Homework Answers

Add Answer to:

A stock is currently selling for RM60. The price of the stock is expected to either...

The stock price of Bravo Corp. is currently $100. The stock price a year from now...

The stock price of Bravo Corp. is currently $100. The stock price a year from now will be either $160 or $60 with equal probabilities. The interest rate at which investors invest in riskless assets at is 6%. Using the binomial OPM, the value of a put option with an exercise price of $135 and an expiration date one year from now should be worth __________ today. Please provide the steps for getting ans: 38.21

GS stock is currently worth $56. Every year, it can increase by 30% or decrease by...

GS stock is currently worth $56. Every year, it can increase by 30% or decrease by 10%. The stock pays no dividends, and the annual continuously-compounded risk-free interest rate is 4%. Using a two-period binomial option pricing model, find the price today of one two-year European put option on the stock with a strike price of $120.

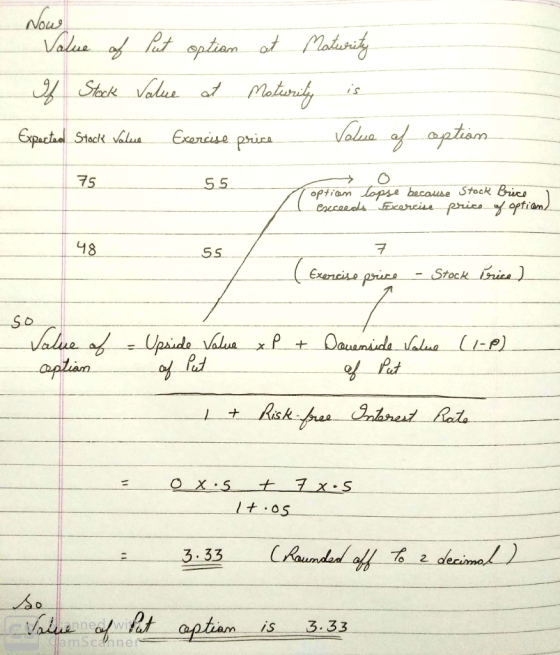

A stock currently sells for $50. In six months it will either rise to $60 or...

A stock currently sells for $50. In six months it will either rise to $60 or decline to $45. The continuous compounding risk-free interest rate is 5% per year. Using the binomial approach, find the value of a European call option with an exercise price of $50. Using the binomial approach, find the value of a European put option with an exercise price of $50. Verify the put-call parity using the results of Questions 1 and 2.

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-...

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-bills will you put to replicate the pay off of a European call option with K = $38 and maturing in 6 months. b. 1pt What is the value of this European call option? Problem 2 Suppose that stock price will increase 5% and decrease 5%...

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-bills will you put to replicate the pay off of a European call option with K = $38 and maturing in 6 months. b. 1pt What is the value of this European call option? Problem 2 Suppose that stock price will increase 5% and decrease 5%...

Woodbridge's stock is currently selling for $26.00 a share but is expected to decrease to either...

Woodbridge's stock is currently selling for $26.00 a share but is expected to decrease to either $23.40 or increase to $28.60 a share over the next year. The risk-free rate is 3 percent. What is the current value of a 1-year call option with an exercise price of $26? $1.50 $1.64 $1.72 $1.86 $2.02

Binomial option pricing model A stock currently trades for $41. In one month, the price will either be $47 or $34. The a...

Binomial option pricing model A stock currently trades for $41. In one month, the price will either be $47 or $34. The annual risk-free rate is 6%; assume daily interest compounding and 365 days per year. The value of a one-month call option with an exercise price of $39 is $______.

A stock selling at $50 will either go up 20% or go down 10% each month...

A stock selling at $50 will either go up 20% or go down 10% each month for the next 3 months. The risk-free rate is 12% per annum with continuous compounding. Assume that a European put option is available for a strike price of $55 and a maturity of 3 months. a. Use a 3-step binomial model to calculate the price of the put option.

Assume that the riskless rate of interest is 4.5% and that the stock price has a volatility of 30%. Given a current...

Assume that the riskless rate of interest is 4.5% and that the stock price has a volatility of 30%. Given a current stock price of $100 and the fact that the stock does not pay any dividend: a) What is the probability that a European put option on the stock with an exercise price of $90 and a maturity date in one year will be exercised? Hint: You need to compute the probability that the stock price at maturity will...

Assume that the riskless rate of interest is 4.5% and that the stock price has a volatility of 30%. Given a current stock price of $100 and the fact that the stock does not pay any dividend: a) What is the probability that a European put option on the stock with an exercise price of $90 and a maturity date in one year will be exercised? Hint: You need to compute the probability that the stock price at maturity will...

A non-paying dividend stock price is currently 40 US$. Over each of the next two three-month...

A non-paying dividend stock price is currently 40 US$. Over each of the next two three-month periods it is expected to go either up by 10% or down by 10%. The riskless interest rate is 12% per annum with continuous compounding. What is the value of a six-month European put option with a strike price of 42 US$? Given the information above find the relevant call and put price of that European non-paying dividend stock option using the Black-Scholes formula

The price of a share of stock is currently $50. The stock does not pay any...

The price of a share of stock is currently $50. The stock does not pay any dividend. At the end of three months it will be either $60 or $40. The risk-free interest rate is 5% per year. An investor buys a European put option with a strike price of $50 per share. Assume that the option is written on 100 shares of stock. What stock position should the investor take today so that she would hold a riskless portfolio...

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-bills will you put to replicate the pay off of a European call option with K = $38 and maturing in 6 months. b. 1pt What is the value of this European call option? Problem 2 Suppose that stock price will increase 5% and decrease 5%...

Problem1 A stock is currently trading at S $40, during next 6 months stock price will increase to $44 or decrease to $32-6-month risk-free rate is rf-2%. a. [4pts) What positions in stock and T-bills will you put to replicate the pay off of a European call option with K = $38 and maturing in 6 months. b. 1pt What is the value of this European call option? Problem 2 Suppose that stock price will increase 5% and decrease 5%...

Assume that the riskless rate of interest is 4.5% and that the stock price has a volatility of 30%. Given a current stock price of $100 and the fact that the stock does not pay any dividend: a) What is the probability that a European put option on the stock with an exercise price of $90 and a maturity date in one year will be exercised? Hint: You need to compute the probability that the stock price at maturity will...

Assume that the riskless rate of interest is 4.5% and that the stock price has a volatility of 30%. Given a current stock price of $100 and the fact that the stock does not pay any dividend: a) What is the probability that a European put option on the stock with an exercise price of $90 and a maturity date in one year will be exercised? Hint: You need to compute the probability that the stock price at maturity will...

Most questions answered within 3 hours.

-

Suppose that you know that in the population of full-time

employees in the United States, the...

asked 20 minutes ago -

This experiment was designed originally to sample various meat and carcass quality

aspects of Ontario pigs...

asked 21 minutes ago -

Dopamine Hydrochloride: draw the structure And Show the

functional groups in different colors and label the...

asked 13 minutes ago -

A rope supports a 10 kg dumbbell hanging from it. What is the

tension in the...

asked 12 minutes ago -

) Raw materials are studied for contamination. Suppose that

the number of particles of contamination per...

asked 35 minutes ago -

After running a regression analysis we calculated an F test and

the significance level was 0.15....

asked 31 minutes ago -

----Can someone please help me solve this one using JAVA

----I thank you in advance

Create...

asked 35 minutes ago -

1. What force primarily attracts the potassium ion to

the nitrate ion?

a. London forces...

asked 37 minutes ago -

What are the negative effects of abruptly stopping the use of

all fossil fuels? Give at...

asked 44 minutes ago -

Given that many conflict are the result of different parties having

different interests, is it possible...

asked 49 minutes ago -

A 750 g block can slide uniformly along the horizontal track

when a string attached to...

asked 52 minutes ago -

In 2017, Juan entered into a contract to write a book. The

publisher advanced Juan $50,000,...

asked 1 hour ago