Consider a call and a put option, both with strike price of $30 and 3 months to expiration. The call trades at $4, the put price is $5, the interest rate is 0, and the price of the underlying stock is...

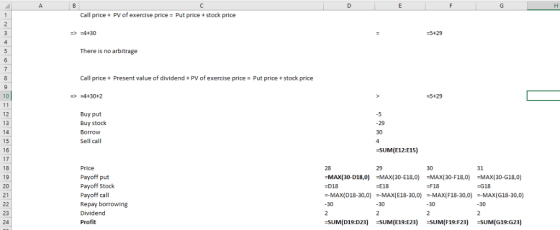

Consider a call and a put option, both with strike price of $30 and 3 months to expiration. The call trades at $4, the put price is $5, the interest rate is 0, and the price of the underlying stock is $29.

a.Suppose the stock does not pay dividends. Is there an arbitrage? If so, write down the sequence of trades and calculate the arbitrage profit you realize in 3 months. If not, explain why not.

b.Suppose the stock will pay a dividend of $2 in 2 months. Assume all other prices are as above. Is there an arbitrage? If so, write down the sequence of trades and calculate the arbitrage profit you realize in 3 months. If not, explain why not.

Homework Answers

Add Answer to:

Consider a call and a put option, both with strike price of $30 and 3 months to expiration. The call trades at $4, the put price is $5, the interest rate is 0, and the price of the underlying stock is...

5. Consider a call and a put option, both with strike price of $30 and 3...

5. Consider a call and a put option, both with strike price of $30 and 3 months to expiration. The call trades at $5, the put price is $6, the interest rate is 0, and the price of the underlying stock is $29. (1) Suppose the stock does not pay dividends. Is there an arbitrage? If so, write down the sequence of trades and calculate the arbitrage profit you realize in 3 months. If not, explain why not. (2) Suppose...

5. Consider a call and a put option, both with strike price of $30 and 3 months to expiration. The call trades at $5, the put price is $6, the interest rate is 0, and the price of the underlying stock is $29. (1) Suppose the stock does not pay dividends. Is there an arbitrage? If so, write down the sequence of trades and calculate the arbitrage profit you realize in 3 months. If not, explain why not. (2) Suppose...

. Consider a call and a put option, both with strike price of $30 and 3...

. Consider a call and a put option, both with strike price of $30 and 3 months to expiration. The call trades at $5, the put price is $6, the interest rate is 0, and the price of the underlying stock is $29. (1) Suppose the stock does not pay dividends. Is there an arbitrage? If so, write down the sequence of trades and calculate the arbitrage profit you realize in 3 months. If not, explain why not. (2) Suppose...

. Consider a call and a put option, both with strike price of $30 and 3 months to expiration. The call trades at $5, the put price is $6, the interest rate is 0, and the price of the underlying stock is $29. (1) Suppose the stock does not pay dividends. Is there an arbitrage? If so, write down the sequence of trades and calculate the arbitrage profit you realize in 3 months. If not, explain why not. (2) Suppose...

A European call option and put option on a stock both have a strike price of...

A European call option and put option on a stock both have a strike price of $45 and an expiration date in six months. Both sell for $2. The risk-free interest rate is 5% p.a. The current stock price is $43. There is no dividend expected for the next six months. a) If the stock price in three months is $48, which option is in the money and which one is out of the money? b) As an arbitrageur, can...

A European call option has a strike price of $20 and an expiration date in six...

A European call option has a strike price of $20 and an expiration date in six months. The premium for the call option is $5. The current stock price is $25. The risk-free rate is 2% per annum with continuous compounding. What is the payoff to the portfolio, short selling the stock, lending $19.80 and buying a call option? (Hint: fill in the table below.) Value of ST Payoff ST ≤ 20 ST > 20 How much do you pay...

Problem 12. A European call and put option on a stock both have a strike price...

Problem 12. A European call and put option on a stock both have a strike price of $30 and an expiration date in three months. The price of the call is $3, and the price of the put is $2.25. The risk free interest rate is 10% per annum, the current stock price is $31. Indentify the arbitrage opportunity open to a trader.

Problem 12. A European call and put option on a stock both have a strike price of $30 and an expiration date in three months. The price of the call is $3, and the price of the put is $2.25. The risk free interest rate is 10% per annum, the current stock price is $31. Indentify the arbitrage opportunity open to a trader.

A put option and a call option on a stock have the same expiration date and the same exercise (or strike price). Both options expire in 6 months. Assume that put-call parity holds and interest rate is...

A put option and a call option on a stock have the same expiration date and the same exercise (or strike price). Both options expire in 6 months. Assume that put-call parity holds and interest rate is positive. If both call and put options have the same price, which of the following is true? A) Put option is in-the-money. B) Call option is in-the-money. C) Both call and put options are in-the-money. D) Both call and put options are out-of-the-money.

Microsoft (MSFT) + IMSETI Underlying stock price = $71.75 Expiration Strike Call Put June 16, 2017...

Microsoft (MSFT) + IMSETI Underlying stock price = $71.75 Expiration Strike Call Put June 16, 2017 70 2.02 0.24 June 16, 2017 72 0.67 0.90 June 16, 2017 74 0.132.37 70 July 7, 2017 July 7, 2017 July 7, 2017 72 2.400.58 1.15 1.32 0.42 2.59 74 Refer to Figure 15.1, which lists the prices of various Microsoft options. Use the data in the figure to calculate the payoff and the profit/loss for investments in each of the following July...

Microsoft (MSFT) + IMSETI Underlying stock price = $71.75 Expiration Strike Call Put June 16, 2017 70 2.02 0.24 June 16, 2017 72 0.67 0.90 June 16, 2017 74 0.132.37 70 July 7, 2017 July 7, 2017 July 7, 2017 72 2.400.58 1.15 1.32 0.42 2.59 74 Refer to Figure 15.1, which lists the prices of various Microsoft options. Use the data in the figure to calculate the payoff and the profit/loss for investments in each of the following July...

A stock's current price is $72. A call option with 3-month maturity and strike price of...

A stock's current price is $72. A call option with 3-month maturity and strike price of $ 68 is trading for 6, while a put with the same strike and expiration is trading for $20. The risk free rate is 2%. How much arbitrage profit can you make by selling the put and purchasing a synthetic put? (Provide your answer rounded to two decimals.) You have purchased a put option for $ 11 three months ago. The option's strike price...

Consider a three-year European call option with the strike price of $150. The underlying stock will...

Consider a three-year European call option with the strike price of $150. The underlying stock will pay $10-dividend two years later from now. The current stock price is $170. The risk-free rate is 3% per annum. Find the range of the call prices that do not allow any arbitrage.

The price of a call option with a strike of $100 is $10. The price of...

The price of a call option with a strike of $100 is $10. The price of a put option with a strike of $100 is $5. Interest rates are 0 and the current price of the underlying is $100. Can you make an arbitrage profit? If so how? Describe the trade and your pay offs in detail?

5. Consider a call and a put option, both with strike price of $30 and 3 months to expiration. The call trades at $5, the put price is $6, the interest rate is 0, and the price of the underlying stock is $29. (1) Suppose the stock does not pay dividends. Is there an arbitrage? If so, write down the sequence of trades and calculate the arbitrage profit you realize in 3 months. If not, explain why not. (2) Suppose...

5. Consider a call and a put option, both with strike price of $30 and 3 months to expiration. The call trades at $5, the put price is $6, the interest rate is 0, and the price of the underlying stock is $29. (1) Suppose the stock does not pay dividends. Is there an arbitrage? If so, write down the sequence of trades and calculate the arbitrage profit you realize in 3 months. If not, explain why not. (2) Suppose...

. Consider a call and a put option, both with strike price of $30 and 3 months to expiration. The call trades at $5, the put price is $6, the interest rate is 0, and the price of the underlying stock is $29. (1) Suppose the stock does not pay dividends. Is there an arbitrage? If so, write down the sequence of trades and calculate the arbitrage profit you realize in 3 months. If not, explain why not. (2) Suppose...

. Consider a call and a put option, both with strike price of $30 and 3 months to expiration. The call trades at $5, the put price is $6, the interest rate is 0, and the price of the underlying stock is $29. (1) Suppose the stock does not pay dividends. Is there an arbitrage? If so, write down the sequence of trades and calculate the arbitrage profit you realize in 3 months. If not, explain why not. (2) Suppose...

Problem 12. A European call and put option on a stock both have a strike price of $30 and an expiration date in three months. The price of the call is $3, and the price of the put is $2.25. The risk free interest rate is 10% per annum, the current stock price is $31. Indentify the arbitrage opportunity open to a trader.

Problem 12. A European call and put option on a stock both have a strike price of $30 and an expiration date in three months. The price of the call is $3, and the price of the put is $2.25. The risk free interest rate is 10% per annum, the current stock price is $31. Indentify the arbitrage opportunity open to a trader.

Microsoft (MSFT) + IMSETI Underlying stock price = $71.75 Expiration Strike Call Put June 16, 2017 70 2.02 0.24 June 16, 2017 72 0.67 0.90 June 16, 2017 74 0.132.37 70 July 7, 2017 July 7, 2017 July 7, 2017 72 2.400.58 1.15 1.32 0.42 2.59 74 Refer to Figure 15.1, which lists the prices of various Microsoft options. Use the data in the figure to calculate the payoff and the profit/loss for investments in each of the following July...

Microsoft (MSFT) + IMSETI Underlying stock price = $71.75 Expiration Strike Call Put June 16, 2017 70 2.02 0.24 June 16, 2017 72 0.67 0.90 June 16, 2017 74 0.132.37 70 July 7, 2017 July 7, 2017 July 7, 2017 72 2.400.58 1.15 1.32 0.42 2.59 74 Refer to Figure 15.1, which lists the prices of various Microsoft options. Use the data in the figure to calculate the payoff and the profit/loss for investments in each of the following July...

Most questions answered within 3 hours.

-

Effect of DCMU and sodium azide on Chlamydomonas? We did an

experiment where we had Chlamydomonas...

asked 1 minute ago -

1a) According to the ideal gas law, _______________.

a. a gas has infinite volume at absolute...

asked 1 hour ago -

Oakdale Fashions, Inc. had $245,000 in 2018 taxable income.

Using the tax schedule in Table 2.3...

asked 1 hour ago -

The marketing class at CSUS had an average score of 150. An

educational analyst determined that...

asked 3 hours ago -

Justin Case has purchased a $250 000 home by putting 20 % down

and taking out...

asked 3 hours ago -

1. In a labor market, marginal cost for a firm is

____________.

a. recruiting cost

b....

asked 3 hours ago -

On January 1, 2019, ABC Company issued $60,000,000 of 20-year,

10.5% bonds when the market rate...

asked 4 hours ago -

39.4% of US homes continue to use a landline in addition to cell

phone service. 3...

asked 5 hours ago -

Starting with benzene, synthesize 1-phenyl-1-butyne.

Show intermediates and reagents.

asked 5 hours ago -

Create a 32-run crossed array design with six control factors

and two noise factors such that...

asked 6 hours ago -

A 500g sample of sand from source A has the following amounts

retained on each sieve....

asked 6 hours ago -

In

your own words, please explain the essay by John Keynes wrote "The

End of Laissez...

asked 6 hours ago