Homework Answers

Add Answer to:

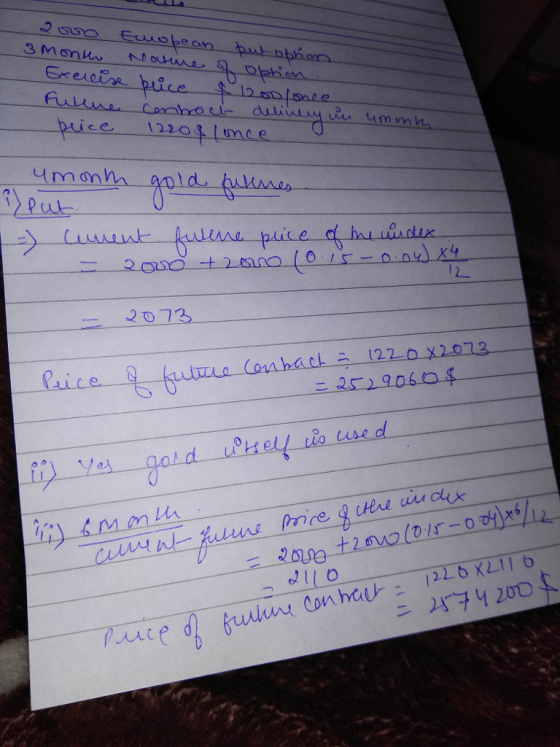

Question 5 (6 marks) A bank has written 1000 European call options and 2000 European put...

What is the delta of a short position in 600 European call options on silver futures?...

What is the delta of a short position in 600 European call options on silver futures? The options mature in 8 months and the silver futures contract matures in 9 months. The current 9 month futures price is $30.00 per ounce. The exercise price of the option is $31.00 per ounce. The risk-free interest rate is 5% per year and the volatility is 20 percent per year.

4. A trader buys a European call option and sells a European put option. The options...

4. A trader buys a European call option and sells a European put option. The options have the same underlying asset, strike price and maturity. Show that the trader's position is equivalent to a forward contract with delivery price that is equal to the strike price of the options.

4. A trader buys a European call option and sells a European put option. The options have the same underlying asset, strike price and maturity. Show that the trader's position is equivalent to a forward contract with delivery price that is equal to the strike price of the options.

1. Based on the data given, which of the following options is most likely to exhibit...

1. Based on the data given, which of the following options is

most likely to exhibit the largest gamma measure?

A. Option I

B. Option J

C. Option K

D. None of the answers

2. If Wayne uses option K contract to hedge its position and

HG’s share price subsequently dropped from $38 to $36, Wayne would

most likely need to take the following action to maintain the same

hedged position:

A. Sell options because the put delta has become...

1. Based on the data given, which of the following options is

most likely to exhibit the largest gamma measure?

A. Option I

B. Option J

C. Option K

D. None of the answers

2. If Wayne uses option K contract to hedge its position and

HG’s share price subsequently dropped from $38 to $36, Wayne would

most likely need to take the following action to maintain the same

hedged position:

A. Sell options because the put delta has become...

g) European call with a strike price of $40 costs $7. European put with the same...

g) European call with a strike price of $40 costs $7. European put with the same strike price and expiration date costs $6. Assume that you buy two calls and one put (strap strategy). Sketch the graph and write down functions of payoff and profit h) Consider a stock with a price of $50 and there is European put option on that stock with the strike of $55 and premium of $4. Assume that you buy 1/3 of a stock...

g) European call with a strike price of $40 costs $7. European put with the same strike price and expiration date costs $6. Assume that you buy two calls and one put (strap strategy). Sketch the graph and write down functions of payoff and profit h) Consider a stock with a price of $50 and there is European put option on that stock with the strike of $55 and premium of $4. Assume that you buy 1/3 of a stock...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000 1020 84.470 101.214 1050 1107 137.167 I 1) Suppose you invest in the S&P stock index for $1000, buy a 950-strike put, and sell a 1050- strike call. Draw a profit diagram for this position. What is the net option premium? 2) Here is a quote from an investment website about an investment strategy using options: One strategy investors apply is a "synthetic stock."...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000 1020 84.470 101.214 1050 1107 137.167 I 1) Suppose you invest in the S&P stock index for $1000, buy a 950-strike put, and sell a 1050- strike call. Draw a profit diagram for this position. What is the net option premium? 2) Here is a quote from an investment website about an investment strategy using options: One strategy investors apply is a "synthetic stock."...

2. (15 points) Suppose that you traded the following options on Facebook’s stock: a. Sold 1 call...

2. (15 points) Suppose that you traded the following options on Facebook’s stock: a. Sold 1 call option with an exercise price of $250 at the price of $40; b. Sold 1 put option with an exercise price of $250 at the price of $30; and c. Bought 1 call option with an exercise price of $300 at the price of $22. Also, suppose that: i. All options are European; ii. The options expire one year from now; and iii. As...

2. Consider the Black-Scholes prices of a European Futures call and put options: C(F,t) = (FN(d1f)...

2. Consider the Black-Scholes prices of a European Futures call and put options: C(F,t) = (FN(d1f) – E N(d2f))e -- (T-1), P(F,t) = (E N(-d2f) – FN(-d1f))e-r(T-1), In(F/E) + ļoʻ(T – t) _In(F/E) – } 0?(T – t) dif = a OVT-t ? 25 OVT-t. Compute and simplify these expressions for at-the-money options (where F = E). Use the identity N(-2) = 1-N2), and, since F = E, the at-the-money prices can be expressed in terms of E, t,r, o,...

2. Consider the Black-Scholes prices of a European Futures call and put options: C(F,t) = (FN(d1f) – E N(d2f))e -- (T-1), P(F,t) = (E N(-d2f) – FN(-d1f))e-r(T-1), In(F/E) + ļoʻ(T – t) _In(F/E) – } 0?(T – t) dif = a OVT-t ? 25 OVT-t. Compute and simplify these expressions for at-the-money options (where F = E). Use the identity N(-2) = 1-N2), and, since F = E, the at-the-money prices can be expressed in terms of E, t,r, o,...

A 1-year European call and put options on a non-dividend paying stock has a strike price...

A 1-year European call and put options on a non-dividend paying stock has a strike price of 80. You are given: (i) The stock’s price is currently 75. (ii) The stock’s price will be either 85 or 65 at the end of the year. (iii) The continuously compounded risk-free rate is 4.5%. (a) Determine the premium for the call. (b) Determine the premium for the put.

Question 7: Consider a European call option and a European put option on a non dividend-paying...

Question 7: Consider a European call option and a European put option on a non dividend-paying stock. The price of the stock is $100 and the strike price of both the call and the put is $103, set to expire in 1 year. Given that the price of the European call option is $10.57 and the risk-free rate is 5%, what is the price of the European put option via put-call parity? Question 8: Suppose a trader buys a call...

A European call option and put option on a stock both have a strike price of...

A European call option and put option on a stock both have a strike price of $45 and an expiration date in six months. Both sell for $2. The risk-free interest rate is 5% p.a. The current stock price is $43. There is no dividend expected for the next six months. a) If the stock price in three months is $48, which option is in the money and which one is out of the money? b) As an arbitrageur, can...

4. A trader buys a European call option and sells a European put option. The options have the same underlying asset, strike price and maturity. Show that the trader's position is equivalent to a forward contract with delivery price that is equal to the strike price of the options.

4. A trader buys a European call option and sells a European put option. The options have the same underlying asset, strike price and maturity. Show that the trader's position is equivalent to a forward contract with delivery price that is equal to the strike price of the options.

1. Based on the data given, which of the following options is

most likely to exhibit the largest gamma measure?

A. Option I

B. Option J

C. Option K

D. None of the answers

2. If Wayne uses option K contract to hedge its position and

HG’s share price subsequently dropped from $38 to $36, Wayne would

most likely need to take the following action to maintain the same

hedged position:

A. Sell options because the put delta has become...

1. Based on the data given, which of the following options is

most likely to exhibit the largest gamma measure?

A. Option I

B. Option J

C. Option K

D. None of the answers

2. If Wayne uses option K contract to hedge its position and

HG’s share price subsequently dropped from $38 to $36, Wayne would

most likely need to take the following action to maintain the same

hedged position:

A. Sell options because the put delta has become...

g) European call with a strike price of $40 costs $7. European put with the same strike price and expiration date costs $6. Assume that you buy two calls and one put (strap strategy). Sketch the graph and write down functions of payoff and profit h) Consider a stock with a price of $50 and there is European put option on that stock with the strike of $55 and premium of $4. Assume that you buy 1/3 of a stock...

g) European call with a strike price of $40 costs $7. European put with the same strike price and expiration date costs $6. Assume that you buy two calls and one put (strap strategy). Sketch the graph and write down functions of payoff and profit h) Consider a stock with a price of $50 and there is European put option on that stock with the strike of $55 and premium of $4. Assume that you buy 1/3 of a stock...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000 1020 84.470 101.214 1050 1107 137.167 I 1) Suppose you invest in the S&P stock index for $1000, buy a 950-strike put, and sell a 1050- strike call. Draw a profit diagram for this position. What is the net option premium? 2) Here is a quote from an investment website about an investment strategy using options: One strategy investors apply is a "synthetic stock."...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000 1020 84.470 101.214 1050 1107 137.167 I 1) Suppose you invest in the S&P stock index for $1000, buy a 950-strike put, and sell a 1050- strike call. Draw a profit diagram for this position. What is the net option premium? 2) Here is a quote from an investment website about an investment strategy using options: One strategy investors apply is a "synthetic stock."...

2. Consider the Black-Scholes prices of a European Futures call and put options: C(F,t) = (FN(d1f) – E N(d2f))e -- (T-1), P(F,t) = (E N(-d2f) – FN(-d1f))e-r(T-1), In(F/E) + ļoʻ(T – t) _In(F/E) – } 0?(T – t) dif = a OVT-t ? 25 OVT-t. Compute and simplify these expressions for at-the-money options (where F = E). Use the identity N(-2) = 1-N2), and, since F = E, the at-the-money prices can be expressed in terms of E, t,r, o,...

2. Consider the Black-Scholes prices of a European Futures call and put options: C(F,t) = (FN(d1f) – E N(d2f))e -- (T-1), P(F,t) = (E N(-d2f) – FN(-d1f))e-r(T-1), In(F/E) + ļoʻ(T – t) _In(F/E) – } 0?(T – t) dif = a OVT-t ? 25 OVT-t. Compute and simplify these expressions for at-the-money options (where F = E). Use the identity N(-2) = 1-N2), and, since F = E, the at-the-money prices can be expressed in terms of E, t,r, o,...

Most questions answered within 3 hours.

-

What mechanisms Drive speciation??

(I.e. what was Dawins theory on the orgin of species, and how...

asked 37 minutes ago -

The manager at a car assembly plant believes that the mean

assembly time for a car...

asked 1 hour ago -

Which of the following is true of electron capture?

A) It decreases the nuclide's mass number...

asked 3 hours ago -

Assuming an efficiency of 43.10%, calculate the actual yield of

magnesium nitrate formed from 114.9 g...

asked 3 hours ago -

The highly pathogenic bacterium Clostridium

perfringens causes gangrene, a disease that results in the

destruction of...

asked 5 hours ago -

In the context of situation analysis, which of the following is

a category for analysis in...

asked 5 hours ago -

In a study of the gas phase decomposition of sulfuryl chloride

at 600 K SO2Cl2(g)SO2(g) +...

asked 5 hours ago -

75 g of 2-propanol (C3H8O) and 25 g of pentane are mixed in a

200 mL...

asked 5 hours ago -

The 2800-turn coil in a dc motor has an area per turn of 1.1 ×

10-2...

asked 5 hours ago -

Draw a combinational logic circuit diagram with a symbol inside

the box for two I/P of...

asked 5 hours ago -

The cliché we use quite a lot in finance is: there is a need to

maximize...

asked 5 hours ago -

In class we discussed the addition of HCl to alpha pinene. Would

you expect one or...

asked 5 hours ago