Homework Answers

1.

6.1937

2.

4.9560

3.

7.2630

4.

11.4430

5.

9.1831

I have shown for the base case below:

Add Answer to:

Use the Black-Scholes formula for the following stock: 6 months Time to expiration Standard deviation Exercise...

Use the Black-Scholes formula for the following stock: Time to expiration 6 months Standard deviation 45%...

Use the Black-Scholes formula for the following stock: Time to expiration 6 months Standard deviation 45% per year $47 $46 Exercise price Stock price Annual interest rate 5% Dividend Calculate the value of a call option. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of a call option

Use the Black-Scholes formula for the following stock: Time to expiration 6 months Standard deviation 45% per year $47 $46 Exercise price Stock price Annual interest rate 5% Dividend Calculate the value of a call option. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of a call option

Use the Black-Scholes formula for the following stock: Time to expiration 6 months Standard deviation 46%...

Use the Black-Scholes formula for the following stock: Time to expiration 6 months Standard deviation 46% per year Exercise price $48 Stock price $47 Annual interest rate 6% Dividend 0 Calculate the value of a call option. (Do not round intermediate calculations. Round your answer to 2 decimal places.)

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock...

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividend 6 months 43% per year $58 $57 Calculate the value of a call option. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of a call option

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividend 6 months 43% per year $58 $57 Calculate the value of a call option. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of a call option

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock...

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividend 6 months 47% per year $59 $58 Calculate the value of a call option. (Do not round Intermediate calculations. Round your answer to 2 decimal places.) Value of a call option

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividend 6 months 47% per year $59 $58 Calculate the value of a call option. (Do not round Intermediate calculations. Round your answer to 2 decimal places.) Value of a call option

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock...

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividend 6 months 56% per year $55 $54 6% Calculate the value of a call option. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of a call optionſ

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividend 6 months 56% per year $55 $54 6% Calculate the value of a call option. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of a call optionſ

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock...

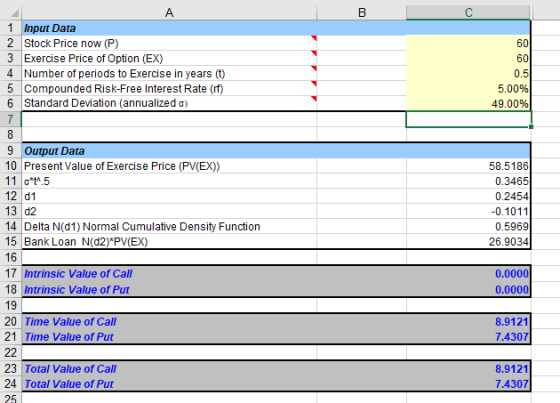

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividend 6 months 49% per year $60 $58 58 Calculate the value of a put option. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of a put option

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividend 6 months 49% per year $60 $58 58 Calculate the value of a put option. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of a put option

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock...

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividende 6 months 51% per year $41 $40 6% Calculate the value of a call option. (Do not round intermediate calculations. Round y Value of a call option

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividende 6 months 51% per year $41 $40 6% Calculate the value of a call option. (Do not round intermediate calculations. Round y Value of a call option

Question #1: Use the Black-Scholes formula to find the value of a call option on the following stock Time to expira...

Question #1: Use the Black-Scholes formula to find the value of a call option on the following stock Time to expiration Standard Deviation Exercise Price Stock Price Interest Rate 6 months 50% per year $50 $50 10% Question #2: Find the value of put option on the stock in the previous problem with the same information above (Hint: there are two ways of calculating such value).

Question #1: Use the Black-Scholes formula to find the value of a call option on the following stock Time to expiration Standard Deviation Exercise Price Stock Price Interest Rate 6 months 50% per year $50 $50 10% Question #2: Find the value of put option on the stock in the previous problem with the same information above (Hint: there are two ways of calculating such value).

Use the Black-Scholes formula to find the value of a call option based on the following...

Use the Black-Scholes formula to find the value of a call option based on the following inputs. (Round your final answer to 2 decimal places. Do not round intermediate calculations.) $ $ 60 56 7% Stock price Exercise price Interest rate Dividend yield Time to expiration Standard deviation of stock's returns 0.50 26% Call value $0

Use the Black-Scholes formula to find the value of a call option based on the following inputs. (Round your final answer to 2 decimal places. Do not round intermediate calculations.) $ $ 60 56 7% Stock price Exercise price Interest rate Dividend yield Time to expiration Standard deviation of stock's returns 0.50 26% Call value $0

Use the Black-Scholes formula to find the value of a call option based on the following...

Use the Black-Scholes formula to find the value of a call option based on the following inputs. (Round your final answer to 2 decimal places. Do not round intermediate calculations.) Stock price Exercise price Interest rate Dividend yield Time to expiration Standard deviation of stock's returns $ 59 $ 56 7% 4% 0.50 28% Call value

Use the Black-Scholes formula to find the value of a call option based on the following inputs. (Round your final answer to 2 decimal places. Do not round intermediate calculations.) Stock price Exercise price Interest rate Dividend yield Time to expiration Standard deviation of stock's returns $ 59 $ 56 7% 4% 0.50 28% Call value

Use the Black-Scholes formula for the following stock: Time to expiration 6 months Standard deviation 45% per year $47 $46 Exercise price Stock price Annual interest rate 5% Dividend Calculate the value of a call option. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of a call option

Use the Black-Scholes formula for the following stock: Time to expiration 6 months Standard deviation 45% per year $47 $46 Exercise price Stock price Annual interest rate 5% Dividend Calculate the value of a call option. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of a call option

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividend 6 months 43% per year $58 $57 Calculate the value of a call option. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of a call option

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividend 6 months 43% per year $58 $57 Calculate the value of a call option. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of a call option

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividend 6 months 47% per year $59 $58 Calculate the value of a call option. (Do not round Intermediate calculations. Round your answer to 2 decimal places.) Value of a call option

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividend 6 months 47% per year $59 $58 Calculate the value of a call option. (Do not round Intermediate calculations. Round your answer to 2 decimal places.) Value of a call option

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividend 6 months 56% per year $55 $54 6% Calculate the value of a call option. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of a call optionſ

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividend 6 months 56% per year $55 $54 6% Calculate the value of a call option. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of a call optionſ

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividend 6 months 49% per year $60 $58 58 Calculate the value of a put option. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of a put option

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividend 6 months 49% per year $60 $58 58 Calculate the value of a put option. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of a put option

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividende 6 months 51% per year $41 $40 6% Calculate the value of a call option. (Do not round intermediate calculations. Round y Value of a call option

Use the Black-Scholes formula for the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividende 6 months 51% per year $41 $40 6% Calculate the value of a call option. (Do not round intermediate calculations. Round y Value of a call option

Question #1: Use the Black-Scholes formula to find the value of a call option on the following stock Time to expiration Standard Deviation Exercise Price Stock Price Interest Rate 6 months 50% per year $50 $50 10% Question #2: Find the value of put option on the stock in the previous problem with the same information above (Hint: there are two ways of calculating such value).

Question #1: Use the Black-Scholes formula to find the value of a call option on the following stock Time to expiration Standard Deviation Exercise Price Stock Price Interest Rate 6 months 50% per year $50 $50 10% Question #2: Find the value of put option on the stock in the previous problem with the same information above (Hint: there are two ways of calculating such value).

Use the Black-Scholes formula to find the value of a call option based on the following inputs. (Round your final answer to 2 decimal places. Do not round intermediate calculations.) $ $ 60 56 7% Stock price Exercise price Interest rate Dividend yield Time to expiration Standard deviation of stock's returns 0.50 26% Call value $0

Use the Black-Scholes formula to find the value of a call option based on the following inputs. (Round your final answer to 2 decimal places. Do not round intermediate calculations.) $ $ 60 56 7% Stock price Exercise price Interest rate Dividend yield Time to expiration Standard deviation of stock's returns 0.50 26% Call value $0

Use the Black-Scholes formula to find the value of a call option based on the following inputs. (Round your final answer to 2 decimal places. Do not round intermediate calculations.) Stock price Exercise price Interest rate Dividend yield Time to expiration Standard deviation of stock's returns $ 59 $ 56 7% 4% 0.50 28% Call value

Use the Black-Scholes formula to find the value of a call option based on the following inputs. (Round your final answer to 2 decimal places. Do not round intermediate calculations.) Stock price Exercise price Interest rate Dividend yield Time to expiration Standard deviation of stock's returns $ 59 $ 56 7% 4% 0.50 28% Call value

Most questions answered within 3 hours.

-

Group Policies

Research GROUP POLICY OBJECTS (GPO'S)

You can start in the Windows Server 2012 eBook...

asked 1 minute ago -

software engineering

Problems.

Create a use case diagram for class registration for a

university.

Create a...

asked 59 seconds ago -

You are trying to convince your friend who wants to attend

medical school to take BY123...

asked 16 minutes ago -

Subject: C++

I have created a class called QueueOfIntegers in a file called

QueueOfIntegers.h, which is...

asked 15 minutes ago -

calculate the number of molecules of gas in a

container of 2.0 liter at 30 degrees...

asked 33 minutes ago -

1.which of the following is a phototroph?

a. sulfolobus

b. chloroflexus

c. bacteroidetes

d. deinococcus radioduran...

asked 29 minutes ago -

The group of companies LC "High-precision measuring instruments"

is the global provider of measurement, analysis and...

asked 35 minutes ago -

I want to write a python function to find the minimum

I have an nested list:...

asked 35 minutes ago -

Convert the high level language programming statementts to 80x86

assembly, Assume X=AX and y=BX

for (i=1;...

asked 44 minutes ago -

SoleMate’s Burkins sneakers cost $40 per pair from the supplier

and are sold by SoleMate at...

asked 48 minutes ago -

The movie Moneyball (based on the book by Michael

Lewis) tells the story of Billy Beane,...

asked 47 minutes ago -

A regional highway uses 8 tollbooths that are open to all

vehicles. A chi-square goodness-of-fit test...

asked 51 minutes ago