Homework Answers

Ans (a):

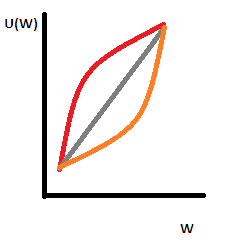

Based on utility function over money, we can compute the utility curve and based on its shape we can know the risk appetite of the individual.

A risk averse utility function is concave (red shaded curve above), risk neutral is upward sloping without curvature (grey shaded curve above), and a risk loving utility function is convex (orange shaded curve above).

Based on the given utility function, we can plot the utility curve as follows:

Therefore, the individual is risk neutral, since the curve is not concave or convex.

Ans (b):

Given:

Initial wealth (WO)= W

Probable Loss (L) = W/2

Probability of Loss (PL) = ½

Probability of No Loss (PN) = ½

Insurance Premium = p

Applying the following formula, we can know the amount of Insurance coverage (C), assuming loss occurs:

L = WO – (PL * C * L) – L + (C * L)

W/2 = W – (1/2 * C * W/2) – W/2 + (C * W/2)

After solving for C, we find C = 0

Therefore, no insurance is needed, in this scenario

Ans (c):

As per the last question, we understood that there is’nt a need for any insurance cover in this case. Therefore, an individual would not want to pay any premium for it. Therefore, an individual would only want to buy an insurance at zero premium.

Add Answer to:

6. Consider an individual whose utility function over money is u(w)= 1+2w2. (a) Is the individual...

8. An individual with utility function over money u(w) = 8Vw has $C in cash and...

8. An individual with utility function over money u(w) = 8Vw has $C in cash and a lottery ticket that pays $W if it wins and nothing if it loses. The probability of winning is .. Suppose an insurance is available at price $p per unit, where each unit of insurance pays $1 if the ticket does not win and nothing if it wins. (a) Is the individual risk averse, risk neutral, or risk loving? (b) What is the fair...

8. An individual with utility function over money u(w) = 8Vw has $C in cash and a lottery ticket that pays $W if it wins and nothing if it loses. The probability of winning is .. Suppose an insurance is available at price $p per unit, where each unit of insurance pays $1 if the ticket does not win and nothing if it wins. (a) Is the individual risk averse, risk neutral, or risk loving? (b) What is the fair...

5. A consumer who lives for two periods has a standard Cobb-Douglas utility func- tion: u(C1,C2)...

5. A consumer who lives for two periods has a standard Cobb-Douglas utility func- tion: u(C1,C2) = ccm where ct = consumption in period t and a + b = 1. Her income in period one is 11 = 500 and 12 = 400, and she can lend or borrow at interest rate r = 0.2. (a) Find the optimal consumption demand. (b) What values of a, if any, makes the consumer a borrower? Interpret this result. (c) Suppose now...

5. A consumer who lives for two periods has a standard Cobb-Douglas utility func- tion: u(C1,C2) = ccm where ct = consumption in period t and a + b = 1. Her income in period one is 11 = 500 and 12 = 400, and she can lend or borrow at interest rate r = 0.2. (a) Find the optimal consumption demand. (b) What values of a, if any, makes the consumer a borrower? Interpret this result. (c) Suppose now...

intermediate micro 4. Steve's utility function over leisure and consumption is given by NLY) - min...

intermediate micro

4. Steve's utility function over leisure and consumption is given by NLY) - min (31.7. Wage rate is w and the price of the composite consumption good is p=1. (a) Suppose w = 5. Find the optimal leisure consumption combination. What is the amount of hours worked? (b) Suppose the overtime law is passed so that every worker needs to be paid 1.5 times their current wage for hours worked beyond the first 8 hours, Will this law...

intermediate micro

4. Steve's utility function over leisure and consumption is given by NLY) - min (31.7. Wage rate is w and the price of the composite consumption good is p=1. (a) Suppose w = 5. Find the optimal leisure consumption combination. What is the amount of hours worked? (b) Suppose the overtime law is passed so that every worker needs to be paid 1.5 times their current wage for hours worked beyond the first 8 hours, Will this law...

6. A decision maker has a vNM utility function over money of u(x) = x2. This...

6. A decision maker has a vNM utility function over money of u(x) = x2. This decision maker is (a) risk-averse. (b) risk-neutral. (c) risk-loving. (d) none of the above. 7. Consider two lotteries: • Lottery 1: The gamble (0.1, 0.6, 0.3) over the final wealth levels ($1, $2, $3). (The expected value of this lottery equals $2.2) • Lottery 2: Get $2.2 for sure. a) Any risk-averse individual will choose the first lottery. b) Any risk-averse individual will choose...

Gamma’s utility function over wealth levels w is given by u(w) = √ w. His initial...

Gamma’s utility function over wealth levels w is given by u(w) = √ w. His initial wealth is $400. With probability π, Gamma will get into an accident that will result in a loss of $300. With probability (1 − π), Gamma does not have an accident, and hence suffers no loss. 1. Argue (mathematically) that Gamma is risk averse. 2. What is the expected value of Gamma’s loss? 3. ABC Inc. sells auto insurance. It charges a premium of...

Terry’s utility of wealth is given by: u(w) = ln(w). Suppose Terry has $1 million in...

Terry’s utility of wealth is given by: u(w) = ln(w). Suppose Terry has $1 million in his bank account and a beach house worth $2 million. With probability 1/3, his beach house will get destroyed by a hurricane. (a) Is Terry risk-averse, risk-neutral, or risk-loving? Verify your answer using calculus. (b) Determine the actuarially fair premium for an insurance plan that will compensate him $2 million if his beach house gets destroyed by a hurricane. (c) Write out the two...

Suppose, as usual, Elmos utility function over gambles satisfies the expected utility property. Consider two gambles...

Suppose, as usual, Elmos utility function over gambles satisfies the expected utility property. Consider two gambles g and h such that E[g] > E[h]. (a) Suppose Elmo is risk-averse. Will Elmo necessarily prefer g to h? Explain. (b) What if Elmo is risk-neutral? Explain. (c) What if Elmo is risk-loving? Explain.

Suppose, as usual, Elmos utility function over gambles satisfies the expected utility property. Consider two gambles g and h such that E[g] > E[h]. (a) Suppose Elmo is risk-averse. Will Elmo necessarily prefer g to h? Explain. (b) What if Elmo is risk-neutral? Explain. (c) What if Elmo is risk-loving? Explain.

1. Suppose that an individual has a wealth of $50,000 and the utility of U(W) =...

1. Suppose that an individual has a wealth of $50,000 and the utility of U(W) = VW. This individual has the option of investing all wealth in risky stock, which is worth $100 per share, which will be worth $105 per share in a good state with probability 1/2 and $95 per share in a bad state with probability 1/2. Assume, the interest rate is zero. (a) Find the expected value and the expected utility of investing all wealth in...

1. Suppose that an individual has a wealth of $50,000 and the utility of U(W) = VW. This individual has the option of investing all wealth in risky stock, which is worth $100 per share, which will be worth $105 per share in a good state with probability 1/2 and $95 per share in a bad state with probability 1/2. Assume, the interest rate is zero. (a) Find the expected value and the expected utility of investing all wealth in...

Consider an individual with the following utility function u(W) = W^(1/4) and u(W) = W^(1/2) Which...

Consider an individual with the following utility function u(W) = W^(1/4) and u(W) = W^(1/2) Which of the utility functions makes the individual more risk Averse (in relative sense)? Which of the utility functions makes the individual more Prudent? Why or Why not?

Question 1 Consider the following three utility functions defined over quantities of money. These functions are...

Question 1 Consider the following three utility functions defined over quantities of money. These functions are risk-neutral, risk-loving, and risk-averse. Match each utility function to its risk attitude u = x^2 [Choose) [Choose ] risk-averse risk loving risk-neutral u = log(x) [Choose ] u = x + 5 Consider two firms, a farm and a railroad, both of whom maximize expected profits. The railroad emits sparks from its engines which sometimes ignite fires on the farm. There is a 1/10...

Question 1 Consider the following three utility functions defined over quantities of money. These functions are risk-neutral, risk-loving, and risk-averse. Match each utility function to its risk attitude u = x^2 [Choose) [Choose ] risk-averse risk loving risk-neutral u = log(x) [Choose ] u = x + 5 Consider two firms, a farm and a railroad, both of whom maximize expected profits. The railroad emits sparks from its engines which sometimes ignite fires on the farm. There is a 1/10...

8. An individual with utility function over money u(w) = 8Vw has $C in cash and a lottery ticket that pays $W if it wins and nothing if it loses. The probability of winning is .. Suppose an insurance is available at price $p per unit, where each unit of insurance pays $1 if the ticket does not win and nothing if it wins. (a) Is the individual risk averse, risk neutral, or risk loving? (b) What is the fair...

8. An individual with utility function over money u(w) = 8Vw has $C in cash and a lottery ticket that pays $W if it wins and nothing if it loses. The probability of winning is .. Suppose an insurance is available at price $p per unit, where each unit of insurance pays $1 if the ticket does not win and nothing if it wins. (a) Is the individual risk averse, risk neutral, or risk loving? (b) What is the fair...

5. A consumer who lives for two periods has a standard Cobb-Douglas utility func- tion: u(C1,C2) = ccm where ct = consumption in period t and a + b = 1. Her income in period one is 11 = 500 and 12 = 400, and she can lend or borrow at interest rate r = 0.2. (a) Find the optimal consumption demand. (b) What values of a, if any, makes the consumer a borrower? Interpret this result. (c) Suppose now...

5. A consumer who lives for two periods has a standard Cobb-Douglas utility func- tion: u(C1,C2) = ccm where ct = consumption in period t and a + b = 1. Her income in period one is 11 = 500 and 12 = 400, and she can lend or borrow at interest rate r = 0.2. (a) Find the optimal consumption demand. (b) What values of a, if any, makes the consumer a borrower? Interpret this result. (c) Suppose now...

intermediate micro

4. Steve's utility function over leisure and consumption is given by NLY) - min (31.7. Wage rate is w and the price of the composite consumption good is p=1. (a) Suppose w = 5. Find the optimal leisure consumption combination. What is the amount of hours worked? (b) Suppose the overtime law is passed so that every worker needs to be paid 1.5 times their current wage for hours worked beyond the first 8 hours, Will this law...

intermediate micro

4. Steve's utility function over leisure and consumption is given by NLY) - min (31.7. Wage rate is w and the price of the composite consumption good is p=1. (a) Suppose w = 5. Find the optimal leisure consumption combination. What is the amount of hours worked? (b) Suppose the overtime law is passed so that every worker needs to be paid 1.5 times their current wage for hours worked beyond the first 8 hours, Will this law...

Suppose, as usual, Elmos utility function over gambles satisfies the expected utility property. Consider two gambles g and h such that E[g] > E[h]. (a) Suppose Elmo is risk-averse. Will Elmo necessarily prefer g to h? Explain. (b) What if Elmo is risk-neutral? Explain. (c) What if Elmo is risk-loving? Explain.

Suppose, as usual, Elmos utility function over gambles satisfies the expected utility property. Consider two gambles g and h such that E[g] > E[h]. (a) Suppose Elmo is risk-averse. Will Elmo necessarily prefer g to h? Explain. (b) What if Elmo is risk-neutral? Explain. (c) What if Elmo is risk-loving? Explain.

1. Suppose that an individual has a wealth of $50,000 and the utility of U(W) = VW. This individual has the option of investing all wealth in risky stock, which is worth $100 per share, which will be worth $105 per share in a good state with probability 1/2 and $95 per share in a bad state with probability 1/2. Assume, the interest rate is zero. (a) Find the expected value and the expected utility of investing all wealth in...

1. Suppose that an individual has a wealth of $50,000 and the utility of U(W) = VW. This individual has the option of investing all wealth in risky stock, which is worth $100 per share, which will be worth $105 per share in a good state with probability 1/2 and $95 per share in a bad state with probability 1/2. Assume, the interest rate is zero. (a) Find the expected value and the expected utility of investing all wealth in...

Question 1 Consider the following three utility functions defined over quantities of money. These functions are risk-neutral, risk-loving, and risk-averse. Match each utility function to its risk attitude u = x^2 [Choose) [Choose ] risk-averse risk loving risk-neutral u = log(x) [Choose ] u = x + 5 Consider two firms, a farm and a railroad, both of whom maximize expected profits. The railroad emits sparks from its engines which sometimes ignite fires on the farm. There is a 1/10...

Question 1 Consider the following three utility functions defined over quantities of money. These functions are risk-neutral, risk-loving, and risk-averse. Match each utility function to its risk attitude u = x^2 [Choose) [Choose ] risk-averse risk loving risk-neutral u = log(x) [Choose ] u = x + 5 Consider two firms, a farm and a railroad, both of whom maximize expected profits. The railroad emits sparks from its engines which sometimes ignite fires on the farm. There is a 1/10...

Most questions answered within 3 hours.

-

A sample of C3H8 has 1.60×1024 H atoms.

How many carbon atoms does the sample contain?...

asked 48 minutes ago -

How many unique codes are possibly formed from two characters,

where the first character can be...

asked 18 minutes ago -

A concentration cell is built based on the reaction:

2H+ + 2e- ----> H2

The pH...

asked 13 minutes ago -

what is the ph of the following solutions?

150 g NH4CI dissolved into 10.0 mL of...

asked 25 minutes ago -

A projectile is launched with an initial speed of 40 m/s at an

angle of 25°...

asked 7 minutes ago -

1. Using a function, display the customer who has the highest

credit limit. Display the customer...

asked 16 minutes ago -

A spatially uniform electric field varies in time according

to E = Eo + 3000 t,...

asked 42 minutes ago -

An electric power station that operates at 25 kV and uses a 20:1

step-up ideal transformer...

asked 35 minutes ago -

1. If 0.02% of a 0.6 M weak acid ionizes in a solution, what is

the...

asked 22 minutes ago -

The College of Business at Northeast College is accumulating

data as a first step in the...

asked 27 minutes ago -

A flint glass plate (n = 1.66) rests on the bottom of an

aquarium tank. The...

asked 36 minutes ago -

The position in an object as a function of time is given as ?

(?) =...

asked 51 minutes ago