Homework Answers

![Page No. Date o yt Bo + B, Yt +E+ By capture the effect of prendus value on a present value of y Elys] = 0 C giren) To show B](http://img.homeworklib.com/questions/12d59320-8d3b-11eb-8cf3-818586585de8.png?x-oss-process=image/resize,w_560)

Add Answer to:

4 (10 marks). Consider a simple model of a time series ytas a function of its...

Consider the model defined by, Yt = BO + B1 Yt-1 + B2 Xt + Ut....

Consider the model defined by, Yt = BO + B1 Yt-1 + B2 Xt + Ut. Compute the long-run coefficients (2 decimals) for the model: Short-Run Long-Run BO 1.38 B1 0.60 B2 -5.26

Consider the model defined by, Yt = BO + B1 Yt-1 + B2 Xt + Ut. Compute the long-run coefficients (2 decimals) for the model: Short-Run Long-Run BO 1.38 B1 0.60 B2 -5.26

1. Consider the simple linear regression model: Ү, — Во + B а; + Ei, where 1, . . , En are i.i.d. N(0,02), for i1,2,......

1. Consider the simple linear regression model: Ү, — Во + B а; + Ei, where 1, . . , En are i.i.d. N(0,02), for i1,2,... ,n. Let b1 = s^y/8r and bo = Y - b1 t be the least squared estimators of B1 and Bo, respectively. We showed in class, that N(B; 02/) Y~N(BoB1 T;o2/n) and bi ~ are uncorrelated, i.e. o{Y;b} We also showed in class that bi and Y 0. = (a) Show that bo is...

1. Consider the simple linear regression model: Ү, — Во + B а; + Ei, where 1, . . , En are i.i.d. N(0,02), for i1,2,... ,n. Let b1 = s^y/8r and bo = Y - b1 t be the least squared estimators of B1 and Bo, respectively. We showed in class, that N(B; 02/) Y~N(BoB1 T;o2/n) and bi ~ are uncorrelated, i.e. o{Y;b} We also showed in class that bi and Y 0. = (a) Show that bo is...

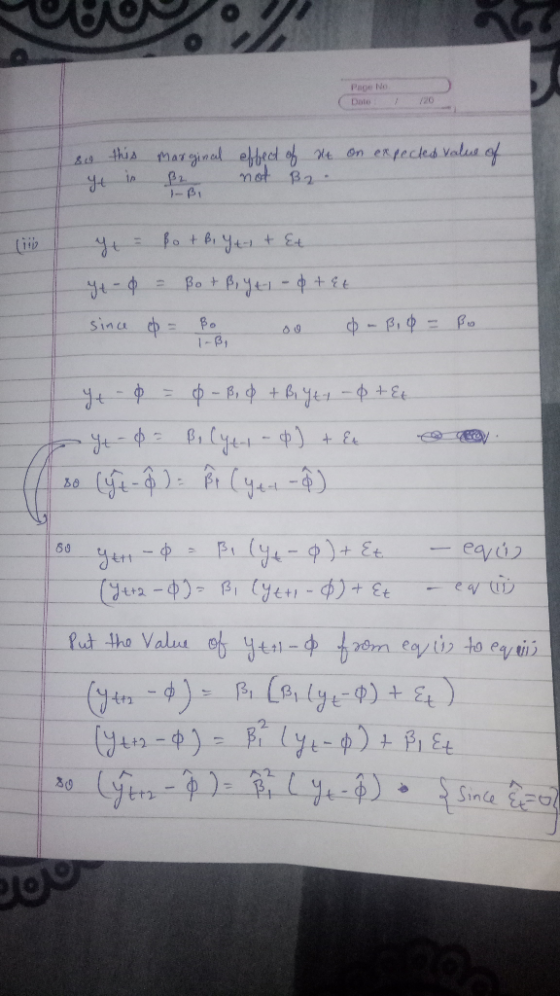

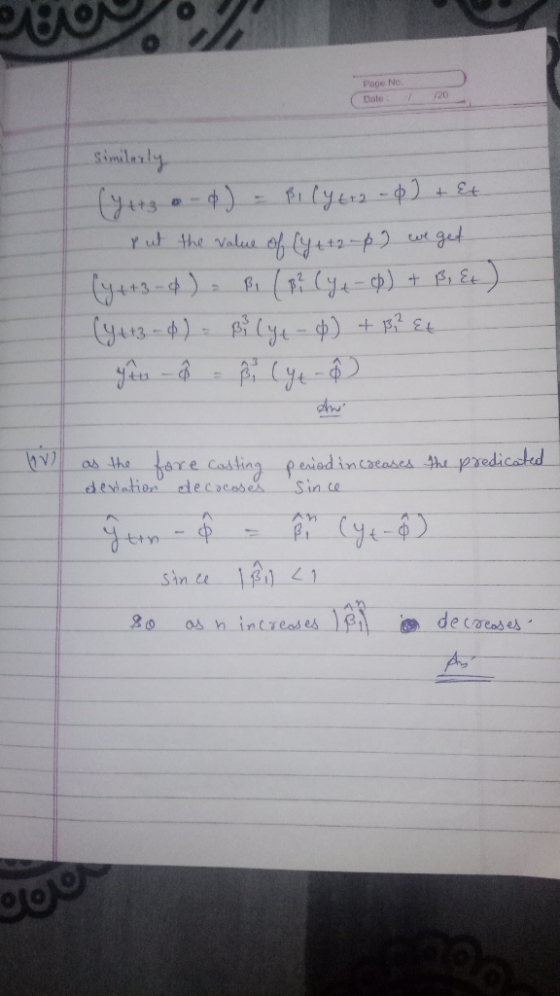

Consider the following AR(1) model: 1. a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. the following random 2. Consider walk...

Consider the following AR(1) model: 1. a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. the following random 2. Consider walk model: yeBo yt-1 +ut, t-0,1,..,T a. Show that yt-3βο + yt-3 + ut + ut-1 + ut-2. b. Suppose that 0-0, show that y.-t βο +4 + ut-1 + + u! c. Suppose that that yo -0, and ut for all t are ii.d. with mean 0 and variance...

Consider the following AR(1) model: 1. a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. the following random 2. Consider walk model: yeBo yt-1 +ut, t-0,1,..,T a. Show that yt-3βο + yt-3 + ut + ut-1 + ut-2. b. Suppose that 0-0, show that y.-t βο +4 + ut-1 + + u! c. Suppose that that yo -0, and ut for all t are ii.d. with mean 0 and variance...

Consider the model, Yt = BO+B1 Xt + Ut, and this is estimated using OLS with...

Consider the model, Yt = BO+B1 Xt + Ut, and this is estimated using OLS with 65 observations. However, it is suspected autocorrelation is present. You estimate the residuals (Uhatt) on the lag of residuals (Uhatt-1), Xt, and a constant. These estimation results are presented in the table below. Coefficient Std. Error Intercept Uhatt-1 Xt 0.006 0.052 0.004 0.051 0.002 0.001 0.004 R2 Adjusted-R2 0.003 Make your decision on autocorrelation and choose the most appropriate action from the responses. A....

Consider the model, Yt = BO+B1 Xt + Ut, and this is estimated using OLS with 65 observations. However, it is suspected autocorrelation is present. You estimate the residuals (Uhatt) on the lag of residuals (Uhatt-1), Xt, and a constant. These estimation results are presented in the table below. Coefficient Std. Error Intercept Uhatt-1 Xt 0.006 0.052 0.004 0.051 0.002 0.001 0.004 R2 Adjusted-R2 0.003 Make your decision on autocorrelation and choose the most appropriate action from the responses. A....

Consider the model, Yt = BO+B1 Xt + Ut, and this is estimated using OLS with...

Consider the model, Yt = BO+B1 Xt + Ut, and this is estimated using OLS with 65 observations. However, it is suspected autocorrelation is present. You estimate the residuals (Uhatt) on the lag of residuals (Uhatt-1), Xt, and a constant. These estimation results are presented in the table below. Std. Error Coefficient 0.006 0.004 Intercept Uhatt-1 Xt 0.052 0.051 0.001 0.002 0.004 R2 Adjusted-R2 0.003 Make your decision on autocorrelation and choose the most appropriate action from the responses. O...

Consider the model, Yt = BO+B1 Xt + Ut, and this is estimated using OLS with 65 observations. However, it is suspected autocorrelation is present. You estimate the residuals (Uhatt) on the lag of residuals (Uhatt-1), Xt, and a constant. These estimation results are presented in the table below. Std. Error Coefficient 0.006 0.004 Intercept Uhatt-1 Xt 0.052 0.051 0.001 0.002 0.004 R2 Adjusted-R2 0.003 Make your decision on autocorrelation and choose the most appropriate action from the responses. O...

Consider the model, Yt = BO+B1 Xt + Ut, and this is estimated using OLS with...

Consider the model, Yt = BO+B1 Xt + Ut, and this is estimated using OLS with 65 observations. However, it is suspected autocorrelation is present. You estimate the residuals (Uhatt) on the lag of residuals (Uhatt-1), Xt, and a constant. These estimation results are presented in the table below. Coefficient Std. Error 0.824 Intercept Uhatt-1 Xt 10.412 0.198 0.325 0.052 0.064 Adjusted-R2 0.122 0.107 Make your decision on autocorrelation and choose the most appropriate action from the responses. A. Not...

Consider the model, Yt = BO+B1 Xt + Ut, and this is estimated using OLS with 65 observations. However, it is suspected autocorrelation is present. You estimate the residuals (Uhatt) on the lag of residuals (Uhatt-1), Xt, and a constant. These estimation results are presented in the table below. Coefficient Std. Error 0.824 Intercept Uhatt-1 Xt 10.412 0.198 0.325 0.052 0.064 Adjusted-R2 0.122 0.107 Make your decision on autocorrelation and choose the most appropriate action from the responses. A. Not...

Consider the following model 1. Consider the following AR(1) model: a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. b. Show th...

Consider the following

model

1. Consider the following AR(1) model: a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. b. Show that 1 t-2 2. Consider the following random walk model: ytBo yt-1 +ut, t 0,1,...,T Show that ye 3o yt-3 + ut + Ut-1 +t-2 Suppose that yo - 0, show that yt - tPo + ut + ut-1++u, Suppose that that yo -0, and ut for all t...

Consider the following

model

1. Consider the following AR(1) model: a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. b. Show that 1 t-2 2. Consider the following random walk model: ytBo yt-1 +ut, t 0,1,...,T Show that ye 3o yt-3 + ut + Ut-1 +t-2 Suppose that yo - 0, show that yt - tPo + ut + ut-1++u, Suppose that that yo -0, and ut for all t...

Consider our intertemporal model, except this time we have three periods, wheret 0 is the first p...

Consider our intertemporal model, except this time we have three periods, wheret 0 is the first period, t = 1 is the second period, and t = 2 is the third and last period. This economy is populated by a representative agent and a government. The consumer seeks to maximize lifetime utility given by u(c) - an amount of gt = 0.2%, yt = 10 Vt. BIn(c). The government aims to spend t-0 Write down the individual's budget constraint. (0.5...

Consider our intertemporal model, except this time we have three periods, wheret 0 is the first period, t = 1 is the second period, and t = 2 is the third and last period. This economy is populated by a representative agent and a government. The consumer seeks to maximize lifetime utility given by u(c) - an amount of gt = 0.2%, yt = 10 Vt. BIn(c). The government aims to spend t-0 Write down the individual's budget constraint. (0.5...

Consider the model, Yt = BO + p1 Yt-1 + Ut, select the assumption(s) that are...

Consider the model, Yt = BO + p1 Yt-1 + Ut, select the assumption(s) that are needed to prove unbiased parameter estimates. (A. E[Ut Us |X, Yt-1, Yt-2, ... ] = 0 B. |p1|< 1 C. E[ Ut? |X, Yt-1, Yt-2, ... ] = su? D. E[ Ut |X, Yt-1, Yt-2, ... ] = 0

Consider the model, Yt = BO + p1 Yt-1 + Ut, select the assumption(s) that are needed to prove unbiased parameter estimates. (A. E[Ut Us |X, Yt-1, Yt-2, ... ] = 0 B. |p1|< 1 C. E[ Ut? |X, Yt-1, Yt-2, ... ] = su? D. E[ Ut |X, Yt-1, Yt-2, ... ] = 0

2. Consider the simple linear regression model: where e1, .. . , es, are i.i.d. N (0, o2), for i= 1,2,... , n. Suppose...

2. Consider the simple linear regression model: where e1, .. . , es, are i.i.d. N (0, o2), for i= 1,2,... , n. Suppose that we would like to estimate the mean response at x = x*, that is we want to estimate lyx=* = Bo + B1 x*. The least squares estimator for /uyx* is = bo bi x*, where bo, b1 are the least squares estimators for Bo, Bi. ayx= (a) Show that the least squares estimator for...

2. Consider the simple linear regression model: where e1, .. . , es, are i.i.d. N (0, o2), for i= 1,2,... , n. Suppose that we would like to estimate the mean response at x = x*, that is we want to estimate lyx=* = Bo + B1 x*. The least squares estimator for /uyx* is = bo bi x*, where bo, b1 are the least squares estimators for Bo, Bi. ayx= (a) Show that the least squares estimator for...

Consider the model defined by, Yt = BO + B1 Yt-1 + B2 Xt + Ut. Compute the long-run coefficients (2 decimals) for the model: Short-Run Long-Run BO 1.38 B1 0.60 B2 -5.26

Consider the model defined by, Yt = BO + B1 Yt-1 + B2 Xt + Ut. Compute the long-run coefficients (2 decimals) for the model: Short-Run Long-Run BO 1.38 B1 0.60 B2 -5.26

1. Consider the simple linear regression model: Ү, — Во + B а; + Ei, where 1, . . , En are i.i.d. N(0,02), for i1,2,... ,n. Let b1 = s^y/8r and bo = Y - b1 t be the least squared estimators of B1 and Bo, respectively. We showed in class, that N(B; 02/) Y~N(BoB1 T;o2/n) and bi ~ are uncorrelated, i.e. o{Y;b} We also showed in class that bi and Y 0. = (a) Show that bo is...

1. Consider the simple linear regression model: Ү, — Во + B а; + Ei, where 1, . . , En are i.i.d. N(0,02), for i1,2,... ,n. Let b1 = s^y/8r and bo = Y - b1 t be the least squared estimators of B1 and Bo, respectively. We showed in class, that N(B; 02/) Y~N(BoB1 T;o2/n) and bi ~ are uncorrelated, i.e. o{Y;b} We also showed in class that bi and Y 0. = (a) Show that bo is...

Consider the following AR(1) model: 1. a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. the following random 2. Consider walk model: yeBo yt-1 +ut, t-0,1,..,T a. Show that yt-3βο + yt-3 + ut + ut-1 + ut-2. b. Suppose that 0-0, show that y.-t βο +4 + ut-1 + + u! c. Suppose that that yo -0, and ut for all t are ii.d. with mean 0 and variance...

Consider the following AR(1) model: 1. a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. the following random 2. Consider walk model: yeBo yt-1 +ut, t-0,1,..,T a. Show that yt-3βο + yt-3 + ut + ut-1 + ut-2. b. Suppose that 0-0, show that y.-t βο +4 + ut-1 + + u! c. Suppose that that yo -0, and ut for all t are ii.d. with mean 0 and variance...

Consider the model, Yt = BO+B1 Xt + Ut, and this is estimated using OLS with 65 observations. However, it is suspected autocorrelation is present. You estimate the residuals (Uhatt) on the lag of residuals (Uhatt-1), Xt, and a constant. These estimation results are presented in the table below. Coefficient Std. Error Intercept Uhatt-1 Xt 0.006 0.052 0.004 0.051 0.002 0.001 0.004 R2 Adjusted-R2 0.003 Make your decision on autocorrelation and choose the most appropriate action from the responses. A....

Consider the model, Yt = BO+B1 Xt + Ut, and this is estimated using OLS with 65 observations. However, it is suspected autocorrelation is present. You estimate the residuals (Uhatt) on the lag of residuals (Uhatt-1), Xt, and a constant. These estimation results are presented in the table below. Coefficient Std. Error Intercept Uhatt-1 Xt 0.006 0.052 0.004 0.051 0.002 0.001 0.004 R2 Adjusted-R2 0.003 Make your decision on autocorrelation and choose the most appropriate action from the responses. A....

Consider the model, Yt = BO+B1 Xt + Ut, and this is estimated using OLS with 65 observations. However, it is suspected autocorrelation is present. You estimate the residuals (Uhatt) on the lag of residuals (Uhatt-1), Xt, and a constant. These estimation results are presented in the table below. Std. Error Coefficient 0.006 0.004 Intercept Uhatt-1 Xt 0.052 0.051 0.001 0.002 0.004 R2 Adjusted-R2 0.003 Make your decision on autocorrelation and choose the most appropriate action from the responses. O...

Consider the model, Yt = BO+B1 Xt + Ut, and this is estimated using OLS with 65 observations. However, it is suspected autocorrelation is present. You estimate the residuals (Uhatt) on the lag of residuals (Uhatt-1), Xt, and a constant. These estimation results are presented in the table below. Std. Error Coefficient 0.006 0.004 Intercept Uhatt-1 Xt 0.052 0.051 0.001 0.002 0.004 R2 Adjusted-R2 0.003 Make your decision on autocorrelation and choose the most appropriate action from the responses. O...

Consider the model, Yt = BO+B1 Xt + Ut, and this is estimated using OLS with 65 observations. However, it is suspected autocorrelation is present. You estimate the residuals (Uhatt) on the lag of residuals (Uhatt-1), Xt, and a constant. These estimation results are presented in the table below. Coefficient Std. Error 0.824 Intercept Uhatt-1 Xt 10.412 0.198 0.325 0.052 0.064 Adjusted-R2 0.122 0.107 Make your decision on autocorrelation and choose the most appropriate action from the responses. A. Not...

Consider the model, Yt = BO+B1 Xt + Ut, and this is estimated using OLS with 65 observations. However, it is suspected autocorrelation is present. You estimate the residuals (Uhatt) on the lag of residuals (Uhatt-1), Xt, and a constant. These estimation results are presented in the table below. Coefficient Std. Error 0.824 Intercept Uhatt-1 Xt 10.412 0.198 0.325 0.052 0.064 Adjusted-R2 0.122 0.107 Make your decision on autocorrelation and choose the most appropriate action from the responses. A. Not...

Consider the following

model

1. Consider the following AR(1) model: a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. b. Show that 1 t-2 2. Consider the following random walk model: ytBo yt-1 +ut, t 0,1,...,T Show that ye 3o yt-3 + ut + Ut-1 +t-2 Suppose that yo - 0, show that yt - tPo + ut + ut-1++u, Suppose that that yo -0, and ut for all t...

Consider the following

model

1. Consider the following AR(1) model: a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. b. Show that 1 t-2 2. Consider the following random walk model: ytBo yt-1 +ut, t 0,1,...,T Show that ye 3o yt-3 + ut + Ut-1 +t-2 Suppose that yo - 0, show that yt - tPo + ut + ut-1++u, Suppose that that yo -0, and ut for all t...

Consider our intertemporal model, except this time we have three periods, wheret 0 is the first period, t = 1 is the second period, and t = 2 is the third and last period. This economy is populated by a representative agent and a government. The consumer seeks to maximize lifetime utility given by u(c) - an amount of gt = 0.2%, yt = 10 Vt. BIn(c). The government aims to spend t-0 Write down the individual's budget constraint. (0.5...

Consider our intertemporal model, except this time we have three periods, wheret 0 is the first period, t = 1 is the second period, and t = 2 is the third and last period. This economy is populated by a representative agent and a government. The consumer seeks to maximize lifetime utility given by u(c) - an amount of gt = 0.2%, yt = 10 Vt. BIn(c). The government aims to spend t-0 Write down the individual's budget constraint. (0.5...

Consider the model, Yt = BO + p1 Yt-1 + Ut, select the assumption(s) that are needed to prove unbiased parameter estimates. (A. E[Ut Us |X, Yt-1, Yt-2, ... ] = 0 B. |p1|< 1 C. E[ Ut? |X, Yt-1, Yt-2, ... ] = su? D. E[ Ut |X, Yt-1, Yt-2, ... ] = 0

Consider the model, Yt = BO + p1 Yt-1 + Ut, select the assumption(s) that are needed to prove unbiased parameter estimates. (A. E[Ut Us |X, Yt-1, Yt-2, ... ] = 0 B. |p1|< 1 C. E[ Ut? |X, Yt-1, Yt-2, ... ] = su? D. E[ Ut |X, Yt-1, Yt-2, ... ] = 0

2. Consider the simple linear regression model: where e1, .. . , es, are i.i.d. N (0, o2), for i= 1,2,... , n. Suppose that we would like to estimate the mean response at x = x*, that is we want to estimate lyx=* = Bo + B1 x*. The least squares estimator for /uyx* is = bo bi x*, where bo, b1 are the least squares estimators for Bo, Bi. ayx= (a) Show that the least squares estimator for...

2. Consider the simple linear regression model: where e1, .. . , es, are i.i.d. N (0, o2), for i= 1,2,... , n. Suppose that we would like to estimate the mean response at x = x*, that is we want to estimate lyx=* = Bo + B1 x*. The least squares estimator for /uyx* is = bo bi x*, where bo, b1 are the least squares estimators for Bo, Bi. ayx= (a) Show that the least squares estimator for...

Most questions answered within 3 hours.

-

Ken believes the average age of men who come to get a haircut at

his barber...

asked 6 minutes ago -

(Ratio Analysis): Last year Co. XYZ had sales of $ 400,000, with

“cost of goods sold”...

asked 14 minutes ago -

can someone please write the balanced chemical

equation for the synthesis of Bromoacetanilide

from;

aniline +...

asked 10 minutes ago -

1. If a corporation purchases land and building and subsequently

tears down the building and uses...

asked 21 minutes ago -

Consider a 23-year bond with 7 percent annual coupon payments.

The market rate (YTM) is 6.4...

asked 24 minutes ago -

a tuba creates a 4th harmonic of frequency 116.5 Hz. what is the

frequency of the...

asked 30 minutes ago -

A coconut mass 2kg falls from a 30m tall tree. The coconut falls

and comes to...

asked 34 minutes ago -

Group Policies

Research GROUP POLICY OBJECTS (GPO'S)

You can start in the Windows Server 2012 eBook...

asked 38 minutes ago -

software engineering

Problems.

Create a use case diagram for class registration for a

university.

Create a...

asked 37 minutes ago -

You are trying to convince your friend who wants to attend

medical school to take BY123...

asked 53 minutes ago -

Subject: C++

I have created a class called QueueOfIntegers in a file called

QueueOfIntegers.h, which is...

asked 52 minutes ago -

calculate the number of molecules of gas in a

container of 2.0 liter at 30 degrees...

asked 1 hour ago