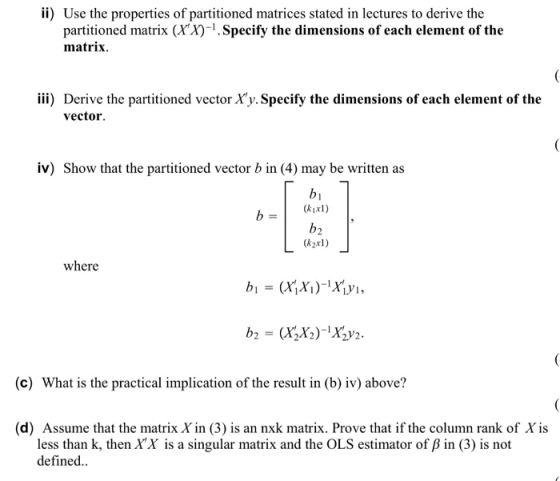

ii) Use the properties of partitioned matrices stated in lectures to derive the partitioned matrix (Xx)-1.Specify the dimensions of each element of the matrix iii) Derive the partitioned vector X'y. Specify the dimensions of each element of the vector. iv) Show that the partitioned vector b in (4) may be written as (kixl) b2 (k2x) where (c) What is the practical implication of the result in (b) iv) above? (d) Assume that the matrix X in (3) is an nxk matrix. Prove that if the column rank of Xis less than k, then X'X is a singular matrix and the OLS estimator of B in (3) is not defined.

Homework Answers

Add Answer to:

Consider two separate linear regression models and For concreteness, assume that the vector yi co...

Please help to solve that question very appreciate if you can help me to solve all the part...

please help to solve that question

very appreciate if you can help me to solve all the part as my due

date coming soon but got stuck in this question.

Consider two separate linear regression models and For concreteness, assume that the vector yi contains observations on the wealth ofn randomly selected individuals in Australia and y2 contains observations on the wealth of n randomly selected individuals in New Zealand. The matrix Xi contains n observations on ki explanatory variables...

please help to solve that question

very appreciate if you can help me to solve all the part as my due

date coming soon but got stuck in this question.

Consider two separate linear regression models and For concreteness, assume that the vector yi contains observations on the wealth ofn randomly selected individuals in Australia and y2 contains observations on the wealth of n randomly selected individuals in New Zealand. The matrix Xi contains n observations on ki explanatory variables...

Please help me to solve part b and c . and please dont copy my answer in part a and then post it ...

please help me to solve part b and c .

and please dont copy my answer in part a and then post it as

an answer.

thanks

Consider two separate linear regression models and For concreteness, assume that the vector yi contains observations on the wealth ofn randomly selected individuals in Australia and y2 contains observations on the wealth of n randomly selected individuals in New Zealand. The matrix Xi contains n observations on ki explanatory variables which are believed...

please help me to solve part b and c .

and please dont copy my answer in part a and then post it as

an answer.

thanks

Consider two separate linear regression models and For concreteness, assume that the vector yi contains observations on the wealth ofn randomly selected individuals in Australia and y2 contains observations on the wealth of n randomly selected individuals in New Zealand. The matrix Xi contains n observations on ki explanatory variables which are believed...

Q. 1 Consider the multiple linear regression model Y = x3 + €, where e indep...

Q. 1 Consider the multiple linear regression model Y = x3 + €, where e indep MV N(0,0²V) and V +In is a diagonal matrix. a) Derive the weighted least squares estimator for B, i.e., Owls. b) Show Bwis is an unbiased estimator for B. c) Derive the variances of w ls and the OLS estimator of 8. Is the OLS estimator of still the BLUE? In one sentence, explain why or why not.

Q. 1 Consider the multiple linear regression model Y = x3 + €, where e indep MV N(0,0²V) and V +In is a diagonal matrix. a) Derive the weighted least squares estimator for B, i.e., Owls. b) Show Bwis is an unbiased estimator for B. c) Derive the variances of w ls and the OLS estimator of 8. Is the OLS estimator of still the BLUE? In one sentence, explain why or why not.

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector,...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector, on an n x (p+1) full rank matrix X. As usual, H = X(XT X)-1 XT is the hat matrix with elements hij at the ith row and jth column. The residual is e; = yi - Ýi. (a) (7 points) Let Y be an n x 1 vector with 1 as its first element and Os elsewhere. Show that the elements of the...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector, on an n x (p+1) full rank matrix X. As usual, H = X(XT X)-1 XT is the hat matrix with elements hij at the ith row and jth column. The residual is e; = yi - Ýi. (a) (7 points) Let Y be an n x 1 vector with 1 as its first element and Os elsewhere. Show that the elements of the...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector,...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector, on an n x (p+1) full rank matrix X. As usual, H = X(XT X)-1 XT is the hat matrix with elements hij at the ith row and jth column. The residual is e; = yi - Ýi. (a) (7 points) Let Y be an n x 1 vector with 1 as its first element and Os elsewhere. Show that the elements of the...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector, on an n x (p+1) full rank matrix X. As usual, H = X(XT X)-1 XT is the hat matrix with elements hij at the ith row and jth column. The residual is e; = yi - Ýi. (a) (7 points) Let Y be an n x 1 vector with 1 as its first element and Os elsewhere. Show that the elements of the...

3. Let y = (yi..... Yn) be a set of re- sponses, and consider the linear...

3. Let y = (yi..... Yn) be a set of re- sponses, and consider the linear model y= +E, where u = (1, ..., and e is a vector of zero mean, uncorrelated errors with variance o'. This is a linear model in which the responses have a constant but unknown mean . We will call this model the location model. (a) If we write the location model in the usual form of the linear model y = X 8+...

3. Let y = (yi..... Yn) be a set of re- sponses, and consider the linear model y= +E, where u = (1, ..., and e is a vector of zero mean, uncorrelated errors with variance o'. This is a linear model in which the responses have a constant but unknown mean . We will call this model the location model. (a) If we write the location model in the usual form of the linear model y = X 8+...

3. In the multiple regression model shown in the previous question, which one of the following st...

3. In the multiple regression model shown in the previous question, which one of the following statements is incorrect: (b) The sum of squared residuals is the square of the length of the vector ü (c) The residual vector is orthogonal to each of the columns of X (d) The square of the length of y is equal to the square of the length of y plus the square of the length of û by the Pythagoras theorem In all...

3. In the multiple regression model shown in the previous question, which one of the following statements is incorrect: (b) The sum of squared residuals is the square of the length of the vector ü (c) The residual vector is orthogonal to each of the columns of X (d) The square of the length of y is equal to the square of the length of y plus the square of the length of û by the Pythagoras theorem In all...

3. Consider the multiple linear regression model where Xii, . .. , Xp-i.i are observed covariate values for observation...

3. Consider the multiple linear regression model where Xii, . .. , Xp-i.i are observed covariate values for observation i, and εί udN(0, σ2) (a) What is the interpretation of in this model? (b) Write the matrix form of the model. Label the response vector, design matrix, coefficient vecto and error vector, and specify the dimensions and elements for each. (c) Write the likelihood, log-likelihood, and 쓿 in matrix form. (d) Solve = 0 for β, the MLE of the...

3. Consider the multiple linear regression model where Xii, . .. , Xp-i.i are observed covariate values for observation i, and εί udN(0, σ2) (a) What is the interpretation of in this model? (b) Write the matrix form of the model. Label the response vector, design matrix, coefficient vecto and error vector, and specify the dimensions and elements for each. (c) Write the likelihood, log-likelihood, and 쓿 in matrix form. (d) Solve = 0 for β, the MLE of the...

3. Consider the multiple linear regression model iid where Xi, . . . ,Xp-1 ,i are observed covariate values for observation i, and Ei ~N(0,ơ2) (a) What is the interpretation of B1 in this model? (b)...

3. Consider the multiple linear regression model iid where Xi, . . . ,Xp-1 ,i are observed covariate values for observation i, and Ei ~N(0,ơ2) (a) What is the interpretation of B1 in this model? (b) Write the matrix form of the model. Label the response vector, design matrix, coefficient vector, and error vector, and specify the dimensions and elements for each. (c) Write the likelihood, log-likelihood, and in matrix form. aB (d) Solve : 0 for β, the MLE...

3. Consider the multiple linear regression model iid where Xi, . . . ,Xp-1 ,i are observed covariate values for observation i, and Ei ~N(0,ơ2) (a) What is the interpretation of B1 in this model? (b) Write the matrix form of the model. Label the response vector, design matrix, coefficient vector, and error vector, and specify the dimensions and elements for each. (c) Write the likelihood, log-likelihood, and in matrix form. aB (d) Solve : 0 for β, the MLE...

linear stat modeling & regression please , i need the solution for Q3, but i copy Q2 because you need info from Q2 in order to answer Q3. 2) Suppose you have multiple regression set up YxXB...

linear stat modeling & regression

please ,

i need the solution for Q3, but i copy Q2 because you need

info from Q2 in order to answer Q3.

2) Suppose you have multiple regression set up YxXBp The ridge regression estimator is given by Here, llell'-Σ.< where is a vector of Vik. a) Find the expectation and variance-covariance matrix of Bridge, when X'X is a diagonal matrix with each diagonal entry is eqal to. Com pare these variances with the...

linear stat modeling & regression

please ,

i need the solution for Q3, but i copy Q2 because you need

info from Q2 in order to answer Q3.

2) Suppose you have multiple regression set up YxXBp The ridge regression estimator is given by Here, llell'-Σ.< where is a vector of Vik. a) Find the expectation and variance-covariance matrix of Bridge, when X'X is a diagonal matrix with each diagonal entry is eqal to. Com pare these variances with the...

please help to solve that question

very appreciate if you can help me to solve all the part as my due

date coming soon but got stuck in this question.

Consider two separate linear regression models and For concreteness, assume that the vector yi contains observations on the wealth ofn randomly selected individuals in Australia and y2 contains observations on the wealth of n randomly selected individuals in New Zealand. The matrix Xi contains n observations on ki explanatory variables...

please help to solve that question

very appreciate if you can help me to solve all the part as my due

date coming soon but got stuck in this question.

Consider two separate linear regression models and For concreteness, assume that the vector yi contains observations on the wealth ofn randomly selected individuals in Australia and y2 contains observations on the wealth of n randomly selected individuals in New Zealand. The matrix Xi contains n observations on ki explanatory variables...

please help me to solve part b and c .

and please dont copy my answer in part a and then post it as

an answer.

thanks

Consider two separate linear regression models and For concreteness, assume that the vector yi contains observations on the wealth ofn randomly selected individuals in Australia and y2 contains observations on the wealth of n randomly selected individuals in New Zealand. The matrix Xi contains n observations on ki explanatory variables which are believed...

please help me to solve part b and c .

and please dont copy my answer in part a and then post it as

an answer.

thanks

Consider two separate linear regression models and For concreteness, assume that the vector yi contains observations on the wealth ofn randomly selected individuals in Australia and y2 contains observations on the wealth of n randomly selected individuals in New Zealand. The matrix Xi contains n observations on ki explanatory variables which are believed...

Q. 1 Consider the multiple linear regression model Y = x3 + €, where e indep MV N(0,0²V) and V +In is a diagonal matrix. a) Derive the weighted least squares estimator for B, i.e., Owls. b) Show Bwis is an unbiased estimator for B. c) Derive the variances of w ls and the OLS estimator of 8. Is the OLS estimator of still the BLUE? In one sentence, explain why or why not.

Q. 1 Consider the multiple linear regression model Y = x3 + €, where e indep MV N(0,0²V) and V +In is a diagonal matrix. a) Derive the weighted least squares estimator for B, i.e., Owls. b) Show Bwis is an unbiased estimator for B. c) Derive the variances of w ls and the OLS estimator of 8. Is the OLS estimator of still the BLUE? In one sentence, explain why or why not.

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector, on an n x (p+1) full rank matrix X. As usual, H = X(XT X)-1 XT is the hat matrix with elements hij at the ith row and jth column. The residual is e; = yi - Ýi. (a) (7 points) Let Y be an n x 1 vector with 1 as its first element and Os elsewhere. Show that the elements of the...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector, on an n x (p+1) full rank matrix X. As usual, H = X(XT X)-1 XT is the hat matrix with elements hij at the ith row and jth column. The residual is e; = yi - Ýi. (a) (7 points) Let Y be an n x 1 vector with 1 as its first element and Os elsewhere. Show that the elements of the...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector, on an n x (p+1) full rank matrix X. As usual, H = X(XT X)-1 XT is the hat matrix with elements hij at the ith row and jth column. The residual is e; = yi - Ýi. (a) (7 points) Let Y be an n x 1 vector with 1 as its first element and Os elsewhere. Show that the elements of the...

Considering multiple linear regression models, we compute the regression of Y, an n x 1 vector, on an n x (p+1) full rank matrix X. As usual, H = X(XT X)-1 XT is the hat matrix with elements hij at the ith row and jth column. The residual is e; = yi - Ýi. (a) (7 points) Let Y be an n x 1 vector with 1 as its first element and Os elsewhere. Show that the elements of the...

3. Let y = (yi..... Yn) be a set of re- sponses, and consider the linear model y= +E, where u = (1, ..., and e is a vector of zero mean, uncorrelated errors with variance o'. This is a linear model in which the responses have a constant but unknown mean . We will call this model the location model. (a) If we write the location model in the usual form of the linear model y = X 8+...

3. Let y = (yi..... Yn) be a set of re- sponses, and consider the linear model y= +E, where u = (1, ..., and e is a vector of zero mean, uncorrelated errors with variance o'. This is a linear model in which the responses have a constant but unknown mean . We will call this model the location model. (a) If we write the location model in the usual form of the linear model y = X 8+...

3. In the multiple regression model shown in the previous question, which one of the following statements is incorrect: (b) The sum of squared residuals is the square of the length of the vector ü (c) The residual vector is orthogonal to each of the columns of X (d) The square of the length of y is equal to the square of the length of y plus the square of the length of û by the Pythagoras theorem In all...

3. In the multiple regression model shown in the previous question, which one of the following statements is incorrect: (b) The sum of squared residuals is the square of the length of the vector ü (c) The residual vector is orthogonal to each of the columns of X (d) The square of the length of y is equal to the square of the length of y plus the square of the length of û by the Pythagoras theorem In all...

3. Consider the multiple linear regression model where Xii, . .. , Xp-i.i are observed covariate values for observation i, and εί udN(0, σ2) (a) What is the interpretation of in this model? (b) Write the matrix form of the model. Label the response vector, design matrix, coefficient vecto and error vector, and specify the dimensions and elements for each. (c) Write the likelihood, log-likelihood, and 쓿 in matrix form. (d) Solve = 0 for β, the MLE of the...

3. Consider the multiple linear regression model where Xii, . .. , Xp-i.i are observed covariate values for observation i, and εί udN(0, σ2) (a) What is the interpretation of in this model? (b) Write the matrix form of the model. Label the response vector, design matrix, coefficient vecto and error vector, and specify the dimensions and elements for each. (c) Write the likelihood, log-likelihood, and 쓿 in matrix form. (d) Solve = 0 for β, the MLE of the...

3. Consider the multiple linear regression model iid where Xi, . . . ,Xp-1 ,i are observed covariate values for observation i, and Ei ~N(0,ơ2) (a) What is the interpretation of B1 in this model? (b) Write the matrix form of the model. Label the response vector, design matrix, coefficient vector, and error vector, and specify the dimensions and elements for each. (c) Write the likelihood, log-likelihood, and in matrix form. aB (d) Solve : 0 for β, the MLE...

3. Consider the multiple linear regression model iid where Xi, . . . ,Xp-1 ,i are observed covariate values for observation i, and Ei ~N(0,ơ2) (a) What is the interpretation of B1 in this model? (b) Write the matrix form of the model. Label the response vector, design matrix, coefficient vector, and error vector, and specify the dimensions and elements for each. (c) Write the likelihood, log-likelihood, and in matrix form. aB (d) Solve : 0 for β, the MLE...

linear stat modeling & regression

please ,

i need the solution for Q3, but i copy Q2 because you need

info from Q2 in order to answer Q3.

2) Suppose you have multiple regression set up YxXBp The ridge regression estimator is given by Here, llell'-Σ.< where is a vector of Vik. a) Find the expectation and variance-covariance matrix of Bridge, when X'X is a diagonal matrix with each diagonal entry is eqal to. Com pare these variances with the...

linear stat modeling & regression

please ,

i need the solution for Q3, but i copy Q2 because you need

info from Q2 in order to answer Q3.

2) Suppose you have multiple regression set up YxXBp The ridge regression estimator is given by Here, llell'-Σ.< where is a vector of Vik. a) Find the expectation and variance-covariance matrix of Bridge, when X'X is a diagonal matrix with each diagonal entry is eqal to. Com pare these variances with the...

Most questions answered within 3 hours.

-

The average length of time between arrivals at a turnpike

toll-booth is 26 seconds. What is...

asked 27 minutes ago -

(a) A piston at 6.1 atm contains a gas that occupies a volume of

3.5 L....

asked 1 hour ago -

Please answer true or false. Words

cannot be changed or added in to make it true...

asked 1 hour ago -

An empty test tube weighs 15.923 grams. Then,

MgCl2•6H2O is added into the test tube. After...

asked 1 hour ago -

Assume memory access is 10 units of time and disk access is

10000 units of time....

asked 1 hour ago -

1. Are all good samples random?

2. Magazines often report surveys giving statistics such as “63%...

asked 2 hours ago -

Under all the various types of market structures, firms

must eventually earn some economic profits for...

asked 2 hours ago -

Consider the following fitness regime for a single locus trait

with two co-dominant alleles: w11 =...

asked 2 hours ago -

A large cable company reports the following.

80% of its customers subscribe to its cable TV...

asked 2 hours ago -

Please answer the question in brief.

Discuss the role of ERP in organizations. Are ERP tools...

asked 2 hours ago -

Discuss the pros and cons of collaborative software such

as SameTime. Does it increase productivity? What...

asked 2 hours ago -

Buying your in-laws a gift because it’s expected is

due to the ____________ motive of gift-giving....

asked 2 hours ago