What is the price of a European put option with the following parameters? s0 = $42...

What is the price of a European put option with the following parameters? s0 = $42 k = $42 r = 10% sigma = 20% T = 0.5 years (required precision 0.01 +/- 0.01) black scholes equation.PNG As a reminder, the cumulative probability function is calculated in Excel as follows: N(d1) = NORM.S.DIST(d1,TRUE) N(d2) = NORM.S.DIST(d2,TRUE) If the above equations don't load for whatever reason, here are the text versions of the equations as a back-up: c = So*N(d1) - K*e^(-rT)*N(d2) p = K*e^(-rT)*N(-d2) - So*N(-d1) d1 = [ln(So/K) + (r + 0.5*(sigma^2))*T] / [sigma * sqrt(T)] d2 = d1 - sigma*sqrt(T) To validate your equations, you may use the following information to ensure you have it coded correctly: s0 = 22 k = 25 r = 0.1 sigma = 0.2 T = 0.75 d1 = -0.2184 d2 = -0.3916 c = 1.03446 p = 2.22805

Homework Answers

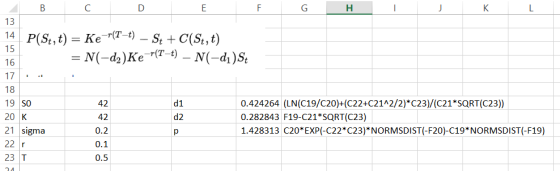

S=42,k=42,r=0.1,T=0.5,sigma=0.2

p=1.4283

Add Answer to:

What is the price of a European put option with the following

parameters? s0 = $42...

Most questions answered within 3 hours.

-

Le Terroir Winery is considering an expansion project to produce

fine wines. The trial expansion will...

asked 3 minutes ago -

The Bahraini public budget experiences deficit in the last

seven years, what are procedures are taken...

asked 11 minutes ago -

You invested $30,000 in a mutual fund at the beginning of the

year when the NAV...

asked 14 minutes ago -

Would you expect the price elasticity of supply for guitars to

be more inelastic in the...

asked 16 minutes ago -

A snowmobile is originally at the point with position vector

30.1 m at 95.0° counterclockwise from...

asked 16 minutes ago -

MAN3240 Organizational Behavior

In one to two paragraphs

6.) How can understanding emotions make me more...

asked 24 minutes ago -

Identify one individual who, in your opinion, is an excellent

leader. List the qualities that this...

asked 21 minutes ago -

For the data set shown below, complete parts (a) through (d)

below. x 3 4 5...

asked 27 minutes ago -

A university administrator working in student housing wants to

determine if the percentage of students residing...

asked 41 minutes ago -

3). Describe human population growth that has occurred in the

past 400 years. Use terms learned...

asked 38 minutes ago -

A

projectile is blue at a target. The distance from the point of

impact to the...

asked 1 hour ago -

Given a 32 bit processor, with 2 MB of physical RAM split into 512

frames. What...

asked 53 minutes ago