Homework Answers

For any query or clarification, please leave a comment.

Add Answer to:

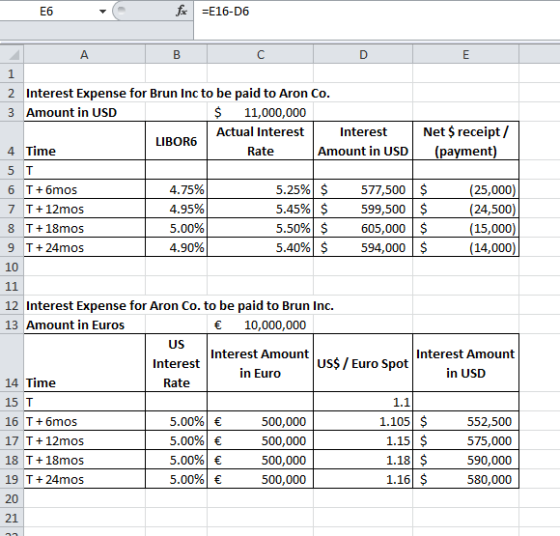

1. Aron Company enters into a 2-year US$ / Euro swap with Brun Inc. on a...

A US company enters into a currency swap in which pays a fixed rate of 5.5%...

A US company enters into a currency swap in which pays a fixed rate of 5.5% in euros and the counterparty pays a fixed rate of 6.75% in dollars. The notional principals are $100 million and €116.5 million. Payments are made semi-annually and on the basis of 30 days per month and 360 days per year. Calculate the final exchange of payments that the US company receives from its counterparty. [Note: let us assume the last semi-annual payment is included...

A US company has entered into an interest rate swap with a dealer in which the...

A US company has entered into an interest rate swap with a dealer in which the notional principal is $50 million. The company will pay a floating rate of LIBOR and receive a fixed rate of 5.75%. Interest is paid semi-annually, and the current LIBOR=5.15%. What is the total amount that the asset manager will pay to (or receive from) the dealer? [Note: You should use a positive number to represents the amount the asset manager pay to the dealer....

Module 9 – Foreign Exchange Rate Risk Homework Exercise Part 1 1. Suppose that the EUR:USD...

Module 9 – Foreign Exchange Rate Risk Homework Exercise Part 1 1. Suppose that the EUR:USD is trading at 1.3342; the GBP:JPY is trading at 67.7600; and the EUR:GBP is trading at 0.8165. What should the USD:JPY rate be? 2. If a price index for US goods stands at 118.93 and the same price index for European goods (i.e., computed from the same consumption basket) stands at 183.34; what is the fair (under the theory of PPP) spot exchange rate...

Most questions answered within 3 hours.

-

What are John’s potential claims if he is terminated

this week?

John is a 54-year-old man...

asked 2 minutes ago -

A (8.5) cm tall object is placed at a distance of (14.2) cm from

a convex...

asked 11 minutes ago -

(2) For the following questions, consider a data set that

exhibits a normal distribution. Report the...

asked 12 minutes ago -

What exactly is an information system? How does it work" What

are its people organization,

...

asked 13 minutes ago -

The Food Marketing Institute shows that 17% of households spend

more than $100 per week on...

asked 23 minutes ago -

Go to NCBI BLAST search web page

1st search: GEKDLRRAKDINQEVYNF

2nd search: PTSQRLQLLEPFDK

3rd search: GEKDLRRAKDINQEVYNF...

asked 26 minutes ago -

Explain how each of the following three conditions could be a

red flag for a register...

asked 31 minutes ago -

In a two-way factorial ANOVA, the final F-ratio for

factor AxB is determined by dividing _____...

asked 1 hour ago -

Show your solutions for answer.

4. An aqueous solution contains 9.21 g of

K4Fe(CN)6 in a...

asked 31 minutes ago -

The random variable X has a uniform distribution with values

between 16 and 18. What is...

asked 41 minutes ago -

Evaluate each of the following transactions in terms of their

effect on assets, liabilities, and equity....

asked 40 minutes ago -

The amounts of nicotine in a certain brand of cigarette are

normally distributed with a mean...

asked 1 hour ago