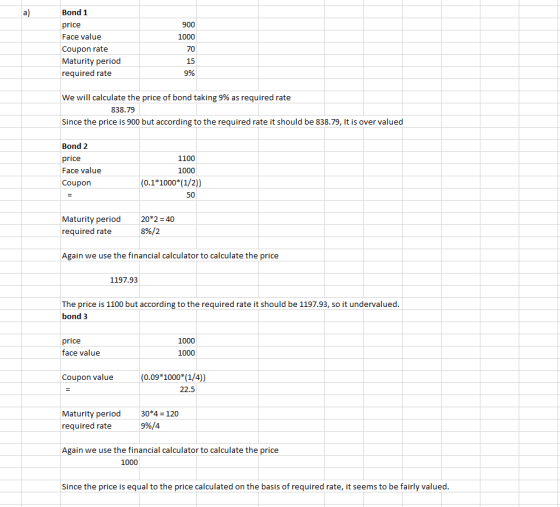

You are considering the following bonds to include in your portfolio: Bond 1 Bond 2 Bond...

- You are considering the following bonds to include in your portfolio:

|

Bond 1 |

Bond 2 |

Bond 3 |

|

|

Price |

$900.00 |

$1,100.00 |

$1,000.00 |

|

Face Value |

$1,000.00 |

$1,000.00 |

$1,000.00 |

|

Coupon Rate |

7.00% |

10.00% |

9.00% |

|

Frequency |

1 |

2 |

4 |

|

Maturity (Years) |

15 |

20 |

30 |

|

Required Return |

9.00% |

8.00% |

9.00% |

- Determine the highest price you would be willing to pay for each of these bonds using the PV function. Also find whether the bond is undervalued, overvalued, or fairly valued.

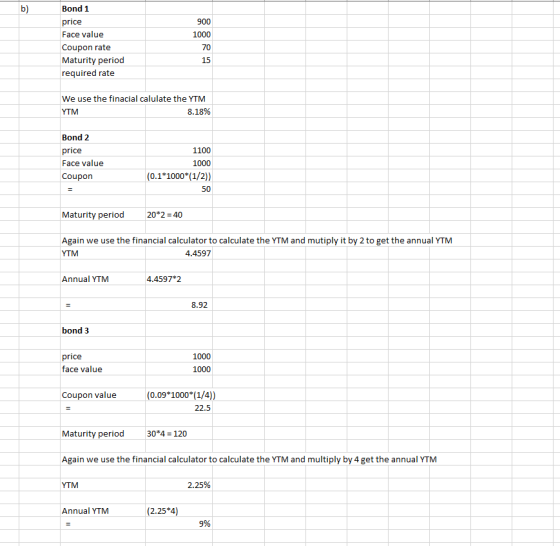

- Determine the yield to maturity on these bonds using the Rate function assuming that you purchase them at the given price. Also calculate the current yield of each bond.

- Assume the following settlement dates for each bond:

|

Bond 1 |

Bond 2 |

Bond 3 |

|

|

Settlement Date |

1/1/2018 |

6/1/2018 |

9/1/2018 |

Use the Price and Yield functions to recalculate your answers on parts (a), (b), and (c).

- Determine the duration and the modified duration of each bond.

Homework Answers

Add Answer to:

You are considering the following bonds to include in

your portfolio:

Bond 1

Bond 2

Bond...

You are considering the following bonds to include in your portfolio: Bond 1 Bond 2 Bond...

You are considering the following bonds to include in your portfolio: Bond 1 Bond 2 Bond 3 Price $900.00 $1,100.00 $1,000.00 Face Value $1,000.00 $1,000.00 $1,000.00 Coupon Rate 7.00% 10.00% 9.00% Frequency 1 2 4 Maturity (Years) 15 20 30 Required Return 9.00% 8.00% 9.00% Determine the highest price you would be willing to pay for each of these bonds using the PV function. Also find whether the bond is undervalued, overvalued, or fairly valued. Determine the yield to maturity...

Calculate the Duration and Modified Duration of each bond (already completed). Create a chart the shows...

Calculate the Duration and Modified Duration of each bond

(already completed). Create a chart the shows both measures

versus term to maturity. Does duration increase linearly

with term? If not, what relationship do you see?

А 2 Settlement Date 3 Maturity Date 4 Coupon Rate 5 Market Price 6 Face Value 7 Required Return 8 Frequency Bond A 2/15/2017 8/15/2027 4.00% 975.00 1,000.00 4.35% 2.00 Bond B 2/15/2017 5/15/2037 6.25% 1,062.00 1,000.00 5.50% 2.00 Bond C 2/15/2017 6/15/2047 7.40% 1,103.00...

Calculate the Duration and Modified Duration of each bond

(already completed). Create a chart the shows both measures

versus term to maturity. Does duration increase linearly

with term? If not, what relationship do you see?

А 2 Settlement Date 3 Maturity Date 4 Coupon Rate 5 Market Price 6 Face Value 7 Required Return 8 Frequency Bond A 2/15/2017 8/15/2027 4.00% 975.00 1,000.00 4.35% 2.00 Bond B 2/15/2017 5/15/2037 6.25% 1,062.00 1,000.00 5.50% 2.00 Bond C 2/15/2017 6/15/2047 7.40% 1,103.00...

b. A bond portfolio consists of the following three annual coupon payment bonds. Prices are per...

b. A bond portfolio consists of the following three annual coupon payment bonds. Prices are per 100 of par value. Price Coupon (%) Bond Maturity Market (years) Value 171,000 B 10 161,800 C 15 150.000 Modified Duration (years) 5.23 3.00 Yield-to- Maturity (%) 5.95 5.99 6.00 85.50 80.90 100.00 3.40 6.00 7.98 9.71 i. Determine the weight of each bond in the bond portfolio. (3 marks) ii. Calculate the bond portfolio's modified duration. (2 marks)

b. A bond portfolio consists of the following three annual coupon payment bonds. Prices are per 100 of par value. Price Coupon (%) Bond Maturity Market (years) Value 171,000 B 10 161,800 C 15 150.000 Modified Duration (years) 5.23 3.00 Yield-to- Maturity (%) 5.95 5.99 6.00 85.50 80.90 100.00 3.40 6.00 7.98 9.71 i. Determine the weight of each bond in the bond portfolio. (3 marks) ii. Calculate the bond portfolio's modified duration. (2 marks)

use Excel and calculate the duration of a $1,000 bond in the following problem: Settlement: 1/1/2018...

use Excel and calculate the duration of a $1,000 bond in the following problem: Settlement: 1/1/2018 Maturity: 12/31/2020 Coupon: 8.00% Yield: 7.00% Frequency: 2 Basis: 1

1.You are considering an investment in the bonds of the Front Range Electric Company. The bonds pay interest quarterly,...

1.You are considering an investment in the bonds of the Front Range Electric Company. The bonds pay interest quarterly, will mature in 15 years, and have a coupon rate of 4.50% on a face value of $1,000. Currently, the bonds are selling for $950. a.If your required return is 4.80% for bonds in this risk class, what is the highest price you would be willing to pay? (Use the PV function.) b.What is the current yield of these bonds? c.What...

You manage a bond portfolio with a current value of $150,000,000 & a duration of 7.32....

You manage a bond portfolio with a current value of $150,000,000 & a duration of 7.32. You need to hedge the interest rate risk of this portfolio for some reason. Today's date is Monday 12/10/2018, so the settlement price for a treasury bond is the 11th. You decide to use the 10 year t-note futures to hedge. The cheapest to deliver bond is the 3 percent coupon bond with maturity date of 09/30/2025 which is currently selling for a yield...

a. An investor buys a 5 % annual coupon payment bond with three years to maturity....

a. An investor buys a 5 % annual coupon payment bond with three years to maturity. The bond has a yield-to-maturity of 9%. The par value is $1000. i. Determine the market price of the bond. (2 marks) ii. Calculate the bond's duration. (3 marks) b.A bond portfolio consists of the following three annual coupon payment bonds. Prices are per 100 of par value. Modified Duration Yield-to- Coupon (%) Bond Maturity Market (years) Price Maturity (%) (years) 5.23 7.98 Value...

a. An investor buys a 5 % annual coupon payment bond with three years to maturity. The bond has a yield-to-maturity of 9%. The par value is $1000. i. Determine the market price of the bond. (2 marks) ii. Calculate the bond's duration. (3 marks) b.A bond portfolio consists of the following three annual coupon payment bonds. Prices are per 100 of par value. Modified Duration Yield-to- Coupon (%) Bond Maturity Market (years) Price Maturity (%) (years) 5.23 7.98 Value...

Question 1 A 12.58-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective...

Question 1 A 12.58-year maturity zero-coupon bond selling at a yield to maturity of 8% (effective annual yield) has convexity of 146.5 and modified duration of 11.65 years. A 30-year maturity 6% coupon bond making annual coupon payments also selling at a yield to maturity of 8% has nearly identical modified duration—-11.79 years—-but considerably higher convexity of 231.2. a. Suppose the yield to maturity on both bonds increases to 9%. What will be the actual percentage capital loss on each...

BOND VALUATION An investor has two bonds in her portfolio, Bond C and Bond Z. Each...

BOND VALUATION An investor has two bonds in her portfolio, Bond

C and Bond Z. Each

bond matures in 4 years, has a face value of $1,000, and has a

yield to maturity of 9 6%.

Bond C pays a 10% annual coupon, while Bond Z is a zero coupon

bond.

a. Assuming that the yield to maturity of each bond remains at 9 6%

over the next 4

years, calculate the price of the bonds at each of the...

BOND VALUATION An investor has two bonds in her portfolio, Bond

C and Bond Z. Each

bond matures in 4 years, has a face value of $1,000, and has a

yield to maturity of 9 6%.

Bond C pays a 10% annual coupon, while Bond Z is a zero coupon

bond.

a. Assuming that the yield to maturity of each bond remains at 9 6%

over the next 4

years, calculate the price of the bonds at each of the...

3. You have a zero coupon bond that pays $100 in two more years. Its price is $69.44. You also have a 5% coupon bon...

3. You have a zero coupon bond that pays $100 in two more years. Its price is $69.44. You also have a 5% coupon bond with a principal of $100. The spot rate for 1 year is r = 5%. (a) What is the spot rate for 2 years, ra? (b) What is the price of the coupon bond? (c) Make a graph to show the term structure of interest rates. 4. Compute the yield to maturity for the two...

3. You have a zero coupon bond that pays $100 in two more years. Its price is $69.44. You also have a 5% coupon bond with a principal of $100. The spot rate for 1 year is r = 5%. (a) What is the spot rate for 2 years, ra? (b) What is the price of the coupon bond? (c) Make a graph to show the term structure of interest rates. 4. Compute the yield to maturity for the two...

Calculate the Duration and Modified Duration of each bond

(already completed). Create a chart the shows both measures

versus term to maturity. Does duration increase linearly

with term? If not, what relationship do you see?

А 2 Settlement Date 3 Maturity Date 4 Coupon Rate 5 Market Price 6 Face Value 7 Required Return 8 Frequency Bond A 2/15/2017 8/15/2027 4.00% 975.00 1,000.00 4.35% 2.00 Bond B 2/15/2017 5/15/2037 6.25% 1,062.00 1,000.00 5.50% 2.00 Bond C 2/15/2017 6/15/2047 7.40% 1,103.00...

Calculate the Duration and Modified Duration of each bond

(already completed). Create a chart the shows both measures

versus term to maturity. Does duration increase linearly

with term? If not, what relationship do you see?

А 2 Settlement Date 3 Maturity Date 4 Coupon Rate 5 Market Price 6 Face Value 7 Required Return 8 Frequency Bond A 2/15/2017 8/15/2027 4.00% 975.00 1,000.00 4.35% 2.00 Bond B 2/15/2017 5/15/2037 6.25% 1,062.00 1,000.00 5.50% 2.00 Bond C 2/15/2017 6/15/2047 7.40% 1,103.00...

b. A bond portfolio consists of the following three annual coupon payment bonds. Prices are per 100 of par value. Price Coupon (%) Bond Maturity Market (years) Value 171,000 B 10 161,800 C 15 150.000 Modified Duration (years) 5.23 3.00 Yield-to- Maturity (%) 5.95 5.99 6.00 85.50 80.90 100.00 3.40 6.00 7.98 9.71 i. Determine the weight of each bond in the bond portfolio. (3 marks) ii. Calculate the bond portfolio's modified duration. (2 marks)

b. A bond portfolio consists of the following three annual coupon payment bonds. Prices are per 100 of par value. Price Coupon (%) Bond Maturity Market (years) Value 171,000 B 10 161,800 C 15 150.000 Modified Duration (years) 5.23 3.00 Yield-to- Maturity (%) 5.95 5.99 6.00 85.50 80.90 100.00 3.40 6.00 7.98 9.71 i. Determine the weight of each bond in the bond portfolio. (3 marks) ii. Calculate the bond portfolio's modified duration. (2 marks)

a. An investor buys a 5 % annual coupon payment bond with three years to maturity. The bond has a yield-to-maturity of 9%. The par value is $1000. i. Determine the market price of the bond. (2 marks) ii. Calculate the bond's duration. (3 marks) b.A bond portfolio consists of the following three annual coupon payment bonds. Prices are per 100 of par value. Modified Duration Yield-to- Coupon (%) Bond Maturity Market (years) Price Maturity (%) (years) 5.23 7.98 Value...

a. An investor buys a 5 % annual coupon payment bond with three years to maturity. The bond has a yield-to-maturity of 9%. The par value is $1000. i. Determine the market price of the bond. (2 marks) ii. Calculate the bond's duration. (3 marks) b.A bond portfolio consists of the following three annual coupon payment bonds. Prices are per 100 of par value. Modified Duration Yield-to- Coupon (%) Bond Maturity Market (years) Price Maturity (%) (years) 5.23 7.98 Value...

BOND VALUATION An investor has two bonds in her portfolio, Bond

C and Bond Z. Each

bond matures in 4 years, has a face value of $1,000, and has a

yield to maturity of 9 6%.

Bond C pays a 10% annual coupon, while Bond Z is a zero coupon

bond.

a. Assuming that the yield to maturity of each bond remains at 9 6%

over the next 4

years, calculate the price of the bonds at each of the...

BOND VALUATION An investor has two bonds in her portfolio, Bond

C and Bond Z. Each

bond matures in 4 years, has a face value of $1,000, and has a

yield to maturity of 9 6%.

Bond C pays a 10% annual coupon, while Bond Z is a zero coupon

bond.

a. Assuming that the yield to maturity of each bond remains at 9 6%

over the next 4

years, calculate the price of the bonds at each of the...

3. You have a zero coupon bond that pays $100 in two more years. Its price is $69.44. You also have a 5% coupon bond with a principal of $100. The spot rate for 1 year is r = 5%. (a) What is the spot rate for 2 years, ra? (b) What is the price of the coupon bond? (c) Make a graph to show the term structure of interest rates. 4. Compute the yield to maturity for the two...

3. You have a zero coupon bond that pays $100 in two more years. Its price is $69.44. You also have a 5% coupon bond with a principal of $100. The spot rate for 1 year is r = 5%. (a) What is the spot rate for 2 years, ra? (b) What is the price of the coupon bond? (c) Make a graph to show the term structure of interest rates. 4. Compute the yield to maturity for the two...

Most questions answered within 3 hours.

-

When determining if a molecule's configuration is E or Z, what

determines the higher priority groups?

asked 1 minute from now -

Sulfuric Acid is a "strong" acid, but only releases a single

proton when it dissolves. What...

asked 3 seconds ago -

13. What is the amount

of conversion cost transferred to finished goods? (Round

your intermediate calculations...

asked 33 seconds ago -

The

second floor of a house is 6 m above the street level. How much

work...

asked 2 minutes ago -

What uncontrollable factor(s) contributed to Hong Kong Disney’s

poor performance during its first year?

asked 3 minutes ago -

I wish to estimate µ, the mean of a population. After I collect

and an-

alyze...

asked 10 minutes ago -

You are interested in whether students that have a male

instructors perform differently on exams. To...

asked 16 minutes ago -

Discuss the following: The policies that promote economic

growth. Why are some countries more developed than...

asked 12 minutes ago -

I am supposed to reduce redundancy in the code and also make

unknown inputs, output "unknown"....

asked 17 minutes ago -

The ages of a group of

147

randomly selected adult females have a standard deviation of...

asked 22 minutes ago -

Blood alcohol content (BAC) is a measure of how much alcohol is

in someone’s blood. It...

asked 29 minutes ago -

A flow rate of 0.4 m / s of air enters a compressor at 100 kPa....

asked 57 minutes ago