Homework Answers

Add Answer to:

2. Consider the information in Table 1 Table 1 Expected Return (% Standard Deviation (% Covariance...

3. Consider Table 2. Table 2 Stock Expected Return 2 12% 6% Standard Deviation 20% 10%...

3. Consider Table 2. Table 2 Stock Expected Return 2 12% 6% Standard Deviation 20% 10% 0.20 Correlation Coefficient (a) Consider Table 2. Compute the expected return and standard deviation of return of an equally-weighted (b) Consider Table 2. Solve for the composition, expected return and standard deviation of the minimum (c) Consider Table 2. Sketch the set of portfolios comprised of stocks 1 and 2. Be sure to include the portfolios (d) Consider Table 2. Suppose that a risk-free...

3. Consider Table 2. Table 2 Stock Expected Return 2 12% 6% Standard Deviation 20% 10% 0.20 Correlation Coefficient (a) Consider Table 2. Compute the expected return and standard deviation of return of an equally-weighted (b) Consider Table 2. Solve for the composition, expected return and standard deviation of the minimum (c) Consider Table 2. Sketch the set of portfolios comprised of stocks 1 and 2. Be sure to include the portfolios (d) Consider Table 2. Suppose that a risk-free...

3. Consider Table 3 Table 3 Stock Expected Return 10% 5% Standard Deviation 12% 8% Correlation...

3. Consider Table 3 Table 3 Stock Expected Return 10% 5% Standard Deviation 12% 8% Correlation Coefficient 0.40 (a) Consider Table 3. Compute the expected return and standard deviation of return of an equally-weighted portfolio of stocks A and B (b) Consider Table 3. Solve for the composition, expected return and standard deviation of the minimum variance portfolio (c) Consider Table 3. Sketch the set of portfolios comprised of stocks A and B (d) Consider Table 3. Suppose that a...

3. Consider Table 3 Table 3 Stock Expected Return 10% 5% Standard Deviation 12% 8% Correlation Coefficient 0.40 (a) Consider Table 3. Compute the expected return and standard deviation of return of an equally-weighted portfolio of stocks A and B (b) Consider Table 3. Solve for the composition, expected return and standard deviation of the minimum variance portfolio (c) Consider Table 3. Sketch the set of portfolios comprised of stocks A and B (d) Consider Table 3. Suppose that a...

Pinulo retums? 1 0 capital asset pricing model given historical data 2. Consider Table 1. (%)...

Pinulo retums? 1 0 capital asset pricing model given historical data 2. Consider Table 1. (%) 3.77 Table 1 Summary Statistics Alpha, Beta, Expected Return and Variance a/c to the Stocks Sample Single Index Model Covariance Residual and Return Alpha Beta with Market Expected Variance Variance Market (%) (%) Return (%) (%) 3.60 3.59 4.80 Market 4.20 0.00 8.70 (a) Consider Table 1. Using the single index model, calculate beta and alpha for stocks 1 and 2. Interpret your findings....

Pinulo retums? 1 0 capital asset pricing model given historical data 2. Consider Table 1. (%) 3.77 Table 1 Summary Statistics Alpha, Beta, Expected Return and Variance a/c to the Stocks Sample Single Index Model Covariance Residual and Return Alpha Beta with Market Expected Variance Variance Market (%) (%) Return (%) (%) 3.60 3.59 4.80 Market 4.20 0.00 8.70 (a) Consider Table 1. Using the single index model, calculate beta and alpha for stocks 1 and 2. Interpret your findings....

2. Consider the information in Table1. Table 1 Standard Deviation of Stock Stock Correlation with Market...

2. Consider the information in Table1. Table 1 Standard Deviation of Stock Stock Correlation with Market Portfolio 0.75 0.20 Stock 20% 15% 14% 0% 49% ected Market Return Risk Free Rate Return (a) Consider Table 1 . Calculate betas for Stock 1, Stock 2, and a portfolio consisting of 75% invested in Stock 1 and (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for Stock 1, Stock 2, and the (c) Consider Table 1 and...

2. Consider the information in Table1. Table 1 Standard Deviation of Stock Stock Correlation with Market Portfolio 0.75 0.20 Stock 20% 15% 14% 0% 49% ected Market Return Risk Free Rate Return (a) Consider Table 1 . Calculate betas for Stock 1, Stock 2, and a portfolio consisting of 75% invested in Stock 1 and (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for Stock 1, Stock 2, and the (c) Consider Table 1 and...

6. Consider the following information for Stocks 1 and 2: Expected Standard Stock Return Deviation 1...

6. Consider the following information for Stocks 1 and 2: Expected Standard Stock Return Deviation 1 20% 40% 2 12% 20% NE a. The correlation between the returns of these two stocks is 0.3. How will you divide your money between Stocks 1 and 2 if your aim is to achieve a portfolio with an expected return of 18% p.a.? That is, what are the weights assigned to each stock? Also take note of the risk (i.e., standard deviation) of...

6. Consider the following information for Stocks 1 and 2: Expected Standard Stock Return Deviation 1 20% 40% 2 12% 20% NE a. The correlation between the returns of these two stocks is 0.3. How will you divide your money between Stocks 1 and 2 if your aim is to achieve a portfolio with an expected return of 18% p.a.? That is, what are the weights assigned to each stock? Also take note of the risk (i.e., standard deviation) of...

Part D and E please 2. Consider the information in Table 1. Table 1 Correlation with...

Part D and E please

2. Consider the information in Table 1. Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio Risk-free asset 5% 12% 8% 0% 16% 2% 0 (a) Consider Table 1. Calculate betas for stock I and stock 2 (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2 (c) Consider Table 1 and the equilibrium expected returns...

Part D and E please

2. Consider the information in Table 1. Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio Risk-free asset 5% 12% 8% 0% 16% 2% 0 (a) Consider Table 1. Calculate betas for stock I and stock 2 (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2 (c) Consider Table 1 and the equilibrium expected returns...

Calculate the expected rate of return, variance and standard deviation of bond and common stock

(a) Calculate the expected rate of return, variance and standard deviation of bond and common stock. (b) Do you think the above stocks and bonds is a good combination to form an investment portfolio? Explain why.(c) Assuming you invest in the portfolio with weights of 70% in stock and 30% in bonds. What are the expected rate of return and standard deviation of the portfolio?

(a) Calculate the expected rate of return, variance and standard deviation of bond and common stock. (b) Do you think the above stocks and bonds is a good combination to form an investment portfolio? Explain why.(c) Assuming you invest in the portfolio with weights of 70% in stock and 30% in bonds. What are the expected rate of return and standard deviation of the portfolio?

Q2 (e) Assume for simplicity sake that one factor has been deemed appropriate to "explain" returns...

Q2

(e) Assume for simplicity sake that one factor has been deemed appropriate to "explain" returns on stocds (0) How and there is no idiosyncratic risk. Derive the arbitrage pricing theory would you perform a test of the predictions of the capital asset pricing model given historical data (APT) model 2. Consider Tablo 1 Return and Variance a/c to the Stocks Sample Covariance Residual AlphaBeta Expected Variance and Return | with Market | Variance | (96) Return Market 3.60 4.80...

Q2

(e) Assume for simplicity sake that one factor has been deemed appropriate to "explain" returns on stocds (0) How and there is no idiosyncratic risk. Derive the arbitrage pricing theory would you perform a test of the predictions of the capital asset pricing model given historical data (APT) model 2. Consider Tablo 1 Return and Variance a/c to the Stocks Sample Covariance Residual AlphaBeta Expected Variance and Return | with Market | Variance | (96) Return Market 3.60 4.80...

I would like part d and e answered please 2. Consider the information in Table 1...

I would like part d and e answered please

2. Consider the information in Table 1 Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio 6% 12% 8% 0% 16% 2% Risk-free asset 0 (a) Consider Table 1. Calculate betas for stock 1 and stock 2. (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2. (c) Consider Table 1 and...

I would like part d and e answered please

2. Consider the information in Table 1 Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio 6% 12% 8% 0% 16% 2% Risk-free asset 0 (a) Consider Table 1. Calculate betas for stock 1 and stock 2. (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2. (c) Consider Table 1 and...

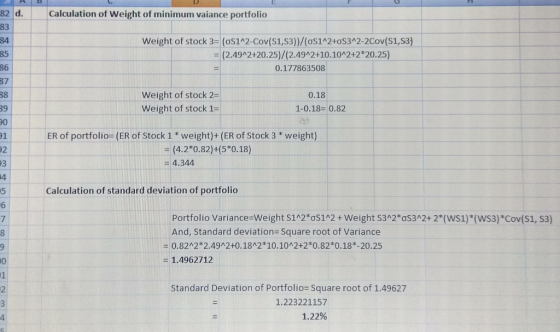

Consider two stocks, Stock D, with an expected return of 20 percent and a standard deviation...

Consider two stocks, Stock D, with an expected return of 20 percent and a standard deviation of 36 percent, and Stock I, an international company, with an expected return of 6 percent and a standard deviation of 16 percent. The correlation between the two stocks is –0.01. What are the expected return and standard deviation of the minimum variance portfolio? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) Expected Return? Standard deviation?

3. Consider Table 2. Table 2 Stock Expected Return 2 12% 6% Standard Deviation 20% 10% 0.20 Correlation Coefficient (a) Consider Table 2. Compute the expected return and standard deviation of return of an equally-weighted (b) Consider Table 2. Solve for the composition, expected return and standard deviation of the minimum (c) Consider Table 2. Sketch the set of portfolios comprised of stocks 1 and 2. Be sure to include the portfolios (d) Consider Table 2. Suppose that a risk-free...

3. Consider Table 2. Table 2 Stock Expected Return 2 12% 6% Standard Deviation 20% 10% 0.20 Correlation Coefficient (a) Consider Table 2. Compute the expected return and standard deviation of return of an equally-weighted (b) Consider Table 2. Solve for the composition, expected return and standard deviation of the minimum (c) Consider Table 2. Sketch the set of portfolios comprised of stocks 1 and 2. Be sure to include the portfolios (d) Consider Table 2. Suppose that a risk-free...

3. Consider Table 3 Table 3 Stock Expected Return 10% 5% Standard Deviation 12% 8% Correlation Coefficient 0.40 (a) Consider Table 3. Compute the expected return and standard deviation of return of an equally-weighted portfolio of stocks A and B (b) Consider Table 3. Solve for the composition, expected return and standard deviation of the minimum variance portfolio (c) Consider Table 3. Sketch the set of portfolios comprised of stocks A and B (d) Consider Table 3. Suppose that a...

3. Consider Table 3 Table 3 Stock Expected Return 10% 5% Standard Deviation 12% 8% Correlation Coefficient 0.40 (a) Consider Table 3. Compute the expected return and standard deviation of return of an equally-weighted portfolio of stocks A and B (b) Consider Table 3. Solve for the composition, expected return and standard deviation of the minimum variance portfolio (c) Consider Table 3. Sketch the set of portfolios comprised of stocks A and B (d) Consider Table 3. Suppose that a...

Pinulo retums? 1 0 capital asset pricing model given historical data 2. Consider Table 1. (%) 3.77 Table 1 Summary Statistics Alpha, Beta, Expected Return and Variance a/c to the Stocks Sample Single Index Model Covariance Residual and Return Alpha Beta with Market Expected Variance Variance Market (%) (%) Return (%) (%) 3.60 3.59 4.80 Market 4.20 0.00 8.70 (a) Consider Table 1. Using the single index model, calculate beta and alpha for stocks 1 and 2. Interpret your findings....

Pinulo retums? 1 0 capital asset pricing model given historical data 2. Consider Table 1. (%) 3.77 Table 1 Summary Statistics Alpha, Beta, Expected Return and Variance a/c to the Stocks Sample Single Index Model Covariance Residual and Return Alpha Beta with Market Expected Variance Variance Market (%) (%) Return (%) (%) 3.60 3.59 4.80 Market 4.20 0.00 8.70 (a) Consider Table 1. Using the single index model, calculate beta and alpha for stocks 1 and 2. Interpret your findings....

2. Consider the information in Table1. Table 1 Standard Deviation of Stock Stock Correlation with Market Portfolio 0.75 0.20 Stock 20% 15% 14% 0% 49% ected Market Return Risk Free Rate Return (a) Consider Table 1 . Calculate betas for Stock 1, Stock 2, and a portfolio consisting of 75% invested in Stock 1 and (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for Stock 1, Stock 2, and the (c) Consider Table 1 and...

2. Consider the information in Table1. Table 1 Standard Deviation of Stock Stock Correlation with Market Portfolio 0.75 0.20 Stock 20% 15% 14% 0% 49% ected Market Return Risk Free Rate Return (a) Consider Table 1 . Calculate betas for Stock 1, Stock 2, and a portfolio consisting of 75% invested in Stock 1 and (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for Stock 1, Stock 2, and the (c) Consider Table 1 and...

6. Consider the following information for Stocks 1 and 2: Expected Standard Stock Return Deviation 1 20% 40% 2 12% 20% NE a. The correlation between the returns of these two stocks is 0.3. How will you divide your money between Stocks 1 and 2 if your aim is to achieve a portfolio with an expected return of 18% p.a.? That is, what are the weights assigned to each stock? Also take note of the risk (i.e., standard deviation) of...

6. Consider the following information for Stocks 1 and 2: Expected Standard Stock Return Deviation 1 20% 40% 2 12% 20% NE a. The correlation between the returns of these two stocks is 0.3. How will you divide your money between Stocks 1 and 2 if your aim is to achieve a portfolio with an expected return of 18% p.a.? That is, what are the weights assigned to each stock? Also take note of the risk (i.e., standard deviation) of...

Part D and E please

2. Consider the information in Table 1. Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio Risk-free asset 5% 12% 8% 0% 16% 2% 0 (a) Consider Table 1. Calculate betas for stock I and stock 2 (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2 (c) Consider Table 1 and the equilibrium expected returns...

Part D and E please

2. Consider the information in Table 1. Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio Risk-free asset 5% 12% 8% 0% 16% 2% 0 (a) Consider Table 1. Calculate betas for stock I and stock 2 (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2 (c) Consider Table 1 and the equilibrium expected returns...

Q2

(e) Assume for simplicity sake that one factor has been deemed appropriate to "explain" returns on stocds (0) How and there is no idiosyncratic risk. Derive the arbitrage pricing theory would you perform a test of the predictions of the capital asset pricing model given historical data (APT) model 2. Consider Tablo 1 Return and Variance a/c to the Stocks Sample Covariance Residual AlphaBeta Expected Variance and Return | with Market | Variance | (96) Return Market 3.60 4.80...

Q2

(e) Assume for simplicity sake that one factor has been deemed appropriate to "explain" returns on stocds (0) How and there is no idiosyncratic risk. Derive the arbitrage pricing theory would you perform a test of the predictions of the capital asset pricing model given historical data (APT) model 2. Consider Tablo 1 Return and Variance a/c to the Stocks Sample Covariance Residual AlphaBeta Expected Variance and Return | with Market | Variance | (96) Return Market 3.60 4.80...

I would like part d and e answered please

2. Consider the information in Table 1 Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio 6% 12% 8% 0% 16% 2% Risk-free asset 0 (a) Consider Table 1. Calculate betas for stock 1 and stock 2. (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2. (c) Consider Table 1 and...

I would like part d and e answered please

2. Consider the information in Table 1 Table 1 Correlation with market portfolio 0.20 0.80 1.00 0.00 Standard deviation Return Beta Stock 1 Stock 2 Market portfolio 6% 12% 8% 0% 16% 2% Risk-free asset 0 (a) Consider Table 1. Calculate betas for stock 1 and stock 2. (b) Consider Table 1. Compute the equilibrium expected return according to the CAPM for stocks 1 and 2. (c) Consider Table 1 and...

Most questions answered within 3 hours.

-

The escape speed from the Earth is 1.12×104m/s, so that a gas

molecule travelling away from...

asked 4 minutes ago -

Explain why the numerical value of the density of a substance will

vary with the units...

asked 9 minutes ago -

Country Able and Country Baker initially have the same real GDP

per capita. Country Able experiences...

asked 6 minutes ago -

In

a student laboratory exercise, the wavelength of a 48,300 Hz

ultrasound wave is measured to...

asked 12 minutes ago -

This model: Yi=β1+β2log(Xi2)+β3log(Xi3)+ei is

Select one:

a. Log – Log model b. Log - Linear model...

asked 23 minutes ago -

Decide whether the two sequences of operations will give the

same results.

Squaring a number, then...

asked 38 minutes ago -

What volume of 0.72 M barium chloride, BaCl2,

contains 0.065 mol of chloride ions?

asked 22 minutes ago -

explain why most marketers avoid deceptive practices

asked 22 minutes ago -

In the movie You've Got Mail, what key concepts of gendered

communication could be related to...

asked 1 hour ago -

A 12.87-g block of solid iron

at 68.39 °C is immersed in a

21.10-g pool of...

asked 55 minutes ago -

What is happening molecularly that causes primers to not bind as

well at high temperatures?

asked 57 minutes ago -

Consider a simple macro model with a constant price level and

demand-determined output. The equations of...

asked 38 minutes ago