of year) Contribution to health care benefit fund (end of year) Discount rate, 8% Return on plan assets (actual and expected), 10% none 100 200 Required: 1. Determine the postretirement benefit...

Pension data for Barry Financial Services Inc. include the following: ($ in 0008) $ 470 Discount rate, 78 Expected return on plan assets, 116 Actual return on plan assets, 108 Service cost, 2018 January 1, 2018: Projected benefit obligation Accumulated benefit obligation Plan assets (fair value) Prior service cost-AOCI (2018 amortization, $45) Net gain-AOCI (2018 amortization, $12) There were no changes in actuarial assumptions. December 31, 2018: Cash contributions to pension fund, December 31, 2018 Benefit payments to retirees, December...

Pension data for Barry Financial Services Inc. include the following: ($ in 0008) $ 470 Discount rate, 78 Expected return on plan assets, 116 Actual return on plan assets, 108 Service cost, 2018 January 1, 2018: Projected benefit obligation Accumulated benefit obligation Plan assets (fair value) Prior service cost-AOCI (2018 amortization, $45) Net gain-AOCI (2018 amortization, $12) There were no changes in actuarial assumptions. December 31, 2018: Cash contributions to pension fund, December 31, 2018 Benefit payments to retirees, December...

Pension data for Barry Financial Services Inc. include the following: ($ in 000) $ 340 Discount rate, 78 Expected return on plan assets, 10% Actual return on plan assets, 99 Service cost, 2018 January 1, 2018: Projected benefit obligation Accumulated benefit obligation Plan assets (fair value) Prior service cost-AOCI (2018 amortization, $40) Net gain-AOCI (2018 amortization, $6) There were no changes in actuarial assumptions. December 31, 2018: Cash contributions to pension fund, December 31, 2018 Benefit payments to retirees, December...

Pension data for Barry Financial Services Inc. include the following: ($ in 000) $ 340 Discount rate, 78 Expected return on plan assets, 10% Actual return on plan assets, 99 Service cost, 2018 January 1, 2018: Projected benefit obligation Accumulated benefit obligation Plan assets (fair value) Prior service cost-AOCI (2018 amortization, $40) Net gain-AOCI (2018 amortization, $6) There were no changes in actuarial assumptions. December 31, 2018: Cash contributions to pension fund, December 31, 2018 Benefit payments to retirees, December...

Exercise 17-22 IFRS; prior service cost [LO17-7, 17-12] Lacy Construction has a noncontributory, defined benefit pension plan. At December 31, 2018. Lacy received the following information: ($ in millions) $ 749 98 Projected Benefit Obligation Balance, January 1 Service cost Prior service cost Interest cost(5%) Benefits paid Balance, December 31 50 (96) $ 829 ($ in millions) $ 610 62 Plan Assets Balance, January 1 Actual return on plan assets Contributions 2018 Benefits paid Balance, December 31 98 (96) The...

Exercise 17-22 IFRS; prior service cost [LO17-7, 17-12] Lacy Construction has a noncontributory, defined benefit pension plan. At December 31, 2018. Lacy received the following information: ($ in millions) $ 749 98 Projected Benefit Obligation Balance, January 1 Service cost Prior service cost Interest cost(5%) Benefits paid Balance, December 31 50 (96) $ 829 ($ in millions) $ 610 62 Plan Assets Balance, January 1 Actual return on plan assets Contributions 2018 Benefits paid Balance, December 31 98 (96) The...

Pension data for Barry Financial Services Inc. include the following: ($ in 000s) Discount rate, 7% Expected return on plan assets, 10% Actual return on plan assets, 9% Service cost, 2018 January 1, 2018: Projected benefit obligation Accumulated benefit obligation Plan assets (fair value) Prior service cost-A0CI (2018 amortization, $40) Net gain-A0CI (2018 amortization, $8) There were no changes in actuarial assumptions. December 31, 2018: Cash contributions to pension fund, December 31, 2018 Benefit payments to retirees, December 31, 2018...

Pension data for Barry Financial Services Inc. include the following: ($ in 000s) Discount rate, 7% Expected return on plan assets, 10% Actual return on plan assets, 9% Service cost, 2018 January 1, 2018: Projected benefit obligation Accumulated benefit obligation Plan assets (fair value) Prior service cost-A0CI (2018 amortization, $40) Net gain-A0CI (2018 amortization, $8) There were no changes in actuarial assumptions. December 31, 2018: Cash contributions to pension fund, December 31, 2018 Benefit payments to retirees, December 31, 2018...

Exercise 17-27 Postretirement benefits; components of postretirement benefit expense (LO17-11] Data pertaining to the postretirement health care benefit plan of Sterling Properties include the following for 2018: ($ in wees) $ 142 1.es 50 Service cost Accumulated postretirement benefit obligation, January 1 Plan assets (fair value), January 1 Prior service cost-AOCI Net gain-AOCI (2018 amortization, $1) Retiree benefits paid (end of year) Contribution to health care benefit fund (end of year) Discount rate, 6% Return on plan assets (actual and...

Exercise 17-27 Postretirement benefits; components of postretirement benefit expense (LO17-11] Data pertaining to the postretirement health care benefit plan of Sterling Properties include the following for 2018: ($ in wees) $ 142 1.es 50 Service cost Accumulated postretirement benefit obligation, January 1 Plan assets (fair value), January 1 Prior service cost-AOCI Net gain-AOCI (2018 amortization, $1) Retiree benefits paid (end of year) Contribution to health care benefit fund (end of year) Discount rate, 6% Return on plan assets (actual and...

Actuary and trustee reports indicate the following changes in the PBO and plan assets of Douglas-Roberts Industries during 2018: Prior service costat Jan. 1. 2018, from plan amendment at the beginning of 2015 (amortization$8 million per year) Net loss-AOCI at Jan.1, 2018 (previous losses exceeded previous gains) Average remaining service life of the active employee group Actuary's discount rate $ 40 million $118 million 10 years 5 ($ in millions) Pво Beginning of 2018 Service cost Plan Assets $ 660...

Actuary and trustee reports indicate the following changes in the PBO and plan assets of Douglas-Roberts Industries during 2018: Prior service costat Jan. 1. 2018, from plan amendment at the beginning of 2015 (amortization$8 million per year) Net loss-AOCI at Jan.1, 2018 (previous losses exceeded previous gains) Average remaining service life of the active employee group Actuary's discount rate $ 40 million $118 million 10 years 5 ($ in millions) Pво Beginning of 2018 Service cost Plan Assets $ 660...

Problem 17-8 Pension spreadsheet; record pension expense and funding; new gains and losses [LO17-7, 17-8] A partially completed pension spreadsheet showing the relationships among the elements that constitute Carney, Inc., defined benefit pension plan follows. Six years earlier. Carney revised its pension formula and recalculated benefits earned by employees in prior years using the more generous formula. The prior service cost created by the recalculation is being amortized at the rate of $4 million per year. At the end of...

Problem 17-8 Pension spreadsheet; record pension expense and funding; new gains and losses [LO17-7, 17-8] A partially completed pension spreadsheet showing the relationships among the elements that constitute Carney, Inc., defined benefit pension plan follows. Six years earlier. Carney revised its pension formula and recalculated benefits earned by employees in prior years using the more generous formula. The prior service cost created by the recalculation is being amortized at the rate of $4 million per year. At the end of...

Data pertaining to the postretirement health care benefit plan of Sterling Properties include the following for 2018: ($ in 0008) $ 136 700 Service cost Accumulated postretirement benefit obligation, January 1 Plan assets (fair value), January 1 Prior service cost-AOCI Net gain-AOCI (2018 amortization, $2) Retiree benefits paid end of year) Contribution to health care benefit fund (end of year) Discount rate, 8% Return on plan assets (actual and expected), 10% none 100 200 Required: 1. Determine the postretirement benefit...

Data pertaining to the postretirement health care benefit plan of Sterling Properties include the following for 2018: ($ in 0008) $ 136 700 Service cost Accumulated postretirement benefit obligation, January 1 Plan assets (fair value), January 1 Prior service cost-AOCI Net gain-AOCI (2018 amortization, $2) Retiree benefits paid end of year) Contribution to health care benefit fund (end of year) Discount rate, 8% Return on plan assets (actual and expected), 10% none 100 200 Required: 1. Determine the postretirement benefit...

Most questions answered within 3 hours.

-

A crate slides up a frictionless slope. At the end of 3 seconds

its velocity is...

asked 8 minutes ago -

Use the following information to answer the next seven

questions.

Suppose there are three potential states...

asked 4 minutes ago -

If we only have interstitial and substitutional diffusion, then

what do we consider the process of...

asked 20 minutes ago -

You look at yourself in a shiny 9.6-cm-diameter Christmas tree

ball.

If your face is 21.0...

asked 22 minutes ago -

If we were to measure the relaxation time of a muscle after

undergoing tetanus compared to...

asked 21 minutes ago -

4CO(g) + 8H2(g) -----> 3CH4(g) +

CO2(g) + 2H2O(l)

Use the following data as needed to...

asked 24 minutes ago -

without using map

1. Write a C++ program to find out the top 10 words in...

asked 38 minutes ago -

1)Calculate the percent ionization of a

0.330 M solution of hypochlorous

acid.

% Ionization = %...

asked 40 minutes ago -

1a) How many grams of K2SO4 are in 250mL

of 0.11 M K2SO4 solution?

_____ g...

asked 31 minutes ago -

The vapor pressure of a solution containing 38.7 g glycerin

(C3H8O3) in 146.2 g ethanol (C2H5OH)...

asked 36 minutes ago -

A physics major is cooking breakfast when he notices that the

frictional force between the steel...

asked 42 minutes ago -

A cyclohexane (c-hex) solution is prepared by fully dissolving

9.11g of a newly synthesized organic compound...

asked 48 minutes ago