Question 1: Cooley Company's stock has a beta (b) of 1.28, the risk-free rate (rRF) is...

Homework Answers

I can only answer 1 question at a time so I am solving question 1. Please do rate me and mention doubts in the comments section.

Add Answer to:

Question 1: Cooley Company's stock has a beta (b) of 1.28, the

risk-free rate (rRF) is...

Question 1: Cooley Company's stock has a beta (b) of 1.28, the risk-free rate (rRF) is...

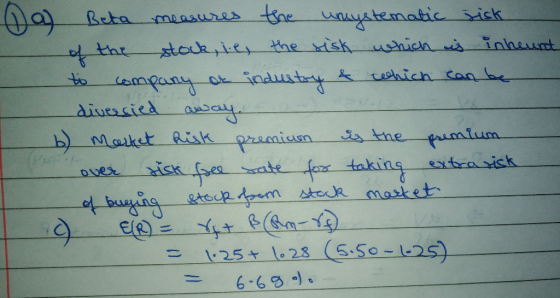

Question 1: Cooley Company's stock has a beta (b) of 1.28, the risk-free rate (rRF) is 1.25%, and the market risk premium (RPM) is 5.50%. a. What does the beta measure? Give a short answer in 1 sentence. b. What is market risk premium? Give a short answer in 1 sentence. c. Calculate the firm's required rate of return? Show the step-by-step calculation and circle your answer. (Hint: Required return = rRF + b(RPM)) Question 2: Consider the following information...

Cooley Company's stock has a beta of 0.60, the risk-free rate is 2.25%, and the market risk premium is 5.50%. What...

Cooley Company's stock has a beta of 0.60, the risk-free rate is 2.25%, and the market risk premium is 5.50%. What is the firm's required rate of return? Do not round your intermediate calculations. 5.55% 4.38% 6.60% 6.16% 4.66%

Cooley Company's stock has a beta of 0.60, the risk-free rate is 2.25%, and the market risk premium is 5.50%. What is the firm's required rate of return? Do not round your intermediate calculations. 5.55% 4.38% 6.60% 6.16% 4.66%

Elba Eateries' stock has a beta of 0.70. Assume that the risk-free rate, rRF, is 5.5%...

Elba Eateries' stock has a beta of 0.70. Assume that the risk-free rate, rRF, is 5.5% and the market risk premium, (rM – rRF), equals 4%. Compute the required rate of return for Elba Eateries. Respond in percentage form without the percent sign and round to the second decimal place

Question 12 Which of the following statements about Security Market Line (SML) equation “ri = rRF...

Question 12 Which of the following statements about Security Market Line (SML) equation “ri = rRF + (rM – rRF)bi = rRF + (RPM)bi” is NOT true? ri is the required rate of return for stock i. rRF is the real risk-free rate. rM is the required rate of return on a portfolio consisting of all stocks, which is called the market portfolio. RPM is the risk premium on market portfolio. It equals to rM - rRF.

Stock A has a beta of 0.8 and Stock B has a beta of 1.2. 50%...

Stock A has a beta of 0.8 and Stock B has a beta of 1.2. 50% of Portfolio P is invested in Stock A and 50% is invested in Stock B. If the market risk premium (r M − rRF) were to increase but the risk-free rate (r RF) remained constant, which of the following would occur? a. The required return would increase for Stock B but decrease for Stock A. b. The required return would increase for Stock A...

ABC Company's stock has a beta of 1.95, the risk-free rate is 2.25%, and the market risk premium is 6.75%. What is A...

ABC Company's stock has a beta of 1.95, the risk-free rate is 2.25%, and the market risk premium is 6.75%. What is ABC's required rate of return using CAPM? Enter your answer rounded to two decimal places. Do not enter % in the answer box. For example, if your answer is 0.12345 or 12.345% then enter as 12.35 in the answer box. Ripken Iron Works believes the following probability distribution exists for its stock. What is the standard deviation of...

If the current risk-free rate is 6%; Stock A has a beta of 1.0; Stock B...

If the current risk-free rate is 6%; Stock A has a beta of 1.0; Stock B has a beta of 2.0; and the market risk premium, r M – r RF, is positive. Which of the following statements is CORRECT? a. If the risk-free rate increases but the market risk premium stays unchanged, Stock B's required return will increase by more than Stock A's. b. If Stock B's required return is 11%, then the market risk premium is 2.5%. c....

CAPM, portfolio risk, and return Consider the following information for three stocks, Stocks A, B, and...

CAPM, portfolio risk, and return Consider the following information for three stocks, Stocks A, B, and C. The returns on the three stocks are positively correlated, but they are not perfectly correlated. (That is, each of the correlation coefficients is between 0 and 1.) Stock Expected Return Standard Deviation Beta A 9.87 % 14 % 0.9 B 11.16 14 1.2 C 12.88 14 1.6 Fund P has one-third of its funds invested in each of the three stocks. The risk-free...

Problem 8-13 CAPM, portfolio risk, and return Consider the following information for three stocks, Stocks A, B, and C. T...

Problem 8-13 CAPM, portfolio risk, and return Consider the following information for three stocks, Stocks A, B, and C. The returns on the three stocks are positively correlated, but they are not perfectly correlated. (That is, each of the correlation coefficients is between 0 and 1.) Stock Expected Return Standard Deviation Beta A 8.30 % 16 % 0.7 B 9.90 16 1.1 C 12.30 16 1.7 Fund P has one-third of its funds invested in each of the three stocks....

Sheridan Industries common stock has a beta of 1.2. If the market risk-free rate is 5.2...

Sheridan Industries common stock has a beta of 1.2. If the

market risk-free rate is 5.2 percent and the expected return on the

market is 8.2 percent, what is Sheridan’s cost of common stock?

I solved this problem incorrectly by doing

Kes=Rrf+(Betaesx market risk

premium)

Kes=0.052+(1.2x0.082)

Kes=0.052+0.098400

Kes=0.1504=15.0%

I'm not sure what I am doing wrong. Please show full

calculation.

X Your answer is incorrect. Sheridan Industries common stock has a beta of 1.2. If the market risk-free rate is...

Sheridan Industries common stock has a beta of 1.2. If the

market risk-free rate is 5.2 percent and the expected return on the

market is 8.2 percent, what is Sheridan’s cost of common stock?

I solved this problem incorrectly by doing

Kes=Rrf+(Betaesx market risk

premium)

Kes=0.052+(1.2x0.082)

Kes=0.052+0.098400

Kes=0.1504=15.0%

I'm not sure what I am doing wrong. Please show full

calculation.

X Your answer is incorrect. Sheridan Industries common stock has a beta of 1.2. If the market risk-free rate is...

Cooley Company's stock has a beta of 0.60, the risk-free rate is 2.25%, and the market risk premium is 5.50%. What is the firm's required rate of return? Do not round your intermediate calculations. 5.55% 4.38% 6.60% 6.16% 4.66%

Cooley Company's stock has a beta of 0.60, the risk-free rate is 2.25%, and the market risk premium is 5.50%. What is the firm's required rate of return? Do not round your intermediate calculations. 5.55% 4.38% 6.60% 6.16% 4.66%

Sheridan Industries common stock has a beta of 1.2. If the

market risk-free rate is 5.2 percent and the expected return on the

market is 8.2 percent, what is Sheridan’s cost of common stock?

I solved this problem incorrectly by doing

Kes=Rrf+(Betaesx market risk

premium)

Kes=0.052+(1.2x0.082)

Kes=0.052+0.098400

Kes=0.1504=15.0%

I'm not sure what I am doing wrong. Please show full

calculation.

X Your answer is incorrect. Sheridan Industries common stock has a beta of 1.2. If the market risk-free rate is...

Sheridan Industries common stock has a beta of 1.2. If the

market risk-free rate is 5.2 percent and the expected return on the

market is 8.2 percent, what is Sheridan’s cost of common stock?

I solved this problem incorrectly by doing

Kes=Rrf+(Betaesx market risk

premium)

Kes=0.052+(1.2x0.082)

Kes=0.052+0.098400

Kes=0.1504=15.0%

I'm not sure what I am doing wrong. Please show full

calculation.

X Your answer is incorrect. Sheridan Industries common stock has a beta of 1.2. If the market risk-free rate is...

Most questions answered within 3 hours.

-

Assuming the following has been encrypted with a Vigenere cipher

below, use the method(s) and assumptions...

asked 17 minutes ago -

How would I use switch statements to write a program that will

take an input of...

asked 8 minutes ago -

Imagine a reaction in which methane gas combusts at a constant

pressure of 1 atm and...

asked 18 minutes ago -

Two parallel wires (each 12 m in length) are separated by a

distance of 0.065 m...

asked 16 minutes ago -

Suppose there were three masses at the corner of uniform

equilateral triangle. The masses are m1...

asked 18 minutes ago -

Situation: A building that is 618 m above the ground floor. How

many times would a...

asked 22 minutes ago -

help me and discuss one successful and one

unsuccessful international company/busines in Indonesia.whyit

succeed and why...

asked 29 minutes ago -

I- Choose the best answer

Which of the following statements about the structure and

packaging of...

asked 30 minutes ago -

1. A sample of 144 incoming freshman found that 45 of them

scored more than 550...

asked 37 minutes ago -

Kc is 2.35 × 1018 at 25 °C for the formation of iron(III)

oxalate complex ion....

asked 38 minutes ago -

Team Values – Discuss as a team what values are important.

Develop a statement or itemised...

asked 50 minutes ago -

C# Visual Studio -The local driver's license

office has asked you to create an application that...

asked 55 minutes ago