Given the following information of the mortgage pool that backs a MPT, what is the dollar...

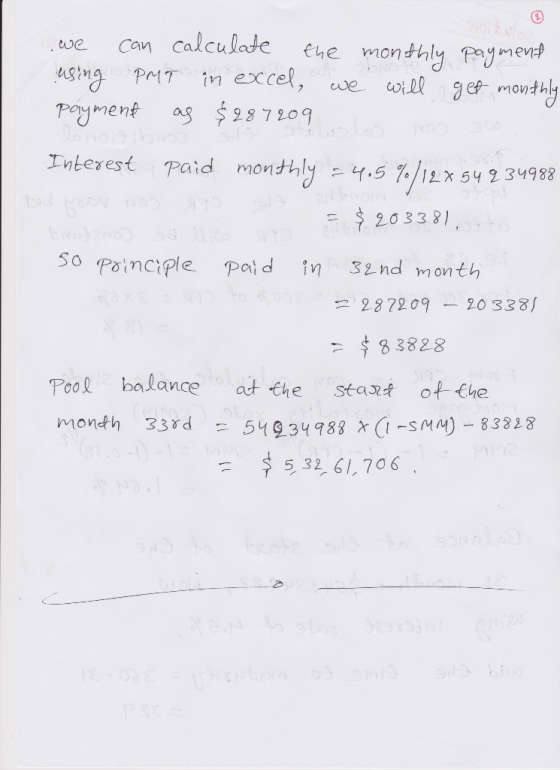

Given the following information of the mortgage pool that backs a MPT, what is the dollar amount of prepayment in month 32? Round your final answer to two decimals. • 30 year FRM, fully amortizing, monthly payments • WAC: 5% • Servicer/Guarantee fee: 0.5% • Prepayment assumption: 300% PSA • Loans were not seasoned before entering the pool • MBS has been active for a few years in collecting payments from borrowers and making payments to investors • Starting pool balance at month 32: $52, 234, 988

Homework Answers

Add Answer to:

Given the following information of the mortgage pool that backs

a MPT, what is the dollar...

QUESTION 6 10 points Save Given the following information of the mortgage pool that backs a...

QUESTION 6 10 points Save Given the following information of the mortgage pool that backs a MPT (same as Question 34,5), what is the total cash flow of investors in month 1 of this security? Round your final answer to two decimals. • 30 year FRM, fully amortizing, monthly payments • Loans seasoned for 3 months before entering pool • WAM: 357 • WAC: 4% • Servicer/Guarantee fee: 0.55% • Starting pool balance: 250,342.967 • Prepayment assumption: 75% PSA

QUESTION 6 10 points Save Given the following information of the mortgage pool that backs a MPT (same as Question 34,5), what is the total cash flow of investors in month 1 of this security? Round your final answer to two decimals. • 30 year FRM, fully amortizing, monthly payments • Loans seasoned for 3 months before entering pool • WAM: 357 • WAC: 4% • Servicer/Guarantee fee: 0.55% • Starting pool balance: 250,342.967 • Prepayment assumption: 75% PSA

HW4

Given the following information of the mortgage pool that backs a MPT, what is the regular scheduled payment in month 1 of the security? Use WAC as the mortgage rate and WAM as the number of periods for your calculations. Round your final answer to two decimals.• 30 year FRM, fully amortizing, monthly payments• Loans seasoned for 3 months before entering pool• WAM: 357 • WAC: 4%• Servicer/Guarantee fee: 0.55%• Starting pool balance: 250,342,967• Prepayment assumption: 75% PSAGiven the following...

Given a pool of 30 year fully-amortizing FRMs making monthly payments to investors with the following...

Given a pool of 30 year fully-amortizing FRMs making monthly payments to investors with the following characteristics: WAC: 6% Pass-through rate: 5.5% Prepayment assumption: 200 PSA Loans were not seasoned before entering pool This MBS has been active for a few years in collecting payments from borrowers and making payments to investors. It's currently month 26 in the pool.(t=26) Starting pool balance month in month 26: 72,534,232 What is the starting pool balance for month 27 of this security? (Hint:...

QUESTION 5 Use the information below to answer questions 5 through 7. The Cashman mortgage company...

QUESTION 5 Use the information below to answer questions 5 through 7. The Cashman mortgage company originated a pool containing 25 five-year fixed interest rate mortgages with an average balance of $100,000 each. All mortgages in the pool carry a coupon of 10%. (For simplicity, assume that all mortgage payments are made annually at 10% interest.) Assuming a constant annual prepayment rate of 10% (for simplicity, assume that prepayments are based on the pool balance at the end of the...

QUESTION 6 10 points Save Given the following information of the mortgage pool that backs a MPT (same as Question 34,5), what is the total cash flow of investors in month 1 of this security? Round your final answer to two decimals. • 30 year FRM, fully amortizing, monthly payments • Loans seasoned for 3 months before entering pool • WAM: 357 • WAC: 4% • Servicer/Guarantee fee: 0.55% • Starting pool balance: 250,342.967 • Prepayment assumption: 75% PSA

QUESTION 6 10 points Save Given the following information of the mortgage pool that backs a MPT (same as Question 34,5), what is the total cash flow of investors in month 1 of this security? Round your final answer to two decimals. • 30 year FRM, fully amortizing, monthly payments • Loans seasoned for 3 months before entering pool • WAM: 357 • WAC: 4% • Servicer/Guarantee fee: 0.55% • Starting pool balance: 250,342.967 • Prepayment assumption: 75% PSA

Most questions answered within 3 hours.

-

Define the following Marketing Psychology Principles of Human

Behavior: Priming, Reciprocity, Social Proof, Decoy Effect,

Scarcity,...

asked 7 minutes ago -

What does the graph of Range vs angle look like? Also what is

the slope of...

asked 10 minutes ago -

a

sample size of _ is needed So there a 99% confidence interval will

have a...

asked 16 minutes ago -

Strategy is an important part of project management and business

decisions. Define strategy and describe in...

asked 19 minutes ago -

Task 5.2 Numerical Analysis Using Nested Loops (13 pts)

Consider the following program:

void setup()

{...

asked 33 minutes ago -

If a lossless transformer has 1000 turns for a primary winding

and 100 turns for the...

asked 41 minutes ago -

Write the net ionic equation for the precipitation reaction that

occurs when aqueous solutions of potassium...

asked 50 minutes ago -

it

should be written in c++

Your program should take numbers from the user until the...

asked 56 minutes ago -

Buses are powered by chemical reactions. Define matter and the

four states of matter. What is...

asked 1 hour ago -

Use conservation of energy to find the velocity of a free point

charge q1 at 22cm...

asked 1 hour ago -

First, describe policies promoted by governments of the

political right to address economic globalization. Second, describe...

asked 1 hour ago -

M2-9 Completing T-Accounts LO2-4

Following are the transactions of Dennen, Inc., for the month of

January....

asked 1 hour ago