Homework Answers

Add Answer to:

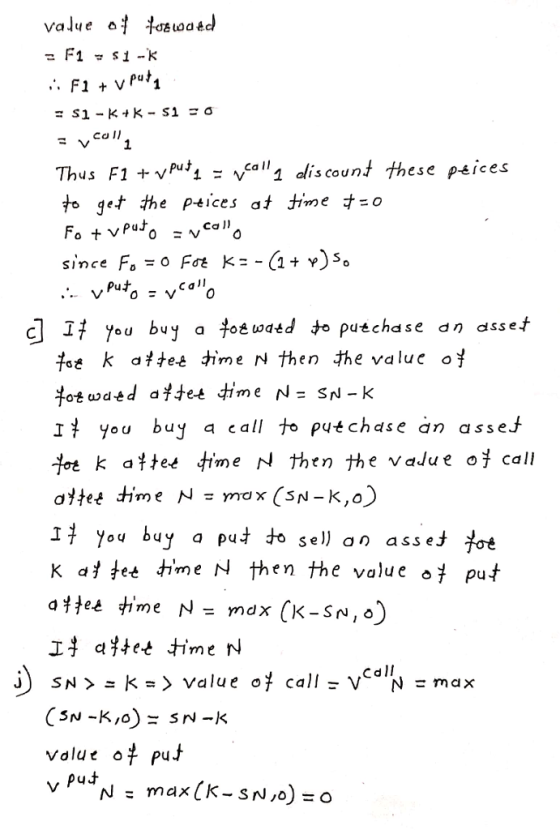

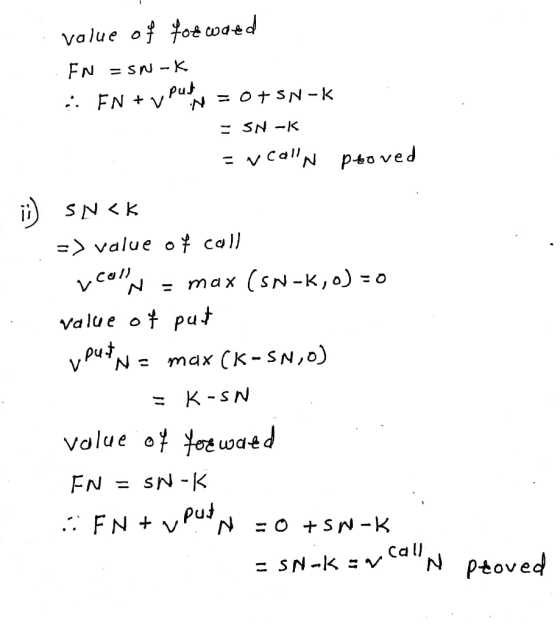

1. (Put-call parity) A stock currently costs So per share. In each time period, the value...

1. (Put-call parity) A stock currently costs So per share. In each time period, the value...

1. (Put-call parity) A stock currently costs So per share. In each time period, the value of the stock will either increase or decrease by u and d respectively, and the risk-free interest rate is r. Let Sn be the price of the stock at t n, for O < n < V, and consider three derivatives which expire at t- N, a call option Vall-(SN-K)+, a put option Vpul-(K-Sy)+, ad a forward contract Fv -SN -K (a) The forward...

1. (Put-call parity) A stock currently costs So per share. In each time period, the value of the stock will either increase or decrease by u and d respectively, and the risk-free interest rate is r. Let Sn be the price of the stock at t n, for O < n < V, and consider three derivatives which expire at t- N, a call option Vall-(SN-K)+, a put option Vpul-(K-Sy)+, ad a forward contract Fv -SN -K (a) The forward...

5. Consider the 3-period binomial model with So 100, u 2, dand r-1. (a) What is...

5. Consider the 3-period binomial model with So 100, u 2, dand r-1. (a) What is the current price of a lookback call option with a strike price of $100 that pays off (at time three) V3- max Sn - 100 Sn3 (b) What is the time-zero price of a lookback put option with a strike price of $100 that pays off (at time three) V 100-min Sn OSnK3 (c) What is the time-zero price of an Asian call option...

5. Consider the 3-period binomial model with So 100, u 2, dand r-1. (a) What is the current price of a lookback call option with a strike price of $100 that pays off (at time three) V3- max Sn - 100 Sn3 (b) What is the time-zero price of a lookback put option with a strike price of $100 that pays off (at time three) V 100-min Sn OSnK3 (c) What is the time-zero price of an Asian call option...

6. A stock currently costs $4 per share. In each time period, the value of th<e...

6. A stock currently costs $4 per share. In each time period, the value of th<e stock will either increase or decrease by 50%, and the risk-free interest rate is r 1/10. Let So, Si, and S2 be the prices of the stock at times 0, 1, and 2, and suppose we are selling a European-style call option expiring at time 2, with a strike price of vS1S2. That is, the value of the option at time 2 is (S2-VS152)+....

6. A stock currently costs $4 per share. In each time period, the value of th<e stock will either increase or decrease by 50%, and the risk-free interest rate is r 1/10. Let So, Si, and S2 be the prices of the stock at times 0, 1, and 2, and suppose we are selling a European-style call option expiring at time 2, with a strike price of vS1S2. That is, the value of the option at time 2 is (S2-VS152)+....

6. A stock currently costs $4 per share. In each time period, the value of th<e...

6. A stock currently costs $4 per share. In each time period, the value of th<e stock will either increase or decrease by 50%, and the risk-free interest rate is r 1/10. Let So, Si, and S2 be the prices of the stock at times 0, 1, and 2, and suppose we are selling a European-style call option expiring at time 2, with a strike price of vS1S2. That is, the value of the option at time 2 is (S2-VS152)+....

6. A stock currently costs $4 per share. In each time period, the value of th<e stock will either increase or decrease by 50%, and the risk-free interest rate is r 1/10. Let So, Si, and S2 be the prices of the stock at times 0, 1, and 2, and suppose we are selling a European-style call option expiring at time 2, with a strike price of vS1S2. That is, the value of the option at time 2 is (S2-VS152)+....

Question 7: 1. Both a call option and a put option are currently traded on stock...

Question 7:

1. Both a call option and a put option are currently traded on stock AXT. Both options have a strike price of $90 and maturity (T) of three months. The call premium (Co) is $2.75, the put premium (Po) is $4.12, and the underlying stock price (So) is $89.50. Assume that you trade one contract that has 100 shares when you calculate profit or loss. What will be your profit (or loss) if you take a long position...

Question 7:

1. Both a call option and a put option are currently traded on stock AXT. Both options have a strike price of $90 and maturity (T) of three months. The call premium (Co) is $2.75, the put premium (Po) is $4.12, and the underlying stock price (So) is $89.50. Assume that you trade one contract that has 100 shares when you calculate profit or loss. What will be your profit (or loss) if you take a long position...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000 1020 84.470 101.214 1050 1107 137.167 I 1) Suppose you invest in the S&P stock index for $1000, buy a 950-strike put, and sell a 1050- strike call. Draw a profit diagram for this position. What is the net option premium? 2) Here is a quote from an investment website about an investment strategy using options: One strategy investors apply is a "synthetic stock."...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000 1020 84.470 101.214 1050 1107 137.167 I 1) Suppose you invest in the S&P stock index for $1000, buy a 950-strike put, and sell a 1050- strike call. Draw a profit diagram for this position. What is the net option premium? 2) Here is a quote from an investment website about an investment strategy using options: One strategy investors apply is a "synthetic stock."...

3. (10 pts) For each k e [0, 1,2,..., 301 the symbol S(k) denotes the price of the stock at time k. A European call option with strike 90 and expiration n- 30 costs 15. A European put option with...

3. (10 pts) For each k e [0, 1,2,..., 301 the symbol S(k) denotes the price of the stock at time k. A European call option with strike 90 and expiration n- 30 costs 15. A European put option with strike 100 and expiration 30 costs 11. Both options have the same stock as their underlying security. What is the price of the security whose payoff structure is 7S (30) 630, if S(30) 100, S(30)-30, if 90 S(30) S 100,...

3. (10 pts) For each k e [0, 1,2,..., 301 the symbol S(k) denotes the price of the stock at time k. A European call option with strike 90 and expiration n- 30 costs 15. A European put option with strike 100 and expiration 30 costs 11. Both options have the same stock as their underlying security. What is the price of the security whose payoff structure is 7S (30) 630, if S(30) 100, S(30)-30, if 90 S(30) S 100,...

g) European call with a strike price of $40 costs $7. European put with the same...

g) European call with a strike price of $40 costs $7. European put with the same strike price and expiration date costs $6. Assume that you buy two calls and one put (strap strategy). Sketch the graph and write down functions of payoff and profit h) Consider a stock with a price of $50 and there is European put option on that stock with the strike of $55 and premium of $4. Assume that you buy 1/3 of a stock...

g) European call with a strike price of $40 costs $7. European put with the same strike price and expiration date costs $6. Assume that you buy two calls and one put (strap strategy). Sketch the graph and write down functions of payoff and profit h) Consider a stock with a price of $50 and there is European put option on that stock with the strike of $55 and premium of $4. Assume that you buy 1/3 of a stock...

9. Put-call parity and the value of a put option Aa Aa E Consider two portfolios...

9. Put-call parity and the value of a put option Aa Aa E Consider two portfolios A and B. At the expiration date, t, both portfolios have identical payoffs. Portfolio A consists of a put option and one share of stock. Portfolio B has a call option (with the same strike price and expiration date as the put option) and cash in the amount equal to the present value (PV) of the strike price discounted at the continuously compounded risk-free...

9. Put-call parity and the value of a put option Aa Aa E Consider two portfolios A and B. At the expiration date, t, both portfolios have identical payoffs. Portfolio A consists of a put option and one share of stock. Portfolio B has a call option (with the same strike price and expiration date as the put option) and cash in the amount equal to the present value (PV) of the strike price discounted at the continuously compounded risk-free...

Problem 22-6 Put-Call Parity A stock is currently selling for $73 per share. A call option...

Problem 22-6 Put-Call Parity A stock is currently selling for $73 per share. A call option with an exercise price of $77 sells for $3.65 and expires in three months. If the risk-free rate of interest is 3.3 percent per year, compounded continuously, what is the price of a put option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Put price

Problem 22-6 Put-Call Parity A stock is currently selling for $73 per share. A call option with an exercise price of $77 sells for $3.65 and expires in three months. If the risk-free rate of interest is 3.3 percent per year, compounded continuously, what is the price of a put option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Put price

1. (Put-call parity) A stock currently costs So per share. In each time period, the value of the stock will either increase or decrease by u and d respectively, and the risk-free interest rate is r. Let Sn be the price of the stock at t n, for O < n < V, and consider three derivatives which expire at t- N, a call option Vall-(SN-K)+, a put option Vpul-(K-Sy)+, ad a forward contract Fv -SN -K (a) The forward...

1. (Put-call parity) A stock currently costs So per share. In each time period, the value of the stock will either increase or decrease by u and d respectively, and the risk-free interest rate is r. Let Sn be the price of the stock at t n, for O < n < V, and consider three derivatives which expire at t- N, a call option Vall-(SN-K)+, a put option Vpul-(K-Sy)+, ad a forward contract Fv -SN -K (a) The forward...

5. Consider the 3-period binomial model with So 100, u 2, dand r-1. (a) What is the current price of a lookback call option with a strike price of $100 that pays off (at time three) V3- max Sn - 100 Sn3 (b) What is the time-zero price of a lookback put option with a strike price of $100 that pays off (at time three) V 100-min Sn OSnK3 (c) What is the time-zero price of an Asian call option...

5. Consider the 3-period binomial model with So 100, u 2, dand r-1. (a) What is the current price of a lookback call option with a strike price of $100 that pays off (at time three) V3- max Sn - 100 Sn3 (b) What is the time-zero price of a lookback put option with a strike price of $100 that pays off (at time three) V 100-min Sn OSnK3 (c) What is the time-zero price of an Asian call option...

6. A stock currently costs $4 per share. In each time period, the value of th<e stock will either increase or decrease by 50%, and the risk-free interest rate is r 1/10. Let So, Si, and S2 be the prices of the stock at times 0, 1, and 2, and suppose we are selling a European-style call option expiring at time 2, with a strike price of vS1S2. That is, the value of the option at time 2 is (S2-VS152)+....

6. A stock currently costs $4 per share. In each time period, the value of th<e stock will either increase or decrease by 50%, and the risk-free interest rate is r 1/10. Let So, Si, and S2 be the prices of the stock at times 0, 1, and 2, and suppose we are selling a European-style call option expiring at time 2, with a strike price of vS1S2. That is, the value of the option at time 2 is (S2-VS152)+....

6. A stock currently costs $4 per share. In each time period, the value of th<e stock will either increase or decrease by 50%, and the risk-free interest rate is r 1/10. Let So, Si, and S2 be the prices of the stock at times 0, 1, and 2, and suppose we are selling a European-style call option expiring at time 2, with a strike price of vS1S2. That is, the value of the option at time 2 is (S2-VS152)+....

6. A stock currently costs $4 per share. In each time period, the value of th<e stock will either increase or decrease by 50%, and the risk-free interest rate is r 1/10. Let So, Si, and S2 be the prices of the stock at times 0, 1, and 2, and suppose we are selling a European-style call option expiring at time 2, with a strike price of vS1S2. That is, the value of the option at time 2 is (S2-VS152)+....

Question 7:

1. Both a call option and a put option are currently traded on stock AXT. Both options have a strike price of $90 and maturity (T) of three months. The call premium (Co) is $2.75, the put premium (Po) is $4.12, and the underlying stock price (So) is $89.50. Assume that you trade one contract that has 100 shares when you calculate profit or loss. What will be your profit (or loss) if you take a long position...

Question 7:

1. Both a call option and a put option are currently traded on stock AXT. Both options have a strike price of $90 and maturity (T) of three months. The call premium (Co) is $2.75, the put premium (Po) is $4.12, and the underlying stock price (So) is $89.50. Assume that you trade one contract that has 100 shares when you calculate profit or loss. What will be your profit (or loss) if you take a long position...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000 1020 84.470 101.214 1050 1107 137.167 I 1) Suppose you invest in the S&P stock index for $1000, buy a 950-strike put, and sell a 1050- strike call. Draw a profit diagram for this position. What is the net option premium? 2) Here is a quote from an investment website about an investment strategy using options: One strategy investors apply is a "synthetic stock."...

Assume the following premia: Strike $950 Call $120.405 93.809 84.470 71.802 51.873 Put $51.777 74.201 1000 1020 84.470 101.214 1050 1107 137.167 I 1) Suppose you invest in the S&P stock index for $1000, buy a 950-strike put, and sell a 1050- strike call. Draw a profit diagram for this position. What is the net option premium? 2) Here is a quote from an investment website about an investment strategy using options: One strategy investors apply is a "synthetic stock."...

3. (10 pts) For each k e [0, 1,2,..., 301 the symbol S(k) denotes the price of the stock at time k. A European call option with strike 90 and expiration n- 30 costs 15. A European put option with strike 100 and expiration 30 costs 11. Both options have the same stock as their underlying security. What is the price of the security whose payoff structure is 7S (30) 630, if S(30) 100, S(30)-30, if 90 S(30) S 100,...

3. (10 pts) For each k e [0, 1,2,..., 301 the symbol S(k) denotes the price of the stock at time k. A European call option with strike 90 and expiration n- 30 costs 15. A European put option with strike 100 and expiration 30 costs 11. Both options have the same stock as their underlying security. What is the price of the security whose payoff structure is 7S (30) 630, if S(30) 100, S(30)-30, if 90 S(30) S 100,...

g) European call with a strike price of $40 costs $7. European put with the same strike price and expiration date costs $6. Assume that you buy two calls and one put (strap strategy). Sketch the graph and write down functions of payoff and profit h) Consider a stock with a price of $50 and there is European put option on that stock with the strike of $55 and premium of $4. Assume that you buy 1/3 of a stock...

g) European call with a strike price of $40 costs $7. European put with the same strike price and expiration date costs $6. Assume that you buy two calls and one put (strap strategy). Sketch the graph and write down functions of payoff and profit h) Consider a stock with a price of $50 and there is European put option on that stock with the strike of $55 and premium of $4. Assume that you buy 1/3 of a stock...

9. Put-call parity and the value of a put option Aa Aa E Consider two portfolios A and B. At the expiration date, t, both portfolios have identical payoffs. Portfolio A consists of a put option and one share of stock. Portfolio B has a call option (with the same strike price and expiration date as the put option) and cash in the amount equal to the present value (PV) of the strike price discounted at the continuously compounded risk-free...

9. Put-call parity and the value of a put option Aa Aa E Consider two portfolios A and B. At the expiration date, t, both portfolios have identical payoffs. Portfolio A consists of a put option and one share of stock. Portfolio B has a call option (with the same strike price and expiration date as the put option) and cash in the amount equal to the present value (PV) of the strike price discounted at the continuously compounded risk-free...

Problem 22-6 Put-Call Parity A stock is currently selling for $73 per share. A call option with an exercise price of $77 sells for $3.65 and expires in three months. If the risk-free rate of interest is 3.3 percent per year, compounded continuously, what is the price of a put option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Put price

Problem 22-6 Put-Call Parity A stock is currently selling for $73 per share. A call option with an exercise price of $77 sells for $3.65 and expires in three months. If the risk-free rate of interest is 3.3 percent per year, compounded continuously, what is the price of a put option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Put price

Most questions answered within 3 hours.

-

An empty test tube weighs 15.923 grams. Then,

MgCl2•6H2O is added into the test tube. After...

asked 45 minutes ago -

Please answer true or false. Words

cannot be changed or added in to make it true...

asked 43 minutes ago -

(a) A piston at 6.1 atm contains a gas that occupies a volume of

3.5 L....

asked 44 minutes ago -

Assume memory access is 10 units of time and disk access is

10000 units of time....

asked 1 hour ago -

1. Are all good samples random?

2. Magazines often report surveys giving statistics such as “63%...

asked 1 hour ago -

Under all the various types of market structures, firms

must eventually earn some economic profits for...

asked 1 hour ago -

Consider the following fitness regime for a single locus trait

with two co-dominant alleles: w11 =...

asked 1 hour ago -

A large cable company reports the following.

80% of its customers subscribe to its cable TV...

asked 1 hour ago -

Please answer the question in brief.

Discuss the role of ERP in organizations. Are ERP tools...

asked 1 hour ago -

Discuss the pros and cons of collaborative software such

as SameTime. Does it increase productivity? What...

asked 1 hour ago -

Buying your in-laws a gift because it’s expected is

due to the ____________ motive of gift-giving....

asked 1 hour ago -

Calculate the expected value, the variance, and the standard

deviation of the given random variable X....

asked 2 hours ago