You plan to invest in the Kish Hedge Fund, which has total capital of $500 million invested in fi...

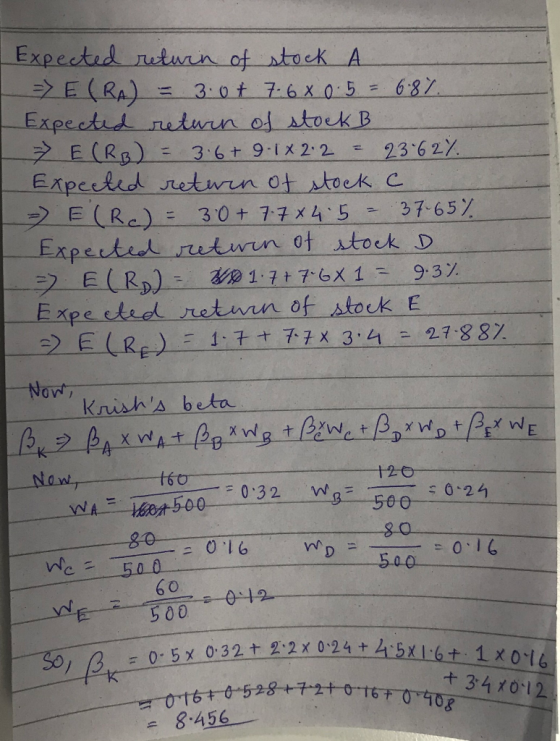

You plan to invest in the Kish Hedge Fund, which has total capital of $500 million invested in five stocks: Stock Investment Stock's Beta Coefficient A $160 million 0.5 B 120 million 2.2 C 80 million 4.5 D 80 million 1.0 E 60 million 3.4 Kish's beta coefficient can be found as a weighted average of its stocks' betas. The risk-free rate is 3%, and you believe the following probability distribution for future market returns is realistic: Probability Market Return 0.1 (5%) 0.2 10 0.4 12 0.2 14 0.1 15 What is the equation for the Security Market Line (SML)? (Hint: First determine the expected market return.) ri = 3.0% + (7.6%)bi ri = 3.6% + (9.1%)bi ri = 3.0% + (7.7%)bi ri = 1.7% + (7.6%)bi ri = 1.7% + (7.7%)bi Calculate Kish's required rate of return. Do not round intermediate calculations. Round your answer to two decimal places. % Suppose Rick Kish, the president, receives a proposal from a company seeking new capital. The amount needed to take a position in the stock is $50 million, it has an expected return of 14%, and its estimated beta is 1.5. Should Kish invest in the new company? The new stock be purchased. At what expected rate of return should Kish be indifferent to purchasing the stock? Round your answer to two decimal places. % Check My Work (2 remaining) Icon Key Previous Question 18 of 18

Homework Answers

Add Answer to:

You plan to invest in the Kish Hedge Fund, which has total capital of $500 million invested in fi...

You plan to invest in the Kish Hedge Fund, which has total capital of $500 million...

You plan to invest in the Kish Hedge Fund, which has total capital of $500 million invested in five stocks: Stock Investment Stock's Beta Coefficient A $160 million 0.4 B 120 million 1.3 C 80 million 1.9 D 80 million 1.0 E 60 million 1.8 Kish's beta coefficient can be found as a weighted average of its stocks' betas. The risk-free rate is 3%, and you believe the following probability distribution for future market returns is realistic: Probability Market Return...

You plan to invest in the Kish Hedge Fund, which has total capital of $500 million...

You plan to invest in the Kish Hedge Fund, which has total capital of $500 million invested in five stocks: Stock Investment Stock's Beta Coefficient A $160 million 0.8 B 120 million 1.6 C 80 million 1.7 D 80 million 1.0 E 60 million 1.9 Kish's beta coefficient can be found as a weighted average of its stocks' betas. The risk-free rate is 6%, and you believe the following probability distribution for future market returns is realistic: Probability Market Return...

You plan to invest in the Kish Hedge Fund, which has total capital of $500 million...

You plan to invest in the Kish Hedge Fund, which has total capital of $500 million invested in five stocks: Stock Stock's Beta Coefficient 1.6 Investment $160 million 120 million 80 million 80 million 60 million 2.0 1.0 1.3 Kish's beta coefficient can be found as a weighted average of its stocks' betas. The risk-free rate is 4%, and you believe the following probability distribution for future market returns is realistic: Probability Market Return -26% 0.1 0.2 0.4 0.2 28...

You plan to invest in the Kish Hedge Fund, which has total capital of $500 million invested in five stocks: Stock Stock's Beta Coefficient 1.6 Investment $160 million 120 million 80 million 80 million 60 million 2.0 1.0 1.3 Kish's beta coefficient can be found as a weighted average of its stocks' betas. The risk-free rate is 4%, and you believe the following probability distribution for future market returns is realistic: Probability Market Return -26% 0.1 0.2 0.4 0.2 28...

You plan to invest in the Kish Hedge Fund, which has total capital of R500 million...

You plan to invest in the Kish Hedge Fund, which has total capital of R500 million invested in five stocks: Stock Investment Stock's Beta Coefficient A 160 million 0.5 B 120 million 1.2 C 80 million 1.8 D 80 million 1.0 E 60 million 1.6 Kish's beta coefficient can be found as a weighted average of its stocks' betas. The risk-free rate is 6%, and you believe the following probability distribution for future market returns is realistic: Probability Market Return...

ignore question 6 i forgot to crop the screenshot 5. You plan to invest in the...

ignore question 6 i forgot to crop the screenshot

5. You plan to invest in the Kish Hedge Fund, which has total capital of $500 million invested in five stocks: Stock Investment Beta А $160 million 0.5 B 120 million 1.2 с 80 million 1.8 D 80 million 1.0 60 million 1.6 Kish's beta coefficient can be found as a weighted average of its stocks" betas. The risk-free rate is 6% and you believe that following probability distribution for future...

ignore question 6 i forgot to crop the screenshot

5. You plan to invest in the Kish Hedge Fund, which has total capital of $500 million invested in five stocks: Stock Investment Beta А $160 million 0.5 B 120 million 1.2 с 80 million 1.8 D 80 million 1.0 60 million 1.6 Kish's beta coefficient can be found as a weighted average of its stocks" betas. The risk-free rate is 6% and you believe that following probability distribution for future...

5. The 3410 Investment Fund has total capital of $500 mil Stock $160 million 32 4.0...

5. The 3410 Investment Fund has total capital of $500 mil Stock $160 million 32 4.0 1.0 64 16 al of $500 million invested in 5 stocks: Investment Stock's Beta 0.5 -16 $120 million 24 2.0 4 $80 million 16 $80 million 16 $60 million ez 3.0 56 The current risk-free rate is 6%, whereas market returns have the following tay distribution: Probability Market Return 2 0.1 0.2 7% of 9% 2018 ER = .06+108 [11] =.258 0.4 0.2 11%...

5. The 3410 Investment Fund has total capital of $500 mil Stock $160 million 32 4.0 1.0 64 16 al of $500 million invested in 5 stocks: Investment Stock's Beta 0.5 -16 $120 million 24 2.0 4 $80 million 16 $80 million 16 $60 million ez 3.0 56 The current risk-free rate is 6%, whereas market returns have the following tay distribution: Probability Market Return 2 0.1 0.2 7% of 9% 2018 ER = .06+108 [11] =.258 0.4 0.2 11%...

Consider the equation for the Capital Asset Pricing Model (CAPM): îi = rrF + (îm-PRE) *...

Consider the equation for the Capital Asset Pricing Model (CAPM): îi = rrF + (îm-PRE) * Cov(ļi, "M) 02M In this equation, the term Cov (ri, rm)lo?m represents the A) Covariance between stock i and the market B) stock's beta coefficient C) variants of markets return Suppose that the market's average excess return on stocks is 6.00% and that the risk-free rate is 2.00%. Complete the following table by computing expected returns to stocks for each beta coefficient using the...

Consider the equation for the Capital Asset Pricing Model (CAPM): îi = rrF + (îm-PRE) * Cov(ļi, "M) 02M In this equation, the term Cov (ri, rm)lo?m represents the A) Covariance between stock i and the market B) stock's beta coefficient C) variants of markets return Suppose that the market's average excess return on stocks is 6.00% and that the risk-free rate is 2.00%. Complete the following table by computing expected returns to stocks for each beta coefficient using the...

29. A mutual fund manager has a $40.00 million portfolio with a beta of 1.00. The...

29. A mutual fund manager has a $40.00 million portfolio with a beta of 1.00. The risk-free rate is 4.25%, and the market risk premium is 6.00%. The manager expects to receive an additional $29.50 million which she plans to invest in additional stocks. After investing the additional funds, she wants the fund's required and expected return to be 13.00%. What must the average beta of the new stocks be to achieve the target required rate of return? Do not...

assume that you are the portfolio manager of the SF Fund, a $3 million hedge fund...

assume that you are the portfolio manager of the SF Fund, a $3 million hedge fund that contains the following stocks. The required rate of return on the market is 11.00% and the risk-free rate is 2.00%, What rate of return should investors expect and require) on this fund? Do not round your intermediate calculations. Stock Amount Beta $525.000 5675,000 0.50 $1.300.000 1.40 5500,000 0.75 $3,000,000 10.68% 9.88% 13.67% 11.49% provirus

assume that you are the portfolio manager of the SF Fund, a $3 million hedge fund that contains the following stocks. The required rate of return on the market is 11.00% and the risk-free rate is 2.00%, What rate of return should investors expect and require) on this fund? Do not round your intermediate calculations. Stock Amount Beta $525.000 5675,000 0.50 $1.300.000 1.40 5500,000 0.75 $3,000,000 10.68% 9.88% 13.67% 11.49% provirus

3. The basics of the Capital Asset Pricing Model Which of the following are assumptions of...

3. The basics of the Capital Asset Pricing Model Which of the following are assumptions of the Capital Asset Pricing Model (CAPM)? Check all that apply. Expected returns are based on individual investor risk sensitivity. Investors have homogeneous expectations. There are no taxes. All investors focus on a single holding period. Consider the equation for the Capital Asset Pricing Model (CAPM): = TRF + OM-TRF) x Cover o In this equation, the term (OM-TRF) represents the Suppose that the market's...

3. The basics of the Capital Asset Pricing Model Which of the following are assumptions of the Capital Asset Pricing Model (CAPM)? Check all that apply. Expected returns are based on individual investor risk sensitivity. Investors have homogeneous expectations. There are no taxes. All investors focus on a single holding period. Consider the equation for the Capital Asset Pricing Model (CAPM): = TRF + OM-TRF) x Cover o In this equation, the term (OM-TRF) represents the Suppose that the market's...

You plan to invest in the Kish Hedge Fund, which has total capital of $500 million invested in five stocks: Stock Stock's Beta Coefficient 1.6 Investment $160 million 120 million 80 million 80 million 60 million 2.0 1.0 1.3 Kish's beta coefficient can be found as a weighted average of its stocks' betas. The risk-free rate is 4%, and you believe the following probability distribution for future market returns is realistic: Probability Market Return -26% 0.1 0.2 0.4 0.2 28...

You plan to invest in the Kish Hedge Fund, which has total capital of $500 million invested in five stocks: Stock Stock's Beta Coefficient 1.6 Investment $160 million 120 million 80 million 80 million 60 million 2.0 1.0 1.3 Kish's beta coefficient can be found as a weighted average of its stocks' betas. The risk-free rate is 4%, and you believe the following probability distribution for future market returns is realistic: Probability Market Return -26% 0.1 0.2 0.4 0.2 28...

ignore question 6 i forgot to crop the screenshot

5. You plan to invest in the Kish Hedge Fund, which has total capital of $500 million invested in five stocks: Stock Investment Beta А $160 million 0.5 B 120 million 1.2 с 80 million 1.8 D 80 million 1.0 60 million 1.6 Kish's beta coefficient can be found as a weighted average of its stocks" betas. The risk-free rate is 6% and you believe that following probability distribution for future...

ignore question 6 i forgot to crop the screenshot

5. You plan to invest in the Kish Hedge Fund, which has total capital of $500 million invested in five stocks: Stock Investment Beta А $160 million 0.5 B 120 million 1.2 с 80 million 1.8 D 80 million 1.0 60 million 1.6 Kish's beta coefficient can be found as a weighted average of its stocks" betas. The risk-free rate is 6% and you believe that following probability distribution for future...

5. The 3410 Investment Fund has total capital of $500 mil Stock $160 million 32 4.0 1.0 64 16 al of $500 million invested in 5 stocks: Investment Stock's Beta 0.5 -16 $120 million 24 2.0 4 $80 million 16 $80 million 16 $60 million ez 3.0 56 The current risk-free rate is 6%, whereas market returns have the following tay distribution: Probability Market Return 2 0.1 0.2 7% of 9% 2018 ER = .06+108 [11] =.258 0.4 0.2 11%...

5. The 3410 Investment Fund has total capital of $500 mil Stock $160 million 32 4.0 1.0 64 16 al of $500 million invested in 5 stocks: Investment Stock's Beta 0.5 -16 $120 million 24 2.0 4 $80 million 16 $80 million 16 $60 million ez 3.0 56 The current risk-free rate is 6%, whereas market returns have the following tay distribution: Probability Market Return 2 0.1 0.2 7% of 9% 2018 ER = .06+108 [11] =.258 0.4 0.2 11%...

Consider the equation for the Capital Asset Pricing Model (CAPM): îi = rrF + (îm-PRE) * Cov(ļi, "M) 02M In this equation, the term Cov (ri, rm)lo?m represents the A) Covariance between stock i and the market B) stock's beta coefficient C) variants of markets return Suppose that the market's average excess return on stocks is 6.00% and that the risk-free rate is 2.00%. Complete the following table by computing expected returns to stocks for each beta coefficient using the...

Consider the equation for the Capital Asset Pricing Model (CAPM): îi = rrF + (îm-PRE) * Cov(ļi, "M) 02M In this equation, the term Cov (ri, rm)lo?m represents the A) Covariance between stock i and the market B) stock's beta coefficient C) variants of markets return Suppose that the market's average excess return on stocks is 6.00% and that the risk-free rate is 2.00%. Complete the following table by computing expected returns to stocks for each beta coefficient using the...

assume that you are the portfolio manager of the SF Fund, a $3 million hedge fund that contains the following stocks. The required rate of return on the market is 11.00% and the risk-free rate is 2.00%, What rate of return should investors expect and require) on this fund? Do not round your intermediate calculations. Stock Amount Beta $525.000 5675,000 0.50 $1.300.000 1.40 5500,000 0.75 $3,000,000 10.68% 9.88% 13.67% 11.49% provirus

assume that you are the portfolio manager of the SF Fund, a $3 million hedge fund that contains the following stocks. The required rate of return on the market is 11.00% and the risk-free rate is 2.00%, What rate of return should investors expect and require) on this fund? Do not round your intermediate calculations. Stock Amount Beta $525.000 5675,000 0.50 $1.300.000 1.40 5500,000 0.75 $3,000,000 10.68% 9.88% 13.67% 11.49% provirus

3. The basics of the Capital Asset Pricing Model Which of the following are assumptions of the Capital Asset Pricing Model (CAPM)? Check all that apply. Expected returns are based on individual investor risk sensitivity. Investors have homogeneous expectations. There are no taxes. All investors focus on a single holding period. Consider the equation for the Capital Asset Pricing Model (CAPM): = TRF + OM-TRF) x Cover o In this equation, the term (OM-TRF) represents the Suppose that the market's...

3. The basics of the Capital Asset Pricing Model Which of the following are assumptions of the Capital Asset Pricing Model (CAPM)? Check all that apply. Expected returns are based on individual investor risk sensitivity. Investors have homogeneous expectations. There are no taxes. All investors focus on a single holding period. Consider the equation for the Capital Asset Pricing Model (CAPM): = TRF + OM-TRF) x Cover o In this equation, the term (OM-TRF) represents the Suppose that the market's...

Most questions answered within 3 hours.

-

Write a c/c++ program to read a list of students from a file and

create a...

asked 2 minutes ago -

Identify two different methods for collecting data in

qualitative research. What are the benefits and challenges...

asked 3 minutes ago -

I am suppose to have my array before the main class but I am

getting the...

asked 5 minutes ago -

Your task is to design the page table for the 32bit Pentium

microprocessor. Answer the following...

asked 11 minutes ago -

The Paradise Shoes Company has estimated its weekly TVC function

from data collected over the past...

asked 10 minutes ago -

A researcher wishes to study the cumulative effects of several

combinations of HIV drugs. There are...

asked 10 minutes ago -

Although Epicurus advocates pursuing pleasure for the

good life, discuss a few reasons why he does...

asked 27 minutes ago -

Problem 1: Present entries to record the selected transactions

described below:

(a)

Issued $2,790,000 of 5-year,...

asked 34 minutes ago -

Using technology to support HR activities increases:

a.

the efficiency of the administrative HR functions.

b....

asked 34 minutes ago -

1. List the features used to classify leaf

types.

2. List some characteristics that are shared...

asked 39 minutes ago -

The three elements of Value Proposition, Key Customers, and

Capabilities operate within an environment. Which of...

asked 42 minutes ago -

Katelynn, a physician, earns $200,000 from her medical practice

in the current year. She receives $45,000...

asked 49 minutes ago