Homework Answers

If an autoregressive moving average model (ARMA) model is assumed for the error variance, the model is a generalized autoregressive conditional heteroskedasticity (GARCH) model.[2]

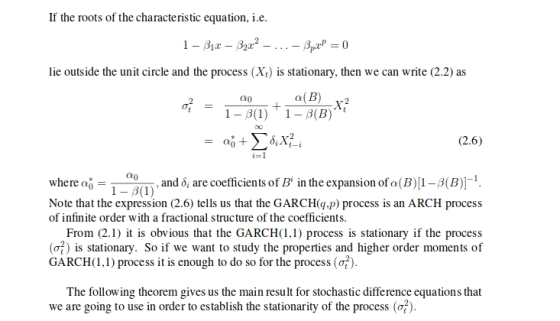

In that case, the GARCH (p, q) model (where

p is the order of the GARCH terms

Generally, when testing for heteroskedasticity in econometric models, the best test is the White test. However, when dealing with time series data, this means to test for ARCH and GARCH errors.

Exponentially weighted moving average (EWMA) is an alternative model in a separate class of exponential smoothing models. As an alternative to GARCH modelling it has some attractive properties such as a greater weight upon more recent observations, but also drawbacks such as an arbitrary decay factor that introduces subjectivity into the estimation.

GARCH(p, q) model specification

The lag length p of a GARCH(p, q) process is established in three steps:

- Estimate the best fitting AR(q) model

.

- Compute and plot the autocorrelations of

by

- The asymptotic, that is for large samples, standard deviation

of

is

. Individual values that are larger than this indicate GARCH errors. To estimate the total number of lags, use the Ljung-Box test until the value of these are less than, say, 10% significant. The Ljung-Box Q-statistic follows

distribution with n degrees of freedom if the squared residuals

are uncorrelated. It is recommended to consider up to T/4 values of n. The null hypothesis states that there are no ARCH or GARCH errors. Rejecting the null thus means that such errors exist in the conditional variance.

.

. by

by

is

is  . Individual values that are larger than this indicate GARCH

errors. To estimate the total number of lags, use the Ljung-Box

test until the value of these are less than, say, 10% significant.

The Ljung-Box Q-statistic follows

. Individual values that are larger than this indicate GARCH

errors. To estimate the total number of lags, use the Ljung-Box

test until the value of these are less than, say, 10% significant.

The Ljung-Box Q-statistic follows  distribution with n degrees of freedom if the squared

residuals

distribution with n degrees of freedom if the squared

residuals  are uncorrelated. It is recommended to consider up to T/4 values

of n. The null hypothesis states that there are no ARCH or

GARCH errors. Rejecting the null thus means that such errors exist

in the conditional variance.

are uncorrelated. It is recommended to consider up to T/4 values

of n. The null hypothesis states that there are no ARCH or

GARCH errors. Rejecting the null thus means that such errors exist

in the conditional variance.

Add Answer to:

B. Consider the GARCH (1, 1) model Xt-σ.zt, σ -00 + α1XL1 + βισ -1 where Zt are iid N (0, 1) proc...

Consider the following AR(2) model: Xt – Xt–1 + + X4-2 = Zt, Z4 ~ WN(0,1)....

Consider the following AR(2) model: Xt – Xt–1 + + X4-2 = Zt, Z4 ~ WN(0,1). (a) Show that X+ is causal. (b) Find the first four coefficients (VO, ..., 43) of the MA(0) representation of Xt. (c) Find the pacf at lag 3, 233, of the AR(2) model.

Consider the following AR(2) model: Xt – Xt–1 + + X4-2 = Zt, Z4 ~ WN(0,1). (a) Show that X+ is causal. (b) Find the first four coefficients (VO, ..., 43) of the MA(0) representation of Xt. (c) Find the pacf at lag 3, 233, of the AR(2) model.

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability 1/2, ie, Xo--0, and Xt+1 Xt+Zt, where Zt-1 with probability 1/...

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability 1/2, ie, Xo--0, and Xt+1 Xt+Zt, where Zt-1 with probability 1/2, and Zt1 with probability 1/2. What is the probability distribution of XT? What is E(X) and Var(XT)?

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability...

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability 1/2, ie, Xo--0, and Xt+1 Xt+Zt, where Zt-1 with probability 1/2, and Zt1 with probability 1/2. What is the probability distribution of XT? What is E(X) and Var(XT)?

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability...

Consider the process where B is a backwards shift operator so that BXt-Xt-i and the {Zt) are assu...

Consider the process where B is a backwards shift operator so that BXt-Xt-i and the {Zt) are assumed to be independent random errors. (a) [2 marks] Identify what kind of nonseasonal ARIMA(p,d,q) process this is; that is give the parameters (p,d,q) and give the abbreviated name for this particular process. (b) [3 marks] (i) Is this particular process stationary? Explain. (ii) Is this process invertible? Why?

Consider the process where B is a backwards shift operator so that BXt-Xt-i and...

Consider the process where B is a backwards shift operator so that BXt-Xt-i and the {Zt) are assumed to be independent random errors. (a) [2 marks] Identify what kind of nonseasonal ARIMA(p,d,q) process this is; that is give the parameters (p,d,q) and give the abbreviated name for this particular process. (b) [3 marks] (i) Is this particular process stationary? Explain. (ii) Is this process invertible? Why?

Consider the process where B is a backwards shift operator so that BXt-Xt-i and...

Suppose that X1, X2, . . . , Xn is an iid sample of N (0, σ2 ) observations, where σ 2 > 0 is unknown. Consider testing H0 : σ 2 = σ 2 0 versus H1 : σ 2 6= σ 2 0

Suppose that X1, X2, . . . , Xn is an iid sample of N (0, σ2

) observations, where σ

2 > 0 is

unknown. Consider testing

H0 : σ

2 = σ

2

0 versus H1 : σ

2

6= σ

2

0

;

where σ

2

0

is known.

(a) Derive a size α likelihood ratio test of H0 versus H1. Your rejection region should

be written in terms of a sufficient statistic.

(b) When the null...

Suppose that X1, X2, . . . , Xn is an iid sample of N (0, σ2

) observations, where σ

2 > 0 is

unknown. Consider testing

H0 : σ

2 = σ

2

0 versus H1 : σ

2

6= σ

2

0

;

where σ

2

0

is known.

(a) Derive a size α likelihood ratio test of H0 versus H1. Your rejection region should

be written in terms of a sufficient statistic.

(b) When the null...

QUESTION 3 (a) Consider the ARMA(1, 1) process Zt-oZt_itat-θ4-1 :Where φ and θ are model parame-...

QUESTION 3 (a) Consider the ARMA(1, 1) process Zt-oZt_itat-θ4-1 :Where φ and θ are model parame- ters, and a, a are independent and identically distributed random variables with mean 0 and variance σ 1-1.4. (i) Show that the variance of the process is γ,- (i) Using () or otherwise, show that the autocorrelation function (ACF) of the process is: if k 0,

QUESTION 3 (a) Consider the ARMA(1, 1) process Zt-oZt_itat-θ4-1 :Where φ and θ are model parame- ters, and a, a are independent and identically distributed random variables with mean 0 and variance σ 1-1.4. (i) Show that the variance of the process is γ,- (i) Using () or otherwise, show that the autocorrelation function (ACF) of the process is: if k 0,

use geometric series. hrt-1 + ur where ur ~ NID(0, σ.). Show that for Consider the...

use geometric series.

hrt-1 + ur where ur ~ NID(0, σ.). Show that for Consider the AR(1) model zt øl<1, the auto-covariance is

use geometric series.

hrt-1 + ur where ur ~ NID(0, σ.). Show that for Consider the AR(1) model zt øl<1, the auto-covariance is

,X, be iid N(μχ, σ*), Yi, ,Yn be iid N(Pv, σ*), and X's and Question 2:...

,X, be iid N(μχ, σ*), Yi, ,Yn be iid N(Pv, σ*), and X's and Question 2: Let X1, Y's are independent. Let be the pooled variance. Show that Sg(0/n+1/m) is distributed at t with (n+m-2) degrees of freedom.

,X, be iid N(μχ, σ*), Yi, ,Yn be iid N(Pv, σ*), and X's and Question 2: Let X1, Y's are independent. Let be the pooled variance. Show that Sg(0/n+1/m) is distributed at t with (n+m-2) degrees of freedom.

consider the ARIMA model 8. Consider the ARIMA model X,-4 + Xt-1 + W-0.75W,-1, W, ~ WN(0, σ*) a. Identify p, d, and q. Write the corresponding ARMA (p,q) model. b. Find E VX and VarVX 8. Cons...

consider the ARIMA model

8. Consider the ARIMA model X,-4 + Xt-1 + W-0.75W,-1, W, ~ WN(0, σ*) a. Identify p, d, and q. Write the corresponding ARMA (p,q) model. b. Find E VX and VarVX

8. Consider the ARIMA model X,-4 + Xt-1 + W-0.75W,-1, W, ~ WN(0, σ*) a. Identify p, d, and q. Write the corresponding ARMA (p,q) model. b. Find E VX and VarVX

consider the ARIMA model

8. Consider the ARIMA model X,-4 + Xt-1 + W-0.75W,-1, W, ~ WN(0, σ*) a. Identify p, d, and q. Write the corresponding ARMA (p,q) model. b. Find E VX and VarVX

8. Consider the ARIMA model X,-4 + Xt-1 + W-0.75W,-1, W, ~ WN(0, σ*) a. Identify p, d, and q. Write the corresponding ARMA (p,q) model. b. Find E VX and VarVX

3. Consider the multiple linear regression model iid where Xi, . . . ,Xp-1 ,i are observed covariate values for observation i, and Ei ~N(0,ơ2) (a) What is the interpretation of B1 in this model? (b)...

3. Consider the multiple linear regression model iid where Xi, . . . ,Xp-1 ,i are observed covariate values for observation i, and Ei ~N(0,ơ2) (a) What is the interpretation of B1 in this model? (b) Write the matrix form of the model. Label the response vector, design matrix, coefficient vector, and error vector, and specify the dimensions and elements for each. (c) Write the likelihood, log-likelihood, and in matrix form. aB (d) Solve : 0 for β, the MLE...

3. Consider the multiple linear regression model iid where Xi, . . . ,Xp-1 ,i are observed covariate values for observation i, and Ei ~N(0,ơ2) (a) What is the interpretation of B1 in this model? (b) Write the matrix form of the model. Label the response vector, design matrix, coefficient vector, and error vector, and specify the dimensions and elements for each. (c) Write the likelihood, log-likelihood, and in matrix form. aB (d) Solve : 0 for β, the MLE...

[4] 7. Let where X0-0 and Zt comes from WN (0, σ*). Find 7x (s, t)-Cor(X,, X,) for all positive i...

[4] 7. Let where X0-0 and Zt comes from WN (0, σ*). Find 7x (s, t)-Cor(X,, X,) for all positive integers s and t. From your result conclude that the process is not stationary.

[4] 7. Let where X0-0 and Zt comes from WN (0, σ*). Find 7x (s, t)-Cor(X,, X,) for all positive integers s and t. From your result conclude that the process is not stationary.

[4] 7. Let where X0-0 and Zt comes from WN (0, σ*). Find 7x (s, t)-Cor(X,, X,) for all positive integers s and t. From your result conclude that the process is not stationary.

[4] 7. Let where X0-0 and Zt comes from WN (0, σ*). Find 7x (s, t)-Cor(X,, X,) for all positive integers s and t. From your result conclude that the process is not stationary.

Consider the following AR(2) model: Xt – Xt–1 + + X4-2 = Zt, Z4 ~ WN(0,1). (a) Show that X+ is causal. (b) Find the first four coefficients (VO, ..., 43) of the MA(0) representation of Xt. (c) Find the pacf at lag 3, 233, of the AR(2) model.

Consider the following AR(2) model: Xt – Xt–1 + + X4-2 = Zt, Z4 ~ WN(0,1). (a) Show that X+ is causal. (b) Find the first four coefficients (VO, ..., 43) of the MA(0) representation of Xt. (c) Find the pacf at lag 3, 233, of the AR(2) model.

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability 1/2, ie, Xo--0, and Xt+1 Xt+Zt, where Zt-1 with probability 1/2, and Zt1 with probability 1/2. What is the probability distribution of XT? What is E(X) and Var(XT)?

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability...

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability 1/2, ie, Xo--0, and Xt+1 Xt+Zt, where Zt-1 with probability 1/2, and Zt1 with probability 1/2. What is the probability distribution of XT? What is E(X) and Var(XT)?

Problem 3 Consider a random walk on the integers. Suppose we start from 0, and at each step, we either go left or right with probability...

Consider the process where B is a backwards shift operator so that BXt-Xt-i and the {Zt) are assumed to be independent random errors. (a) [2 marks] Identify what kind of nonseasonal ARIMA(p,d,q) process this is; that is give the parameters (p,d,q) and give the abbreviated name for this particular process. (b) [3 marks] (i) Is this particular process stationary? Explain. (ii) Is this process invertible? Why?

Consider the process where B is a backwards shift operator so that BXt-Xt-i and...

Consider the process where B is a backwards shift operator so that BXt-Xt-i and the {Zt) are assumed to be independent random errors. (a) [2 marks] Identify what kind of nonseasonal ARIMA(p,d,q) process this is; that is give the parameters (p,d,q) and give the abbreviated name for this particular process. (b) [3 marks] (i) Is this particular process stationary? Explain. (ii) Is this process invertible? Why?

Consider the process where B is a backwards shift operator so that BXt-Xt-i and...

QUESTION 3 (a) Consider the ARMA(1, 1) process Zt-oZt_itat-θ4-1 :Where φ and θ are model parame- ters, and a, a are independent and identically distributed random variables with mean 0 and variance σ 1-1.4. (i) Show that the variance of the process is γ,- (i) Using () or otherwise, show that the autocorrelation function (ACF) of the process is: if k 0,

QUESTION 3 (a) Consider the ARMA(1, 1) process Zt-oZt_itat-θ4-1 :Where φ and θ are model parame- ters, and a, a are independent and identically distributed random variables with mean 0 and variance σ 1-1.4. (i) Show that the variance of the process is γ,- (i) Using () or otherwise, show that the autocorrelation function (ACF) of the process is: if k 0,

use geometric series.

hrt-1 + ur where ur ~ NID(0, σ.). Show that for Consider the AR(1) model zt øl<1, the auto-covariance is

use geometric series.

hrt-1 + ur where ur ~ NID(0, σ.). Show that for Consider the AR(1) model zt øl<1, the auto-covariance is

,X, be iid N(μχ, σ*), Yi, ,Yn be iid N(Pv, σ*), and X's and Question 2: Let X1, Y's are independent. Let be the pooled variance. Show that Sg(0/n+1/m) is distributed at t with (n+m-2) degrees of freedom.

,X, be iid N(μχ, σ*), Yi, ,Yn be iid N(Pv, σ*), and X's and Question 2: Let X1, Y's are independent. Let be the pooled variance. Show that Sg(0/n+1/m) is distributed at t with (n+m-2) degrees of freedom.

consider the ARIMA model

8. Consider the ARIMA model X,-4 + Xt-1 + W-0.75W,-1, W, ~ WN(0, σ*) a. Identify p, d, and q. Write the corresponding ARMA (p,q) model. b. Find E VX and VarVX

8. Consider the ARIMA model X,-4 + Xt-1 + W-0.75W,-1, W, ~ WN(0, σ*) a. Identify p, d, and q. Write the corresponding ARMA (p,q) model. b. Find E VX and VarVX

consider the ARIMA model

8. Consider the ARIMA model X,-4 + Xt-1 + W-0.75W,-1, W, ~ WN(0, σ*) a. Identify p, d, and q. Write the corresponding ARMA (p,q) model. b. Find E VX and VarVX

8. Consider the ARIMA model X,-4 + Xt-1 + W-0.75W,-1, W, ~ WN(0, σ*) a. Identify p, d, and q. Write the corresponding ARMA (p,q) model. b. Find E VX and VarVX

3. Consider the multiple linear regression model iid where Xi, . . . ,Xp-1 ,i are observed covariate values for observation i, and Ei ~N(0,ơ2) (a) What is the interpretation of B1 in this model? (b) Write the matrix form of the model. Label the response vector, design matrix, coefficient vector, and error vector, and specify the dimensions and elements for each. (c) Write the likelihood, log-likelihood, and in matrix form. aB (d) Solve : 0 for β, the MLE...

3. Consider the multiple linear regression model iid where Xi, . . . ,Xp-1 ,i are observed covariate values for observation i, and Ei ~N(0,ơ2) (a) What is the interpretation of B1 in this model? (b) Write the matrix form of the model. Label the response vector, design matrix, coefficient vector, and error vector, and specify the dimensions and elements for each. (c) Write the likelihood, log-likelihood, and in matrix form. aB (d) Solve : 0 for β, the MLE...

[4] 7. Let where X0-0 and Zt comes from WN (0, σ*). Find 7x (s, t)-Cor(X,, X,) for all positive integers s and t. From your result conclude that the process is not stationary.

[4] 7. Let where X0-0 and Zt comes from WN (0, σ*). Find 7x (s, t)-Cor(X,, X,) for all positive integers s and t. From your result conclude that the process is not stationary.

[4] 7. Let where X0-0 and Zt comes from WN (0, σ*). Find 7x (s, t)-Cor(X,, X,) for all positive integers s and t. From your result conclude that the process is not stationary.

[4] 7. Let where X0-0 and Zt comes from WN (0, σ*). Find 7x (s, t)-Cor(X,, X,) for all positive integers s and t. From your result conclude that the process is not stationary.

Most questions answered within 3 hours.

-

Koo argues that the Japanese economy in the 1990s suffered from

a balance sheet recession. What...

asked 9 minutes ago -

Automobile mechanics conduct diagnosis tests on 150 new cars of

particular make and model to determine...

asked 3 minutes ago -

11) Find the proceeds of a 5 year non-interest

bearing note for $6500 discounted 2.5 years...

asked 10 minutes ago -

If

the more comprehensive data is available in MEPS, why does the NHIS

still exist? How...

asked 16 minutes ago -

Required: Prepare the consolidated financial statements of

Griffin Ltd at 30 June 2019.

Griffin Ltd is...

asked 19 minutes ago -

1.How large must the coefficient of static friction be between

the tires and the road if...

asked 34 minutes ago -

What is the time complexity (Big-O) of the following code?

class Main

{

// Recursive...

asked 34 minutes ago -

Economists look at any situation in terms of its component

parts: the people making decisions, the...

asked 40 minutes ago -

What is a population?

Select one:

a. All of the individual organisms belonging to the same...

asked 44 minutes ago -

You have a yeast cell culture with a concentration of 5x10^4

cells/ml. If you dilute this...

asked 48 minutes ago -

In which direction the Reaction goes? Show detailed process.

SeO3 + 2ClO2. + 2H3O <---> Se...

asked 1 hour ago -

Unexposed silver halides are removed from photographic film when

they react with sodium thiosulfate

(Na2S2O3, called...

asked 1 hour ago