Homework Answers

9)

Answer : (e)

Penetrative pricing is followed to attract the buyers quickly towards the new products. It is temporary pricing strategy.

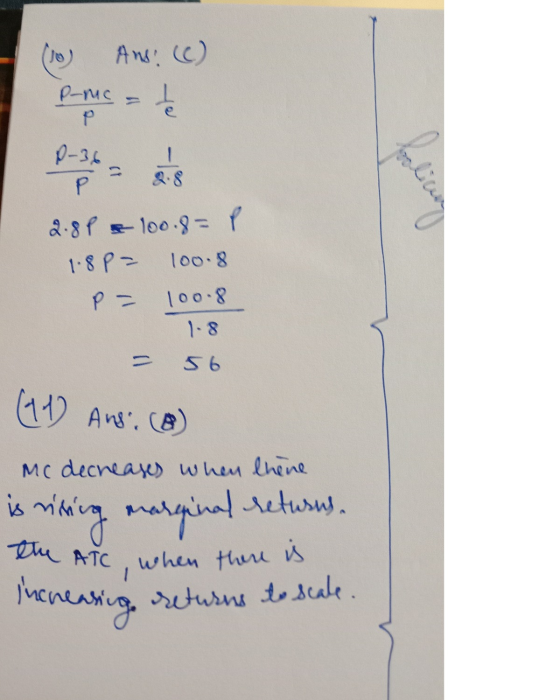

10)

Add Answer to:

Question 9 1 pts Which of the following is correct regarding penetration pricing? There is more...

Which of the following is correct regarding penetration pricing? There is more than one answer to...

Which of the following is correct regarding penetration pricing? There is more than one answer to this question. You must mark all of the answers to receive full credit for this question. It is a temporary pricing strategy intended to quickly attract consumers to a firm. It is a strategy that is commonly found among perfectly competitive firms. It is used by firms to overcome network effects of well- established firms. It is used by firms with a long history...

Which of the following is correct regarding penetration pricing? There is more than one answer to this question. You must mark all of the answers to receive full credit for this question. It is a temporary pricing strategy intended to quickly attract consumers to a firm. It is a strategy that is commonly found among perfectly competitive firms. It is used by firms to overcome network effects of well- established firms. It is used by firms with a long history...

1. Which of the following correctly summarizes the strategy used by firms that employ third-degree price...

1. Which of the following correctly summarizes the strategy used by firms that employ third-degree price discrimination? Group of answer choices a.The firm’s marginal revenue will be lower in the market with the more elastic demand. b.The firm sets the price higher in the market with the more elastic demand. c.The firm sets the price lower in the market with the more inelastic demand. d.The firm’s marginal revenue will be higher in the market with the more elastic demand. e.None...

.Question Completion Status QUESTION 11 Suppose a firm doubles its employment of all inptuts in the long run. If th...

.Question Completion Status QUESTION 11 Suppose a firm doubles its employment of all inptuts in the long run. If this action more than doubles the amount of capital produced, then this firm is experiencing O Increasing returns to scale diminishing marginal returns o technological progress O positive marginal revenue QUESTION 12 When input prices are fixed, decreasing returns to scale implies that the long run average cost curve is downward sloping O horizontal upward sloping O Ushaped QUESTION 13 If...

.Question Completion Status QUESTION 11 Suppose a firm doubles its employment of all inptuts in the long run. If this action more than doubles the amount of capital produced, then this firm is experiencing O Increasing returns to scale diminishing marginal returns o technological progress O positive marginal revenue QUESTION 12 When input prices are fixed, decreasing returns to scale implies that the long run average cost curve is downward sloping O horizontal upward sloping O Ushaped QUESTION 13 If...

Which of the following statements is correct regarding the Sweezy model of oligopoly? Competitors match price...

Which of the following statements is correct regarding the Sweezy model of oligopoly? Competitors match price increases but do not match price decreases. The flatter portion of the demand curve corresponds to the quantity range where competitors match price changes. The firm faces more elastic demand when it lowers its price than when it raises its price. None of the statements listed is correct. The marginal revenue curve of the firm is horizontal. Question 22 1 pts Assume that the...

Which of the following statements is correct regarding the Sweezy model of oligopoly? Competitors match price increases but do not match price decreases. The flatter portion of the demand curve corresponds to the quantity range where competitors match price changes. The firm faces more elastic demand when it lowers its price than when it raises its price. None of the statements listed is correct. The marginal revenue curve of the firm is horizontal. Question 22 1 pts Assume that the...

These two question please Question 8 (1 point) When do constant returns to scale occur? when...

These two question please

Question 8 (1 point) When do constant returns to scale occur? when long-run total costs are constant as output increases when long-run average total costs are constant as output increases when the firm's long-run average-cost curve is falling as output increases when the firm's long-run average-cost curve is rising as output increases Figure 13-4 The curves in this figure reflect information about the average total cost, average fixed cost, average variable cost, and marginal cost for...

These two question please

Question 8 (1 point) When do constant returns to scale occur? when long-run total costs are constant as output increases when long-run average total costs are constant as output increases when the firm's long-run average-cost curve is falling as output increases when the firm's long-run average-cost curve is rising as output increases Figure 13-4 The curves in this figure reflect information about the average total cost, average fixed cost, average variable cost, and marginal cost for...

(Click to select) economies of scale a. Long-run average total cost falls as the firm realize: rises when the firm...

(Click to select) economies of scale a. Long-run average total cost falls as the firm realize: rises when the firm experiences [ (Click to select) diseconomies of scale diminishing marginal returns increasing marginal returns b. The minimum efficient scale is the level of output produced by the smallest firm in the industry. smallest level of output at which a firm can produce. only level of output where long-run average total costs are minimized. smallest level of output needed to attain...

(Click to select) economies of scale a. Long-run average total cost falls as the firm realize: rises when the firm experiences [ (Click to select) diseconomies of scale diminishing marginal returns increasing marginal returns b. The minimum efficient scale is the level of output produced by the smallest firm in the industry. smallest level of output at which a firm can produce. only level of output where long-run average total costs are minimized. smallest level of output needed to attain...

Question 13 1 pts Capital 2 5 10 Labeth Figure 6.4.2 Refer to Figure 6.4.2 above....

Question 13 1 pts Capital 2 5 10 Labeth Figure 6.4.2 Refer to Figure 6.4.2 above. The situation pictured in Figure 6.4.2: is one of increasing marginal returns to capital. is one of increasing marginal returns to labor. contradicts the law of diminishing marginal product. shows decreasing returns to scale. is consistent with diminishing marginal product.

Question 13 1 pts Capital 2 5 10 Labeth Figure 6.4.2 Refer to Figure 6.4.2 above. The situation pictured in Figure 6.4.2: is one of increasing marginal returns to capital. is one of increasing marginal returns to labor. contradicts the law of diminishing marginal product. shows decreasing returns to scale. is consistent with diminishing marginal product.

Question 24 6 pts Clearly type out your answer to parts (A), (B) and (C) in...

Question 24 6 pts Clearly type out your answer to parts (A), (B) and (C) in the space provided. Retain all of your handwritten work for this question to be uploaded separately after you have completed the exam. Given the following long run production and cost functions: 9 = 1362 C = 15L +3K (A) What input has diminishing marginal returns? (B) Does this production function display increasing, decreasing or constant returns to scale? (C) What is this firm's expansion...

Question 24 6 pts Clearly type out your answer to parts (A), (B) and (C) in the space provided. Retain all of your handwritten work for this question to be uploaded separately after you have completed the exam. Given the following long run production and cost functions: 9 = 1362 C = 15L +3K (A) What input has diminishing marginal returns? (B) Does this production function display increasing, decreasing or constant returns to scale? (C) What is this firm's expansion...

Please show as much work and explanation as possible, thank you so much! 10. Which ones of the following statements are...

Please show as much work and explanation as

possible, thank you so much!

10. Which ones of the following statements are true about perfectly competitive markets? (a) The short run supply curve for a firm is upward sloping due to the law of diminishing returns. (b) The industry's short run supply curve is upward sloping due to the law of diminishing returns. (c) The slope of the long run supply curve for an individual firm depends on the industry cost...

Please show as much work and explanation as

possible, thank you so much!

10. Which ones of the following statements are true about perfectly competitive markets? (a) The short run supply curve for a firm is upward sloping due to the law of diminishing returns. (b) The industry's short run supply curve is upward sloping due to the law of diminishing returns. (c) The slope of the long run supply curve for an individual firm depends on the industry cost...

Given the following long run production and cost functions: q=LPK1/4 C = 12L +4K (A) What...

Given the following long run production and cost functions: q=LPK1/4 C = 12L +4K (A) What input has diminishing marginal returns? (B) Does this production function display increasing, decreasing or constant returns to scale? (C) What is this firm's expansion path assuming input prices do not change? Clearly type out your answer to parts (A), (B) and (C) in the space provided. Retain all of your handwritten work for this question to be uploaded separately after you have completed the...

Given the following long run production and cost functions: q=LPK1/4 C = 12L +4K (A) What input has diminishing marginal returns? (B) Does this production function display increasing, decreasing or constant returns to scale? (C) What is this firm's expansion path assuming input prices do not change? Clearly type out your answer to parts (A), (B) and (C) in the space provided. Retain all of your handwritten work for this question to be uploaded separately after you have completed the...

Which of the following is correct regarding penetration pricing? There is more than one answer to this question. You must mark all of the answers to receive full credit for this question. It is a temporary pricing strategy intended to quickly attract consumers to a firm. It is a strategy that is commonly found among perfectly competitive firms. It is used by firms to overcome network effects of well- established firms. It is used by firms with a long history...

Which of the following is correct regarding penetration pricing? There is more than one answer to this question. You must mark all of the answers to receive full credit for this question. It is a temporary pricing strategy intended to quickly attract consumers to a firm. It is a strategy that is commonly found among perfectly competitive firms. It is used by firms to overcome network effects of well- established firms. It is used by firms with a long history...

.Question Completion Status QUESTION 11 Suppose a firm doubles its employment of all inptuts in the long run. If this action more than doubles the amount of capital produced, then this firm is experiencing O Increasing returns to scale diminishing marginal returns o technological progress O positive marginal revenue QUESTION 12 When input prices are fixed, decreasing returns to scale implies that the long run average cost curve is downward sloping O horizontal upward sloping O Ushaped QUESTION 13 If...

.Question Completion Status QUESTION 11 Suppose a firm doubles its employment of all inptuts in the long run. If this action more than doubles the amount of capital produced, then this firm is experiencing O Increasing returns to scale diminishing marginal returns o technological progress O positive marginal revenue QUESTION 12 When input prices are fixed, decreasing returns to scale implies that the long run average cost curve is downward sloping O horizontal upward sloping O Ushaped QUESTION 13 If...

Which of the following statements is correct regarding the Sweezy model of oligopoly? Competitors match price increases but do not match price decreases. The flatter portion of the demand curve corresponds to the quantity range where competitors match price changes. The firm faces more elastic demand when it lowers its price than when it raises its price. None of the statements listed is correct. The marginal revenue curve of the firm is horizontal. Question 22 1 pts Assume that the...

Which of the following statements is correct regarding the Sweezy model of oligopoly? Competitors match price increases but do not match price decreases. The flatter portion of the demand curve corresponds to the quantity range where competitors match price changes. The firm faces more elastic demand when it lowers its price than when it raises its price. None of the statements listed is correct. The marginal revenue curve of the firm is horizontal. Question 22 1 pts Assume that the...

These two question please

Question 8 (1 point) When do constant returns to scale occur? when long-run total costs are constant as output increases when long-run average total costs are constant as output increases when the firm's long-run average-cost curve is falling as output increases when the firm's long-run average-cost curve is rising as output increases Figure 13-4 The curves in this figure reflect information about the average total cost, average fixed cost, average variable cost, and marginal cost for...

These two question please

Question 8 (1 point) When do constant returns to scale occur? when long-run total costs are constant as output increases when long-run average total costs are constant as output increases when the firm's long-run average-cost curve is falling as output increases when the firm's long-run average-cost curve is rising as output increases Figure 13-4 The curves in this figure reflect information about the average total cost, average fixed cost, average variable cost, and marginal cost for...

(Click to select) economies of scale a. Long-run average total cost falls as the firm realize: rises when the firm experiences [ (Click to select) diseconomies of scale diminishing marginal returns increasing marginal returns b. The minimum efficient scale is the level of output produced by the smallest firm in the industry. smallest level of output at which a firm can produce. only level of output where long-run average total costs are minimized. smallest level of output needed to attain...

(Click to select) economies of scale a. Long-run average total cost falls as the firm realize: rises when the firm experiences [ (Click to select) diseconomies of scale diminishing marginal returns increasing marginal returns b. The minimum efficient scale is the level of output produced by the smallest firm in the industry. smallest level of output at which a firm can produce. only level of output where long-run average total costs are minimized. smallest level of output needed to attain...

Question 13 1 pts Capital 2 5 10 Labeth Figure 6.4.2 Refer to Figure 6.4.2 above. The situation pictured in Figure 6.4.2: is one of increasing marginal returns to capital. is one of increasing marginal returns to labor. contradicts the law of diminishing marginal product. shows decreasing returns to scale. is consistent with diminishing marginal product.

Question 13 1 pts Capital 2 5 10 Labeth Figure 6.4.2 Refer to Figure 6.4.2 above. The situation pictured in Figure 6.4.2: is one of increasing marginal returns to capital. is one of increasing marginal returns to labor. contradicts the law of diminishing marginal product. shows decreasing returns to scale. is consistent with diminishing marginal product.

Question 24 6 pts Clearly type out your answer to parts (A), (B) and (C) in the space provided. Retain all of your handwritten work for this question to be uploaded separately after you have completed the exam. Given the following long run production and cost functions: 9 = 1362 C = 15L +3K (A) What input has diminishing marginal returns? (B) Does this production function display increasing, decreasing or constant returns to scale? (C) What is this firm's expansion...

Question 24 6 pts Clearly type out your answer to parts (A), (B) and (C) in the space provided. Retain all of your handwritten work for this question to be uploaded separately after you have completed the exam. Given the following long run production and cost functions: 9 = 1362 C = 15L +3K (A) What input has diminishing marginal returns? (B) Does this production function display increasing, decreasing or constant returns to scale? (C) What is this firm's expansion...

Please show as much work and explanation as

possible, thank you so much!

10. Which ones of the following statements are true about perfectly competitive markets? (a) The short run supply curve for a firm is upward sloping due to the law of diminishing returns. (b) The industry's short run supply curve is upward sloping due to the law of diminishing returns. (c) The slope of the long run supply curve for an individual firm depends on the industry cost...

Please show as much work and explanation as

possible, thank you so much!

10. Which ones of the following statements are true about perfectly competitive markets? (a) The short run supply curve for a firm is upward sloping due to the law of diminishing returns. (b) The industry's short run supply curve is upward sloping due to the law of diminishing returns. (c) The slope of the long run supply curve for an individual firm depends on the industry cost...

Given the following long run production and cost functions: q=LPK1/4 C = 12L +4K (A) What input has diminishing marginal returns? (B) Does this production function display increasing, decreasing or constant returns to scale? (C) What is this firm's expansion path assuming input prices do not change? Clearly type out your answer to parts (A), (B) and (C) in the space provided. Retain all of your handwritten work for this question to be uploaded separately after you have completed the...

Given the following long run production and cost functions: q=LPK1/4 C = 12L +4K (A) What input has diminishing marginal returns? (B) Does this production function display increasing, decreasing or constant returns to scale? (C) What is this firm's expansion path assuming input prices do not change? Clearly type out your answer to parts (A), (B) and (C) in the space provided. Retain all of your handwritten work for this question to be uploaded separately after you have completed the...

Most questions answered within 3 hours.

-

Engineers must consider the breadths of male heads when

designing helmets. The company researchers have determined...

asked 27 minutes ago -

In the Williamson Ether Synthesis of Phenacetin from

Acetaminophen, sodium methoxide in methanol and 100% ethanol...

asked 32 minutes ago -

If the spin of the earth suddenly changed to spin in the

opposite direction, what effect...

asked 46 minutes ago -

An orb weaver spider with a mass of 0.23 grams hangs vertically

by one of its...

asked 42 minutes ago -

Determine the sample size required to estimate the mean score on

a standardized test within

2...

asked 1 hour ago -

The idea that one can remain relatively 'anonymous' on the

internet if they so choose, for...

asked 51 minutes ago -

In the reaction of N2 and H2 to produce

NH3, how many moles of H2 will...

asked 52 minutes ago -

When a certain coin is flipped, the probability of

obtaining a tails is 0.55. Which of...

asked 49 minutes ago -

Can you show how a sulfonic acid group

is introduced into an aromatic ring by Friedal...

asked 55 minutes ago -

Implement the Smith-Waterman algorithm in C that accepts a

substitution matrix.

You may assume the substitution...

asked 55 minutes ago -

The equilibrium constant Kp for the reaction

C(s)+H2O(g)⇌CO(g)+H2(g) is 2.44 at 1000 K. What are the...

asked 1 hour ago -

HACKING

1: Discuss the tricks of hacking in 300 words.

2: Explain in you own words...

asked 1 hour ago