Homework Answers

1.

Add Answer to:

Part II (Binomial Tree) ai' 1. Compute the price of a call option using the stock...

Using a binomial tree, calculate the price of a $40 strike 6-month call option, using 3-month...

Using a binomial tree, calculate the price of a $40 strike 6-month call option, using 3-month intervals as the time period. Using the US system. Assume the following data: S = $37.90, r = 5.0%, σ = 30%.

A 1-year European call option is modeled with a 1-period binomial tree with u = 1.2, d = 0.7.

A 1-year European call option is modeled with a 1-period binomial tree with u = 1.2, d = 0.7. The stock price is 50. The strike price is 55. The stock pays no dividends. The call premium is 3.10. σ = 0.25.Determine the risk-free rate

5. Consider a European call option on the stock of XYZ, with a strike price of...

5. Consider a European call option on the stock of XYZ, with a strike price of $25 and two months to expiration. The stock pays continuous dividends at the annual yield rate of 5%. The annual continuously compounded risk free interst rate is 11%. The stock currently trades for $23 per share. Suppose that in two months, the stock will trade for either S18 per share or $29 per share. Use the one-period binomial option pricing model to find today's...

5. Consider a European call option on the stock of XYZ, with a strike price of $25 and two months to expiration. The stock pays continuous dividends at the annual yield rate of 5%. The annual continuously compounded risk free interst rate is 11%. The stock currently trades for $23 per share. Suppose that in two months, the stock will trade for either S18 per share or $29 per share. Use the one-period binomial option pricing model to find today's...

A stock price is currently $100. A call option on this stock with a strike price...

A stock price is currently $100. A call option on this stock with a strike price of $100 and one year to maturity costs $13.61. The continuous-time interest rate is 5%. By using a one-step binomial tree, estimate the expected volatility level (σ) for the stock. Assume that u and d are modeled as below. ( Excel's Goal Seek will help solving this and will be much appreciated to be posted to see how it has been used to solve this problem, thanks)...

Consider the binomial model for an American call and put on a stock whose price is...

Consider the binomial model for an American call and put on a stock whose price is $90. The exercise price for both the put and the call is $65. The standard deviation of the stock returns is 25 percent per annum, and the risk-free rate is 6 percent per annum. The options expire in 120 days. The stock will pay a dividend equal to 4 percent of its value in 60 days. (a) Draw the three-period stock tree and the...

A 1-year American put option on a stock is modeled with a 2-period binomial tree. Given that

A 1-year American put option on a stock is modeled with a 2-period binomial tree. Given that the price of the stock is 100, the strike price is 105. σ = 0.4. The continuously compounded risk-free rate is 6%. The stock pays no dividends.Determine the risk-neutral probability and the put premium

Using a binomial tree, what is the price of a $40 strike 6-month American put option,...

Using a binomial tree, what is the price of a $40 strike 6-month American put option, using 3-month intervals as the time period? Assume the following data: S=$37.90, r=5.0%, 5=35%, =0.

Using a binomial tree, what is the price of a $40 strike 6-month American put option, using 3-month intervals as the time period? Assume the following data: S=$37.90, r=5.0%, 5=35%, =0.

Consider the following call option: The current price of the stock on which the call option...

Consider the following call option: The current price of the stock on which the call option is written is $32.00; The exercise or strike price of the call option is $30.00; The maturity of the call option is .25 years; The (annualized) variance in the returns of the stock is .16; and The risk-free rate of interest is 4 percent. Use the Black-Scholes option pricing model to estimate the value of the call option.

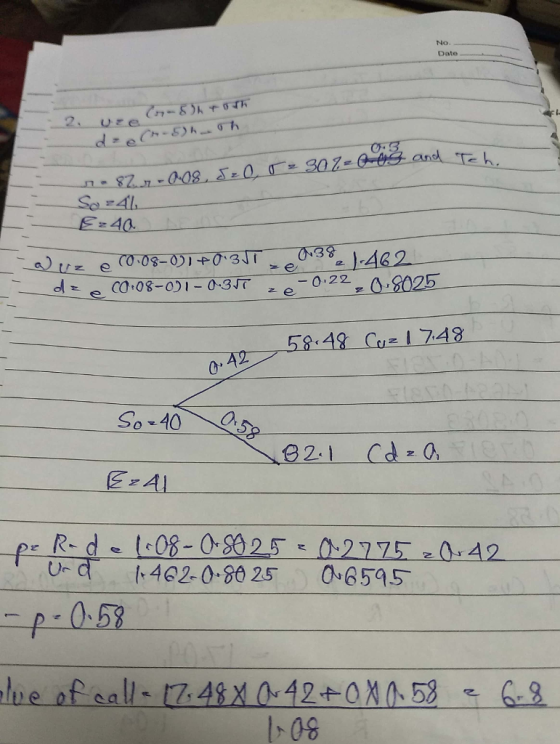

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annu...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

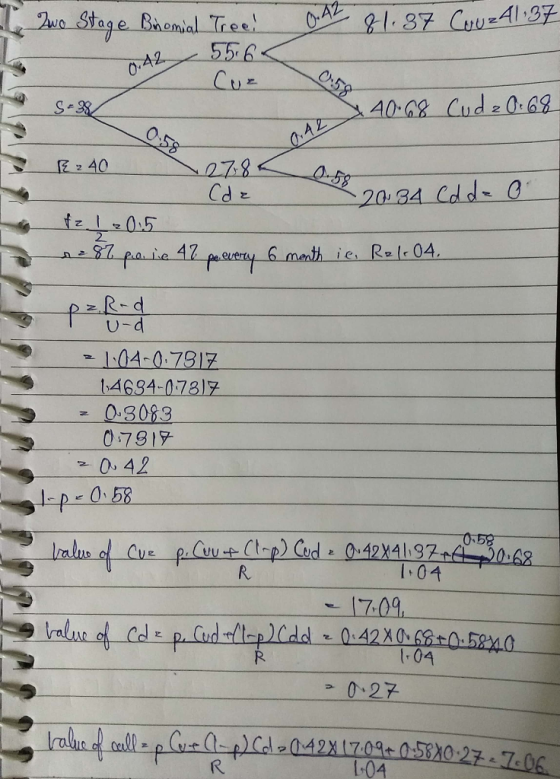

Use a two-step binomial model to evaluate a call option on a stock with the following...

Use a two-step binomial model to evaluate a call option on a stock with the following price projections. The current stock price is $80 and the strike price on the options is $82. The option expires in 6 months so each step is 3 months. The risk- free rate is 5%. What is the value of the call option? Note: to be eligible for partial credit, please show your work as much as possible and be sure to clearly indicate...

Use a two-step binomial model to evaluate a call option on a stock with the following price projections. The current stock price is $80 and the strike price on the options is $82. The option expires in 6 months so each step is 3 months. The risk- free rate is 5%. What is the value of the call option? Note: to be eligible for partial credit, please show your work as much as possible and be sure to clearly indicate...

5. Consider a European call option on the stock of XYZ, with a strike price of $25 and two months to expiration. The stock pays continuous dividends at the annual yield rate of 5%. The annual continuously compounded risk free interst rate is 11%. The stock currently trades for $23 per share. Suppose that in two months, the stock will trade for either S18 per share or $29 per share. Use the one-period binomial option pricing model to find today's...

5. Consider a European call option on the stock of XYZ, with a strike price of $25 and two months to expiration. The stock pays continuous dividends at the annual yield rate of 5%. The annual continuously compounded risk free interst rate is 11%. The stock currently trades for $23 per share. Suppose that in two months, the stock will trade for either S18 per share or $29 per share. Use the one-period binomial option pricing model to find today's...

Using a binomial tree, what is the price of a $40 strike 6-month American put option, using 3-month intervals as the time period? Assume the following data: S=$37.90, r=5.0%, 5=35%, =0.

Using a binomial tree, what is the price of a $40 strike 6-month American put option, using 3-month intervals as the time period? Assume the following data: S=$37.90, r=5.0%, 5=35%, =0.

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Problem 12.25. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is six months a. Calculate u, d, and p for a two step tree b. Value the option using a two step tree. c. Verify that DerivaGem gives the same answer d. Use DerivaGem to value the option with 5,...

Use a two-step binomial model to evaluate a call option on a stock with the following price projections. The current stock price is $80 and the strike price on the options is $82. The option expires in 6 months so each step is 3 months. The risk- free rate is 5%. What is the value of the call option? Note: to be eligible for partial credit, please show your work as much as possible and be sure to clearly indicate...

Use a two-step binomial model to evaluate a call option on a stock with the following price projections. The current stock price is $80 and the strike price on the options is $82. The option expires in 6 months so each step is 3 months. The risk- free rate is 5%. What is the value of the call option? Note: to be eligible for partial credit, please show your work as much as possible and be sure to clearly indicate...

Most questions answered within 3 hours.

-

The blues made its way into many kinds of music. Eric Clapton,

The Beatles, and Elvis...

asked 1 hour ago -

8. A wave in a string has a wave function given by: y (x, t) =...

asked 1 hour ago -

If you’re standing at the bottom of a hill and asked to evaluate

it while being...

asked 2 hours ago -

1. Which region has taken the lead in the world of

e-waste handling?

a) European Union...

asked 2 hours ago -

A 8.15- g bullet from a 9-mm pistol has a velocity of 366.0 m/s.

It strikes...

asked 4 hours ago -

The outstanding bonds of Alpha Extracts have a yield to maturity

of 7.4 percent and a...

asked 4 hours ago -

The Problem: The Case of the Harmonizing Vacations

Your CEO is exploring partnering with a European...

asked 5 hours ago -

A chemical equation is balanced by adding coefficients in front

of some formulas so that the...

asked 5 hours ago -

From the literature (reference your sources): What are the

lattice parameters of calcite and aragonite? Why...

asked 6 hours ago -

Your system is rejecting the question am asking which is

preceded by a case study. It...

asked 6 hours ago -

3. On January 2, 2000, Larry creates a trust with himself as

trustee. Larry as trustee...

asked 6 hours ago -

A member of the volleyball team spikes the ball. During this

process, she changes the velocity...

asked 6 hours ago