Identify the correct principle for each of the following

activities using the drop-down list.

Homework Answers

Accounting principles are the rules and guidelines that companies must follow when reporting financial data. The Financial Accounting Standards Board (FASB) issues a standardized set of accounting principles in the U.S. referred to as generally accepted accounting principles (GAAP).

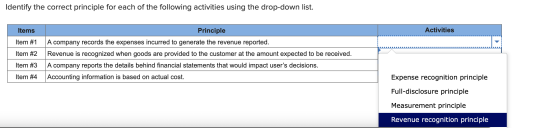

Item 1

A company records the expenses incurred to generate the revenue

reported.

Correct Principle - Expense recognition principle.

The expense recognition principle states that expenses should be

recognized in the same period as the revenues to which they relate.

According to the matching principle, expenses should be recognized

in the same period as the related revenues. If expenses are

recorded as they are incurred, they may not match the revenues that

they relate to.

Item 2.

Revenue is recognized when goods are provided to the customer at

the amount expected to be received.

Correct Principle - Revenue recognition principle.

The revenue recognition principle using accrual accounting requires

that revenues are recognized when realized and earned–not when cash

is received. Revenue realized during an accounting period is

included in the income of the same period. The revenue recognition

principle is a cornerstone of accrual accounting together with the

matching principle.

Item 3

A company reports the details behind financial statements that

would impact user's decision.

Correct Principle - Full disclosure principle.

The full disclosure principle requires a company to provide the

necessary information so that people who are accustomed to reading

financial information are able to make informed decisions regarding

the company. The disclosures required under this principle can be

found in a number of places, like, the company's financial

statements including the notes to the financial statements and

supplementary schedules, quarterly earnings reports, press releases

and other communications.

Item 4

Accounting information is based on actual cost.

Correct Principle - Measurement principle.

Accounting measurement is the computation of economic or financial data in terms of money, hours, or other units. The measurement concept states that a business should only record an accounting transaction if it can be expressed in terms of money. The method used in accounting measurement helps compare and evaluate accounting data. When a company uses standard accounting measurements, it becomes easier to compare certain variables over specific time frames and therefore allows a company to better understand how it operates. This could include units sold, unit revenues, hours worked, cost per hour, etc.

Add Answer to:

Identify the correct principle for each of the following

activities using the drop-down list.

Identify the...

Match each of the numbered descriptions with the principle or assumption it best reflects. Principle/Assumption Description...

Match each of the numbered descriptions with the principle or assumption it best reflects. Principle/Assumption Description 1. A company reports details behind financial statements that would impact users' decisions 2. Financial statements reflect the assumption that the business continues operating 3. A company records the expenses incurred to generate the revenues reported 4. Concepts, assumptions, and guidelines for preparing financial statements. 5. Each business is accounted for separately from its owner or owners. 6. Revenue is recorded when products and...

Match each of the numbered descriptions with the principle or assumption it best reflects. Principle/Assumption Description 1. A company reports details behind financial statements that would impact users' decisions 2. Financial statements reflect the assumption that the business continues operating 3. A company records the expenses incurred to generate the revenues reported 4. Concepts, assumptions, and guidelines for preparing financial statements. 5. Each business is accounted for separately from its owner or owners. 6. Revenue is recorded when products and...

Options: Correctness: Correct or Incorrect Principle: a. Faithfull representation b. Faithful representation (Full disclosure) Materiality c....

Options:

Correctness: Correct or Incorrect

Principle:

a. Faithfull representation

b. Faithful representation (Full disclosure) Materiality

c. Faithful representation (Net asset principle)

d. Historical Cost Measurement

e. Historical cost measurement and Net asset principle, Full

disclosure materiality and separate-entity

f. Matching; Comparability

g. Matching; Time-period assumption

h. Revenue and Historical cost measurement

i. Revenue and matching; Faithful representation and Freedom

from bias

j. Revenue recognition

k. Separate-entity

l. Time-period assumption

The following list of statements poses conceptual issues: Required: 1 and...

Options:

Correctness: Correct or Incorrect

Principle:

a. Faithfull representation

b. Faithful representation (Full disclosure) Materiality

c. Faithful representation (Net asset principle)

d. Historical Cost Measurement

e. Historical cost measurement and Net asset principle, Full

disclosure materiality and separate-entity

f. Matching; Comparability

g. Matching; Time-period assumption

h. Revenue and Historical cost measurement

i. Revenue and matching; Faithful representation and Freedom

from bias

j. Revenue recognition

k. Separate-entity

l. Time-period assumption

The following list of statements poses conceptual issues: Required: 1 and...

Review the transactional information and identify the accounting assumption, principle, and or constraint to which it...

Review the transactional information and identify the accounting assumption, principle, and or constraint to which it is related. Select an option below to match with each question: A) Time Period or Periodicity Assumption B) Economic Entity Assumption C) Fair Value D) Revenue and Expense Recognition Principle E) Revenue Recognition Principle F) Cost principle G) Full Disclosure Principle H) Separate or Economic entity Principle I) Expense Recognition Principle 1) The amount of goodwill recorded by a company that purchases another company...

Instructions Identify by number the accounting assumption, principle, or constraint that describes each situation below. Do...

Instructions Identify by number the accounting assumption, principle, or constraint that describes each situation below. Do not use a number more than once. a. Allocates expenses to revenues in the proper period. b. Indicates that fair value changes subsequent to purchase are not recorded in the accounts. (Do not use revenue recognition principle.) c. Ensures that all relevant financial information is reported. d. Rationale why plant assets are not reported at liquidation value. (Do not use historical cost principle.) e....

Instructions Identify by number the accounting assumption, principle, or constraint that describes each situation below. Do not use a number more than once. a. Allocates expenses to revenues in the proper period. b. Indicates that fair value changes subsequent to purchase are not recorded in the accounts. (Do not use revenue recognition principle.) c. Ensures that all relevant financial information is reported. d. Rationale why plant assets are not reported at liquidation value. (Do not use historical cost principle.) e....

Exercise 1-7 Identifying accounting principles and assumptions LO C4 Match each of the numbered descriptions with...

Exercise 1-7 Identifying accounting principles and assumptions LO C4 Match each of the numbered descriptions with the principle or assumption it best reflects Description Principle/Assumption 1-A company reports details behind financial statements that would impact users' decisions. 2. Financial statements reflect the assumption that the business continues operating 3. A company records the expenses incurred to generate the revenues reported. Derived from long-used and generally accepted accounting practices such as the 4. concepts, assumptions, and guidelines for preparing the financial...

Exercise 1-7 Identifying accounting principles and assumptions LO C4 Match each of the numbered descriptions with the principle or assumption it best reflects Description Principle/Assumption 1-A company reports details behind financial statements that would impact users' decisions. 2. Financial statements reflect the assumption that the business continues operating 3. A company records the expenses incurred to generate the revenues reported. Derived from long-used and generally accepted accounting practices such as the 4. concepts, assumptions, and guidelines for preparing the financial...

assify the following business activities using the drop-down list. Items Item #1 Acquiring resources (assets) that...

assify the following business activities using the drop-down list. Items Item #1 Acquiring resources (assets) that an organization plans to use to acquire and sell its products or services Item #2 Resources contributed by creditors Item #3 Disposing of resources (assets) that an organization uses to acquire and sell its products or services Item #4 Sales and revenues Item #15 Resources contributed by the owner along with any income the owner leaves in the organization Activities Investing Financing Operating Financing...

assify the following business activities using the drop-down list. Items Item #1 Acquiring resources (assets) that an organization plans to use to acquire and sell its products or services Item #2 Resources contributed by creditors Item #3 Disposing of resources (assets) that an organization uses to acquire and sell its products or services Item #4 Sales and revenues Item #15 Resources contributed by the owner along with any income the owner leaves in the organization Activities Investing Financing Operating Financing...

Drop area The following is a partial list of items that wluld appear on the various...

Drop area The following is a partial list of items that wluld appear on the various financial statements. Drag each item into the correct column to identify the financial statement. Balance Sheet Income Statement Statement of Retained Earnings drop item here drop item drop item here drop item here drop Item here drop item here drop item here drop item hore drop Item here drop Item here drop item here drop item here Statement of Cash Flows drop item here...

Drop area The following is a partial list of items that wluld appear on the various financial statements. Drag each item into the correct column to identify the financial statement. Balance Sheet Income Statement Statement of Retained Earnings drop item here drop item drop item here drop item here drop Item here drop item here drop item here drop item hore drop Item here drop Item here drop item here drop item here Statement of Cash Flows drop item here...

Identify the basic assumption, accounting principle, or constraint that applies to each statement. See bottom for...

Identify the basic assumption, accounting principle, or constraint that applies to each statement. See bottom for list of choices. Also Circle “OK” or “NOT OK”. Choose Not OK if the explanation violates the assumption, principle or constraint. (10 points): 1. Wagner Corporation adjusted the value of all assets and liabilities to reflect changes in the purchasing power of the dollar, Wagner uses the current rate of inflation as a guide. OK NOT OK Assumption/Principle: ______________________ 2. Maui Jims, Inc., provides...

Identify which accounting principle or assumption best describes each of the following practices: 1. Stark Company's...

Identify which accounting principle or assumption best describes each of the following practices: 1. Stark Company's accounting system maintains the equipment account as if the business will continue operating and not close. 2. Mike Derr owns both Salling Passions and Dockside Digs. In preparing financial statements for Dockside Digs, Mike makes sure that the expense transactions of Sailing Passions are kept separate from Dockside Digs's transactions and financial statements. 3. If $51 thousand cash is paid to buy land, the...

Identify which accounting principle or assumption best describes each of the following practices: 1. Stark Company's accounting system maintains the equipment account as if the business will continue operating and not close. 2. Mike Derr owns both Salling Passions and Dockside Digs. In preparing financial statements for Dockside Digs, Mike makes sure that the expense transactions of Sailing Passions are kept separate from Dockside Digs's transactions and financial statements. 3. If $51 thousand cash is paid to buy land, the...

Identify each of the following items as revenues, expenses, or withdrawals from the drop down provided....

Identify each of the following items as revenues, expenses, or withdrawals from the drop down provided. 1. Salaries 2. Owner withdrawal 3. Sales revenue 4. Cost of sales Expenses Revenues 5. Printing 6. Dividend income 7. Freight 8. Insurance Withdrawals

Identify each of the following items as revenues, expenses, or withdrawals from the drop down provided. 1. Salaries 2. Owner withdrawal 3. Sales revenue 4. Cost of sales Expenses Revenues 5. Printing 6. Dividend income 7. Freight 8. Insurance Withdrawals

Match each of the numbered descriptions with the principle or assumption it best reflects. Principle/Assumption Description 1. A company reports details behind financial statements that would impact users' decisions 2. Financial statements reflect the assumption that the business continues operating 3. A company records the expenses incurred to generate the revenues reported 4. Concepts, assumptions, and guidelines for preparing financial statements. 5. Each business is accounted for separately from its owner or owners. 6. Revenue is recorded when products and...

Match each of the numbered descriptions with the principle or assumption it best reflects. Principle/Assumption Description 1. A company reports details behind financial statements that would impact users' decisions 2. Financial statements reflect the assumption that the business continues operating 3. A company records the expenses incurred to generate the revenues reported 4. Concepts, assumptions, and guidelines for preparing financial statements. 5. Each business is accounted for separately from its owner or owners. 6. Revenue is recorded when products and...

Options:

Correctness: Correct or Incorrect

Principle:

a. Faithfull representation

b. Faithful representation (Full disclosure) Materiality

c. Faithful representation (Net asset principle)

d. Historical Cost Measurement

e. Historical cost measurement and Net asset principle, Full

disclosure materiality and separate-entity

f. Matching; Comparability

g. Matching; Time-period assumption

h. Revenue and Historical cost measurement

i. Revenue and matching; Faithful representation and Freedom

from bias

j. Revenue recognition

k. Separate-entity

l. Time-period assumption

The following list of statements poses conceptual issues: Required: 1 and...

Options:

Correctness: Correct or Incorrect

Principle:

a. Faithfull representation

b. Faithful representation (Full disclosure) Materiality

c. Faithful representation (Net asset principle)

d. Historical Cost Measurement

e. Historical cost measurement and Net asset principle, Full

disclosure materiality and separate-entity

f. Matching; Comparability

g. Matching; Time-period assumption

h. Revenue and Historical cost measurement

i. Revenue and matching; Faithful representation and Freedom

from bias

j. Revenue recognition

k. Separate-entity

l. Time-period assumption

The following list of statements poses conceptual issues: Required: 1 and...

Instructions Identify by number the accounting assumption, principle, or constraint that describes each situation below. Do not use a number more than once. a. Allocates expenses to revenues in the proper period. b. Indicates that fair value changes subsequent to purchase are not recorded in the accounts. (Do not use revenue recognition principle.) c. Ensures that all relevant financial information is reported. d. Rationale why plant assets are not reported at liquidation value. (Do not use historical cost principle.) e....

Instructions Identify by number the accounting assumption, principle, or constraint that describes each situation below. Do not use a number more than once. a. Allocates expenses to revenues in the proper period. b. Indicates that fair value changes subsequent to purchase are not recorded in the accounts. (Do not use revenue recognition principle.) c. Ensures that all relevant financial information is reported. d. Rationale why plant assets are not reported at liquidation value. (Do not use historical cost principle.) e....

Exercise 1-7 Identifying accounting principles and assumptions LO C4 Match each of the numbered descriptions with the principle or assumption it best reflects Description Principle/Assumption 1-A company reports details behind financial statements that would impact users' decisions. 2. Financial statements reflect the assumption that the business continues operating 3. A company records the expenses incurred to generate the revenues reported. Derived from long-used and generally accepted accounting practices such as the 4. concepts, assumptions, and guidelines for preparing the financial...

Exercise 1-7 Identifying accounting principles and assumptions LO C4 Match each of the numbered descriptions with the principle or assumption it best reflects Description Principle/Assumption 1-A company reports details behind financial statements that would impact users' decisions. 2. Financial statements reflect the assumption that the business continues operating 3. A company records the expenses incurred to generate the revenues reported. Derived from long-used and generally accepted accounting practices such as the 4. concepts, assumptions, and guidelines for preparing the financial...

assify the following business activities using the drop-down list. Items Item #1 Acquiring resources (assets) that an organization plans to use to acquire and sell its products or services Item #2 Resources contributed by creditors Item #3 Disposing of resources (assets) that an organization uses to acquire and sell its products or services Item #4 Sales and revenues Item #15 Resources contributed by the owner along with any income the owner leaves in the organization Activities Investing Financing Operating Financing...

assify the following business activities using the drop-down list. Items Item #1 Acquiring resources (assets) that an organization plans to use to acquire and sell its products or services Item #2 Resources contributed by creditors Item #3 Disposing of resources (assets) that an organization uses to acquire and sell its products or services Item #4 Sales and revenues Item #15 Resources contributed by the owner along with any income the owner leaves in the organization Activities Investing Financing Operating Financing...

Drop area The following is a partial list of items that wluld appear on the various financial statements. Drag each item into the correct column to identify the financial statement. Balance Sheet Income Statement Statement of Retained Earnings drop item here drop item drop item here drop item here drop Item here drop item here drop item here drop item hore drop Item here drop Item here drop item here drop item here Statement of Cash Flows drop item here...

Drop area The following is a partial list of items that wluld appear on the various financial statements. Drag each item into the correct column to identify the financial statement. Balance Sheet Income Statement Statement of Retained Earnings drop item here drop item drop item here drop item here drop Item here drop item here drop item here drop item hore drop Item here drop Item here drop item here drop item here Statement of Cash Flows drop item here...

Identify which accounting principle or assumption best describes each of the following practices: 1. Stark Company's accounting system maintains the equipment account as if the business will continue operating and not close. 2. Mike Derr owns both Salling Passions and Dockside Digs. In preparing financial statements for Dockside Digs, Mike makes sure that the expense transactions of Sailing Passions are kept separate from Dockside Digs's transactions and financial statements. 3. If $51 thousand cash is paid to buy land, the...

Identify which accounting principle or assumption best describes each of the following practices: 1. Stark Company's accounting system maintains the equipment account as if the business will continue operating and not close. 2. Mike Derr owns both Salling Passions and Dockside Digs. In preparing financial statements for Dockside Digs, Mike makes sure that the expense transactions of Sailing Passions are kept separate from Dockside Digs's transactions and financial statements. 3. If $51 thousand cash is paid to buy land, the...

Identify each of the following items as revenues, expenses, or withdrawals from the drop down provided. 1. Salaries 2. Owner withdrawal 3. Sales revenue 4. Cost of sales Expenses Revenues 5. Printing 6. Dividend income 7. Freight 8. Insurance Withdrawals

Identify each of the following items as revenues, expenses, or withdrawals from the drop down provided. 1. Salaries 2. Owner withdrawal 3. Sales revenue 4. Cost of sales Expenses Revenues 5. Printing 6. Dividend income 7. Freight 8. Insurance Withdrawals

Most questions answered within 3 hours.

-

Suppose we have a binomial experiment in which success is

defined to be a particular quality...

asked 13 minutes ago -

march the type of cellular control with the description: enzyme

induction and the enzyme repression. How...

asked 23 minutes ago -

Brief Exercise 5-09 (Part Level Submission)

The following information relates to Blue Spruce Corp. for the...

asked 23 minutes ago -

An unknown amount of a compound with a molecular mass of 284.04

g/mol is dissolved in...

asked 28 minutes ago -

You are at rest at a stop sign. There is another stop sign that

is 100...

asked 29 minutes ago -

Calculate the equilibrium electrode potential for Fe3+/Fe2+

redox system, if the initial concentration of Fe2+ is...

asked 33 minutes ago -

Describe in detail with graph and diagram how bonding force,

bonding curves and bonding energy at...

asked 50 minutes ago -

Gingerbread cookies become inedible if not eaten quickly enough.

Clarence is trying to determine how many...

asked 45 minutes ago -

A

crane lifts a 200 kg block a height of 10 m in 18 seconds. What...

asked 48 minutes ago -

A 12.0-g bullet is fired horizontally into a 115-g wooden block

that is initially at rest...

asked 49 minutes ago -

Which DNA primer would have the HIGHEST melting temperature?

Question 17 options:

a)

GCATCGGC

b)

AATCGGAT...

asked 57 minutes ago -

what is the charge on the chromium ion in Cr2O3.

a -3

b -2

c 0...

asked 57 minutes ago