. Suppose that the forward rate of £ in $ is given: F1$/£=$1.20/£, but all other values are the same (see Slide #21).

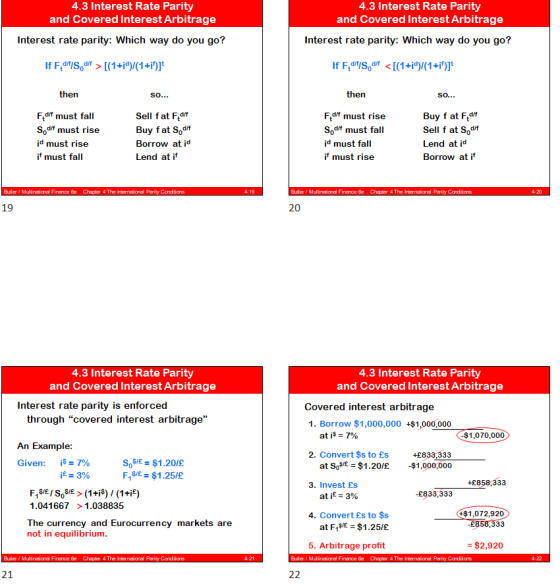

First show that the “covered interest arbitrage” is possible. Then, discuss the arbitrage strategies and its profit in $. Review lecture notes Slide #19, 20, 21, and 22.

Homework Answers

Interest

rate parity is possible because

Interest

rate parity is possible because

Add Answer to:

. Suppose that the forward rate of £

in $ is given: F1$/£=$1.20/£,

but all other...

3. Currently, the spot exchange rate is $1.50/£ and the three-month forward exchange rate is $1.52/£....

3. Currently, the spot exchange rate is $1.50/£ and the three-month forward exchange rate is $1.52/£. The three-month interest rate is 8.0 percent per annum in the U.S. and 5.8 percent per annum in the U.K. Assume that you can borrow as much as $1,500,000 or £1,000,000. a. Determine whether interest rate parity is currently holding. b. If IRP is not holding, how would you carry out covered interest arbitrage? Show all the steps and determine the arbitrage profit. c....

3. Currently, the spot exchange rate is $1.50/£ and the three-month forward exchange rate is $1.52/£. The three-month interest rate is 8.0 percent per annum in the U.S. and 5.8 percent per annum in the U.K. Assume that you can borrow as much as $1,500,000 or £1,000,000. a. Determine whether interest rate parity is currently holding. b. If IRP is not holding, how would you carry out covered interest arbitrage? Show all the steps and determine the arbitrage profit. c....

Suppose that the current spot exchange rate is €0.8250/$ and the three month forward exchange rate...

Suppose that the current spot exchange rate is €0.8250/$ and the three month forward exchange rate is €0.8132/$. The three-month interest rate is 5.80 percent per annum in the United States and 5.40 percent per annum in France. Assume that you can borrow up to $1,000,000 or €825,000. Show how to realize a certain profit via covered interest arbitrage, assuming that you want to realize profit in terms of U.S. dollars. Also determine the size of your arbitrage profit

Suppose that the current spot exchange rate is €0.8250/$ and the three month forward exchange rate is €0.8132/$. The three-month interest rate is 5.80 percent per annum in the United States and 5.40 percent per annum in France. Assume that you can borrow up to $1,000,000 or €825,000. Show how to realize a certain profit via covered interest arbitrage, assuming that you want to realize profit in terms of U.S. dollars. Also determine the size of your arbitrage profit

Suppose that the current spot exchange rate is €0.8250/$ and the three month forward exchange rate...

Suppose that the current spot exchange rate is €0.8250/$ and the three month forward exchange rate is €0.8132/$. The three-month interest rate is 5.80 percent per annum in the United States and 5.40 percent per annum in France. Assume that you can borrow up to $1,000,000 or €825,000. Show how to realize a certain profit via covered interest arbitrage, assuming that you want to realize profit in terms of U.S. dollars. Also determine the size of your arbitrage profit

Suppose that the current spot exchange rate is €0.8250/$ and the three month forward exchange rate is €0.8132/$. The three-month interest rate is 5.80 percent per annum in the United States and 5.40 percent per annum in France. Assume that you can borrow up to $1,000,000 or €825,000. Show how to realize a certain profit via covered interest arbitrage, assuming that you want to realize profit in terms of U.S. dollars. Also determine the size of your arbitrage profit

suppose that the current spot exchange rate is €0.815/$ and the three month forward exchange rate...

suppose that the current spot exchange rate is €0.815/$ and the three month forward exchange rate is €0.815/$. the three month interest rate is 6.00 percent per annum in the United States and 5.40 percent per annum in France . assume that you can borrow up to $1,000,000 or €30,000. show how to realize a certain profit via covered interest arbitrage, assuming that you want to realize profit in terms of U.S dollars. also determine the size of your arbitrage...

3. Covered Interest Arbitrage. Assume the following information: Spot rate of Mexican peso = $ .100 1-year Forward...

3. Covered Interest Arbitrage. Assume the following information: Spot rate of Mexican peso = $ .100 1-year Forward rate of Mexican peso = $ .098 Mexican interest rate = 8% US. interest rate =5% Show how to identify any arbitrage opportunity based on the Interest Rate Parity (IRP). What is your strategy to achieve your profit? What is your arbitrage profit per $1,000,000 (CIA) ?

Currently, the spot exchange rate is €1=$2 and the six month forward exchange rate is €1=$2.5....

Currently, the spot exchange rate is €1=$2 and the six month forward exchange rate is €1=$2.5. The six-month interest rate is 5% in the U.S. and 3% in the Germany. Assume that you can borrow as much as $1,000,000. Determine whether you can carry out a covered interest arbitrage. Show all the steps and the arbitrage profit if there is any.

Currently, the spot exchange rate is €1=$2 and the six month forward exchange rate is €1=$2.5. The six-month interest rate is 5% in the U.S. and 3% in the Germany. Assume that you can borrow as much as $1,000,000. Determine whether you can carry out a covered interest arbitrage. Show all the steps and the arbitrage profit if there is any.

Suppose that the current spot exchange rate is 0.80/$ and the three-month forward exchange rate i...

Suppose that the current spot exchange rate is 0.80/$ and the three-month forward exchange rate is 0.7813/$. The three-month interest rate is 5.60 percent per annum in the United States and 5.40 percent per annum in France. Assume that you can borrow up to $1,000,000 or 800,000. assuming that you want to realize profit in terms of U.S. dollars. The size of your arbitrage profit is S rounded)

Suppose that the current spot exchange rate is 0.80/$ and the three-month...

Suppose that the current spot exchange rate is 0.80/$ and the three-month forward exchange rate is 0.7813/$. The three-month interest rate is 5.60 percent per annum in the United States and 5.40 percent per annum in France. Assume that you can borrow up to $1,000,000 or 800,000. assuming that you want to realize profit in terms of U.S. dollars. The size of your arbitrage profit is S rounded)

Suppose that the current spot exchange rate is 0.80/$ and the three-month...

3. Assume the following information: Quoted Price Spot rate of Canadian dollar $0.81 90day forward rate of Canadian...

3. Assume the following information: Quoted Price Spot rate of Canadian dollar $0.81 90day forward rate of Canadian dollar $0.79 90day Canadian interest rate 4% (per 90 days) 90day U.S. interest rate 2.5% (per 90 days) a) Given this information, what would be the yield (percentage return) to a U.S. investor who used covered interest arbitrage? (Assume the investor invests $1,000,000.) b) The forward rate should rise, True or False?

3. Assume the following information: Quoted Price Spot rate of Canadian dollar $0.81 90day forward rate of Canadian dollar $0.79 90day Canadian interest rate 4% (per 90 days) 90day U.S. interest rate 2.5% (per 90 days) a) Given this information, what would be the yield (percentage return) to a U.S. investor who used covered interest arbitrage? (Assume the investor invests $1,000,000.) b) The forward rate should rise, True or False?

1. Assume the following information: Spot rate of Canadian dollar : $.80 90-day forward rate of Canadian dollar : $.79 9...

1. Assume the following information: Spot rate of Canadian dollar : $.80 90-day forward rate of Canadian dollar : $.79 90-day Canadian interest rate : 4% 90-day U.S. interest rate : 2.5% a) What would be the return to a U.S. investor who used covered interest arbitrage from investing in Canada? (assume the investor invests $1,000,000). Does the return exceed the return from investing in the U.S. over the 90-day period? Is it worthwhile for the U.S. investor to invest...

According to covered interest rate parity, what must the 1-year Japanese yen/US dollar forward rate assuming...

According to covered interest rate parity, what must the 1-year Japanese yen/US dollar forward rate assuming the following: E¥/$ = 123.85 (¥/$ spot rate), i¥ = 1.00% and i$ = 5.50%.

3. Currently, the spot exchange rate is $1.50/£ and the three-month forward exchange rate is $1.52/£. The three-month interest rate is 8.0 percent per annum in the U.S. and 5.8 percent per annum in the U.K. Assume that you can borrow as much as $1,500,000 or £1,000,000. a. Determine whether interest rate parity is currently holding. b. If IRP is not holding, how would you carry out covered interest arbitrage? Show all the steps and determine the arbitrage profit. c....

3. Currently, the spot exchange rate is $1.50/£ and the three-month forward exchange rate is $1.52/£. The three-month interest rate is 8.0 percent per annum in the U.S. and 5.8 percent per annum in the U.K. Assume that you can borrow as much as $1,500,000 or £1,000,000. a. Determine whether interest rate parity is currently holding. b. If IRP is not holding, how would you carry out covered interest arbitrage? Show all the steps and determine the arbitrage profit. c....

Suppose that the current spot exchange rate is €0.8250/$ and the three month forward exchange rate is €0.8132/$. The three-month interest rate is 5.80 percent per annum in the United States and 5.40 percent per annum in France. Assume that you can borrow up to $1,000,000 or €825,000. Show how to realize a certain profit via covered interest arbitrage, assuming that you want to realize profit in terms of U.S. dollars. Also determine the size of your arbitrage profit

Suppose that the current spot exchange rate is €0.8250/$ and the three month forward exchange rate is €0.8132/$. The three-month interest rate is 5.80 percent per annum in the United States and 5.40 percent per annum in France. Assume that you can borrow up to $1,000,000 or €825,000. Show how to realize a certain profit via covered interest arbitrage, assuming that you want to realize profit in terms of U.S. dollars. Also determine the size of your arbitrage profit

Suppose that the current spot exchange rate is €0.8250/$ and the three month forward exchange rate is €0.8132/$. The three-month interest rate is 5.80 percent per annum in the United States and 5.40 percent per annum in France. Assume that you can borrow up to $1,000,000 or €825,000. Show how to realize a certain profit via covered interest arbitrage, assuming that you want to realize profit in terms of U.S. dollars. Also determine the size of your arbitrage profit

Suppose that the current spot exchange rate is €0.8250/$ and the three month forward exchange rate is €0.8132/$. The three-month interest rate is 5.80 percent per annum in the United States and 5.40 percent per annum in France. Assume that you can borrow up to $1,000,000 or €825,000. Show how to realize a certain profit via covered interest arbitrage, assuming that you want to realize profit in terms of U.S. dollars. Also determine the size of your arbitrage profit

Currently, the spot exchange rate is €1=$2 and the six month forward exchange rate is €1=$2.5. The six-month interest rate is 5% in the U.S. and 3% in the Germany. Assume that you can borrow as much as $1,000,000. Determine whether you can carry out a covered interest arbitrage. Show all the steps and the arbitrage profit if there is any.

Currently, the spot exchange rate is €1=$2 and the six month forward exchange rate is €1=$2.5. The six-month interest rate is 5% in the U.S. and 3% in the Germany. Assume that you can borrow as much as $1,000,000. Determine whether you can carry out a covered interest arbitrage. Show all the steps and the arbitrage profit if there is any.

Suppose that the current spot exchange rate is 0.80/$ and the three-month forward exchange rate is 0.7813/$. The three-month interest rate is 5.60 percent per annum in the United States and 5.40 percent per annum in France. Assume that you can borrow up to $1,000,000 or 800,000. assuming that you want to realize profit in terms of U.S. dollars. The size of your arbitrage profit is S rounded)

Suppose that the current spot exchange rate is 0.80/$ and the three-month...

Suppose that the current spot exchange rate is 0.80/$ and the three-month forward exchange rate is 0.7813/$. The three-month interest rate is 5.60 percent per annum in the United States and 5.40 percent per annum in France. Assume that you can borrow up to $1,000,000 or 800,000. assuming that you want to realize profit in terms of U.S. dollars. The size of your arbitrage profit is S rounded)

Suppose that the current spot exchange rate is 0.80/$ and the three-month...

3. Assume the following information: Quoted Price Spot rate of Canadian dollar $0.81 90day forward rate of Canadian dollar $0.79 90day Canadian interest rate 4% (per 90 days) 90day U.S. interest rate 2.5% (per 90 days) a) Given this information, what would be the yield (percentage return) to a U.S. investor who used covered interest arbitrage? (Assume the investor invests $1,000,000.) b) The forward rate should rise, True or False?

3. Assume the following information: Quoted Price Spot rate of Canadian dollar $0.81 90day forward rate of Canadian dollar $0.79 90day Canadian interest rate 4% (per 90 days) 90day U.S. interest rate 2.5% (per 90 days) a) Given this information, what would be the yield (percentage return) to a U.S. investor who used covered interest arbitrage? (Assume the investor invests $1,000,000.) b) The forward rate should rise, True or False?

Most questions answered within 3 hours.

-

lease solve all the

questions, don't need to explanations

Q1 - All animal

species have general...

asked 4 hours ago -

Business Phasing

1.Discuss the logical progression for growing a business, which

starts from the initial idea...

asked 4 hours ago -

Modify

When executing on the command line having only

this program name, the program will accept...

asked 6 hours ago -

Kenny Electric Company's noncallable bonds were issued several

years ago and now have 20 years to...

asked 6 hours ago -

find H(e^Jtheta) at theta= 0, pi/10, pi/20, pi/2 for

the following:

a) H(e^Jtheta)= 1+e^Jtheta

b) H(e^Jtheta)=...

asked 6 hours ago -

Home Corporation will open a new store on January 1. Based on

experience from its other...

asked 7 hours ago -

In a neoclassical model, use the IS-LM to analyze the effect of

a permanent money supply...

asked 7 hours ago -

An electron passes through a point 2.67 cm from a long straight

wire as it moves...

asked 8 hours ago -

A grammar is a 4-tuple G, G = (Ν, Σ, Π, Σ, S) where, Ν is...

asked 9 hours ago -

In this part, calculate the present values. Use the Excel PV

function to compute the present...

asked 9 hours ago -

Part 1. Primitive Types, Sorting, Recursion for

Homework.java

a) Implement the static method initializeArray that receives...

asked 10 hours ago -

Using C++, build a sorter that can rank a sequence of numbers in

a descending order....

asked 10 hours ago