Homework Answers

Competitive market is a market in which there are many firms and product is similar, all firms are price takers and there is free entry and exit for any firm.

This market in the long run only has normal profit. In the short run it may have a abnormal profit or a loss but it achieves the normal profit in the long run.

Profit is maximised when marginal cost= marginal revenue and firm charge that price.

Let us look at the following figure.

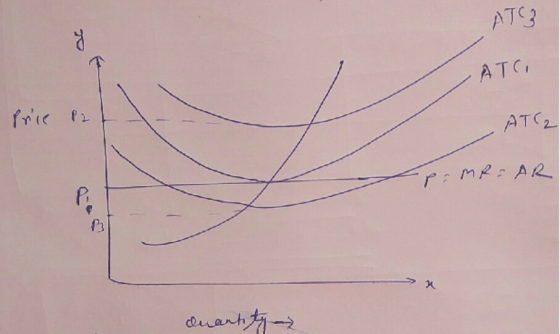

Case 1: Firm j is having a abnormal profit as the price charged is P1 and average total cost in the market is ATC1 , then looking at this other firms will enter in the market and supply curve in the market will shift to right, it will decrease the prices and this firm will be forced to charge only P3 as a price which is equal to average total cost. Normal profit.

Case 2: Firm is having a loss as the price charged is P1 and average total cost in the market is ATC3, costs went up due to increase in material costs but as market is too competitive firms may nor raise prices immediately and will continue to produce as firms are able to cover variable costs atleast. Those firms which do not cover these costs willl be forced out, and supply curve in the market will shift to left, it will increase the prices and firms will be charging P2 as a price which is equal to average total cost. Normal profit.

Hence in the short run a firm j may have loss or abnormal profit but in the long run it achieves only normal profit in the competitive markets.

In monopoly, firm is a price maker and charges price above the average total cost and hence aims at abnormal profits.

Add Answer to:

Vild is lile pi UIL-IlldX1121118 yudlilily UI Uutput IUI HAAVVdlelleil CUITIPdlly. IS lielildl kel llI IUIlg-Tuileyului...

Return again to the market for good G, and illustrate movement back to long run equilibrium...

Return again to the market for good G, and illustrate movement back to long run equilibrium both in the market for good Gand for firm j. What is the profit situation of firm j? PROBLEM 3 Assume perfect competition exists for Good W, and assume the market is in long run equilibrium. Depict the market for good W, and indicate initial supply, demand, equilibrium price and quantity with subscript 1. To the right of the market, depict the long run...

Return again to the market for good G, and illustrate movement back to long run equilibrium both in the market for good Gand for firm j. What is the profit situation of firm j? PROBLEM 3 Assume perfect competition exists for Good W, and assume the market is in long run equilibrium. Depict the market for good W, and indicate initial supply, demand, equilibrium price and quantity with subscript 1. To the right of the market, depict the long run...

Assume that pistachios are produced in a perfectly competitive constant-cost industry. *****I JUST NEED part C...

Assume that pistachios are produced in a perfectly competitive constant-cost industry. *****I JUST NEED part C AND D ANSWERED NOT A AND B, JUST INCLUDED FOR REFERENCE TO PROBLEM****** a. The market for pistachios is in a full long-run equilibrium state. Use side-by-side diagrams for the market and a typical firm to illustrate the equilibrium, being sure to include price, market output, the output of the typical firm and relevant cost curves.. b. Now assume that there is an increase...

NEED ANSWERS OF PART (f,g,h,j) Problem 2 [21 marks] Consider a firm that uses two inputs. The quantity used of input 1...

NEED ANSWERS OF PART (f,g,h,j)

Problem 2 [21 marks] Consider a firm that uses two inputs. The quantity used of input 1 is denoted by x, and the quantity used of input 2 is denoted by x2. The firm produces and sells one good using the production function f(x1, x2)-4x053x25. The final good is sold at price P $10. The prices of inputs 1 and 2 are w$2 and w2 $3, respectively. The markets for the final good and both...

NEED ANSWERS OF PART (f,g,h,j)

Problem 2 [21 marks] Consider a firm that uses two inputs. The quantity used of input 1 is denoted by x, and the quantity used of input 2 is denoted by x2. The firm produces and sells one good using the production function f(x1, x2)-4x053x25. The final good is sold at price P $10. The prices of inputs 1 and 2 are w$2 and w2 $3, respectively. The markets for the final good and both...

PART 1 Costs & Revenue Price MC The INDUSTRY is the price maker The SINGLE FIRM...

PART 1 Costs & Revenue Price MC The INDUSTRY is the price maker The SINGLE FIRM IS a price taker S ATC ARMR D Q Q Quantity Output Price Costs Revenue The INDUSTRY is the TSINGLES a proto MC pro NOIVAL proft in the US ATC AR-MR P1 AR-MR D Q01 Q10 Output a. What type of market structure is shown in the diagram above and how did you determine this? b. What are the firm's short run profit maximizing...

PART 1 Costs & Revenue Price MC The INDUSTRY is the price maker The SINGLE FIRM IS a price taker S ATC ARMR D Q Q Quantity Output Price Costs Revenue The INDUSTRY is the TSINGLES a proto MC pro NOIVAL proft in the US ATC AR-MR P1 AR-MR D Q01 Q10 Output a. What type of market structure is shown in the diagram above and how did you determine this? b. What are the firm's short run profit maximizing...

Problem 4: A firm has total cost function: c(y) = 50y2 + 40y + 30 A)...

Problem 4: A firm has total cost function: c(y) = 50y2 + 40y + 30 A) What is the total fixed cost? B) What is the average fixed cost? C) What is the total variable cost? D) What is the average variable cost? E) What is the marginal cost? F) What is the average total cost? G) In a competitive market, what is the lowest price at which the firm will supply a positive quantity in long-run equilibrium? H) What...

Problem 4: A firm has total cost function: c(y) = 50y2 + 40y + 30 A) What is the total fixed cost? B) What is the average fixed cost? C) What is the total variable cost? D) What is the average variable cost? E) What is the marginal cost? F) What is the average total cost? G) In a competitive market, what is the lowest price at which the firm will supply a positive quantity in long-run equilibrium? H) What...

a) Why is a monopolistically competitive firm less efficient than a perfectly competitive firm? It produces...

a) Why is a monopolistically competitive firm less efficient than a perfectly competitive firm? It produces at an output that is lower than its minimum efficient scale (MES) It earns positive economic profits in the long run It deters entry of new firms by putting up entry barriers All of the answers are correct b) Suppose a monopolistically competitive firm has MC=4Q+5. Its demand is P=145-3Q and marginal revenue is MR=145-6Q. What is its profit-maximizing output level? 17 14 16...

please please help me! one long problem and some vocab (For this question you have 20...

please please help me! one long problem and some vocab

(For this question you have 20 attempts) Throughout this problem assume that for an industry aggregate demand is given by: QP) - 900 - 50p Also, each firm in the industry has a production function of f(k)= Vik. Each firm has a short run capital stock of 100 units and r6. Initially, we 2. a. Find the firm's short run cost function in the first box put the variable costs...

please please help me! one long problem and some vocab

(For this question you have 20 attempts) Throughout this problem assume that for an industry aggregate demand is given by: QP) - 900 - 50p Also, each firm in the industry has a production function of f(k)= Vik. Each firm has a short run capital stock of 100 units and r6. Initially, we 2. a. Find the firm's short run cost function in the first box put the variable costs...

1. Consumer’s utility function is: U (X,Y) = 10X + Y. Consumer’s income M is 40...

1. Consumer’s utility function is: U (X,Y) = 10X + Y. Consumer’s income M is 40 euros, the price per unit of good X (i.e. Px ) is 5 euros and the price per unit of good Y (i.e. Py) is 1 euro. a) What is the marginal utility of good X (MUx) for the consumer? ( Answer: MUx = 10) b) What is the marginal utility of good Y (MUy) for the consumer? ( Answer: MUy = 1) c)...

Total Points 100 pts. Il credit will be given only when () your answers are correct...

Total Points 100 pts. Il credit will be given only when () your answers are correct and (a) you explain the steps or reasoning behind your answers. . Due date: Thursday, Dec a7th 2018, in class and in hard copy cost as follow: TC 0.Q2+ Q +10 and MC -o.2 Q +1. It faces the demand curve Q 35- 5P. (35 points) a) What are the price, output, and profit for this monopolist? b) Carefully draw the diagram that illustrates...

Total Points 100 pts. Il credit will be given only when () your answers are correct and (a) you explain the steps or reasoning behind your answers. . Due date: Thursday, Dec a7th 2018, in class and in hard copy cost as follow: TC 0.Q2+ Q +10 and MC -o.2 Q +1. It faces the demand curve Q 35- 5P. (35 points) a) What are the price, output, and profit for this monopolist? b) Carefully draw the diagram that illustrates...

This homework assignment compares a competitive market with a monopolistic market. The market demand curve is...

This homework assignment compares a competitive market with a monopolistic market. The market demand curve is P 122-¼Q. For each firm, marginal oosts are 20 + qi50 and fixed costs are 1 00. We assume first that the market is competitive. Module 8explains the competitive pricing procedure. Wederive the long-run price from the firms' cost curve competitive firms price at long-run minimum average costs. Question: Why is this relation true? Answer: Decreasing marginal utility implies an upward sloping marginal cost...

This homework assignment compares a competitive market with a monopolistic market. The market demand curve is P 122-¼Q. For each firm, marginal oosts are 20 + qi50 and fixed costs are 1 00. We assume first that the market is competitive. Module 8explains the competitive pricing procedure. Wederive the long-run price from the firms' cost curve competitive firms price at long-run minimum average costs. Question: Why is this relation true? Answer: Decreasing marginal utility implies an upward sloping marginal cost...

Return again to the market for good G, and illustrate movement back to long run equilibrium both in the market for good Gand for firm j. What is the profit situation of firm j? PROBLEM 3 Assume perfect competition exists for Good W, and assume the market is in long run equilibrium. Depict the market for good W, and indicate initial supply, demand, equilibrium price and quantity with subscript 1. To the right of the market, depict the long run...

Return again to the market for good G, and illustrate movement back to long run equilibrium both in the market for good Gand for firm j. What is the profit situation of firm j? PROBLEM 3 Assume perfect competition exists for Good W, and assume the market is in long run equilibrium. Depict the market for good W, and indicate initial supply, demand, equilibrium price and quantity with subscript 1. To the right of the market, depict the long run...

NEED ANSWERS OF PART (f,g,h,j)

Problem 2 [21 marks] Consider a firm that uses two inputs. The quantity used of input 1 is denoted by x, and the quantity used of input 2 is denoted by x2. The firm produces and sells one good using the production function f(x1, x2)-4x053x25. The final good is sold at price P $10. The prices of inputs 1 and 2 are w$2 and w2 $3, respectively. The markets for the final good and both...

NEED ANSWERS OF PART (f,g,h,j)

Problem 2 [21 marks] Consider a firm that uses two inputs. The quantity used of input 1 is denoted by x, and the quantity used of input 2 is denoted by x2. The firm produces and sells one good using the production function f(x1, x2)-4x053x25. The final good is sold at price P $10. The prices of inputs 1 and 2 are w$2 and w2 $3, respectively. The markets for the final good and both...

PART 1 Costs & Revenue Price MC The INDUSTRY is the price maker The SINGLE FIRM IS a price taker S ATC ARMR D Q Q Quantity Output Price Costs Revenue The INDUSTRY is the TSINGLES a proto MC pro NOIVAL proft in the US ATC AR-MR P1 AR-MR D Q01 Q10 Output a. What type of market structure is shown in the diagram above and how did you determine this? b. What are the firm's short run profit maximizing...

PART 1 Costs & Revenue Price MC The INDUSTRY is the price maker The SINGLE FIRM IS a price taker S ATC ARMR D Q Q Quantity Output Price Costs Revenue The INDUSTRY is the TSINGLES a proto MC pro NOIVAL proft in the US ATC AR-MR P1 AR-MR D Q01 Q10 Output a. What type of market structure is shown in the diagram above and how did you determine this? b. What are the firm's short run profit maximizing...

Problem 4: A firm has total cost function: c(y) = 50y2 + 40y + 30 A) What is the total fixed cost? B) What is the average fixed cost? C) What is the total variable cost? D) What is the average variable cost? E) What is the marginal cost? F) What is the average total cost? G) In a competitive market, what is the lowest price at which the firm will supply a positive quantity in long-run equilibrium? H) What...

Problem 4: A firm has total cost function: c(y) = 50y2 + 40y + 30 A) What is the total fixed cost? B) What is the average fixed cost? C) What is the total variable cost? D) What is the average variable cost? E) What is the marginal cost? F) What is the average total cost? G) In a competitive market, what is the lowest price at which the firm will supply a positive quantity in long-run equilibrium? H) What...

please please help me! one long problem and some vocab

(For this question you have 20 attempts) Throughout this problem assume that for an industry aggregate demand is given by: QP) - 900 - 50p Also, each firm in the industry has a production function of f(k)= Vik. Each firm has a short run capital stock of 100 units and r6. Initially, we 2. a. Find the firm's short run cost function in the first box put the variable costs...

please please help me! one long problem and some vocab

(For this question you have 20 attempts) Throughout this problem assume that for an industry aggregate demand is given by: QP) - 900 - 50p Also, each firm in the industry has a production function of f(k)= Vik. Each firm has a short run capital stock of 100 units and r6. Initially, we 2. a. Find the firm's short run cost function in the first box put the variable costs...

Total Points 100 pts. Il credit will be given only when () your answers are correct and (a) you explain the steps or reasoning behind your answers. . Due date: Thursday, Dec a7th 2018, in class and in hard copy cost as follow: TC 0.Q2+ Q +10 and MC -o.2 Q +1. It faces the demand curve Q 35- 5P. (35 points) a) What are the price, output, and profit for this monopolist? b) Carefully draw the diagram that illustrates...

Total Points 100 pts. Il credit will be given only when () your answers are correct and (a) you explain the steps or reasoning behind your answers. . Due date: Thursday, Dec a7th 2018, in class and in hard copy cost as follow: TC 0.Q2+ Q +10 and MC -o.2 Q +1. It faces the demand curve Q 35- 5P. (35 points) a) What are the price, output, and profit for this monopolist? b) Carefully draw the diagram that illustrates...

This homework assignment compares a competitive market with a monopolistic market. The market demand curve is P 122-¼Q. For each firm, marginal oosts are 20 + qi50 and fixed costs are 1 00. We assume first that the market is competitive. Module 8explains the competitive pricing procedure. Wederive the long-run price from the firms' cost curve competitive firms price at long-run minimum average costs. Question: Why is this relation true? Answer: Decreasing marginal utility implies an upward sloping marginal cost...

This homework assignment compares a competitive market with a monopolistic market. The market demand curve is P 122-¼Q. For each firm, marginal oosts are 20 + qi50 and fixed costs are 1 00. We assume first that the market is competitive. Module 8explains the competitive pricing procedure. Wederive the long-run price from the firms' cost curve competitive firms price at long-run minimum average costs. Question: Why is this relation true? Answer: Decreasing marginal utility implies an upward sloping marginal cost...

Most questions answered within 3 hours.

-

When 60.1 gg of calcium is reacted with nitrogen gas, 31.7 gg of

calcium nitride is...

asked 2 minutes ago -

The random variable X is exponentially distributed, where X

represents the time it takes for a...

asked 16 minutes ago -

a) Write a verilog module for 1:4 Demultiplexer using verilog

primitives.

b) Design 1-to-4 DEMUX using...

asked 11 minutes ago -

MATLAB

write a MATLAB function (1) output a third-order polynomial

function with the coefficients as the...

asked 24 minutes ago -

A z-score

communicates a raw score’s "relative standing"

under the normal curve in relation to:

asked 33 minutes ago -

An object is vibrating on a spring with the following equation

of motion:

?=(30 ??)cos((2?)/(160)?)

a)...

asked 32 minutes ago -

Vulcan Flyovers offers scenic overflights of Mount St. Helens,

the volcano in Washington State that explosively...

asked 34 minutes ago -

If organizations do not adapt fast enough and move incrementally

from the twentieth-century model to the...

asked 35 minutes ago -

A helium balloon with 2.5L of gas has a gauge pressure of 10,000

Pa. The balloon...

asked 39 minutes ago -

What is responsible for Jupiter's enormous magnetic field?

asked 55 minutes ago -

At the end of the year, a company offered to buy 5,000 units of

a product...

asked 56 minutes ago -

Implement C++ program for each of the following.

Let D = [-48, -14, -8, 0, 1,...

asked 1 hour ago