Suppose an industry is composed of 50 price-taking firms, each one possessing the cost structure given...

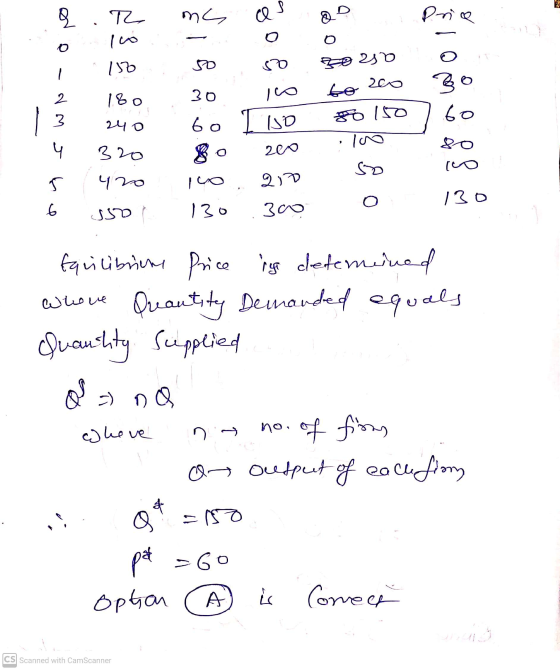

Suppose an industry is composed of 50 price-taking firms, each one possessing the cost structure given below:

| Quantity | 0 | 1 | 2 | 3 | 4 | 5 | 6 |

| Total Cost | 100 | 150 | 180 | 240 | 320 | 420 | 550 |

Also assume the market demand curve contains the following points:

| Quantity Demanded | 250 | 200 | 150 | 100 | 50 | 0 |

| Price | 0 | 30 | 60 | 80 | 100 | 130 |

What is the equilibrium price in this market?

Group of answer choices

a P = 60

b P = 100

c P = 80

d P = 30

e P = 130

Homework Answers

Add Answer to:

Suppose an industry is composed of 50 price-taking firms, each

one possessing the cost structure given...

A perfectly competitive industry is composed of 1000 identical firms with cost structure: TCVC FC AVC...

A perfectly competitive industry is composed of 1000 identical firms with cost structure: TCVC FC AVC ATC MC 40 10 80 20 100 30 140 40 200 280 60 380 a) Complete the preceding Table. b) Assuming that the market price is p = 8, what are the quantity produced by each firm and the profit it makes?

A perfectly competitive industry is composed of 1000 identical firms with cost structure: TCVC FC AVC ATC MC 40 10 80 20 100 30 140 40 200 280 60 380 a) Complete the preceding Table. b) Assuming that the market price is p = 8, what are the quantity produced by each firm and the profit it makes?

1) Given the following cost information for a price-taking firm, what is the maximum amount of...

1) Given the following cost information for a price-taking firm, what is the maximum amount of profit that can be earned if the price is $60? Quantity 0 1 2 3 4 5 6 Total Cost 50 100 130 150 190 250 330 Group of answer choices a $300 b $40 c $30 d $50 2) Given the following cost information for a price-taking firm, what is the profit-maximizing quantity given a market price of $40? Quantity 0 1...

Suppose there are 100 firms in a perfectly competitive (price-taking) market and they each individually have...

Suppose there are 100 firms in a perfectly competitive (price-taking) market and they each individually have the following average total costs: Quantity 0 1 2 3 4 5 6 ATC - 200 140 110 105 104 110 If the market equilibrium quantity is 400 units, what is the market equilibrium price? Group of answer choices a $420 b $90 c $120 d $105

please answer ASAP please help A perfectly competitive industry is composed of 100 identical firms with...

please answer ASAP

please help

A perfectly competitive industry is composed of 100 identical firms with cost structure: TCVC FC AVC ATC MC a) Complete the preceding Table. b) Assuming that the market price is p-8, what are the quantity produced by each firm and the profit it makes? c) Suppose that the market demand schedule is as follows: P QD 0 700 2 650 4 600 6 550 500 10 450 is the price p = 8 a short-run...

please answer ASAP

please help

A perfectly competitive industry is composed of 100 identical firms with cost structure: TCVC FC AVC ATC MC a) Complete the preceding Table. b) Assuming that the market price is p-8, what are the quantity produced by each firm and the profit it makes? c) Suppose that the market demand schedule is as follows: P QD 0 700 2 650 4 600 6 550 500 10 450 is the price p = 8 a short-run...

1) A price-taking firm sells 2,000 units at a price of $7 each. If their AFC...

1) A price-taking firm sells 2,000 units at a price of $7 each. If their AFC = $5 and their AVC = $3, how much profit will it make? Group of answer choices a profit = -2,000 b profit = 14,000 c profit = 4,000 d None of these answers e profit = 8,000 2) Assume there are 50 identical firms in a perfectly competitive (price-taking) market. Assume EACH firm has the cost structure given below. Quantity 0 1 2...

1) Suppose a perfectly competitive (price-taking) market is made up of 100 identical firms. Each firm...

1) Suppose a perfectly competitive (price-taking) market is made up of 100 identical firms. Each firm individually has the following costs: Quantity 0 1 2 3 4 5 6 Total Cost 10 16 20 27 36 46 58 Also assume the market demand curve is: Q Demanded 600 500 400 300 200 100 0 Price 4 7 9 10 12 15 20 What is the equilibrium price in this market? Group of answer choices a $12 b $9...

Box 1 Options: (Price takers) (Monopolistically Competitive firms) (price makers) Box 2 Options: (Supply) (Demand) (Aver...

Box 1 Options: (Price takers)

(Monopolistically Competitive firms) (price makers)

Box 2 Options: (Supply) (Demand) (Average total cost)

Consider Kellogg's production and price choices in the breakfast cereal industry when it is characterized by the price leadership model price makers Therefore, the horizontal Under this theory of oligopoly, all firms other than the dominant firm act as sum of their marginal cost curves is their curve The following graph shows the market demand curve and the horizontal sum of the...

Box 1 Options: (Price takers)

(Monopolistically Competitive firms) (price makers)

Box 2 Options: (Supply) (Demand) (Average total cost)

Consider Kellogg's production and price choices in the breakfast cereal industry when it is characterized by the price leadership model price makers Therefore, the horizontal Under this theory of oligopoly, all firms other than the dominant firm act as sum of their marginal cost curves is their curve The following graph shows the market demand curve and the horizontal sum of the...

1) Given the following cost information for a price-taking firm, what is the profit-maximizing quantity given...

1) Given the following cost information for a price-taking firm, what is the profit-maximizing quantity given a market price of $80. Quantity 0 1 2 3 4 5 6 7 8 Total Cost 100 200 250 280 300 340 400 480 600 Group of answer choices a Q = 0 b Q = 7 c Q = 5 d Q = 3 2) Suppose a price-taking firm has the following costs: Quantity 0 1 2 3 4 5 6...

ATC Demand MC Cost of Webcam BARABARBERBESAR BRAS Price of Webcam $80 $72 $64 $56 $48...

ATC Demand MC Cost of Webcam BARABARBERBESAR BRAS Price of Webcam $80 $72 $64 $56 $48 $40 $32 E $24 $16 $8 $0 0 50 100 150 200 250 300 350 400 450 500 550 600 650 700 Quantity of Webcams AVC Supply 2 8 9 10 4 5 Quantity of Webcams Assume the perfectly competitive webcam industry in this question is made up of identical firms. The graph on the left shows the costs of producing webcams at one...

ATC Demand MC Cost of Webcam BARABARBERBESAR BRAS Price of Webcam $80 $72 $64 $56 $48 $40 $32 E $24 $16 $8 $0 0 50 100 150 200 250 300 350 400 450 500 550 600 650 700 Quantity of Webcams AVC Supply 2 8 9 10 4 5 Quantity of Webcams Assume the perfectly competitive webcam industry in this question is made up of identical firms. The graph on the left shows the costs of producing webcams at one...

Question 27 A perfectly competitive industry is composed of 100 firms. Each firm has an identical...

Question 27 A perfectly competitive industry is composed of 100 firms. Each firm has an identical short-run marginal cost function SMC = 5+10q (where q is the firm's level of output). If Q denotes industry output, what is the short-run market supply curve for output? a) Q = -50 + 10p if p > 5 and 0 if p 5 5 α Q = -5 + TOP p if p > 5 and 0 if p < 5 + α...

Question 27 A perfectly competitive industry is composed of 100 firms. Each firm has an identical short-run marginal cost function SMC = 5+10q (where q is the firm's level of output). If Q denotes industry output, what is the short-run market supply curve for output? a) Q = -50 + 10p if p > 5 and 0 if p 5 5 α Q = -5 + TOP p if p > 5 and 0 if p < 5 + α...

A perfectly competitive industry is composed of 1000 identical firms with cost structure: TCVC FC AVC ATC MC 40 10 80 20 100 30 140 40 200 280 60 380 a) Complete the preceding Table. b) Assuming that the market price is p = 8, what are the quantity produced by each firm and the profit it makes?

A perfectly competitive industry is composed of 1000 identical firms with cost structure: TCVC FC AVC ATC MC 40 10 80 20 100 30 140 40 200 280 60 380 a) Complete the preceding Table. b) Assuming that the market price is p = 8, what are the quantity produced by each firm and the profit it makes?

please answer ASAP

please help

A perfectly competitive industry is composed of 100 identical firms with cost structure: TCVC FC AVC ATC MC a) Complete the preceding Table. b) Assuming that the market price is p-8, what are the quantity produced by each firm and the profit it makes? c) Suppose that the market demand schedule is as follows: P QD 0 700 2 650 4 600 6 550 500 10 450 is the price p = 8 a short-run...

please answer ASAP

please help

A perfectly competitive industry is composed of 100 identical firms with cost structure: TCVC FC AVC ATC MC a) Complete the preceding Table. b) Assuming that the market price is p-8, what are the quantity produced by each firm and the profit it makes? c) Suppose that the market demand schedule is as follows: P QD 0 700 2 650 4 600 6 550 500 10 450 is the price p = 8 a short-run...

Box 1 Options: (Price takers)

(Monopolistically Competitive firms) (price makers)

Box 2 Options: (Supply) (Demand) (Average total cost)

Consider Kellogg's production and price choices in the breakfast cereal industry when it is characterized by the price leadership model price makers Therefore, the horizontal Under this theory of oligopoly, all firms other than the dominant firm act as sum of their marginal cost curves is their curve The following graph shows the market demand curve and the horizontal sum of the...

Box 1 Options: (Price takers)

(Monopolistically Competitive firms) (price makers)

Box 2 Options: (Supply) (Demand) (Average total cost)

Consider Kellogg's production and price choices in the breakfast cereal industry when it is characterized by the price leadership model price makers Therefore, the horizontal Under this theory of oligopoly, all firms other than the dominant firm act as sum of their marginal cost curves is their curve The following graph shows the market demand curve and the horizontal sum of the...

ATC Demand MC Cost of Webcam BARABARBERBESAR BRAS Price of Webcam $80 $72 $64 $56 $48 $40 $32 E $24 $16 $8 $0 0 50 100 150 200 250 300 350 400 450 500 550 600 650 700 Quantity of Webcams AVC Supply 2 8 9 10 4 5 Quantity of Webcams Assume the perfectly competitive webcam industry in this question is made up of identical firms. The graph on the left shows the costs of producing webcams at one...

ATC Demand MC Cost of Webcam BARABARBERBESAR BRAS Price of Webcam $80 $72 $64 $56 $48 $40 $32 E $24 $16 $8 $0 0 50 100 150 200 250 300 350 400 450 500 550 600 650 700 Quantity of Webcams AVC Supply 2 8 9 10 4 5 Quantity of Webcams Assume the perfectly competitive webcam industry in this question is made up of identical firms. The graph on the left shows the costs of producing webcams at one...

Question 27 A perfectly competitive industry is composed of 100 firms. Each firm has an identical short-run marginal cost function SMC = 5+10q (where q is the firm's level of output). If Q denotes industry output, what is the short-run market supply curve for output? a) Q = -50 + 10p if p > 5 and 0 if p 5 5 α Q = -5 + TOP p if p > 5 and 0 if p < 5 + α...

Question 27 A perfectly competitive industry is composed of 100 firms. Each firm has an identical short-run marginal cost function SMC = 5+10q (where q is the firm's level of output). If Q denotes industry output, what is the short-run market supply curve for output? a) Q = -50 + 10p if p > 5 and 0 if p 5 5 α Q = -5 + TOP p if p > 5 and 0 if p < 5 + α...

Most questions answered within 3 hours.

-

A college student is employed as a door-to-door newspaper

salesman. Historical data suggests that the student...

asked 31 minutes ago -

MATLAB HW 11 problem using Switch Case and Input commands

Write a script file that calculates...

asked 16 minutes ago -

Considering gravitational time dilation, calculate the time that

passes in Earth’s surface while 1 hour passes...

asked 55 minutes ago -

Minitab Problem: Take the Lake Hume June rainfall data and find

use the processes outlined in...

asked 1 hour ago -

X Company is trying to decide whether to continue using old

equipment to make Product A...

asked 1 hour ago -

IN PYTHON ONLY !! Program 2: Re-work

program #5 (WeeklyHours) from the previous assignment such that...

asked 2 hours ago -

The average length of time between arrivals at a turnpike

toll-booth is 26 seconds. What is...

asked 4 hours ago -

(a) A piston at 6.1 atm contains a gas that occupies a volume of

3.5 L....

asked 5 hours ago -

Please answer true or false. Words

cannot be changed or added in to make it true...

asked 5 hours ago -

An empty test tube weighs 15.923 grams. Then,

MgCl2•6H2O is added into the test tube. After...

asked 5 hours ago -

Assume memory access is 10 units of time and disk access is

10000 units of time....

asked 5 hours ago -

1. Are all good samples random?

2. Magazines often report surveys giving statistics such as “63%...

asked 5 hours ago